Author: Nancy, PANews

Science fiction writer Hao Jingfang depicted a future city in "Beijing Folding" that is divided into three spaces by class, where people in different spaces enjoy vastly different time and resources. Today, this metaphor is playing out as a harsh reality in the Ethereum L2 world.

With the surge of Layer 2 chains, there is an oversupply, and the market may not need so many L2s. Over the past few years, from crypto-native institutions and various protocols to traditional giants, many have bet on Ethereum L2, making it a popular strategy for brand upgrades. On the surface, this appears to be a thriving new battlefield, but in reality, only a few chains are truly sharing the "cake," while most L2s quietly slide towards silent extinction.

A Few L2s Support the Ecosystem, Over a Hundred Chains Fall Silent

The trend of differentiation among Ethereum L2s is happening faster and more brutally than many industry practitioners anticipated.

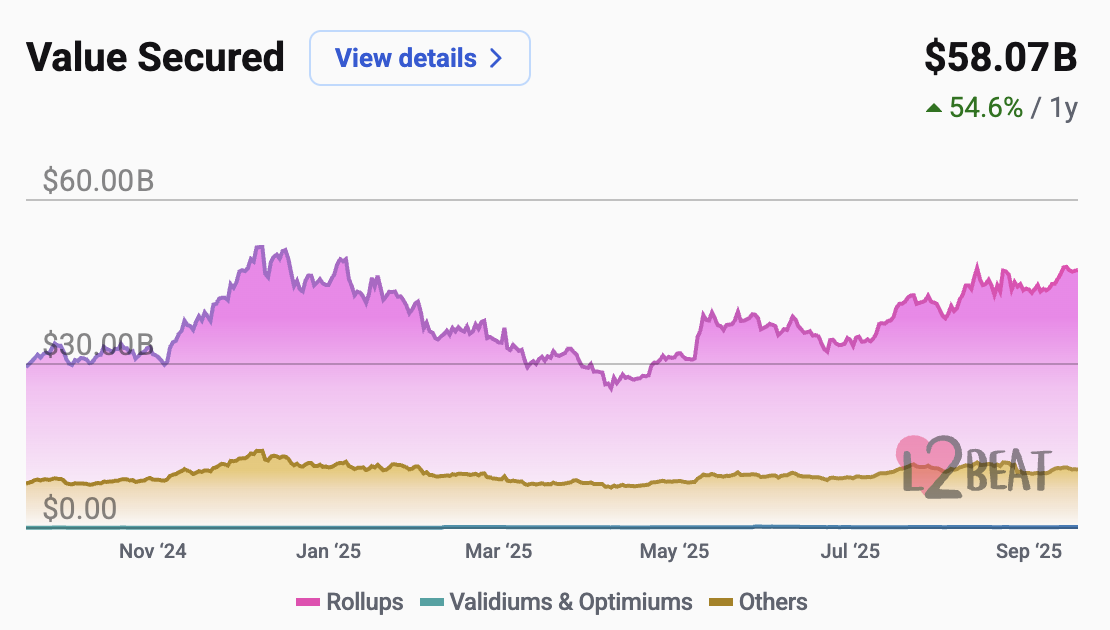

According to data from L2BEAT, as of September 17, the TVL of Ethereum L2 exceeded $58 billion, growing by 54.6% over the past year. It looks impressive, but when broken down, it reveals a different, imbalanced picture.

Among over 160 L2s, only 8 have a TVL exceeding $1 billion, almost occupying half of the entire market; 17 have a TVL between $100 million and $1 billion, still showing some activity; another 35 are in the tens of millions, barely maintaining a presence; while over 100 chains have a TVL below $1 million, with activity close to zero, becoming true "ghost chains."

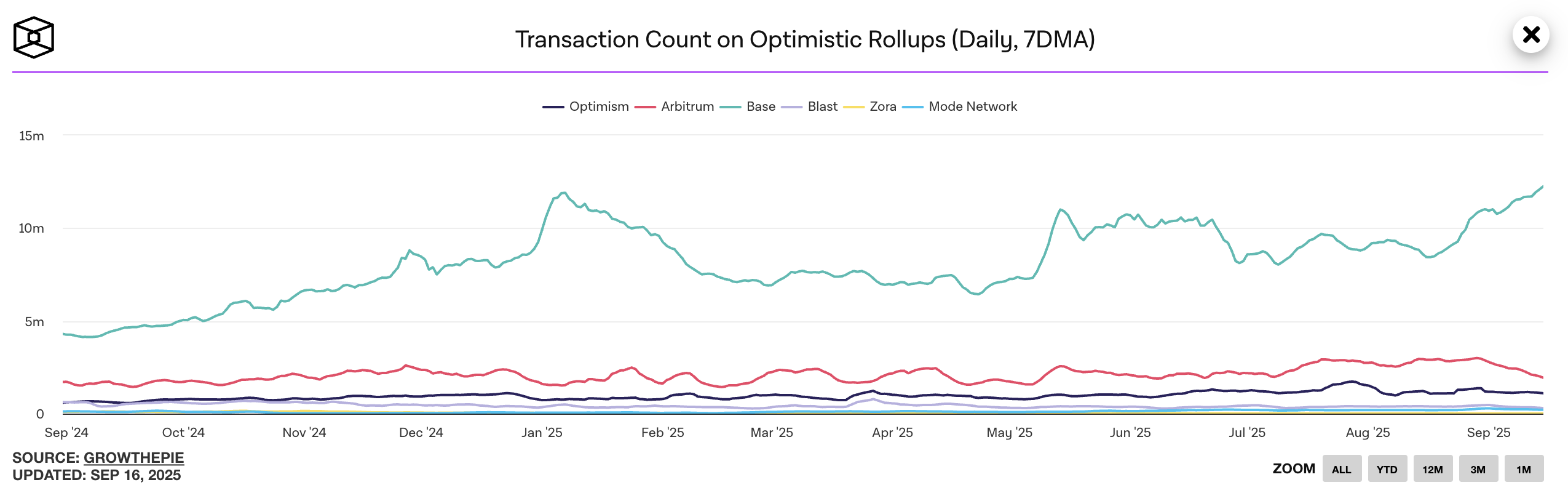

Transaction activity more intuitively reveals the gap. Data from The Block shows that as of September 15, in the Optimism Rollups camp, Base's seven-day average transaction count reached 12.26 million, far exceeding Arbitrum's 1.93 million and Optimism's 1.1 million, while L2s like Blast and Mode had only tens of thousands of transactions. The situation in the ZK Rollups ecosystem is also not optimistic, with most L2s, including Linea, Starknet, Scroll, and zkSync, having only tens or even hundreds of transactions.

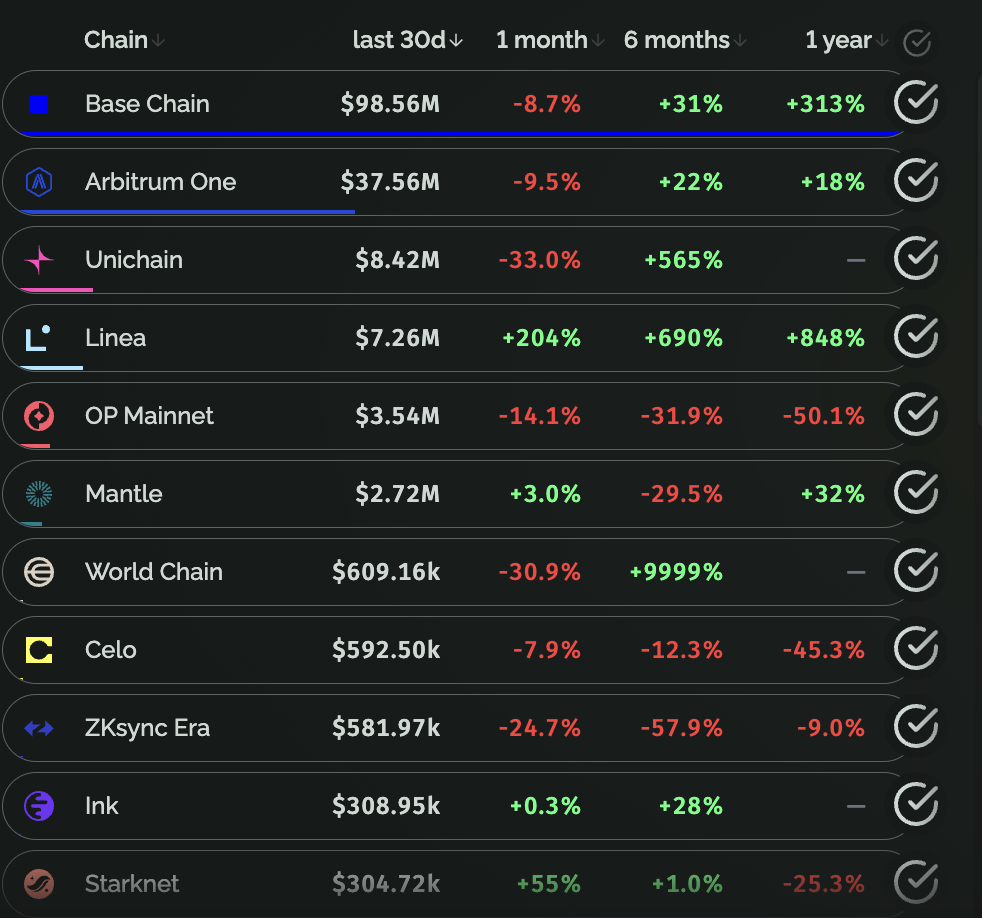

User activity differences are also very significant. Data from Growthepie shows that in the past 30 days, Base has maintained the top position with over 19.78 million active interaction addresses; in contrast, Arbitrum One has only 3.71 million, OP Mainnet 1.53 million, Linea 1.36 million, and some chains have only a few thousand active addresses. Revenue distribution is equally extreme, with Base's monthly revenue nearing $100 million, Arbitrum One reaching the tens of millions, while most other L2s earn only thousands to tens of thousands of dollars, hardly covering operational costs.

Some L2s have directly declared failure; Scroll DAO recently announced the suspension of its governance process, with the entire leadership team resigning and redesigning the governance structure, but it has not clarified whether to withdraw existing proposals; Kroma has decided to shut down its existing L2 network to focus on new directions. Some projects are still "surviving," with the founder of an L2 public chain lamenting to PANews that they are now taking on outsourced work to support their team. Whatever they do now seems futile; they can only survive and wait for the wind to come.

This polarization has led ecosystem projects to ponder whether most L2s truly have value. For instance, recently, Aave proposed shutting down underperforming L2s, while the Curve community suggested halting all new L2 network integrations.

Resource Determines Victory, Centralization Concerns Emerge

In recent months, several L2 projects have been active, with both technological innovations and ecosystem expansions.

For example, Coinbase recently launched the "Universal App" Base App, which will fully operate on the Base network and is about to open invitation features. Subsequently, Base also stated that it is exploring the possibility of issuing a network-native token, but it cannot yet provide a specific timeline, design plan, or governance details. Other L2 projects that have recently issued tokens include Kraken's L2 network Ink and Linea.

Arbitrum has partnered with Robinhood to target tokenized stock products and launched token incentives and subsidy programs to promote ecosystem development; Optimism's OP Stack has been adopted by several institutions such as Upbit, GIWA, Clearpool, and cLabs as an L2 solution, providing fast verifiable transaction ordering; Starknet approved the v0.14.0 version proposal, taking an important step towards decentralized ordering, and recently launched BTC staking integration upgrades; zkSync has introduced the institutional private blockchain infrastructure Prividium and released a new type of zero-knowledge prover "Airbender" based on RISC-V.

At the same time, under the internal competition of L2s, some projects have chosen to adjust their strategies or reposition themselves. The Movement network announced its transformation into a Layer 1 blockchain, supporting native token staking and the Move 2.0 protocol, but who says the L1 battlefield is easier than L2?

In fact, behind the intensifying competition among Ethereum L2s, more and more traditional and crypto institutions are inclined to issue their own L2s. Compared to relying on existing L2s, building their own chains not only reduces operational costs and meets regulatory requirements but also captures more potential profits.

Strong resource support is also providing L2s with greater competitive space. For instance, the highest-earning Base is backed by Coinbase, the largest compliant exchange in the U.S., providing strong support for its ecosystem and user growth; Mantle recently formed a deep partnership with mainstream crypto exchange Bybit, showcasing the advantage of "a big tree provides shade." Additionally, institutions like JPMorgan, Robinhood, Sony, and Upbit, when laying out L2s, already possess rich business resources and a large user flow, giving them an advantage in market competition compared to new chains starting from scratch. In contrast, L2s lacking resources, even if they attempt to gain bargaining power, may struggle to sustain development due to insufficient liquidity and market fragmentation.

However, this trend has also intensified market concerns about the centralization of L2 networks. In particular, recent outages have occurred in L2s such as Base, Linea, and Starknet, highlighting the potential risks posed by centralized orderers. In response, SEC Commissioner Peirce recently warned that a matching engine controlled by a single entity resembles an exchange, and L2s with centralized orderers may face exchange registration requirements.

This statement serves as a wake-up call to the market: in the pursuit of efficiency and scale, L2s must not sacrifice decentralization.

Today’s L2 arena is no longer just a technical competition; it is a comprehensive contest of ecosystems, resources, and governance models. Those chains without stories, users, or resources may ultimately fade into silence or quietly wait for the wind to come.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。