Written by: Gui Ruofei, Cheryl, Queenie

"Having shed the shadow of the SEC lawsuit, Ripple is continuing its journey into the payment sector it has been laying the groundwork for over the years amidst controversy. The construction of compliance directions such as cross-jurisdictional regulation and disclosure obligations still constitutes the underlying constraints on Ripple's operations and financing. Under these constraints, Ripple's 'payment (flow) - custody (assets) - stablecoin (settlement)' flywheel is gradually opening up."

On August 7, 2025, the SEC officially announced the joint withdrawal of the appeal with Ripple and two executives, confirming that the final judgment and relief arrangements remain valid. After nearly five years, this significant regulatory marathon has finally come to a close. This judgment fundamentally changes the compliance path for Ripple's issuance and operation of XRP, while also establishing a new standard for determining the securities nature of cryptocurrencies. Meanwhile, over the past five years, the entire XRP ecosystem has been continuously developing and evolving, preparing to make a significant impact in the new cycle. This article will delve into the details of the Ripple and SEC lawsuit and provide a detailed analysis of the XRP token and its vast ecosystem.

1. What are the key details worth noting in the Ripple vs SEC lawsuit?

(1) Detailed Overview of the Lawsuit Process and Timeline

To thoroughly analyze the tug-of-war between Ripple and the SEC, it is necessary to first outline the timeline of the lawsuit's development and major progress.

On December 22, 2020, the U.S. Securities and Exchange Commission (SEC) sued Ripple and two executives in the Southern District of New York (SDNY), accusing them of raising over $1.3 billion through the unregistered issuance of digital asset securities, seeking injunctions, disgorgement, and civil penalties.

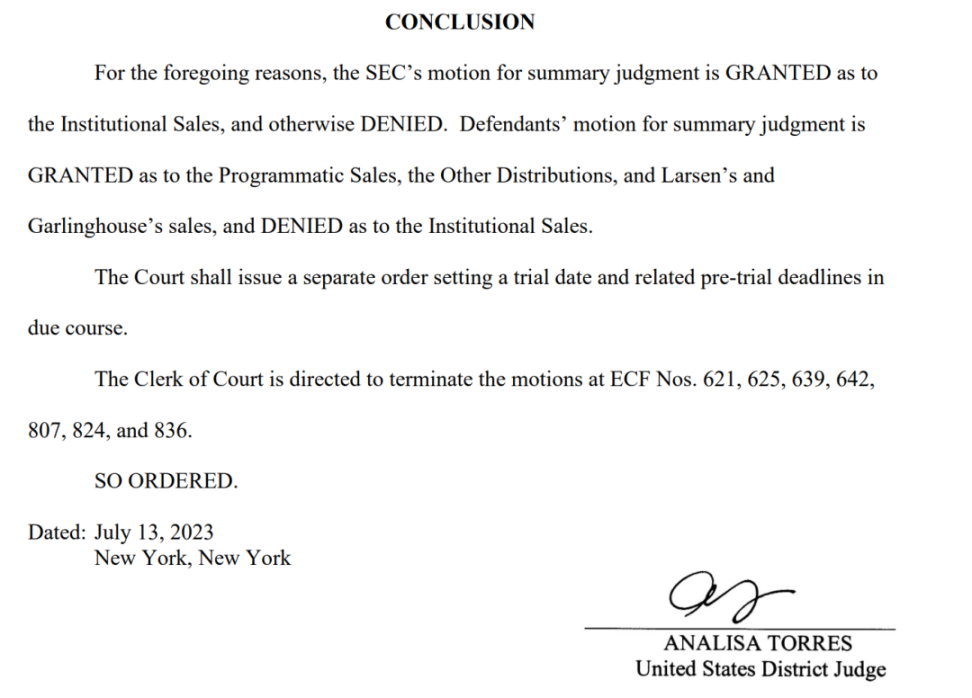

On July 13, 2023, Judge Analisa Torres issued a partial summary judgment:

For "Institutional Sales" of XRP, the court found that under existing facts and contractual arrangements, it met the investment contract standard in the Howey test;

For "Programmatic Sales" of XRP, the court determined that the SEC failed to prove that the retail buyers in the unspecified trading counterparties had reliance on Ripple's management efforts and profit expectations;

For XRP distributed through "Other Distributions," the court found a lack of the element of "investment of money," meaning it did not constitute an investment contract.

(The above image shows the final conclusions of the summary judgment in July 2023)

On October 3, 2023, the court denied the SEC's request to appeal the favorable rulings for Ripple. On October 19, 2023, the SEC voluntarily withdrew its remaining claims against the two executives, thus avoiding a scheduled jury trial.

Entering the relief phase, on August 7, 2024, the court issued a final judgment and permanent injunction:

The judgment does not order the disgorgement of XRP nor the calculation of interest;

Imposed a civil penalty of approximately $125 million;

Imposed a permanent injunction on institutional sales of XRP.

At the same time, the court rejected both parties' request for a "summary judgment" to settle for a lower amount in June 2025.

This protracted tug-of-war has finally come to a close. On August 7, 2025, the SEC announced the joint withdrawal of the appeal with Ripple and two executives, confirming that the final judgment and relief arrangements remain valid.

(2) What is the core dispute in the SEC vs Ripple lawsuit?

The core of the dispute in this case cannot simply be understood as "whether XRP is a security," but rather whether Ripple's specific issuance/sale activities of XRP constitute an investment contract under the Securities Act.

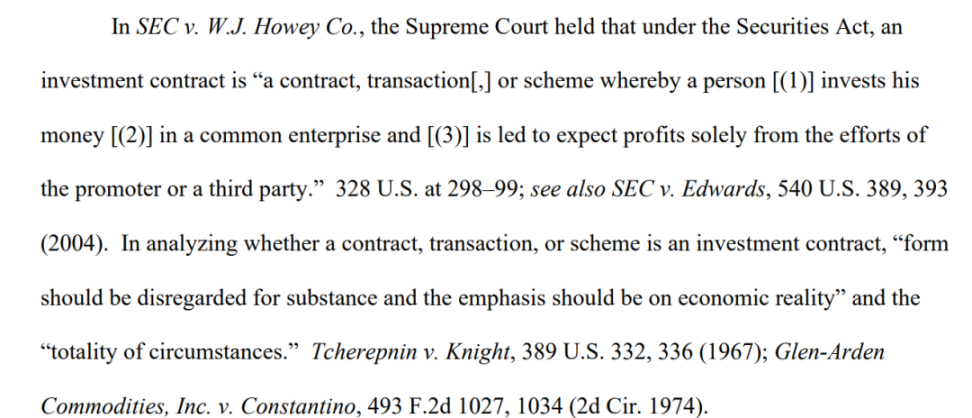

The U.S. Supreme Court's ruling in the Howey case provides a classic definition of "investment contract": "A contract, transaction, or scheme in which a person invests money in a common enterprise and expects to derive profits primarily from the efforts of others."

This standard can be elaborated into the following four elements:

Investment of money (an investment of money);

Common enterprise (in a common enterprise);

Reasonable expectation of profits derived from the efforts of others (with a reasonable expectation of profits to be derived from the efforts of others);

The profit acquisition is entirely or primarily dependent on the managerial or entrepreneurial efforts of the promoter or a third party (derived solely from the managerial or entrepreneurial efforts of the promoter or a third party).

(The above image provides a detailed analysis of the Howey test in the summary judgment of July 2023)

Within the framework of the SEC's accusations, Ripple's institutional sales of XRP were accompanied by negotiations, information communication, and contractual commitments directed at institutions. The court thus determined that these institutional buyers had a more apparent profit expectation and attribution to Ripple's management efforts, meeting the investment contract standards in the Howey test;

Conversely, XRP's programmatic trading essentially refers to secondary trading occurring in the public market through a central counterparty matching mechanism, making it difficult for the SEC to prove that these buyers had a reasonable profit expectation that could be recognized by the court. Therefore, the Southern District Court of New York determined that the SEC's evidence for such transactions was insufficient;

As for XRP in other distribution channels, this portion of XRP is primarily used for Ripple's employee incentives or ecosystem subsidies. Moreover, holders of this XRP typically did not pay corresponding consideration when acquiring it. Therefore, these buyers lack the core element of "investment of money," and thus do not trigger the Howey test.

In summary, the court made a fine distinction regarding XRP based on the type of behavior. The same token can yield entirely different conclusions under securities law depending on the trading context, which is precisely the reference value of this case's judgment.

(3) What impact will this lawsuit have on Ripple and the XRP ecosystem?

For Ripple, this lawsuit has forcibly delineated the boundaries of Ripple's compliance and business. Financing and distributing XRP to institutions or targeted investors must comply with the securities issuance compliance framework or fully meet exemption conditions. While the risks in the market circulation of XRP have not been completely resolved, under the judgment framework of the Howey test, the SEC's regulation of it has been significantly curtailed. For the XRP ecosystem, most of the XRP circulating in the secondary market has escaped the possibility of being classified as "securities," which objectively alleviates the direct compliance risks for trading platforms and market makers. However, any scenarios involving targeted financing, over-the-counter agreements, placements, and lock-ups based on XRP still require meticulous compliance design and risk management.

More broadly, this case further alters the industry's discussion paradigm regarding the "attributes of tokens" — the applicability of securities law to cryptocurrencies should be segmented based on "trading behavior," rather than applying a one-size-fits-all approach based on "token nature." This could have long-term structural impacts on subsequent cryptocurrency token economics design (such as functional tokens, incentive distributions, ecosystem subsidies) and specific standards for information disclosure.

Overall, Ripple has achieved a key victory in the most sensitive area of secondary market circulation, but has accepted SEC regulatory requirements in the "fundraising - issuance" aspect directed at institutions.

2. How does Ripple's business empire operate and develop?

The formal end of the legal dispute not only clears the way for Ripple to expand its global market with the U.S. as a key node but also brings renewed attention from investors worldwide to this company, which has long been surrounded by controversy, and its closely associated token, XRP. Among the well-known old coins, XRP has always been a significant presence. It once created a fervent wealth myth but was also widely delisted by major exchanges; it has a large following, and every market fluctuation, big or small, tends to trigger a rally, yet it faces the most criticism for reasons including but not limited to: bubbles, centralization, lack of on-chain ecosystem, unclear value capture mechanisms, etc. Next, this article attempts to provide a preliminary introduction to Ripple's vast product system, the underlying public chain XRP Ledger (XRPL), and the native token XRP, starting from Ripple's product landscape, business model, development opportunities, and the risks it faces, to help readers gain an initial understanding of this complex project and the value logic behind it.

(1) What exactly is Ripple?

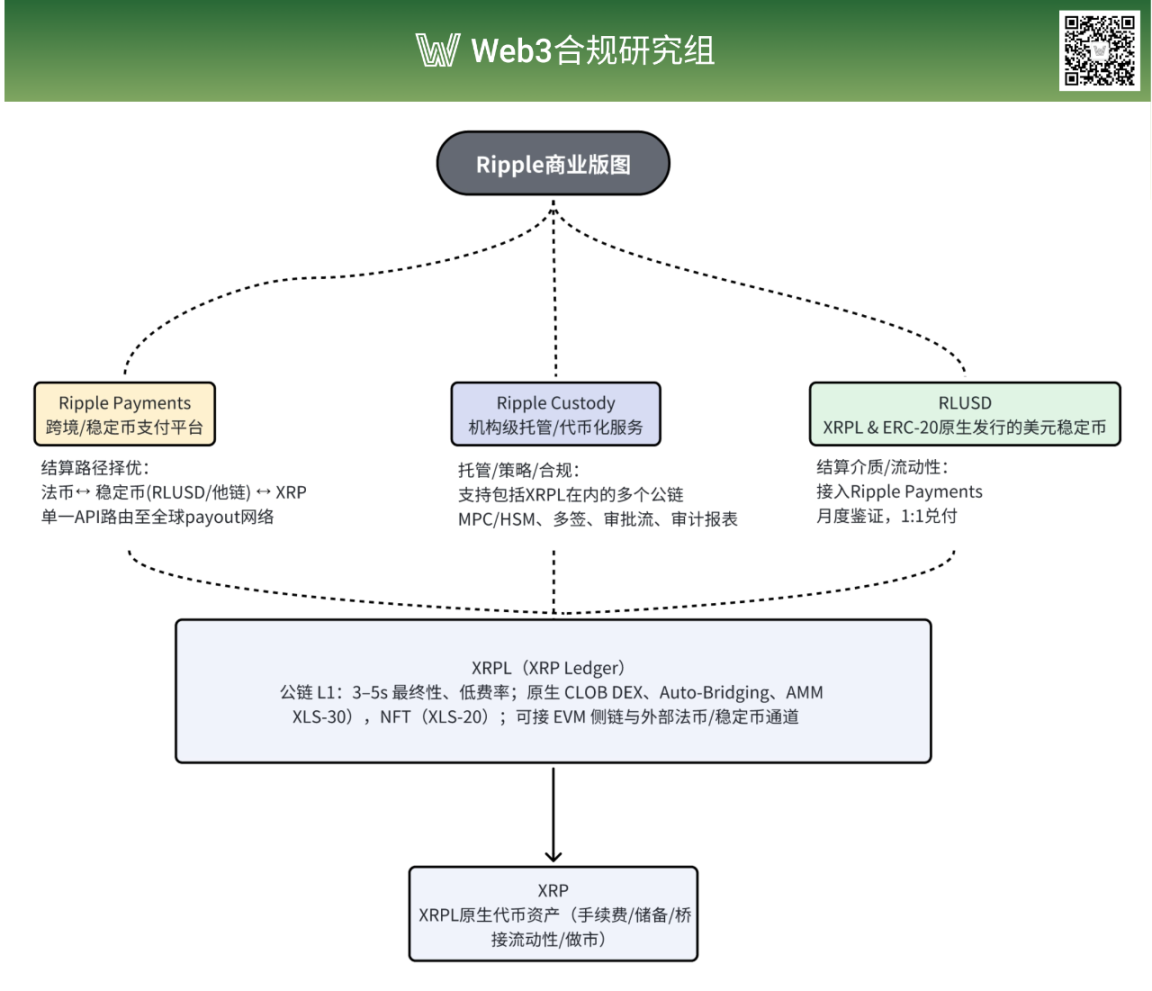

Ripple, also known as Ripple Labs, is a comprehensive financial technology company aimed at institutions, integrating cross-border payments, institutional-grade digital asset custody, stablecoin issuance, and blockchain infrastructure.

Ripple was originally founded in 2012 by developers Ryan Fugger and Jed McCaleb, aiming to establish a trust-based payment network using decentralized and efficient ledger technology. However, it was the addition of Wall Street financial elite and founder of the U.S. online lending platform E-Loan, Chris Larsen, that laid the groundwork for its commercial empire. Unlike many believers in decentralization, Larsen's background in traditional finance allowed him to see another possibility for Ripple and the broader blockchain technology. In Larsen's vision, Ripple was not a new system to replace the centralized financial system represented by banks, but rather an excellent tool to provide underlying technical support for the leapfrog upgrade of banks' cross-border payment functions. Larsen's philosophy was fiercely criticized by decentralization advocates like McCaleb at the time, but in light of the widespread application of stablecoins today and Ripple's vast payment business landscape, it appears prescient.

Today, Ripple utilizes the XRP Ledger public chain (XRPL) as its underlying technology stack, using XRP as the native liquidity and fee asset of XRPL, providing a comprehensive and systematic financial service that includes Ripple Payments for cross-border payment settlement, Ripple Custody for digital asset custody and tokenization, and the stablecoin RLUSD.

(2) Detailed Overview of Ripple's Product Landscape

1. Ripple Payments Cross-Border Payment Platform

Ripple Payments provides cross-border payment services for payment providers, banks, multinational corporations, and other institutions from around the world. The cross-border payments of Ripple Payments include three paths: fiat currency, stablecoins (including its own stablecoin RLUSD and other third-party stablecoins), and XRP. It routes in real-time based on compliance, cost, liquidity, and other factors to achieve real-time cross-border payments, with built-in KYC/AML/sanctions screening and reconciliation audit functions. Typical delivery scenarios include: B2B/platform merchant settlements, remittances, cross-border payroll disbursements, and corporate treasury dollar acquisition.

As a global payment platform, Ripple Payments currently covers over 90 markets and more than 55 currencies. In terms of compliance, Ripple Payments has obtained licenses and MTL certificates issued by 64 jurisdictions, including the U.S. and the UAE, and is applying for compliance licenses from institutions in jurisdictions such as the EU, the UK, and Singapore. Additionally, Ripple Payments has obtained international security certifications such as SOC 2 Type II and ISO 27001, and has joined the American Bankers Association (ABA) and multiple national payment industry associations, establishing a global payment trust mechanism covering data security, operational compliance, and industry collaboration, significantly enhancing its accessibility. As of June 2025, Ripple Payments has processed over $70 billion in fund settlements.

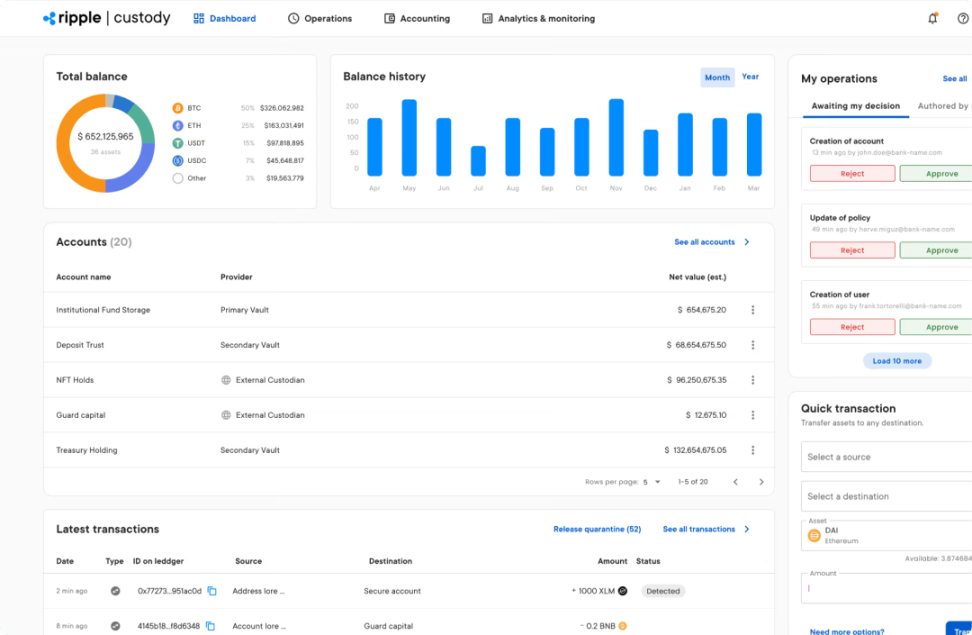

2. Ripple Custody Digital Asset Custody Solution

Ripple Custody is an institutional-grade digital asset custody solution aimed at banks, custodians, exchanges, and large enterprises. Custody is the foundation of digital asset business, providing underlying security support for institutional tokenization, stablecoin issuance, and digital asset management use cases. Ripple Custody combines features such as MPC/HSM key management, hierarchical cold and hot wallets, policy-based approvals/permissions, audit reports, and compliance modules, and can be deployed on-premises or in the cloud, offering customized custody services for institutions.

In addition to core digital asset custody functions, Ripple Custody also provides users with stablecoin issuance and management, and unified governance orchestration for corporate backends. Using Ripple Custody, institutions can mint/burn stablecoins and manage reserves on the XRP Ledger and any EVM-compatible chain, serving payment, settlement, and collateral scenarios (existing use cases include SocGen FORGE issuing EURCV on XRPL, and Korea's BDACS custody of RLUSD). Furthermore, institutions can utilize Ripple Custody to automate backend processes such as settlement, reconciliation, and reporting on-chain, connecting public/private chains with core banking systems, and meeting regulatory and internal control requirements through configurable policies and approval workflows. Through these functional designs, it is evident that Ripple Custody aims not to be a single digital custody service provider but to create a one-stop digital asset operation platform covering the entire lifecycle of corporate tokenization and payments.

The ability to provide this integrated service comes from Ripple's collaboration with several established brokers with extensive custody experience. By acquiring Swiss custody technology provider Metaco, which serves well-known institutions such as HSBC, Citibank, BNP Paribas, and SocGen FORGE, and Standard Custody & Trust (SCTC), which holds a NYDFS trust license, Ripple not only introduced bank-grade custody and tokenization technology capabilities but also strengthened its product's compliance qualifications in various markets, including the U.S. Currently, Ripple Custody has obtained FIPS 140-2 Level 4 certification, compliant with SOC 2 Type II and ISO 27001 standards. In April of this year, Ripple announced the acquisition of Hidden Road for $1.25 billion, marking one of the largest acquisitions in the cryptocurrency industry. This large-scale acquisition will make Ripple the first cryptocurrency company to own and operate a global multi-asset prime broker, and the acquisition is still awaiting regulatory approval and closing processes.

3. RLUSD Stablecoin

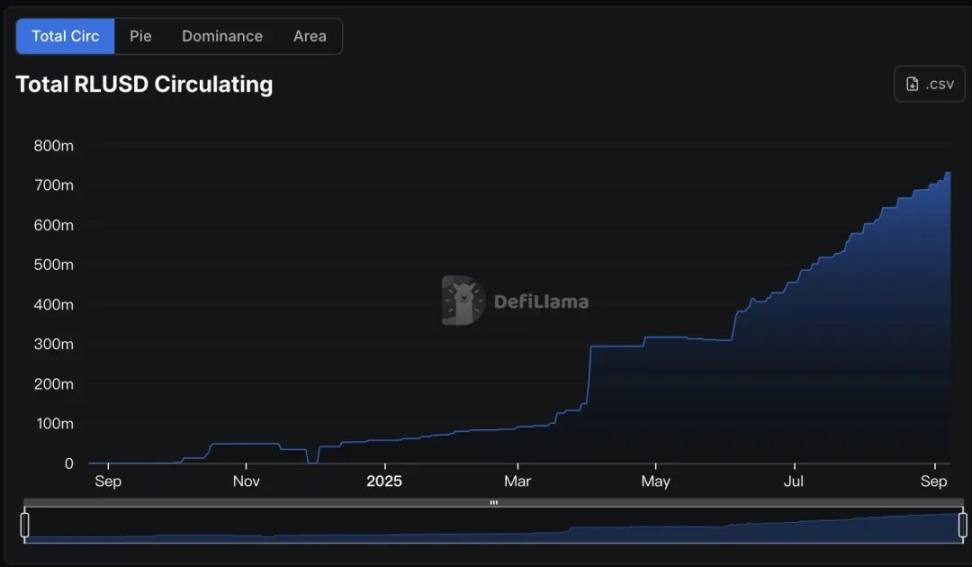

RLUSD is a dollar stablecoin issued natively on the XRPL and ERC-20 dual chains by the regulated entity SCTC under a limited trust license in New York: it promises 1:1 redemption, reserves held in cash and equivalents, and is verified monthly. Currently, RLUSD has been integrated into Ripple Payments and connects with several deposit and withdrawal platforms and global trading platforms, including Kraken, Gemini, Bitget, BitMEX, and Alchemy Pay. As of September 9, RLUSD has issued and circulated over $730 million.

(3) Ripple's Technology Stack: XRP Ledger and Its Native Currency XRP

As the technical foundation of Ripple's products, the XRP Ledger (XRPL) public chain has been optimized for financial scenarios since its design:

It can process over 1,000 transactions per second, with blocks closing in about 3–5 seconds, eliminating long-tail waiting for "block rollbacks," making the time for funds to arrive more predictable;

Transaction fees are extremely low (baseline 10 drops = 0.00001 XRP, adjusted elastically with load and burned to combat spam), suitable for high-frequency, small-amount transactions; it does not spike like bidding Gas;

Protocol upgrades require support from >80% of trusted validators for two consecutive weeks to activate, combined with a Negative UNL, meaning that "change management and fault tolerance" are written into the protocol layer, reducing the risk of forks/rollbacks and enhancing the predictability of SLA and compliance launches.

The low-cost, high-efficiency, and controllable characteristics of XRPL make it naturally suitable as the technical foundation for all of Ripple's products.

In Ripple Payments, XRPL can handle a large volume of transaction settlement needs with approximately 3–5 seconds of deterministic settlement and extremely low, predictable fees, and through built-in DEX/AMM + Auto-Bridging, it can automatically optimize routing between fiat IOUs, stablecoins (including RLUSD/USDC on XRPL), and XRP, completing "currency exchange + transfer" in one go;

On the RLUSD side, the RLUSD stablecoin is natively issued on the XRPL chain, allowing direct participation in ledger-level trading pairs and liquidity pools, serving as a stable settlement medium for Payments;

On the Ripple Custody side, XRPL's multi-signature, account/object reserves, Escrow/Checks, authorizations, and freezes (IOU level) provide native control primitives that offer programmable governance and reconciliation paths for institutional custody, tokenization, and compliance auditing.

In addition to the mainnet, in June of this year, XRPL also launched the XRPL EVM Sidechain, which runs in parallel with the mainnet and is fully compatible with Ethereum. This aims to bring EVM smart contract capabilities into the XRPL ecosystem while achieving value interoperability with the Ethereum mainnet through bridging. As a result, complex business logic can be supported on the sidechain, while the XRPL mainnet focuses on low-latency clearing and settlement, thus closing the loop of "Payments (traffic) × Stablecoins (settlement) × Custody (governance)" within the same technology stack. This initiative also further fills the long-standing gap in on-chain use cases for XRP. Although the XRPL EVM sidechain is still in its early stages, with overall user scale, liquidity depth, and protocol maturity yet to be validated, as of September 9, the sidechain has attracted over 30 dApps for development.

XRP is the native asset of XRPL, generated entirely at the genesis of the XRPL network, with a total supply cap of 100 billion, and cannot be reissued; XRP is used to pay network fees on XRPL (which are burned to combat spam), as collateral for account and ledger object reserves, and acts as bridging liquidity in the built-in DEX/AMM and path optimization (Auto-Bridging) on XRPL, completing "currency exchange + transfer" in a single transaction for different tokens or fiat gateway assets. It can also be used on the XRPL EVM Sidechain to pay for contract execution fees, connecting to a more general EVM application ecosystem. However, it is important to note that XRP ≠ Ripple equity, and does not entitle holders to a share of Ripple's profits or the interest spread from RLUSD reserves; its value is more dependent on the actual usage of XRPL (payments/exchanges/market making), liquidity and supply arrangements (fee burning, reserves, custody releases), as well as macro risk preferences and other factors.

(4) Market and Competition Facing Ripple

Unlike the internal communication of other crypto projects, Ripple has set its sights from the beginning on the much larger cross-border settlement market outside the crypto market. According to a report by the International Monetary Fund, the global cross-border payment market is expected to reach $100 trillion by 2024, while cross-border payment transactions settled using cryptocurrencies such as USDT, USDC, BTC, and ETH account for only $2.5 trillion. This indicates that cryptocurrency settlement is still in its early stages, with many issues yet to be resolved: first, there are significant differences in cross-jurisdiction licensing/KYC/AML and the execution of the "travel rule," leading to uncertain compliance availability, making it difficult for banks and large enterprises to launch globally in a unified manner; second, last-mile (fiat deposit and withdrawal, recipient-side account and refund processing) remains a bottleneck, as many local clearing and reconciliation processes in corridors are not connected; third, on-chain liquidity and market-making depth are primarily concentrated in a few coins and platforms, making it difficult to continuously cover large, low-slippage demands for mainstream currencies such as the dollar, euro, pound, and yen; fourth, enterprise-level internal control and accounting audits (multi-signature, separation of duties, accounting and tax processing, audit trails) are more mature in traditional stacks, while on-chain and stablecoin stacks still need time to adapt. Meanwhile, traditional cross-border payment systems are also continuously accelerating and reducing friction (SWIFT gpi/ISO 20022, interconnection of various countries' instant payment systems, etc.), raising the "availability baseline." Most institutions prefer to treat cryptocurrencies/stablecoins as a supplementary path rather than the primary one.

Ripple CEO Brad Garlinghouse stated at the 2025 Singapore APEX Summit that XRP is expected to replace 14% of SWIFT system settlement volume within the next five years. As the world's primary transaction settlement network, SWIFT handles transaction settlements that are tens or even hundreds of times greater than the total volume of cryptocurrency settlements. Even if we limit 14% of SWIFT system business volume to $20 trillion, for cryptocurrency payments represented by Ripple to replace this portion of settlement volume, they would need to achieve a compound growth rate of over 51%, which presents a highly challenging growth curve. Therefore, Ripple's expectations for development resemble a "visionary goal." Before competing for market share with traditional payment systems like SWIFT, Ripple still needs to address a series of preliminary issues such as compliance licensing, deposit and withdrawal channels, and liquidity depth.

For Ripple, a more realistic growth path is to achieve segment breakthroughs in specific corridors/specific customer groups (crypto-native enterprises, platform economies, and emerging markets with underdeveloped traditional financial settlements) while running parallel to traditional tracks; as compliance (especially in the U.S./EU) and stablecoin governance become clearer, and custody and market-making depth improve, it can gradually expand its penetration. A significant characteristic of the cross-border payment market is that these payments often cannot bypass regions with mature financial systems, such as the U.S., EU, and UK, where regulatory frameworks are well-established and compliance is challenging. Especially for Ripple, which primarily serves institutions, compliance construction in major jurisdictions around the world will inevitably become the first issue it needs to address.

(5) What is Ripple's Moat? Compliance, Public Sector Endorsement, and Capital Accumulation

Compliance construction is not only the first issue Ripple needs to address but also an important opportunity for Ripple to seize market opportunities in the cryptocurrency cross-border payment field and establish a product moat. As of April 2025, Ripple has obtained over 55 remittance licenses (MTL) globally, covering 33 states in the U.S. and places like Dubai. Its company and subsidiaries have obtained the MAS Major Payment Institution (MPI) license in Singapore, completed VASP registration in Ireland, and received DFSA permission in the Dubai International Financial Centre (DIFC); meanwhile, its own stablecoin RLUSD is issued by a NYDFS-regulated trust entity, implementing 100% cash and equivalent reserves + monthly verification, and has been recognized by the DFSA as a Recognised Crypto Token, with reserves held by BNY Mellon, forming a closed loop of "regulatory framework—transparent reserves—first-line custodians," significantly reducing entry friction and compliance uncertainty for corporate clients.

What truly enables Ripple's compliance to be effective is its active efforts to engage the public sector and absorb the potential of other crypto assets. For Ripple, compliance is merely a ticket to enter the global cross-border payment market. How to expand usage channels and gain the trust of global institutions, which is costly, difficult to obtain, and extremely scarce, may be the biggest challenge Ripple needs to address in its current and future development. At this stage, Ripple's answer is to promote government-enterprise cooperation, introducing public sector projects to provide intangible endorsements for its products. Ripple provides institutional-grade custody for the Dubai Land Department's (DLD) real estate tokenization project through Ctrl Alt, and serves as a support platform for public sector CBDC projects in countries like Georgia, Bhutan, and Palau. Additionally, Ripple has integrated mainstream stablecoins into XRPL (including the native launch of USDC), forming a deeper stablecoin liquidity pool alongside RLUSD, enhancing the accessibility and success rate of cross-border settlement paths; externally, Ripple Payments connects a single API to a network of over 90 markets and 55+ currencies, accommodating real traffic from banks, PSPs, and crypto enterprises, creating a positive cycle of "scenarios—liquidity—compliance."

Ripple's confidence comes from its strong capital accumulation. XRP is one of the largest cryptocurrencies by market capitalization, and although debates over its price and functionality have never ceased, it is undeniable that XRP provides Ripple with substantial capital. Unlike the general pursuit of decentralization in most crypto projects, the Ripple team holds a large amount of XRP tokens. Its CEO has openly stated that selling XRP tokens is one of Ripple's important sources of revenue. In its Q1 financial report this year, Ripple disclosed that it holds 4.56 million XRP in its corporate wallet, valued at approximately $10.27 billion. Additionally, Ripple has 371 million XRP in custody accounts, valued at up to $83.5 billion, which will be gradually unlocked over the next few years. The "internalization" of capital and channels further strengthens Ripple's fundraising capabilities: long-standing strategic shareholder SBI Holdings continues to deepen cooperation, planning to distribute RLUSD with Ripple in Japan (targeting early 2026), transforming shareholder relationships into operational channels; at the same time, Ripple repurchased C-round shares in 2022 at an estimated valuation of about $15 billion, demonstrating strong capital resilience and self-sustaining capabilities, providing flexibility for subsequent acquisitions, license expansions, and ecosystem investments.

III. How Does XRP Differ from Other Similar Tokens?

(1) XRP vs XLM: "Design Divergence" and Implementation Routes of Similar Payment Settlement Networks

1. Positioning and Origin

Although XRP and XLM both focus on cross-border payments and financial infrastructure, there are fundamental differences in their philosophies and target markets.

XRP is primarily developed by Ripple and is aimed at banks and traditional financial institutions, emphasizing compatibility with the traditional financial system and regulatory compliance, with the goal of becoming a digital intelligent upgrade solution for traditional interbank settlements.

XLM is developed by the Stellar Development Foundation, taking an inclusive approach aimed at providing financial services to ordinary people worldwide. Therefore, the Stellar network places greater emphasis on inclusive finance, supporting the native issuance and trading of various assets, and includes decentralized exchange functionality.

2. Consensus and Network Structure

Both parties have chosen different consensus mechanisms based on their positioning.

XRPL employs a Byzantine fault-tolerant consensus based on UNL (Unique Node List) and a Negative UNL fault tolerance mechanism, requiring support from over 80% of validators for two consecutive weeks to activate protocol upgrades. This mechanism creates a highly controllable network environment, ensuring stability and predictability at the institutional level, but at the cost of concentrating governance power in the hands of a few trusted nodes, forming a quasi-permissioned ecosystem more suitable for traditional financial institutions.

XLM adopts the SCP (Federated Byzantine Agreement) federated consensus and "quorum slice" structure. This design releases the network's autonomy and inclusivity, allowing any node to participate and build trust relationships without permission, creating a truly decentralized global payment network that can adapt to the diverse needs of participants from different regions and of different scales, but it also brings higher complexity and uncertainty.

3. Functional Components and Programmability

XRPL has a more mature native trading infrastructure—native CLOB + DEX has existed since 2012, and the XLS-30 AMM went live on the mainnet in 2024 and continues to be optimized. The launch of the EVM sidechain mainnet in 2025 allows XRP to be used as gas fees, achieving multi-chain interoperability through the Axelar bridge, forming a complete ecosystem from native trading to EVM compatibility.

In contrast, Stellar has chosen a more aggressive smart contract route, activating the Soroban smart contract platform with Protocol 20 in 2024, supported by an official ecosystem fund from the SDF to encourage developer adoption.

4. Token Economics and Supply Governance

In terms of token economics, XRP adopts a pre-mined model with a fixed total supply of 100 billion tokens, currently with a circulating supply of 59.48 billion. Ripple holds nearly one-third of the XRP and has placed 55 billion on-chain in a monthly released escrow since 2017, with any unused portion of the month being rolled back and re-locked. This model provides stable funding support for the network but also raises concerns about centralized control. The XRP destruction mechanism is implemented through transaction fees, with a small amount of XRP being destroyed with each transaction, theoretically giving it deflationary characteristics.

XLM also adopts a pre-mined model, having destroyed 55 billion XLM in a one-time event in 2019, reducing the total supply to 50 billion tokens, with a current circulating supply of 31.73 billion, and completely eliminating the original annual inflation mechanism. The current fee model employs a destruction mechanism—transaction fees are no longer distributed to validating nodes but accumulate into a fee pool (non-circulating pool), which can theoretically be changed through governance.

5. Ecosystem and Implementation

In terms of ecosystem, RippleNet has established partnerships with over 300 financial institutions globally, including well-known entities like Santander Bank, American Express, and Standard Chartered Bank. The launch of the XRPL EVM sidechain in 2025 marks an important expansion of the XRP ecosystem into the DeFi space. Currently, over 160 tokens have been launched on the mainnet, with more than 17,000 unique wallet addresses participating. From a regulatory perspective, XRP reached a settlement agreement with the SEC in 2025, paying a $50 million fine, clearing significant obstacles for its development in the U.S. market, with multiple XRP ETF applications awaiting SEC approval.

The ecosystem development of XLM is evolving towards practicality. Currently, the Stellar network's TVL has reached $139.8 million, primarily composed of DEX trading and lending protocols. The native issuance of Stellar USDC/EURC makes it a key node in stablecoin infrastructure; collaborations with MoneyGram Ramps for cash deposits and withdrawals, as well as pilot projects for humanitarian payments with the United Nations High Commissioner for Refugees, directly connect fiat currency to the public. These efforts have established practical application scenarios for Stellar in the payments and remittances sector.

6. Conclusion

Similarities: Both focus on payment settlement, low fees, and require account reserves; both are working to enhance "smart contract" capabilities (XRPL is pursuing "AMM + EVM sidechain," while Stellar is pursuing "L1 Soroban").

Differences: XRPL emphasizes "native market infrastructure (DEX/AMM) + sidechain expansion," while Stellar emphasizes "broad coverage of fiat deposits and withdrawals and stablecoin circulation." In terms of compliance, XRP has gained secondary market clarity due to case law; XLM has long pursued payment network expansion led by a non-profit foundation.

(2) XRP vs LINK: Comparison of "Value Capture Models" in Different Tracks

1. Product and Network Functions

The core function of the XRPL network is to complete ledger settlement, payments, issuance, and matching. As the native token of the XRPL network, XRP's value primarily comes from payment demand driven by network effects, institutional-level liquidity bridging functions, and the deflationary destruction mechanism as transaction fees. After the launch of the XRPL EVM sidechain mainnet in June 2025, XRP serves as the native gas token on the sidechain, providing fuel for the DeFi ecosystem while achieving cross-chain interoperability with over 100 blockchains through the Axelar bridge.

Chainlink, as the leading decentralized oracle network, covers price oracles for over 3,000 assets, with a daily processing volume exceeding $166 million through its cross-chain communication protocol (CCIP) and proof of reserves. Additionally, Chainlink is making milestone collaborations with SWIFT, SBI Group, and even the Federal Reserve. This deep integration elevates the value capture of the $LINK token from a single service payment to a multi-dimensional token used for node staking and ensuring network economic security.

2. Token Use and Value Capture

The value capture of XRP is primarily achieved through several dimensions: first, the liquidity demand as a bridging currency, where financial institutions need to hold a certain amount of tokens when using XRP for cross-border transfers; second, payment of network fees, which, although extremely low per transaction (0.00001 XRP), has a significant cumulative effect under large-scale applications; third, institutional reserve demand, as more enterprises incorporate XRP into their asset allocations, driving up reserve demand and consequently the price.

The value capture mechanism of LINK is more diverse and sustainable. Each data query from the oracle requires payment in LINK tokens. The staking mechanism requires node operators to lock LINK as a service deposit, reducing the circulating supply. The introduction of the Cross-Chain Interoperability Protocol (CCIP) requires users to pay LINK for cross-chain asset transfers. Furthermore, Chainlink's revenue-sharing mechanism allows LINK holders to participate in network revenue distribution.

3. Ecosystem and Institutional Collaboration Signals

Chainlink is establishing its leadership position in institutional collaboration from a deeper strategic value perspective. It aims to jointly develop tokenized asset standards in the Asia-Pacific region through its partnership with SBI Group, and it has become the first platform to provide blockchain data services to the government through collaboration with the U.S. Department of Commerce. Additionally, by obtaining enterprise-level security certifications such as ISO and SOC2, Chainlink is clearing key compliance barriers for large-scale adoption by traditional financial institutions, indicating that the market's "standardized adoption" of its services has become an established trend.

Meanwhile, with the historic settlement reached with the SEC in 2025, XRP has finally broken free from regulatory shackles and entered a new phase of multi-dimensional expansion. Its core banking partnership network is accelerating from concept to scaled implementation, with integration testing with SWIFT and ETF applications and custody services in the Asia-Pacific region highlighting its increasing regulatory acceptance. More critically, through the combination of the RLUSD stablecoin and the EVM sidechain, XRP's strategic narrative is expanding from a singular focus on "cross-border payments" to "multi-chain programmable finance," a momentum that has been preliminarily validated in the active development of over 75 testnet DApps and the asset allocations of listed companies.

4. "Is XRP Overvalued Like LINK?" — The Correct Benchmarking Method

Simply comparing XRP and LINK by market capitalization often leads to "misalignment." It is recommended to use three sets of quantifiable metrics for cross-validation of "value capture intensity":

Cash Flow / Fee Side

LINK and XRP have completely different cash flow models. LINK generates real fee income through oracle data requests and CCIP cross-chain messages, with oracle service fees reaching $400.22K within 30 days and cumulative fees for CCIP cross-chain services totaling $603.07K, showing that approximately 32% of fees convert into protocol revenue, with a wide range of active paying clients from DeFi protocols to traditional financial institutions. More importantly, the $1.01B in staking TVL provides security for the network, and the staking coverage indicates that fees are sufficient to support the network's security budget.

In contrast, XRP's network fees are directly destroyed rather than distributed as dividends. Although there are payment settlements and DEX/AMM activities on XRPL, and Ripple Payments is handling cross-border remittances, the key lies in demand elasticity—how much users are willing to pay for fast settlements. The actual circulation and payment uses of stablecoins like RLUSD on-chain are the core of value capture, rather than traditional cash flow dividends.

Supply and Unlocking Side

XRP faces continuous release pressure from the hundreds of billions of tokens held by Ripple through the escrow mechanism. Although there is a rollback rhythm, the total amount is large, and any significant changes in Ripple's wallet will affect market expectations.

In contrast, LINK's annual release rate is about 7% of the total supply, which is relatively controllable and transparent, with clear disclosures on the usage of the team and treasury. More importantly, the newly introduced staking lock-up mechanism has begun to hedge some of the release pressure.

This difference in supply structure directly affects the price elasticity of the two tokens and the confidence of long-term holders.

Adoption and Network Effect Side

In terms of adoption and network effects, the two are taking completely different paths. LINK has already become the standard for cross-chain infrastructure, with the number of connected public chains continuously increasing, and the volume of CCIP cross-chain messages growing exponentially. Its productization progress with SWIFT, major custodians, and exchanges has established an irreplaceable moat in the traditional financial sector. Although XRP has a grand vision for a payment network, actual data shows that the TVL of the EVM sidechain is $96.80M and the number of active contracts is still limited. The liquidity and routing share of the native DEX/AMM are also not high. While the actual payment numbers of fiat deposits and withdrawals and stablecoins on XRPL are increasing, there is still a long way to go before it becomes a global payment infrastructure. The depth of network effects determines the width of the moat, which is why investment value cannot simply be judged by market capitalization rankings.

IV. Conclusion

Having shed the shadow of the SEC lawsuit, Ripple is continuing its journey into the payment sector it has been laying out for many years amidst controversy. The construction of compliance directions such as cross-jurisdictional regulation and disclosure obligations still constitutes the underlying constraints on Ripple's operations and financing. On top of these constraints, Ripple's "Payments (Flow) - Custody (Assets) - Stablecoins (Settlement)" flywheel is gradually opening up. However, for Ripple to achieve large-scale or even "alternative-level" penetration, it still depends on three things—

(1) Regulatory Clarity: Institutional inclusion of stablecoins and on-chain settlements in major jurisdictions;

(2) First and Last Mile and Liquidity: Market-making depth, failure rates, and in-transit position management metrics for core corridors like USD/EUR must meet bank-level SLAs;

(3) Unit Economics: The difference between Ripple Payments' take-rate/failure rate/operating cost and the yield on reserves - compliance costs of RLUSD, which can provide "room" for both customers and the company in the long term. If Ripple can make significant progress in these three areas, we can expect Ripple to ride the wave of asset tokenization and form scalable, replicable unit economics in several corridors ahead of others. However, at this stage, Ripple's cross-border payment business will play a supplementary role, coexisting alongside traditional rails for a long time.

Compared to other projects that are often mentioned together, XRP vs XLM has chosen different paths within the same sector—XRP is pursuing "institutional compliance + native market infrastructure (CLOB/AMM) + sidechain expansion," while XLM is focusing on "inclusivity + fiat deposits and withdrawals + broad coverage of stablecoins"; whereas XRP vs LINK essentially belongs to different tracks, with XRP's value anchored in "settlement scale and turnover routed through XRP + supply/destruction constraints," while LINK is anchored in "paid usage and security budget" (oracle/CCIP fees and staking). Therefore, it is inappropriate to use the same multiple to assert overvaluation/undervaluation; a more pragmatic approach is to track: XRP's routing share and depth, net changes in escrow; LINK's paid income and staking coverage, etc. Whoever can pull their respective core KPIs into a sustained upward curve first deserves a valuation premium.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。