In a market environment with insufficient liquidity in the spot market, market makers can only focus on the increasingly growing perpetual contract market. To this end, all parties are brainstorming ways to connect the spot and contract paths, organically combining the liquidity and profit and loss determination rules of both mechanisms, ultimately giving rise to new token economics models and community expectation management models, creating a dramatic "demon coin" long-short slaughter.

The so-called "demon coin" is a collection of specific market conditions: highly concentrated chips (i.e., "low circulation, high control") and simultaneously listed in both the illiquid spot market and the highly liquid high-leverage perpetual contract market.

This article will analyze the complete lifecycle of this manipulation process, from the initial token economics design that facilitates manipulation, to guiding retail investor sentiment, and finally to executing spot-driven attacks with precision, with the ultimate goal of triggering chain liquidations in the derivatives market to gain profits.

Disclaimer

The purpose of this article is not to endorse such behaviors or target any project or exchange, but to provide a technical, quantitative, and objective mechanism analysis to help mature market participants identify and potentially avoid related risks.

Part One: Building the Trap: Preparations Before Manipulation

The success of the entire operation depends on a carefully designed market structure, where manipulators have established near-absolute control over the asset's supply and price discovery mechanism before any significant retail participation.

1.1. Creating Scarcity: Low Circulation, High Control Token Economics Model

The starting point of this strategy is not in the trading phase, but in the conceptual stage of the token. The manipulator, usually the project party or its closely associated supporters, will design a token economics model that ensures the vast majority of token supply (e.g., 95%) is locked or held by insiders, with only a very small portion—i.e., the "circulating supply"—available for public trading at the initial issuance.

This "low float, high fully diluted valuation (FDV)" model creates artificial scarcity. Due to the limited number of tokens in circulation, even a small amount of buying pressure can lead to rapid price increases and extremely high volatility. This dynamic is intentional, as it significantly reduces the capital required for manipulators to arbitrarily push the spot price.

This token economics model aims to create a market that is structurally very susceptible to the spot-driven liquidation strategies detailed in this report. A normal project issuance aims to build a community through decentralization and fair distribution, while the low circulation model does the opposite, concentrating power. Major holders gain near-complete price control. Manipulators do not need to "hoard" later; they have had market control from the beginning. When this pre-designed asset is placed in an environment of dual listing in both spot and contract markets, its token economic structure becomes a weapon.

Low circulation ensures that the spot price can be easily manipulated, while the contract market provides a pool of leveraged participants to be harvested. Therefore, token economics is a prerequisite for this strategy. Without such a level of control, the cost of manipulating the spot price would be prohibitively high. Choosing which token economics to adopt is the primary and most critical step in the manipulation script.

From a psychological perspective, although the circulating supply is very low, a high FDV creates an illusion of grandeur and ambition for the project, while low circulation generates initial hype and a "scarcity effect," attracting speculative retail interest and creating conditions for subsequent "fear of missing out" (FOMO).

1.2. Catalyst for Dual Listing: Building a Dual Front

Simultaneously or almost simultaneously listing on a liquid spot exchange and the perpetual contract market is a key part of the entire strategy. Platforms like Binance Alpha serve as a "pre-listing token screening pool," signaling potential future mainboard listings and building initial hype.

These two fronts are:

- Spot Market (Control Zone): This is where manipulators exert their overwhelming supply advantage. Due to the extremely small circulating supply, they can dominate the price with relatively little capital.

- Perpetual Contract Market (Harvest Zone): This is where retail and speculative capital congregate. It offers high leverage, amplifying retail traders' positions and making them highly susceptible to liquidation shocks. The main goal of manipulators is not to profit from spot trading but to use their control over the spot price to trigger more profitable events in this second battlefield.

Introducing derivatives alongside spot assets creates a powerful linkage effect. It increases the overall liquidity, price synchronization, and efficiency of the market, but in this controlled environment, it also creates a direct attack vector for manipulation.

Part Two: Market Preheating: Creating Sentiment and Measuring Risk Exposure

Once the market structure is in place, the next phase for manipulators is to attract targets into the harvest zone (contract market) and accurately measure their risk exposure. This includes creating false narratives of activity and demand while using derivatives data as a "fuel gauge."

2.1. The Illusion of Activity: Wash Trading and Faked Trading Volume

A new token with low trading volume lacks appeal. Manipulators must create an illusion of an active, liquid market to attract retail traders and automated trading bots that consider trading volume as a key indicator.

To achieve this, manipulators use multiple controlled wallets to trade with themselves in the spot market. On-chain, this manifests as funds or assets circulating between related parties. This behavior artificially inflates trading volume metrics on exchanges and data aggregators, creating a misleading impression of high demand and high liquidity.

Despite the complexity of the methods, such behavior can still be identified by analyzing specific patterns in on-chain data:

- High-frequency trading exists between a small number of unknown exchange or market maker wallets.

- Buy and sell orders occur almost simultaneously, with no meaningful change in actual beneficial ownership.

- Reported high trading volume is mismatched with shallow order book depth or low on-chain holder growth.

2.2. Interpreting the Derivatives Battlefield: Open Interest and Funding Rate Analysis

Manipulators do not trade blindly. They meticulously monitor the derivatives market to assess the effectiveness of their preheating efforts. The two most critical indicators are Open Interest (OI) and funding rates.

Manipulators do not use OI and funding rates as predictive indicators like ordinary traders; instead, they treat them as a real-time feedback and targeting system. These indicators act like a "fuel gauge," precisely telling them when the market has been sufficiently penetrated by one-sided leverage, maximizing the profits of a liquidation storm that can sustain itself.

An ordinary trader seeing high OI and positive funding rates might think, "The trend is strong; maybe I should go long," or "The market is overextended; it might reverse." Their perspective is probabilistic. In contrast, manipulators controlling the spot price have a deterministic perspective. They know they can force the price down. Their question is not whether a reversal will happen, but when to trigger it at the most advantageous interval, essentially when they can "cut" the market. Increasing OI tells them that the number of leveraged positions is rising. High funding rates indicate that these positions are overwhelmingly one-sided. The combination of these two indicators allows manipulators to quantify the size of the "liquidation pool." They can estimate the dollar value of positions that will be liquidated at different price levels below the market. Therefore, they are not predicting the market top; they are waiting for the perfect moment to create the market top. OI and funding rates are their signals indicating that enough "fuel" has been loaded into the system to launch a successful attack.

- Open Interest (OI) as a measure of "fuel": OI represents the total number of open futures contracts. Rising OI, especially in an upward price trend, indicates that new capital and new leveraged positions are entering the market. This is not just existing traders exchanging positions but an expansion of the total stake size. For manipulators, rising OI confirms that the pool of potential liquidation targets is expanding.

- Funding rate as a measure of sentiment: The funding rate is the amount exchanged between long and short position holders to anchor the perpetual contract price to the spot price.

- High positive funding rate: The contract price is above the spot price. Longs pay fees to shorts. This indicates extremely bullish market sentiment, with leveraged long positions highly concentrated.

- High negative funding rate: The contract price is below the spot price. Shorts pay fees to longs. This indicates extremely bearish market sentiment, with leveraged short positions highly concentrated.

- Combination signals: Manipulators wait for a specific combination of signals: a sharp increase in OI, accompanied by sustained high funding rates (whether positive or negative). This combination signal indicates that a large number of retail traders have established leveraged positions in the same direction, forming dense clusters of liquidation levels below (for longs) or above (for shorts) the current price. This is the "fuel" for chain liquidations.

2.3. Narrative Warfare and FOMO Creation

While conducting quantitative preheating, manipulators often launch a "soft power" offensive. This includes using social media, paid KOLs, and press releases to build an engaging narrative around the token.

Announcing false partnerships, previewing "major developments," or simply promoting a "get rich quick" narrative can trigger intense FOMO. This psychological manipulation pushes retail traders into the contract market, making them bet on leverage and directly providing data for the OI and funding rate metrics that manipulators are monitoring.

Part Three: Execution: Weaponizing the Mark Price

This is the momentum phase of the operation. Manipulators use their control over the spot market to launch direct, precise attacks on the derivatives market, weaponizing the exchange's own mechanisms.

3.1. Mechanical Linkage: Analyzing the Calculation of Mark Price

The key to the entire strategy is that liquidations of perpetual contracts are triggered by the mark price rather than the last traded price. This is a crucial distinction. The last traded price can fluctuate wildly and is easily manipulated within a single exchange, so exchanges use a more robust mark price to prevent unfair liquidations.

Although the formula for mark price varies slightly between exchanges, it fundamentally relies on an index price plus a decaying funding rate component. The index price is a volume-weighted average of the asset's spot prices across multiple mainstream exchanges.

This design creates a direct and unavoidable causal chain:

Manipulator's Spot Market Behavior → Spot Price Movement → Index Price Movement → Mark Price Movement → Triggering Liquidation.

By controlling the dominant spot market of a new token with poor liquidity, manipulators effectively control the primary input variable for the mark price calculation. They are not influencing the liquidation mechanism; they are dominating it.

Manipulators are using the exchange's own risk management system—namely, the mark price and automatic liquidation engine—as a tool for profit amplification. This system was originally designed to protect exchanges and traders from excessive risk, but when an entity controls the underlying spot price, it becomes the very mechanism for "harvesting." The introduction of the mark price mechanism by exchanges is intended to prevent manipulation based on the latest transaction price from a single exchange, as they assume that the aggregated index price is difficult for any single actor to manipulate. This assumption holds true for highly liquid, decentralized assets like BTC or ETH. However, for a low-circulation new token, the "exchanges" that constitute the index price may only be one or two (some are just liquidity pools on DEXs). By controlling the vast majority (e.g., 98%) of the circulating supply, manipulators can easily control the price of the most critical input variable in the index price calculation. Thus, manipulators turn the exchange's protective measures into weapons.

Chain liquidations are not a secondary goal of their actions but the primary objective. The forced market orders generated by liquidations provide massive liquidity for manipulators to close their large futures positions at optimal prices.

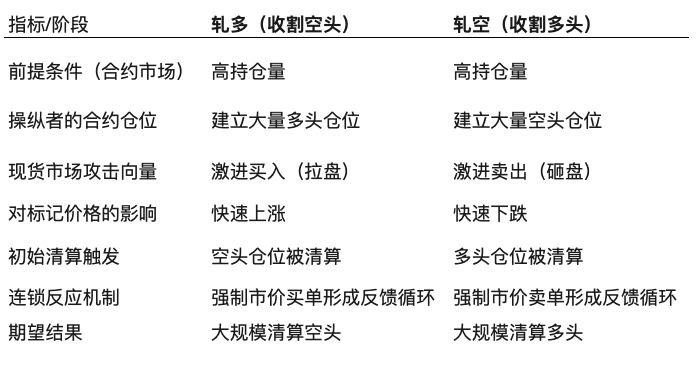

3.2. Short Squeeze Script (Harvesting Shorts)

Prerequisites: Manipulators observe a price decline, rising open interest, and negative funding rates (which can also be used as a means to lure longs and shorts), indicating that a large number of leveraged short positions are accumulating. Retail sentiment is bearish.

First Stage: Position Building: Manipulators quietly establish a massive long position in the perpetual contract market, typically absorbing selling pressure from retail shorts. They are willing to temporarily pay negative funding rates, viewing it as the cost of setting a trap.

Second Stage: Spot Market Attack: Manipulators execute a series of large buy orders in the spot market using a small portion of their massive token holdings. Due to the extremely small public circulating supply, this action requires relatively little capital to trigger a huge, almost instantaneous price surge.

Third Stage: Chain Liquidation:

- The surge in the spot price immediately pushes up the index price.

- The index price subsequently raises the mark price.

- The rising mark price reaches the liquidation level of the most leveraged short positions.

- These liquidations are enforced as market buy orders, further increasing upward price pressure.

- This creates a feedback loop or "short squeeze": forced buying drives up prices, liquidating the next tier of shorts, leading to more forced buying, and so on. This chain reaction continues until most short positions are cleared.

3.3. Long Squeeze Script (Harvesting Longs)

Prerequisites: Manipulators observe a price increase (usually driven by their own wash trading and hype), soaring open interest, and high positive funding rates (which can also be used as a means to lure longs and shorts). Retail sentiment is euphoric, with significant leverage being used to go long.

First Stage: Position Building: Manipulators establish a massive short position in the perpetual contract market. They collect funding fees from numerous longs while waiting to profit.

Second Stage: Spot Market Attack: Manipulators sell a small portion of their token holdings into the spot market. This sudden, massive selling pressure immediately causes the spot price to plummet.

Third Stage: Chain Liquidation:

- The plummet in the spot price pulls down the index price, and thus the mark price.

- The falling mark price triggers the liquidation of leveraged long positions.

- These liquidations are enforced as market sell orders, further increasing downward price pressure.

- This results in a "long squeeze" or chain liquidation effect, where forced selling triggers more forced selling, clearing long positions like a domino effect until the excessive leverage in the market is eliminated.

Part Four: Aftermath: Profits, Risks, and Recognition

4.1. Profit Realization

Closing Profits: The main profits come from the large futures positions established in the first step of the execution phase. During the chain liquidation, a massive influx of forced market orders (buy orders during a short squeeze, sell orders during a long squeeze) enters the market. This provides manipulators with perfect, high-volume exit liquidity, allowing them to close their multi-million dollar positions at extremely high profits.

Secondary Profits: Manipulators can also profit from the actions in the spot market itself. After crashing the price to liquidate longs, they can repurchase their tokens at very low prices (even more). After driving up the price to liquidate shorts, they can sell tokens into a FOMO-driven rally.

4.2. Risk Analysis for Manipulators

Cost of Capital: Although spot market manipulation is effective, it is not without costs. Executing a price surge or absorbing a crash incurs significant slippage costs.

Exchange Intervention: Exchanges like Binance/OKX/Bitget have internal market surveillance teams. Severe manipulative behavior, especially if detected, can lead to account freezes, asset delistings, or investigations. There have been cases where Binance/Bitget fired investigators who exposed major client manipulative behavior, indicating a complex environment that sometimes involves conflicts of interest.

Counterparty Risk: This strategy assumes that the manipulator is the only "whale" in the pond. While it is unlikely with 97% control, there remains the possibility of another large entity attempting to manipulate in the opposite direction, which could lead to a costly price control war.

4.3. Danger Signals and Defensive Analysis for Retail Traders

Danger Signals in Token Economics (from Part One): Verify the concentration of on-chain holders. If the top 10 holders control over 90% of the supply, the asset is structurally compromised and carries a high risk of manipulation. Avoid tokens with extremely low initial circulating supply.

Danger Signals in Market Activity (from Part Two): Be wary of tokens with soaring prices accompanied by suspiciously high trading volumes but lacking genuine community growth or utility. Cross-reference trading volume with on-chain transaction counts and holder growth to uncover potential wash trading.

Danger Signals in Derivatives (from Parts Two and Three): The strongest warning signal is a sustained rapid increase in open interest, accompanied by extreme funding rates. This indicates that market leverage is too high and that a severe "cleaning" event, carefully orchestrated by an entity controlling the spot price, is imminent. Analyzing the rate of change in open interest may provide more insight than its absolute value.

By understanding the structure of this strategy—from its structural foundation in token economics to its execution via mark price—mature market participants can better identify these carefully designed traps and avoid becoming the "liquidity" that manipulators intend to harvest.

Know the facts and understand the reasons behind them.

May we always hold a sense of reverence for the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。