Written by: Daren Matsuoka, Robert Hackett, Jeremy Zhang, Stephanie Zinn, and Eddy Lazzarin, a16z crypto

Compiled by: Glendon, Techub news

This is the year the world moves on-chain.

When we released the first "State of Cryptocurrency Report," the industry was still in its infancy. The total global cryptocurrency market capitalization was only half of what it is today, with blockchain technology being slower, more expensive, and less reliable.

Over the past three years, cryptocurrency developers have navigated significant market corrections and political uncertainties, yet they have continued to drive infrastructure upgrades and other technological advancements. These efforts have brought the industry to where it is today—cryptocurrency has become an essential part of the modern economy.

The cryptocurrency story of 2025 is a story of industry maturation. In short, cryptocurrency has grown up:

Traditional financial giants (such as Visa, BlackRock, Fidelity, and JPMorgan) and tech-native challengers (such as PayPal, Stripe, and Robinhood) are launching or planning to launch cryptocurrency products.

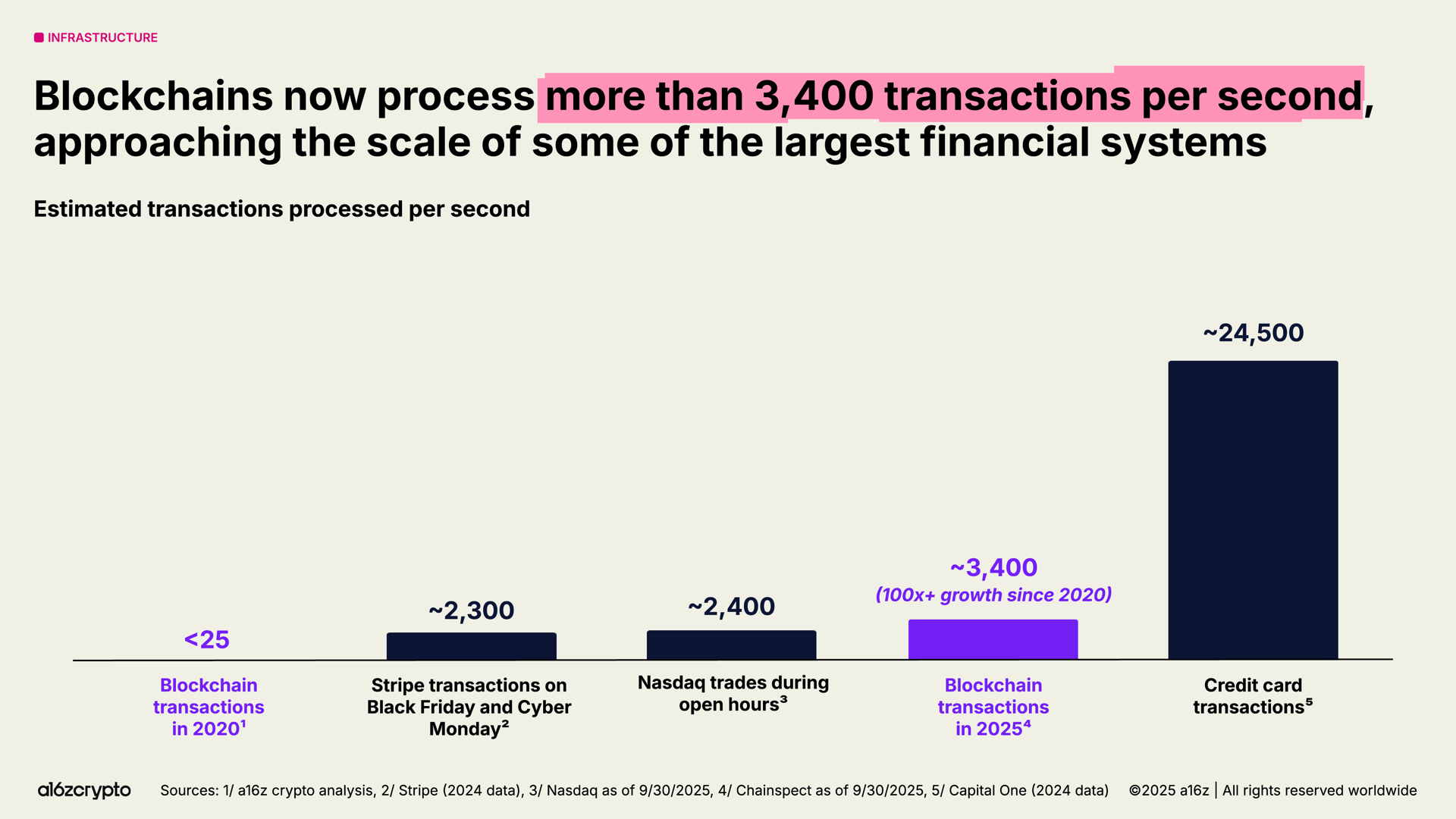

Blockchain processes over 3,400 transactions per second (growing more than 100 times in the past five years).

Stablecoins drive an annual transaction volume of $46 trillion (adjusted to $9 trillion), comparable to the scale of Visa and PayPal.

Bitcoin and Ethereum exchange-traded products (ETPs) have a funding scale exceeding $175 billion.

This latest "State of Cryptocurrency Report" delves into the industry's transformation, covering topics such as institutional adoption, the rise of stablecoins, and the integration of cryptocurrency with AI. Additionally, we are introducing a brand new way to present the state of cryptocurrency with a data dashboard that tracks industry evolution through key metrics.

Here are the core findings.

Key Points

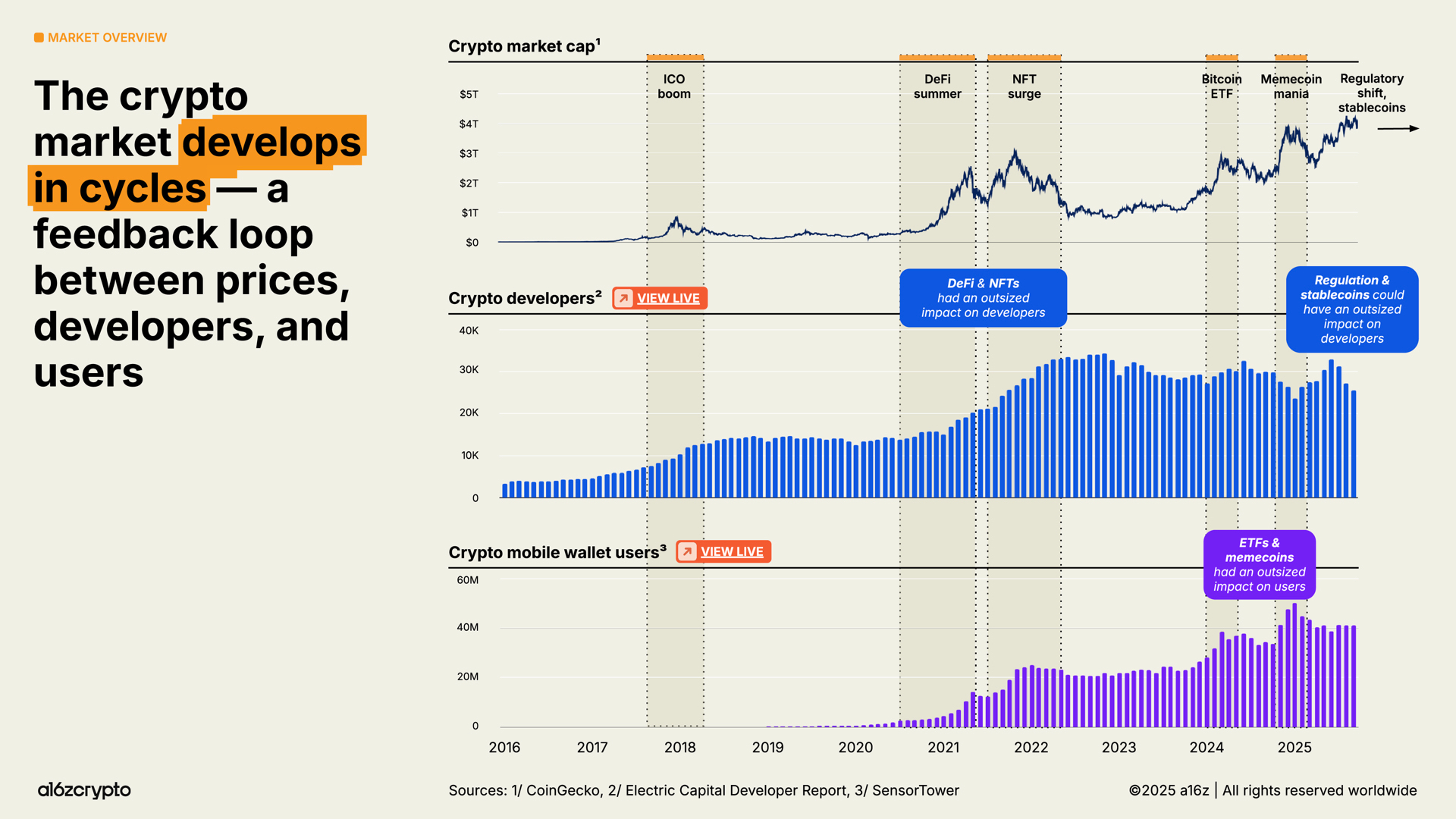

The cryptocurrency market is large, global, and continuously growing.

Financial institutions have adopted cryptocurrency.

Stablecoins have become mainstream.

Cryptocurrency is stronger in the U.S. than ever before.

The world is moving on-chain.

Blockchain infrastructure is (almost) ready for prime time.

Crypto technology and artificial intelligence are converging.

The Cryptocurrency Market is Large, Global, and Continuously Growing

In 2025, the total market capitalization of cryptocurrency surpassed $4 trillion for the first time, marking a significant advancement for the industry. The number of active cryptocurrency wallet users also reached a historic high, growing by 20% compared to last year.

The regulatory environment has shifted from hostile to more supportive, while the adoption of these technologies (from stablecoins to the tokenization of traditional financial assets to other emerging use cases) is accelerating, which will define the next cycle.

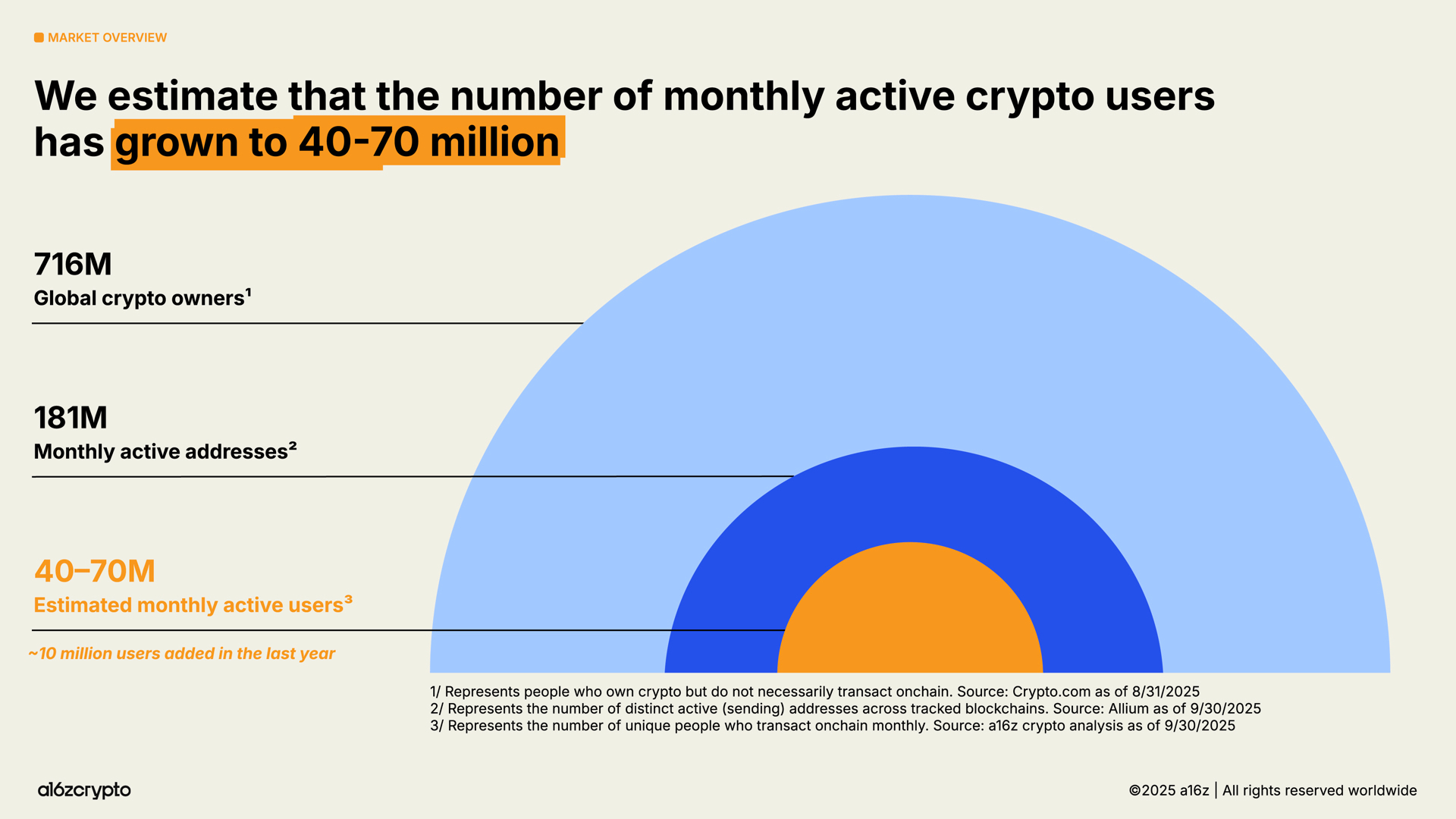

According to our updated analysis based on this methodology, there are approximately 40 million to 70 million active crypto users, an increase of about 10 million from last year. This is just a small fraction of the estimated 716 million cryptocurrency holders, a figure that has grown by 16% from last year. Additionally, there are about 181 million monthly active addresses on-chain, down 18% from last year.

The gap between passive cryptocurrency holders (those who own cryptocurrency but do not engage in on-chain transactions) and active users (those who regularly conduct on-chain transactions) presents an opportunity for cryptocurrency builders to reach more potential users who already own cryptocurrency.

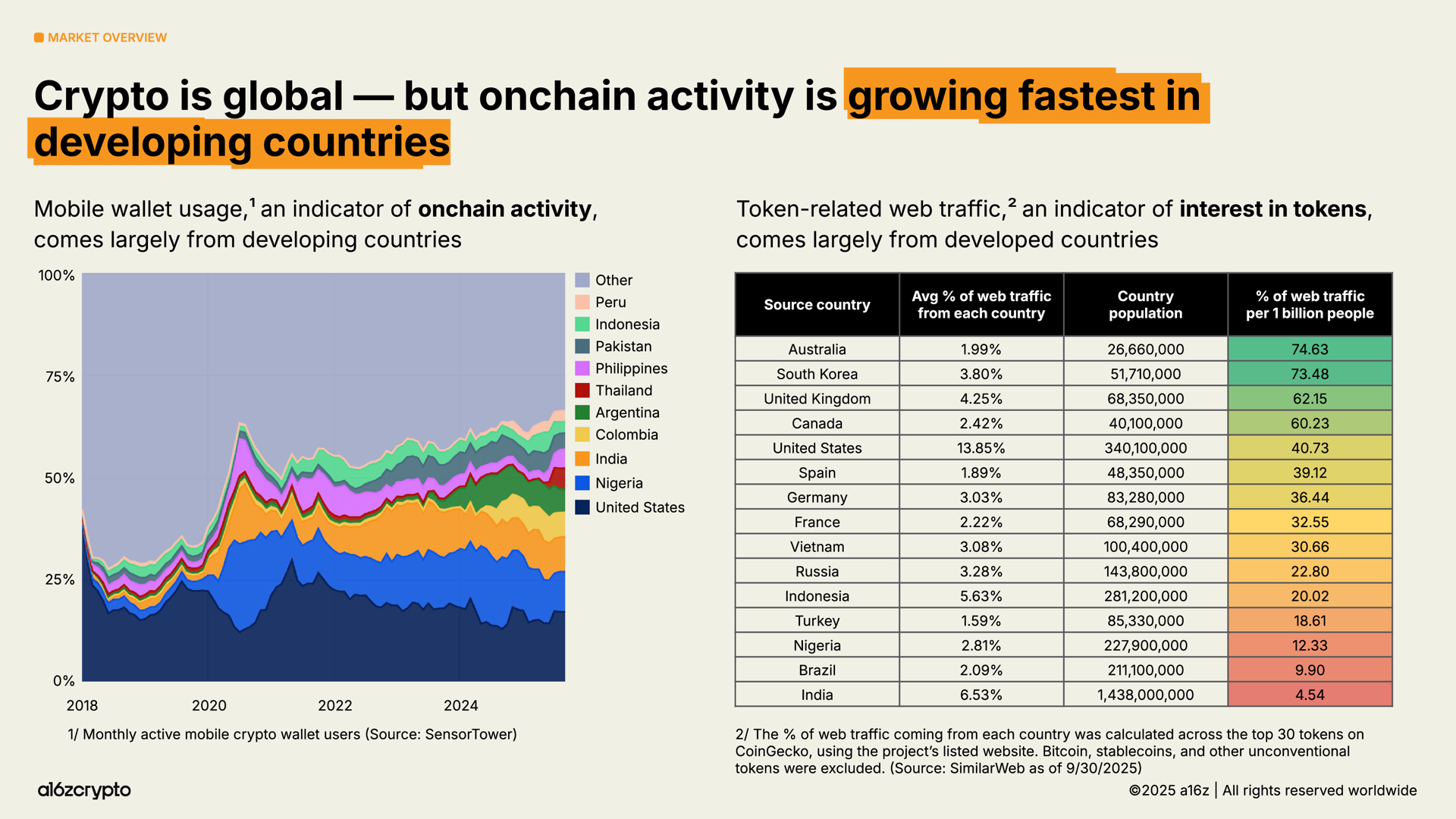

So where are these crypto users, and what are they doing?

Cryptocurrency is global, but the ways it is used around the world seem to vary. The usage rate of mobile wallets (an indicator of on-chain activity) is growing fastest in emerging markets like Argentina, Colombia, India, and Nigeria. (In Argentina, in particular, due to the escalating currency crisis, the usage rate of crypto mobile wallets has increased 16 times over the past three years.)

Meanwhile, our analysis of the geographic sources of token-related network traffic shows that interest in tokens tends to be higher in developed countries. Compared to user behavior in developing countries, activities in these nations (especially Australia and South Korea) may be more focused on trading and speculation.

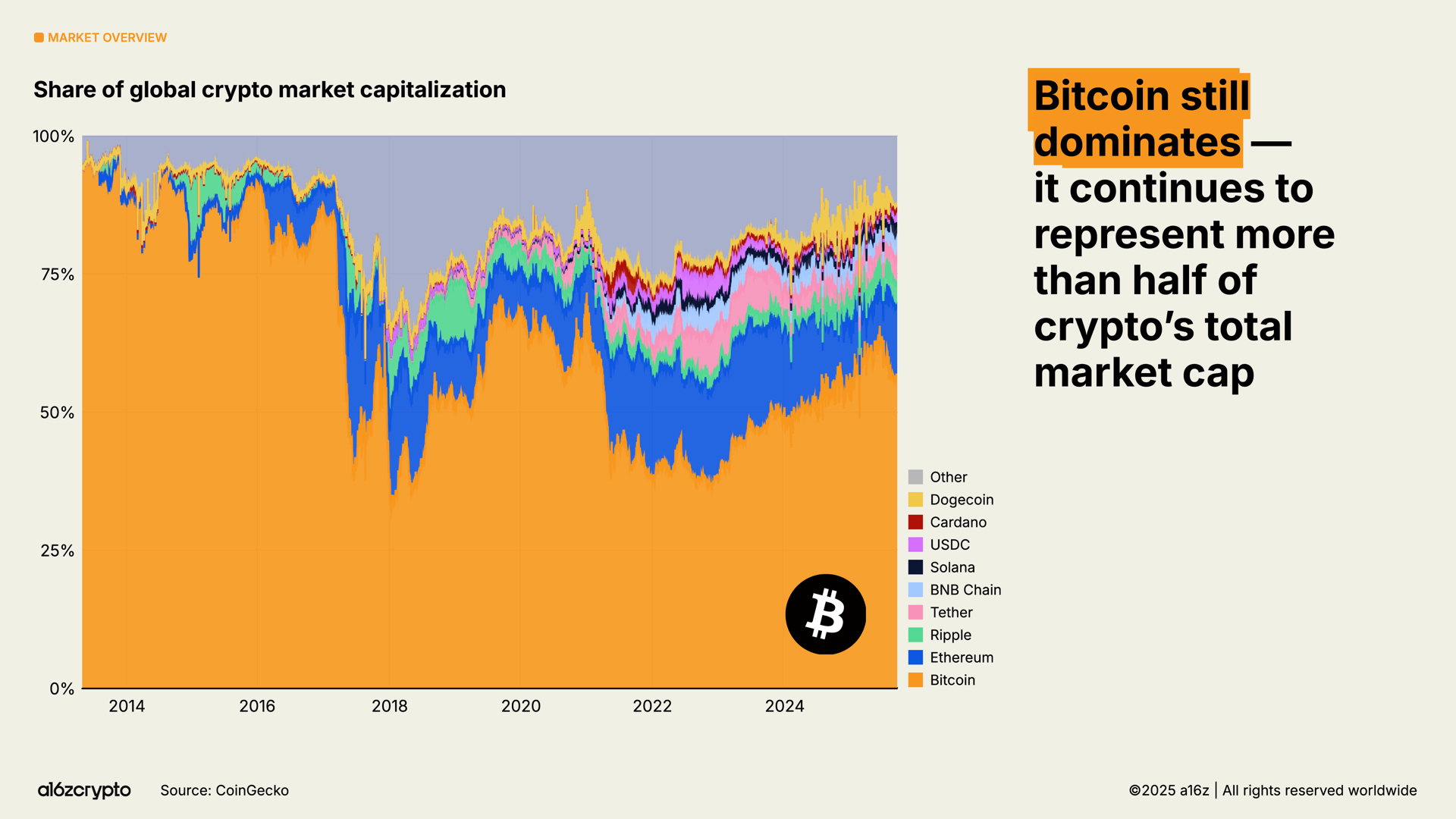

Bitcoin still accounts for more than half of the total cryptocurrency market capitalization and reached an all-time high of $126,000, as it increasingly appeals to investors as a store of value. Meanwhile, Ethereum and Solana have recovered most of their losses since 2022.

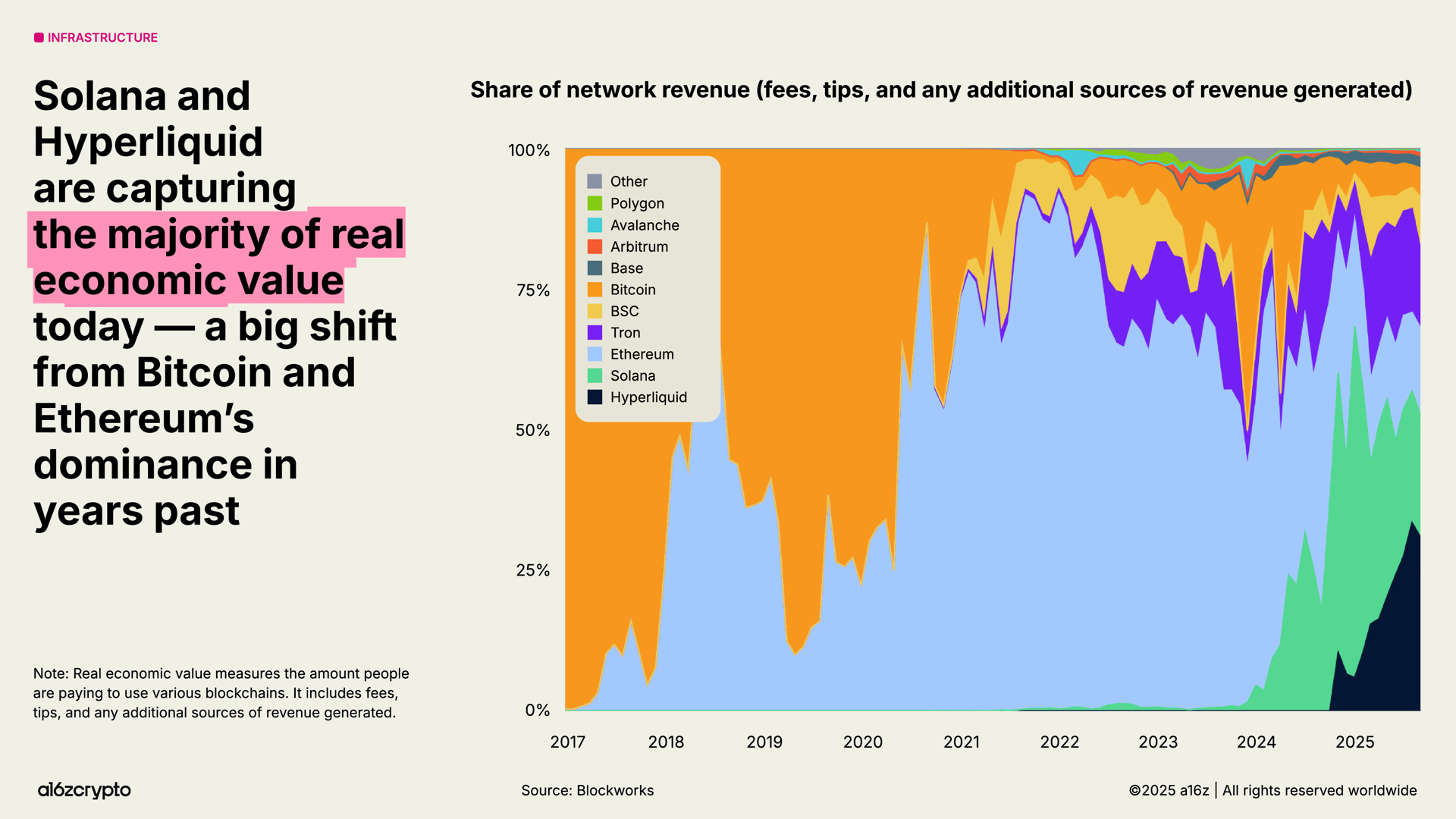

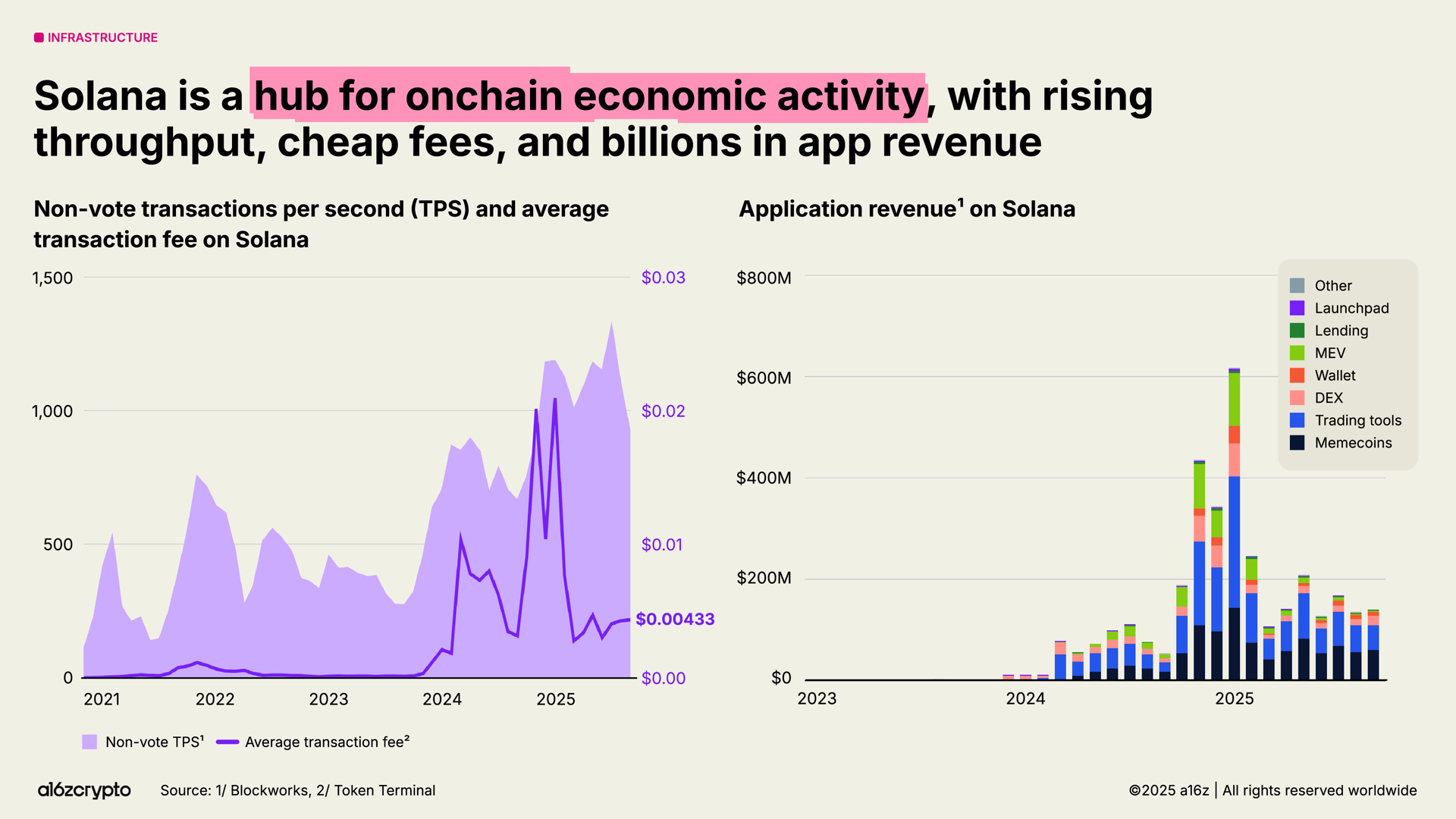

As the scale of blockchain continues to expand, the fee market matures, and new applications emerge, certain metrics are becoming increasingly important; one of them is "real economic value"—measuring the actual fees people are paying to use blockchain. Hyperliquid and Solana currently account for 53% of revenue-generating economic activity, which is a stark contrast to the dominance of Bitcoin and Ethereum in previous years.

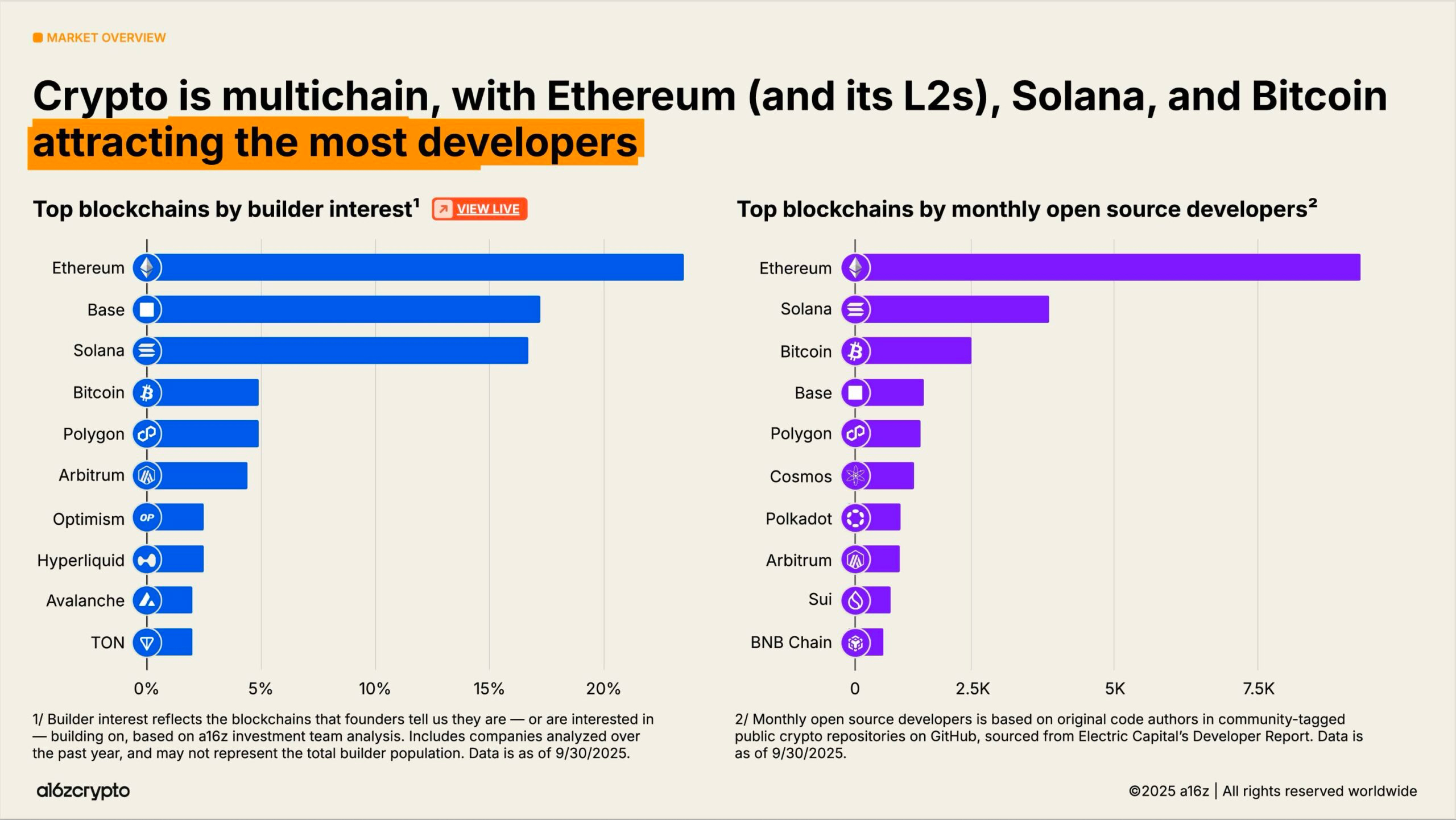

In terms of builders, cryptocurrency remains multi-chain, with Bitcoin, Ethereum (and its Layer-2 solutions), and Solana attracting the most developers. Ethereum and its Layer-2 solutions are the preferred destinations for new developers in 2025. Meanwhile, Solana is one of the fastest-growing ecosystems, with builder interest increasing by 78% over the past two years; according to the analysis from the a16z crypto investment team, this reflects what many founders have told us about which ecosystems they are building on or are interested in building on.

Financial Institutions Have Adopted Cryptocurrency

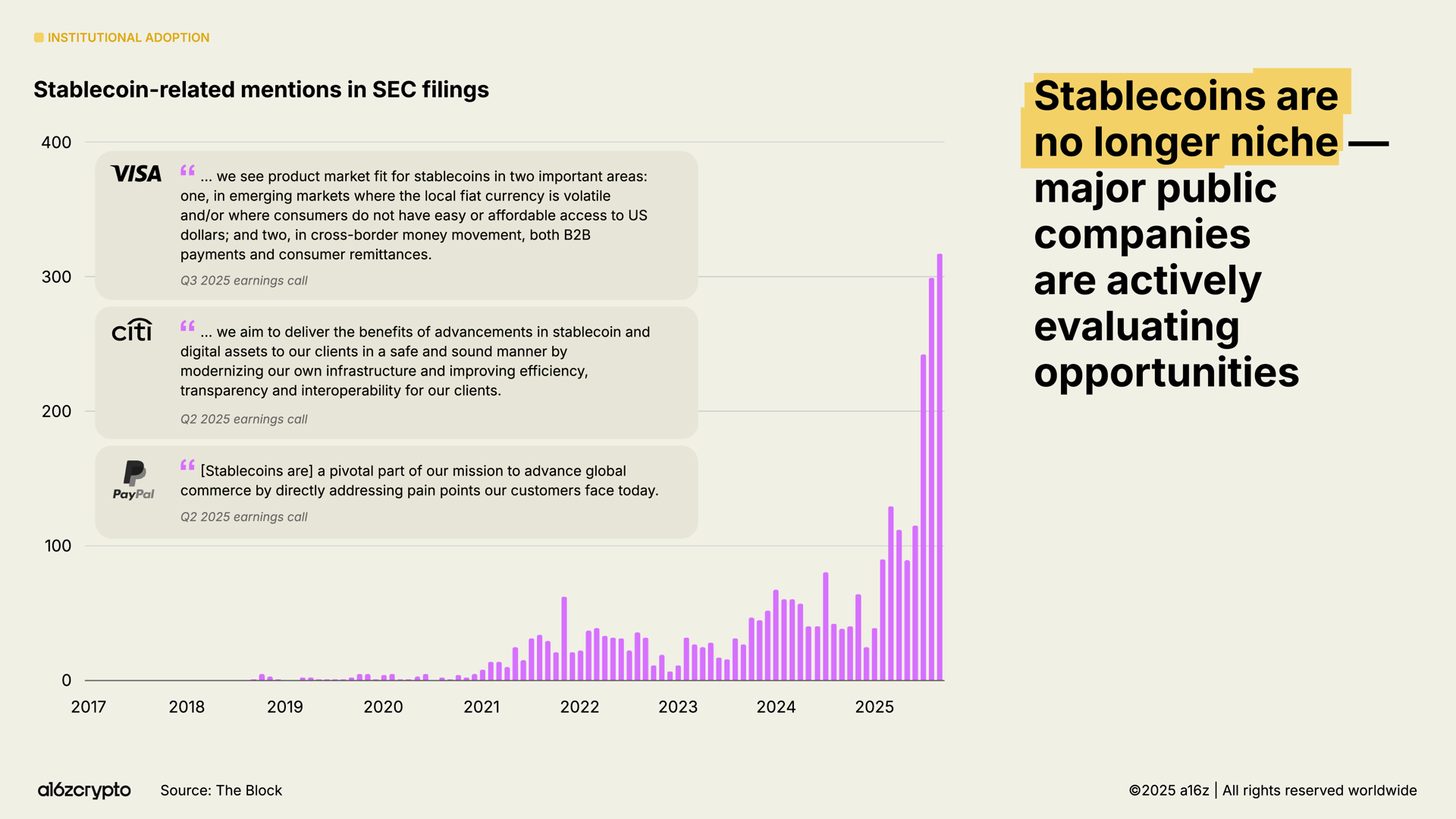

2025 is the year of institutional adoption. In last year's "State of Cryptocurrency Report," Stripe noted that stablecoins had found product-market fit, and just five days later, Stripe announced its intention to acquire the stablecoin infrastructure platform Bridge. This marked the beginning of competition: traditional financial companies are also ready to publicly launch stablecoins.

A few months later, Circle's $1 billion IPO marked stablecoin issuers as mainstream financial institutions. In July, the bipartisan "GENIUS Act" was passed, providing clear guidance for stablecoin developers and institutions for future development. In the following months, as mentions of stablecoins in SEC filings increased by 64%, major financial institutions began to release a series of announcements.

The rate of institutional adoption is rapidly increasing. Traditional institutions, including Citigroup, Fidelity, JPMorgan, Mastercard, Morgan Stanley, and Visa, are now directly offering (or planning to offer) crypto products to consumers, allowing them to buy, sell, and hold digital assets, as well as stocks, exchange-traded products, and other traditional tools. Meanwhile, platforms like PayPal and Shopify are doubling down on payment services and building infrastructure for everyday transactions between merchants and customers.

In addition to directly offering products, major fintech companies, including Circle, Robinhood, and Stripe, are actively developing or have announced plans to develop new blockchains, focusing on payments, physical assets, and stablecoins. These initiatives can lead to more on-chain payment flows, encourage enterprise adoption, and ultimately create a larger, faster, and more global financial system.

These companies have vast distribution networks. If this trend continues, cryptocurrency could become deeply integrated into the financial services we use daily.

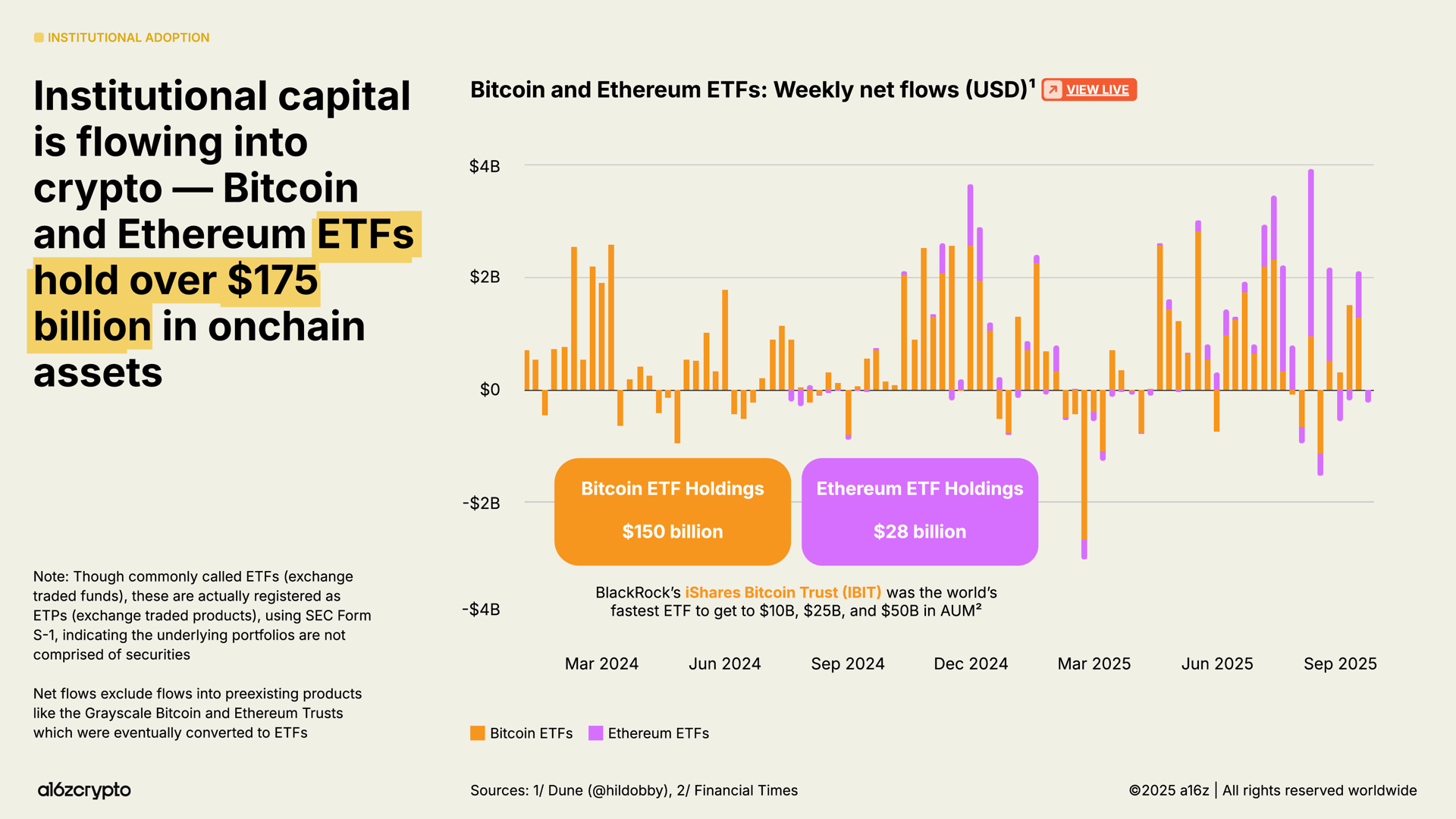

Exchange-traded products are another key driver of institutional investment, with on-chain cryptocurrency holdings currently exceeding $175 billion, a 169% increase from $65 billion a year ago.

BlackRock's iShares Bitcoin Trust (IBIT) is considered the largest exchange-traded product by trading volume in history, and its subsequent Ethereum exchange-traded product has also seen significant inflows in recent months. (Note: While commonly referred to as exchange-traded funds (ETFs), they are actually registered as ETPs, or exchange-traded products, using the SEC's S-1 form, indicating that their underlying portfolios do not contain securities.)

These products make cryptocurrency more accessible, unlocking a significant amount of institutional capital that has historically been on the fringes of the industry.

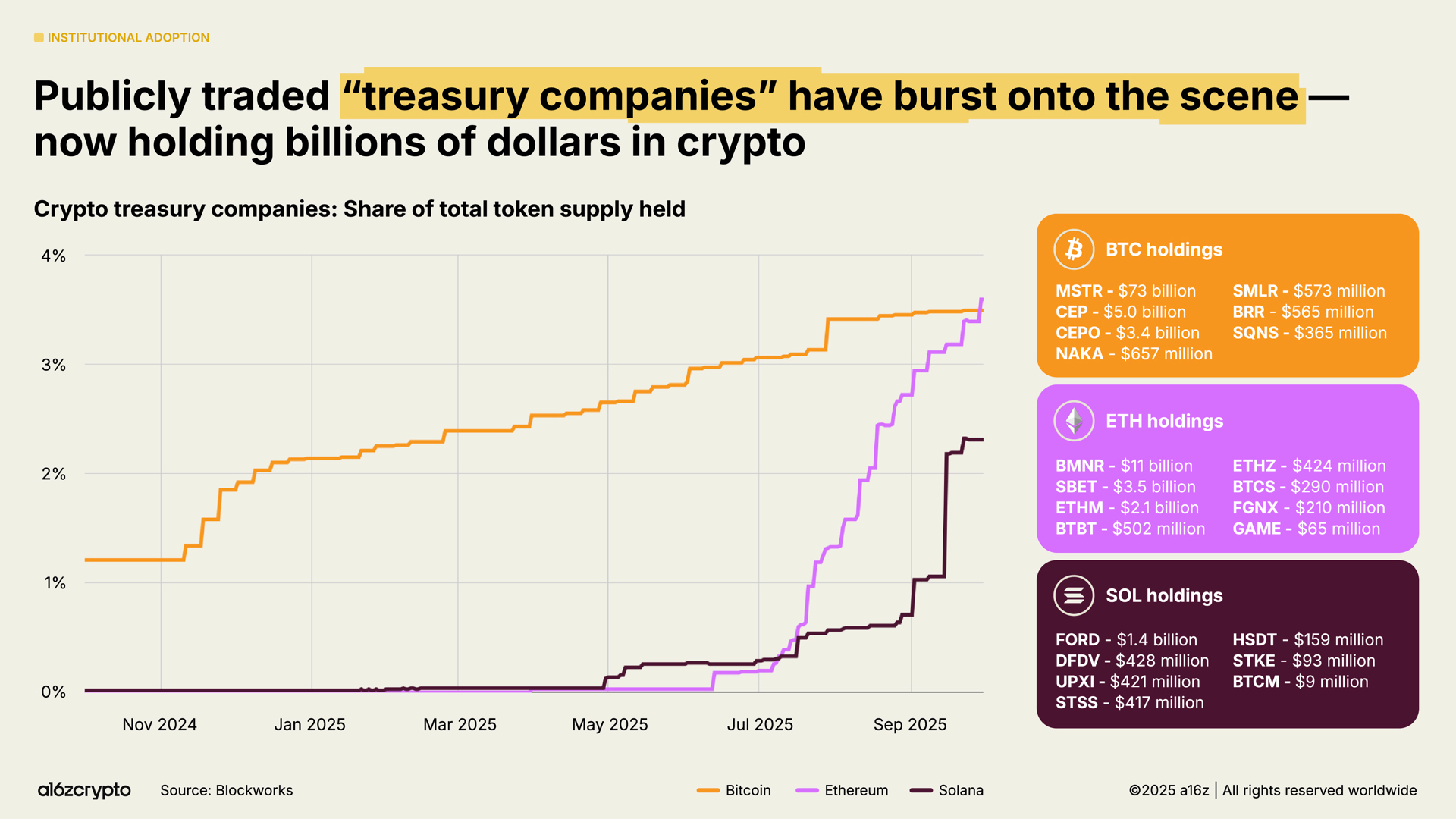

Publicly traded Digital Asset Treasury (DAT) companies continuously hold cryptocurrency on their balance sheets, just like corporate finance departments hold cash, currently holding about 4% of the circulating supply of Bitcoin and Ethereum. These DATs, along with exchange-traded products, currently hold about 10% of the token supply of Bitcoin and Ethereum.

Stablecoins Have Become Mainstream

Nothing signifies the maturity of cryptocurrency in 2025 more than the rise of stablecoins. In recent years, stablecoins were primarily used for settling speculative cryptocurrency trades; however, in recent years, they have become the fastest, cheapest, and most global way to transfer dollars—transferring to almost anywhere in the world in less than a second and for less than a cent.

This year, they have become the backbone of the on-chain economy.

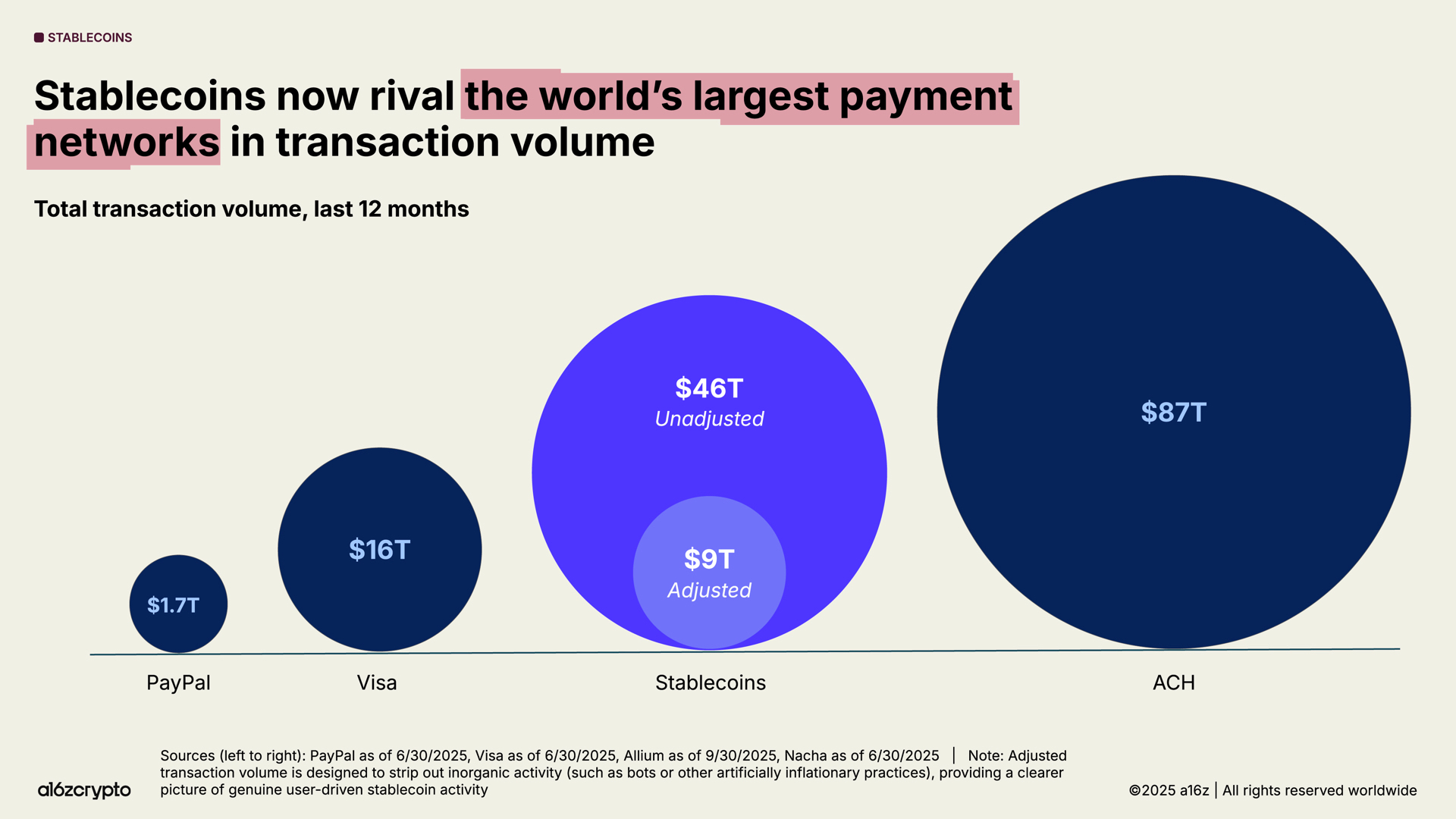

Stablecoin's total transaction volume reached $46 trillion last year, a year-on-year increase of 106%. Although this figure primarily represents financial flows (rather than retail payments through credit card networks), making direct comparisons difficult, it is nearly three times that of Visa and approaches the scale of the ACH network that covers the entire U.S. banking system. (Techub News note: The Automated Clearing House (ACH) is an electronic funds transfer network operating between U.S. financial institutions, processing batch transactions through computer technology and automated systems.)

After adjustments (a more accurate measure of organic activity designed to filter out bot and other artificial inflation activities), stablecoins' transaction volume over the past 12 months has reached $9 trillion, a year-on-year increase of 87%. This is more than five times PayPal's transaction volume and accounts for over half of Visa's transaction volume.

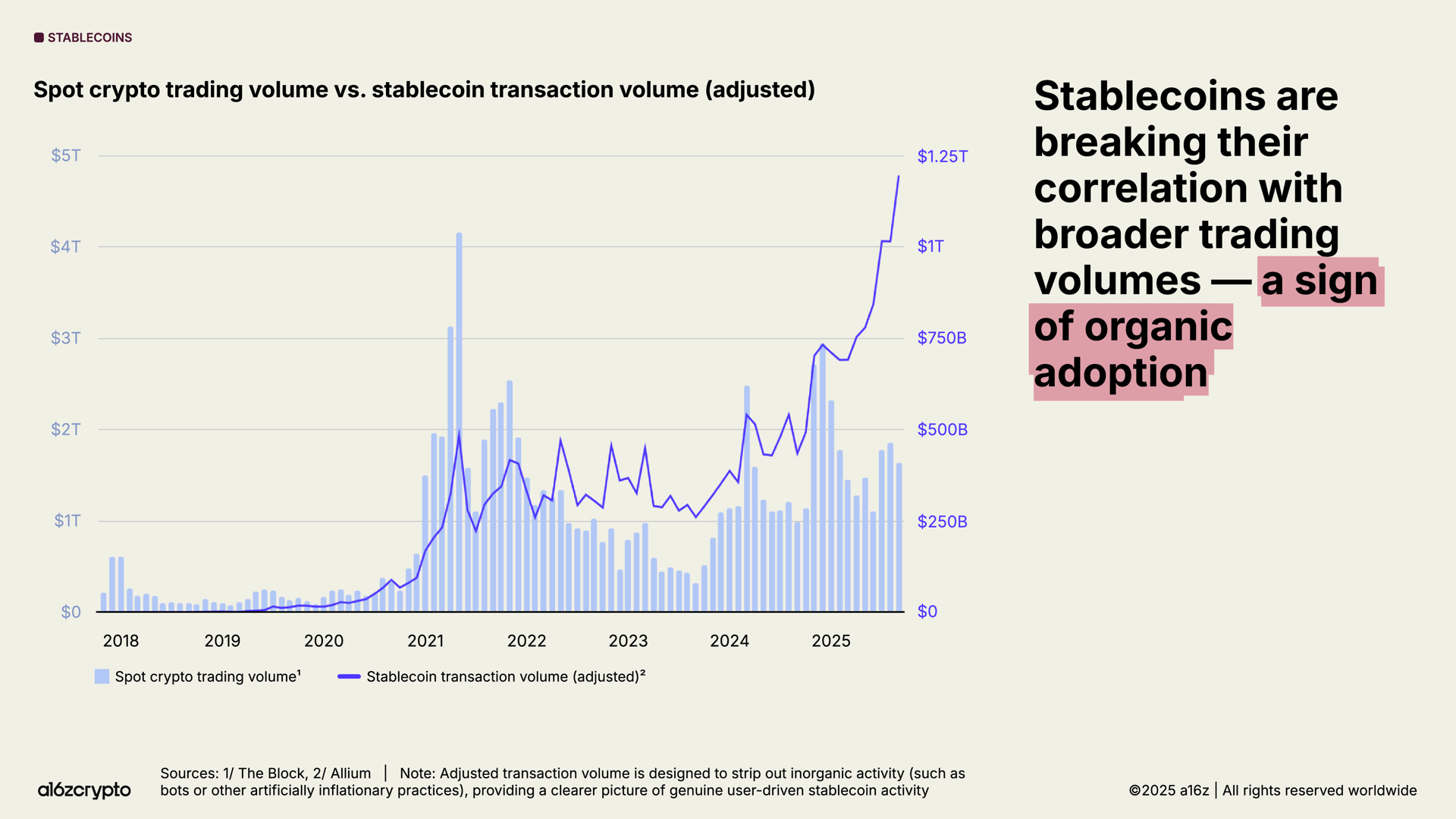

The adoption rate of stablecoins is accelerating. Monthly adjusted stablecoin transaction volume has surged to an all-time high, nearing $1.25 trillion in September 2025 alone.

Notably, this activity is largely unrelated to broader cryptocurrency transaction volumes, indicating that the use of stablecoins is non-speculative and, more importantly, that their products fit well with the market.

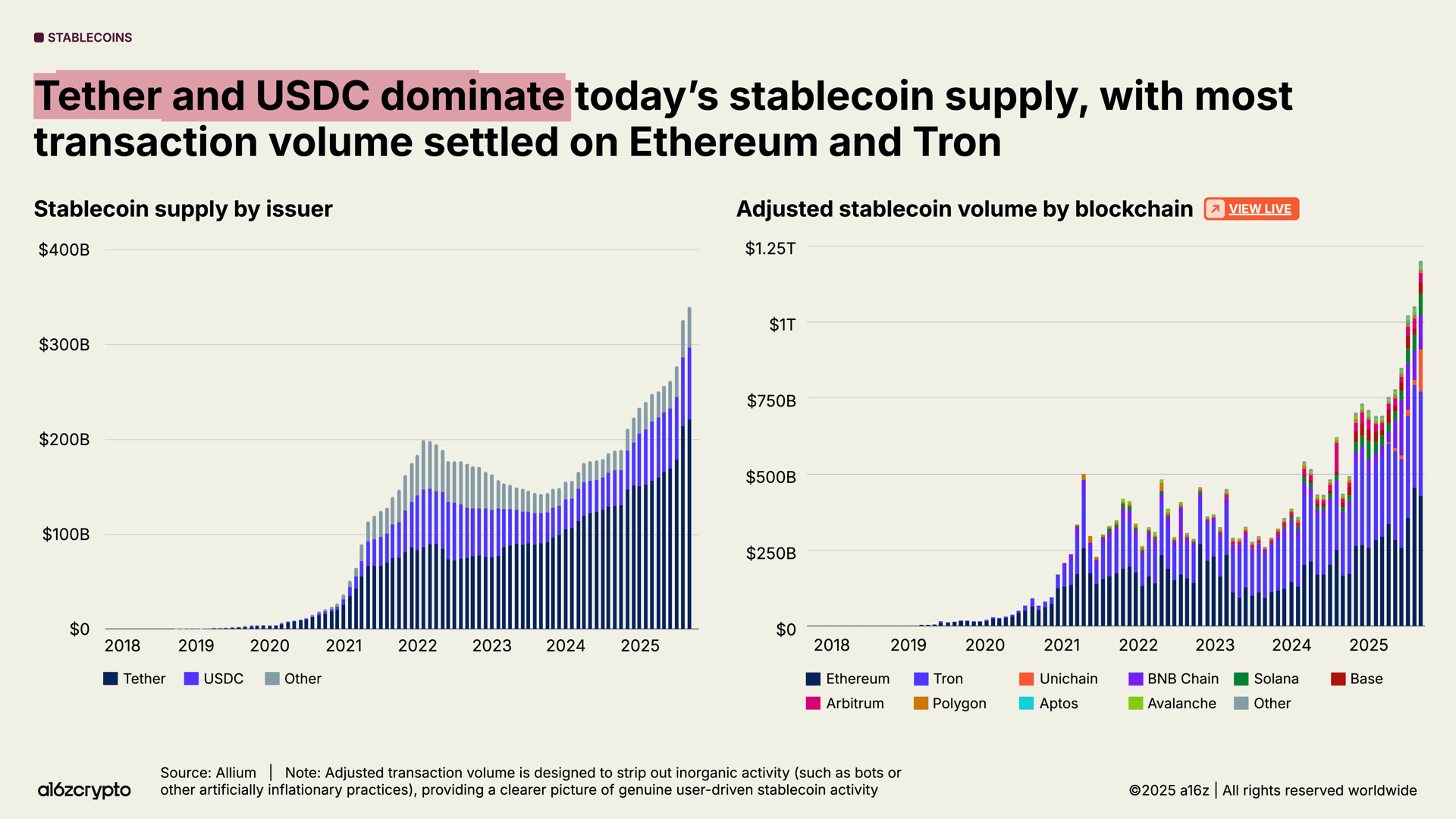

The total supply of stablecoins has also reached a historic high, now exceeding $300 billion.

The largest stablecoins dominate the market: Tether and USDC account for 87% of the total supply. In September 2025, the adjusted transaction volume of stablecoins settled on the Ethereum and Tron blockchains reached $772 billion, accounting for 64% of the total transaction volume. While these two issuers and blockchains dominate stablecoin transactions, the growth of new blockchains and new issuers is also accelerating.

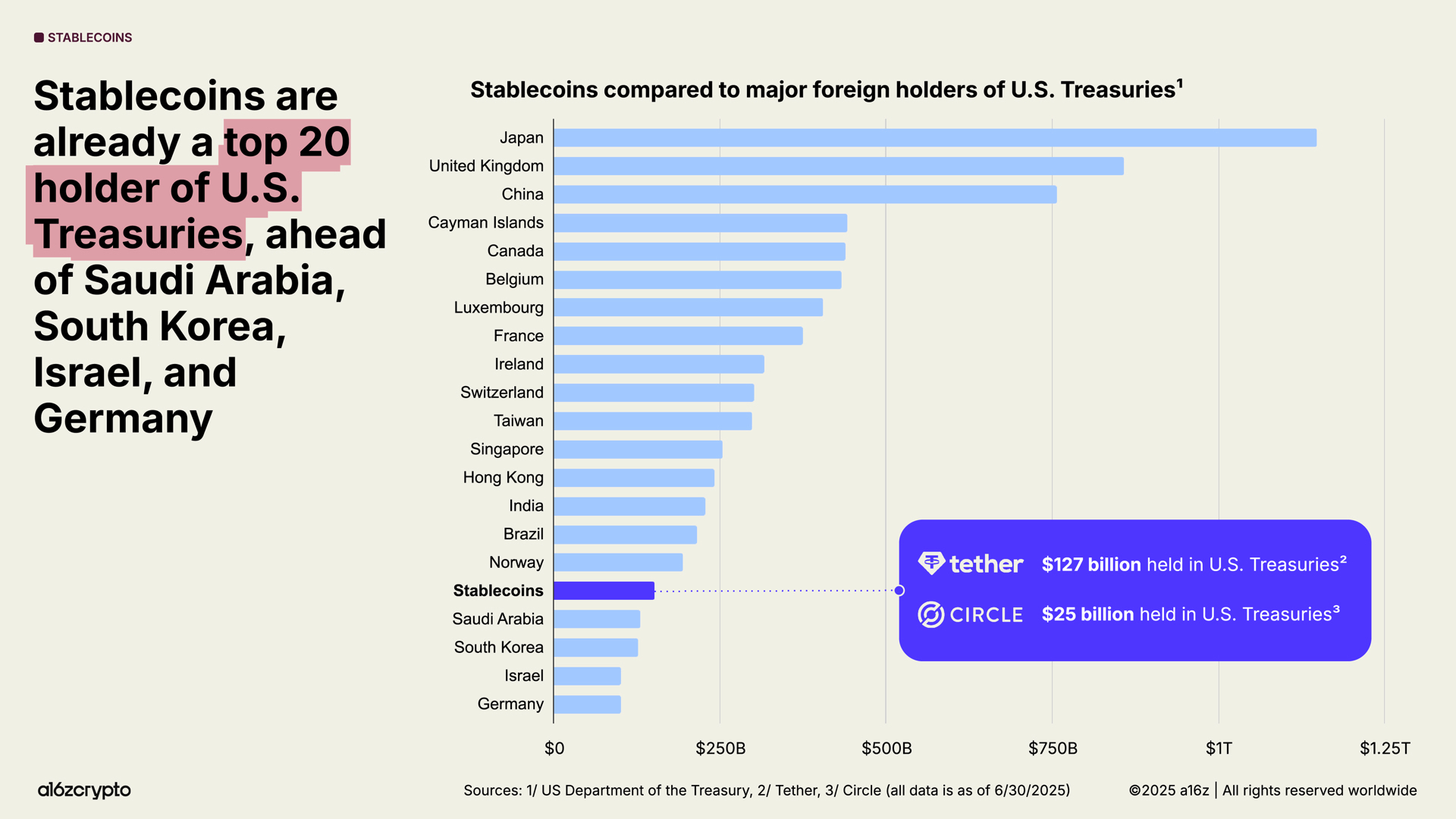

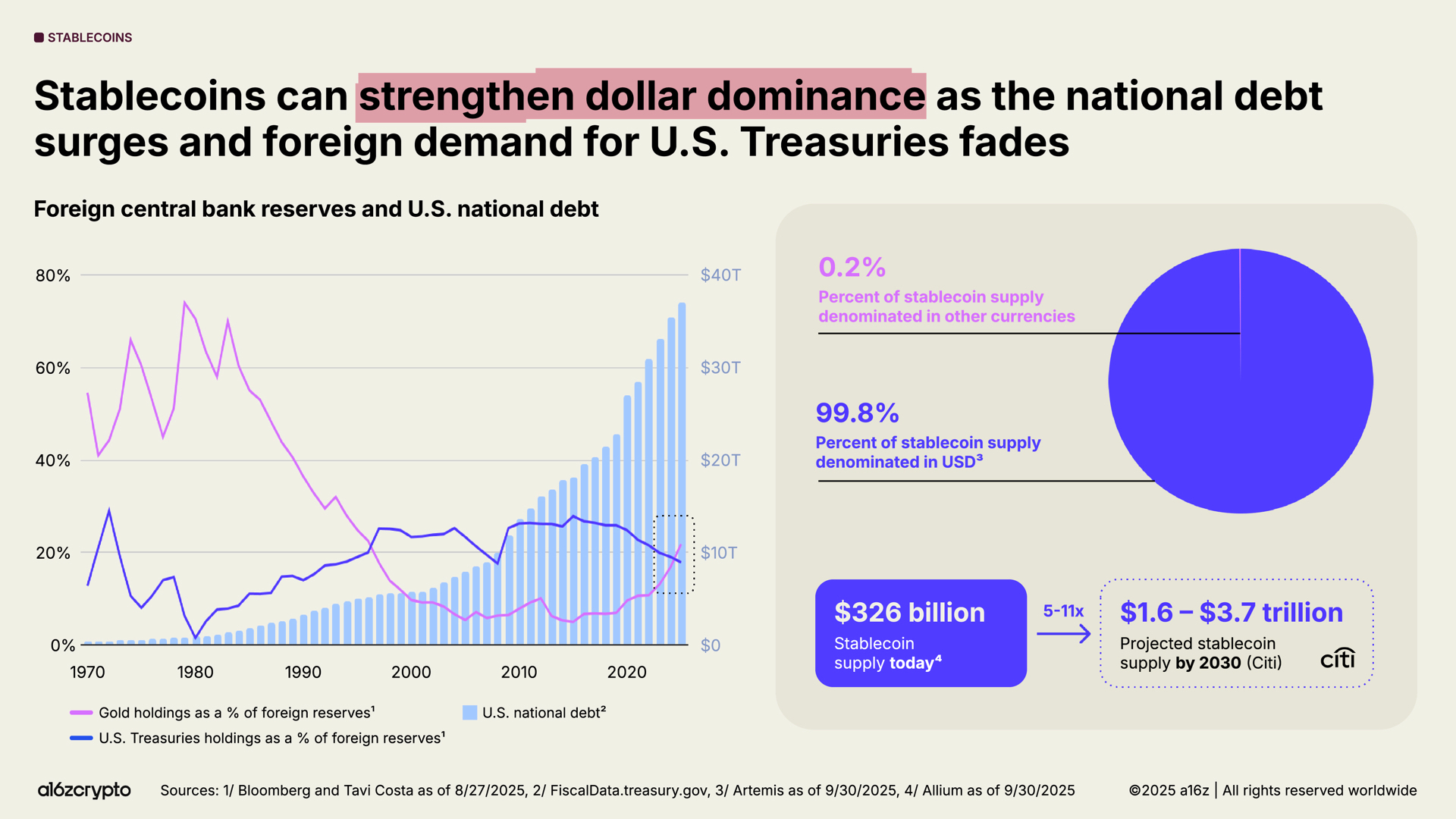

Stablecoins have now become a force in the global macroeconomy: currently, over 1% of dollars exist in tokenized stablecoin form on public chains, and the amount of U.S. Treasury bonds held by stablecoins has risen from 20th place last year to 17th place this year. Moreover, stablecoins collectively hold over $150 billion in U.S. Treasury bonds, surpassing the bond holdings of many sovereign nations.

Meanwhile, despite weakening global demand for U.S. Treasury bonds, the scale of U.S. Treasury bonds continues to soar. For the first time in 30 years, foreign central banks' gold reserves have surpassed U.S. Treasury bonds.

However, stablecoins are going against the trend: over 99% of stablecoins are dollar-denominated, and they are expected to grow tenfold by 2030, exceeding $3 trillion, providing a strong and sustainable potential source of demand for U.S. debt in the coming years. Even if foreign central banks reduce their Treasury bond holdings, stablecoins continue to strengthen the dollar's dominance.

Cryptocurrency is Stronger in the U.S. Than Ever Before

The U.S. has shifted from its previously hostile stance toward cryptocurrency, revitalizing investor confidence.

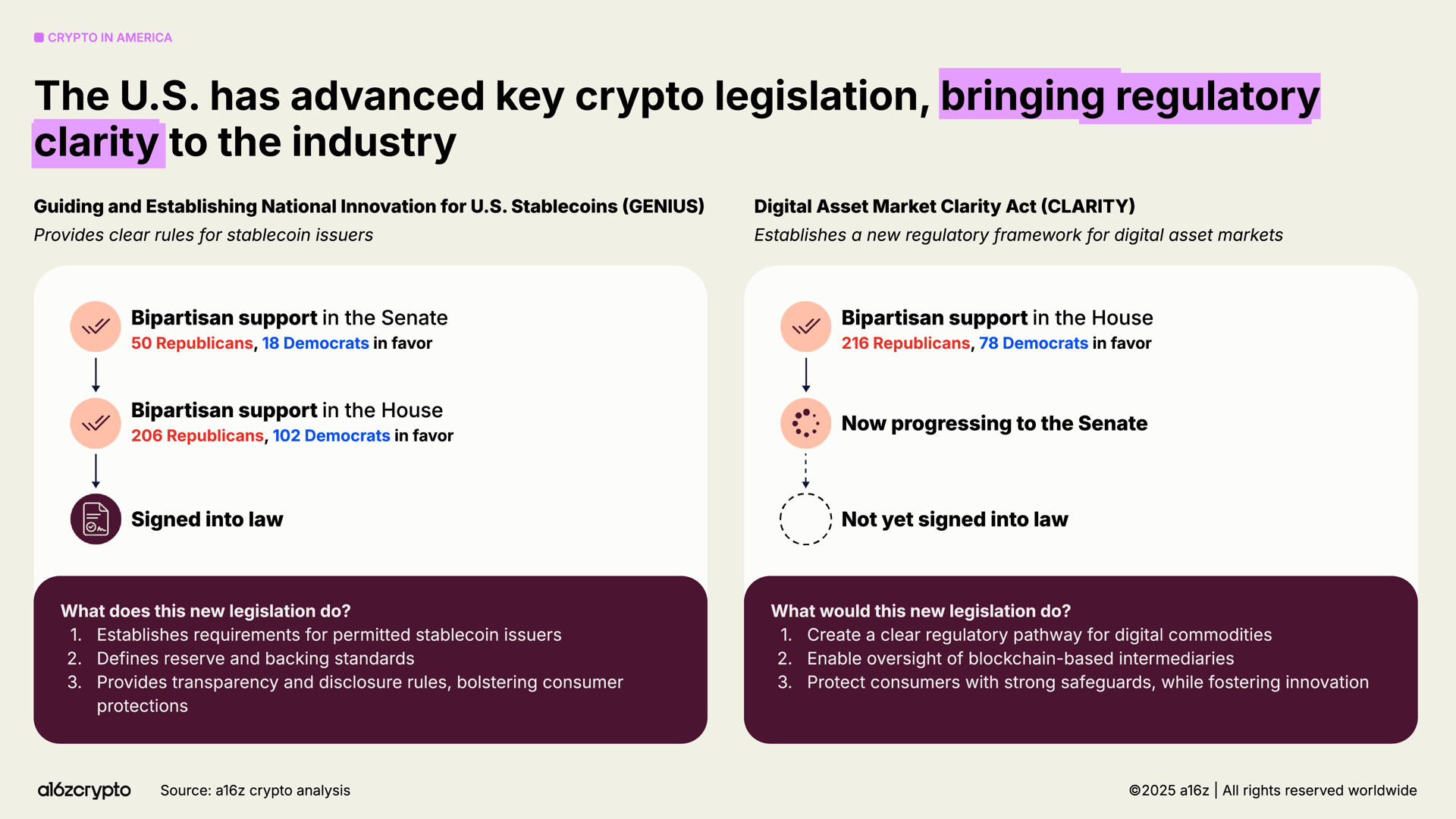

This year, the passage of the GENIUS Act and the House's approval of the CLARITY Act marked a bipartisan consensus that cryptocurrency will not only continue to exist in the U.S. but is expected to thrive. These bills collectively build a regulatory framework for stablecoins, market structure, and digital assets, balancing innovation with investor protection. Additionally, Executive Order 14178 supplements these bills by overturning previous anti-cryptocurrency directives and establishing an interagency working group to advance the modernization of federal digital asset policy.

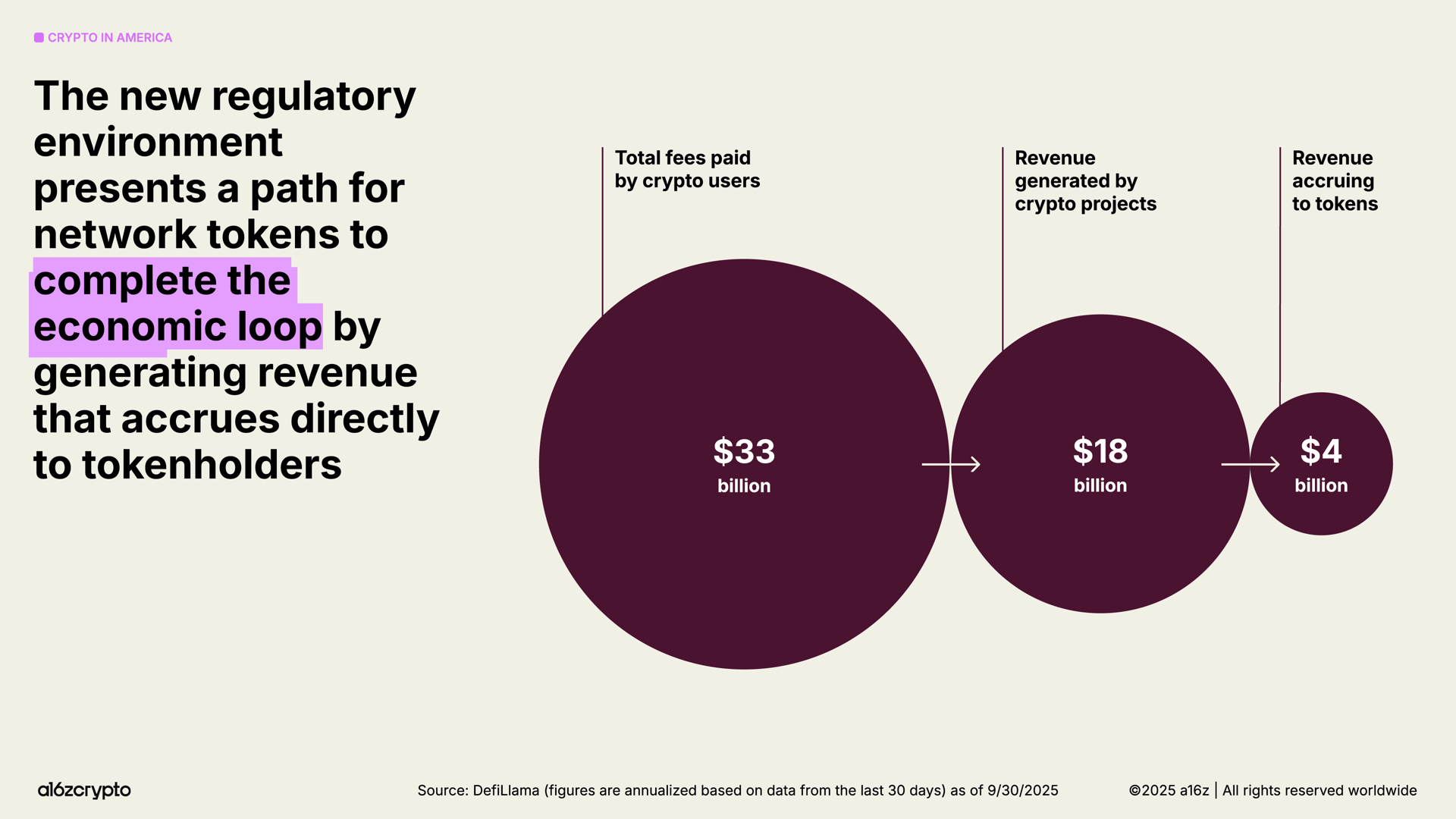

The regulatory environment is paving the way for builders to fully realize the potential of tokens as a new digital primitive, similar to websites in earlier generations of the internet. With clearer regulations, more network tokens will be able to complete their economic cycles by generating revenue that will belong to token holders, thereby creating a new economic engine for the internet that can sustain itself and allow more users to have stakes in the system.

The World is Moving On-Chain

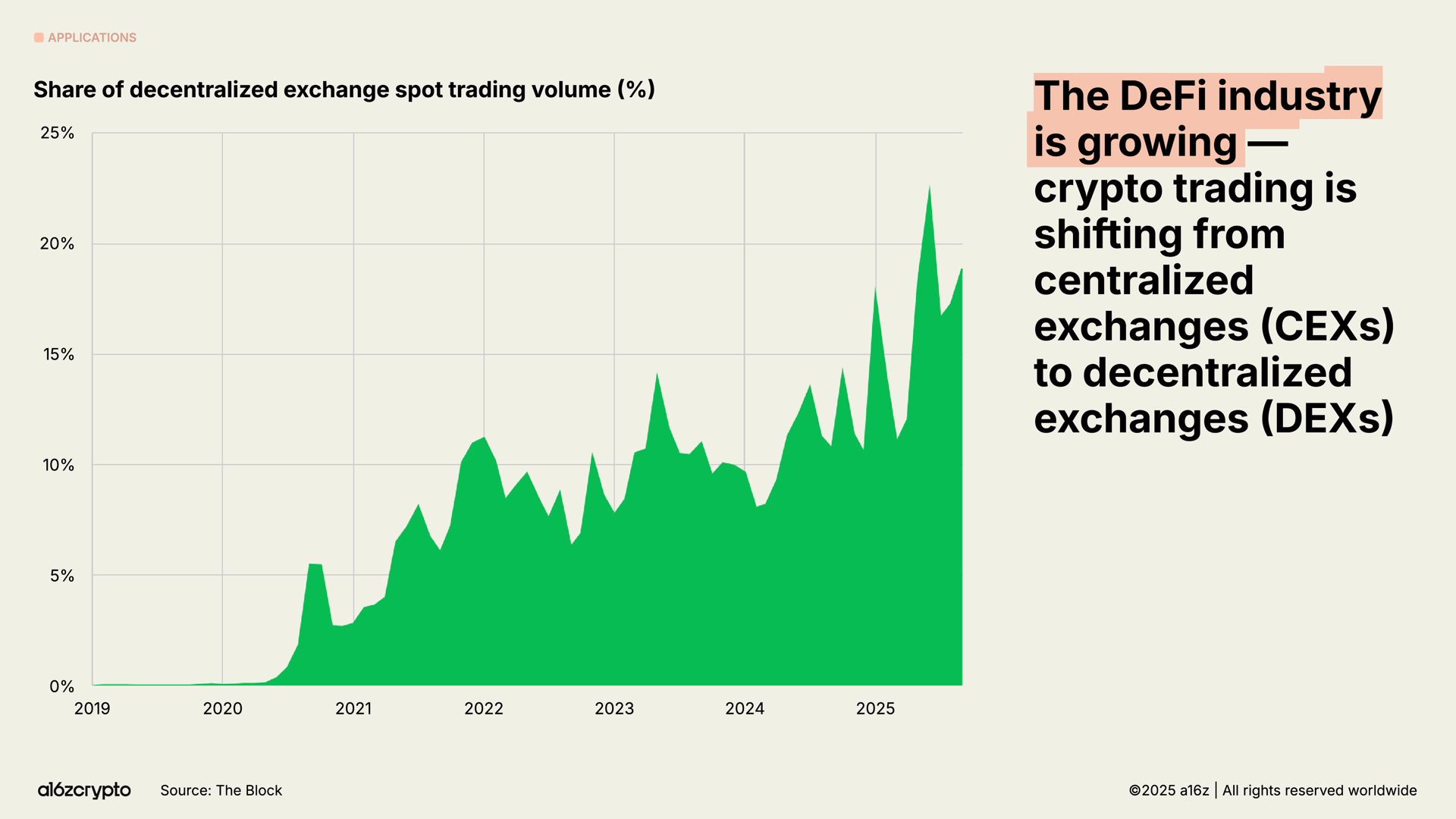

The on-chain economy, once a "niche playground" for early adopters, has now evolved into a multi-domain market with tens of millions of participants each month. Currently, nearly one-fifth of spot trading volume occurs on decentralized exchanges.

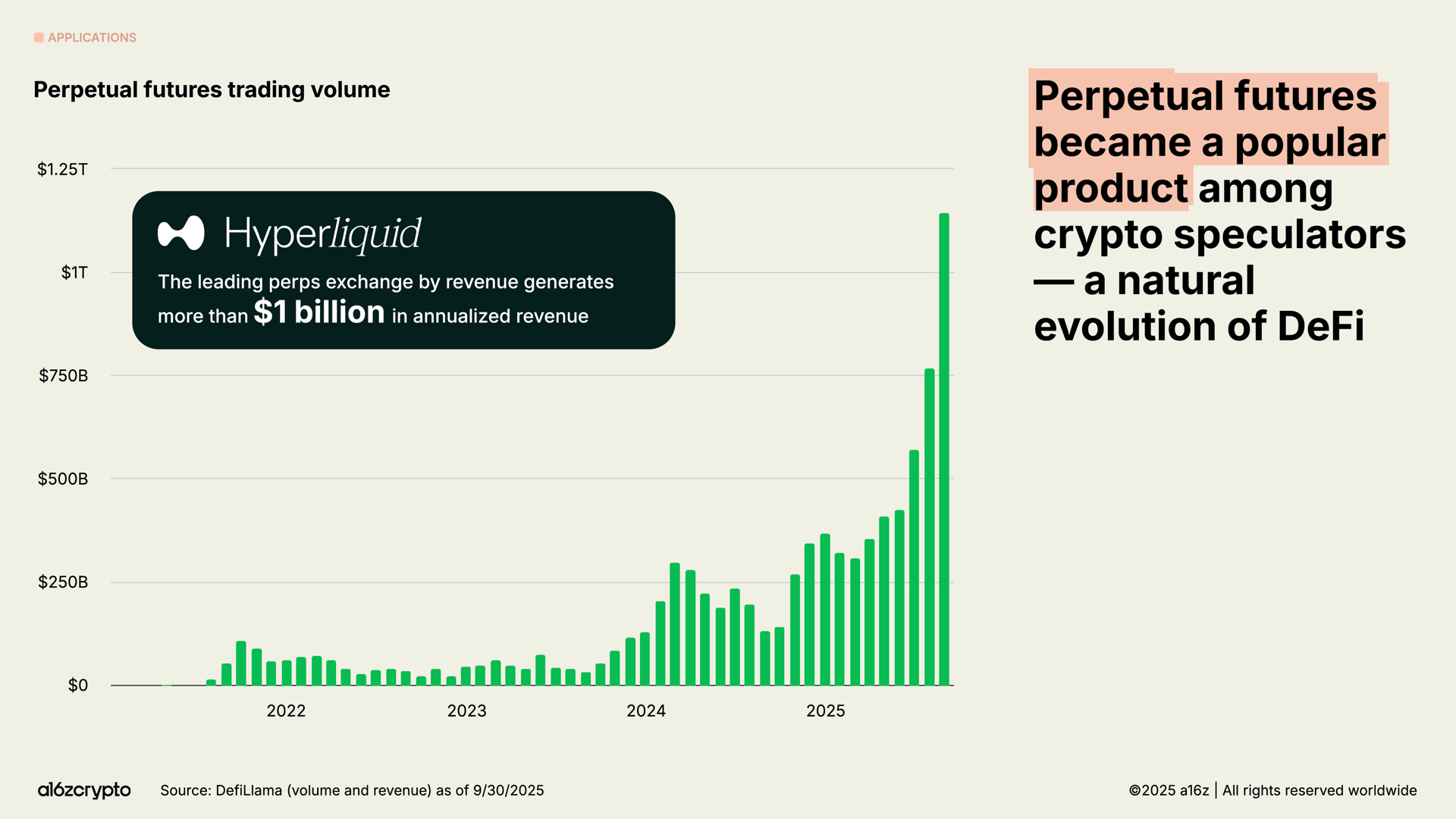

The trading volume of perpetual futures has grown nearly eightfold in the past year, exploding among cryptocurrency speculators. Decentralized perpetual futures exchanges like Hyperliquid have processed trillions of dollars in transactions, with annualized revenue exceeding $1 billion this year—numbers that rival some centralized exchanges.

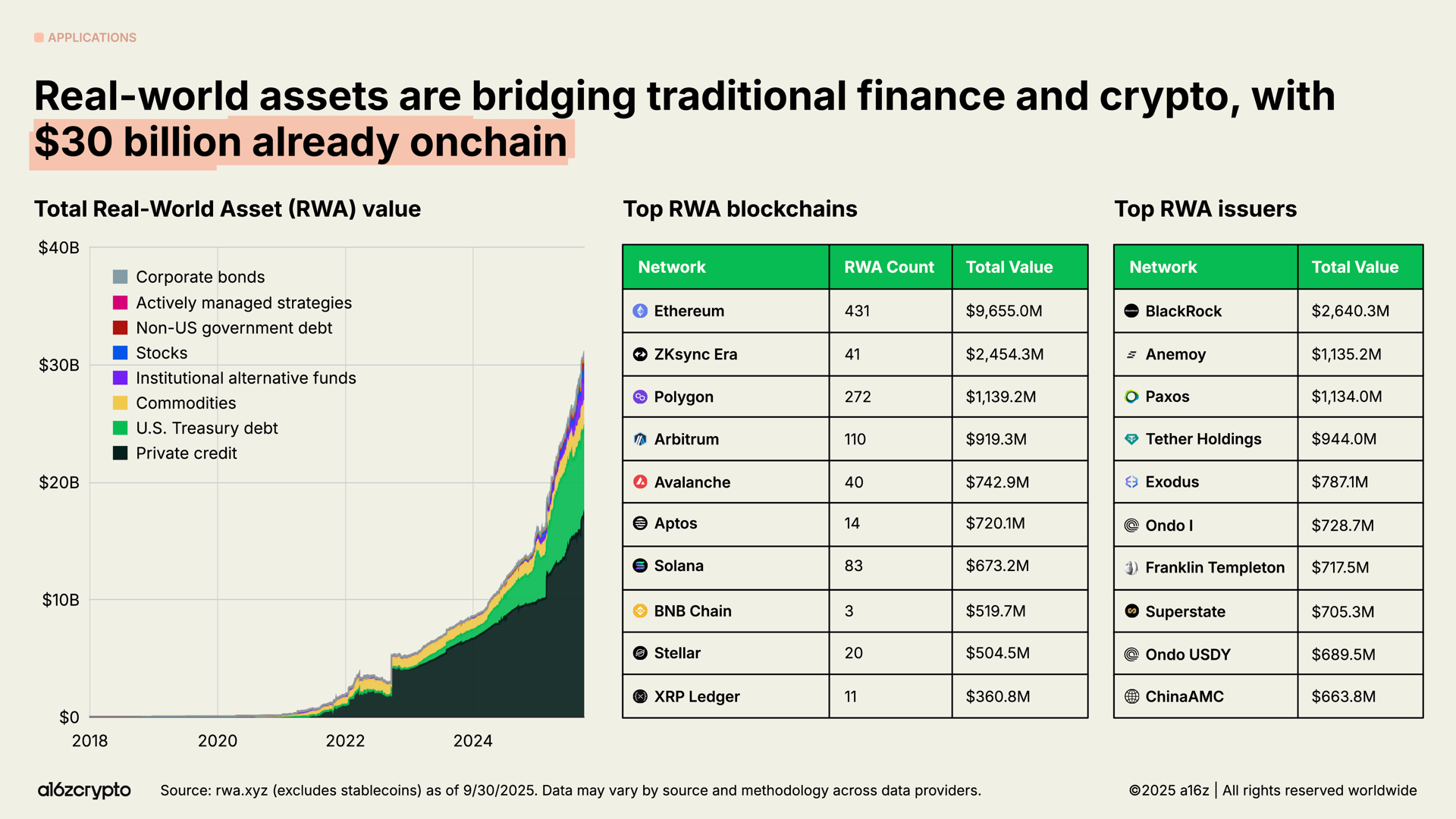

In terms of real-world assets (RWAs), traditional assets such as U.S. Treasury bonds, money market funds, private credit, and real estate are being tokenized on-chain—connecting cryptocurrency with traditional finance. The total market size for tokenized RWAs is $30 billion, having grown nearly fourfold in the past two years.

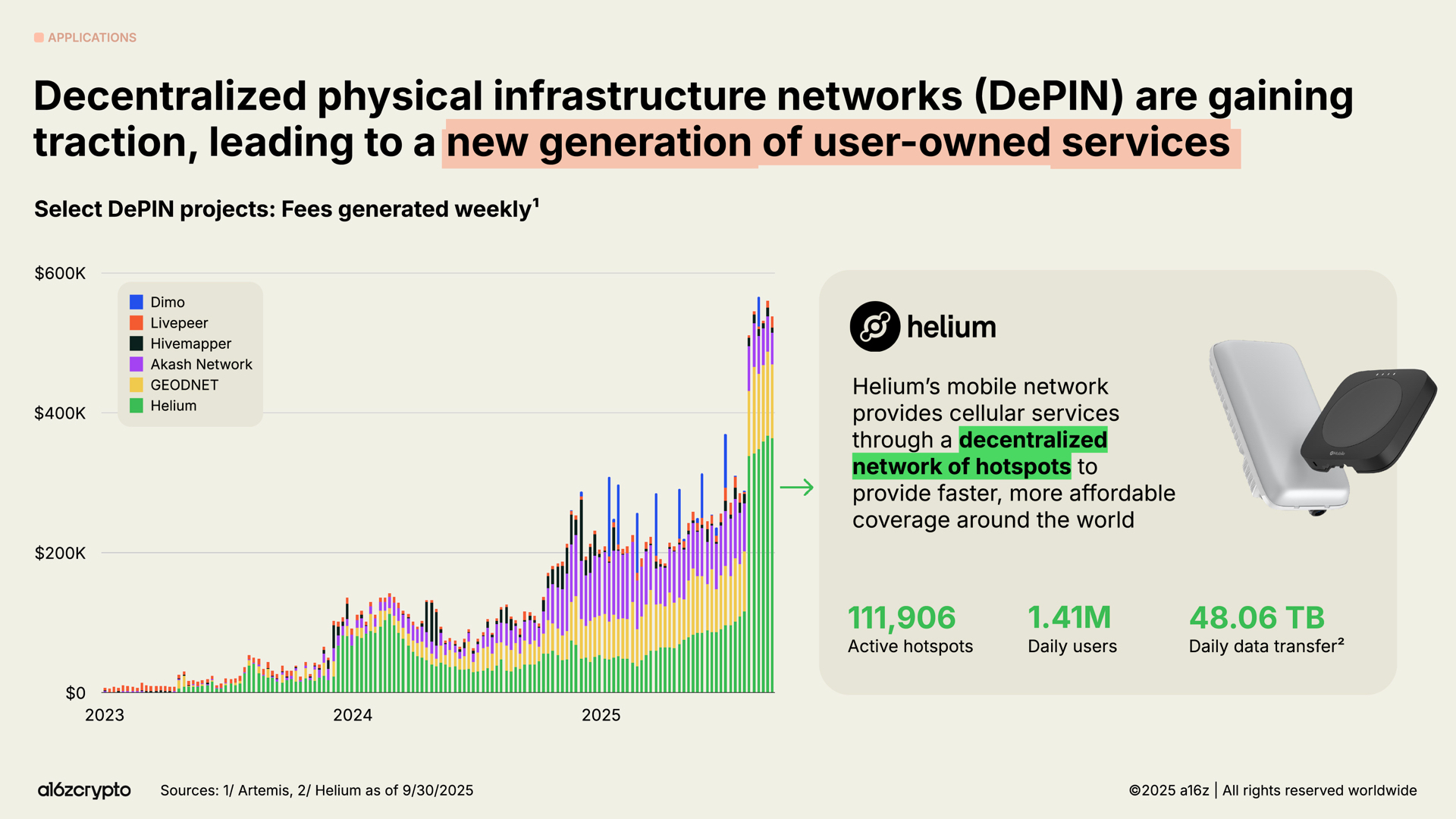

Beyond finance, one of the most ambitious frontiers for blockchain in 2025 is DePIN, or decentralized physical infrastructure networks.

DeFi is reshaping finance, while DePIN is transforming physical infrastructure, including telecommunications and transportation networks, energy networks, and more. The opportunities for DePIN are immense; the World Economic Forum has predicted that by 2028, the market size for DePIN will grow to $3.5 trillion.

The Helium network is one of the most notable examples. This grassroots wireless network currently provides 5G cellular coverage for 1.4 million daily active users operating over 111,000 hotspots.

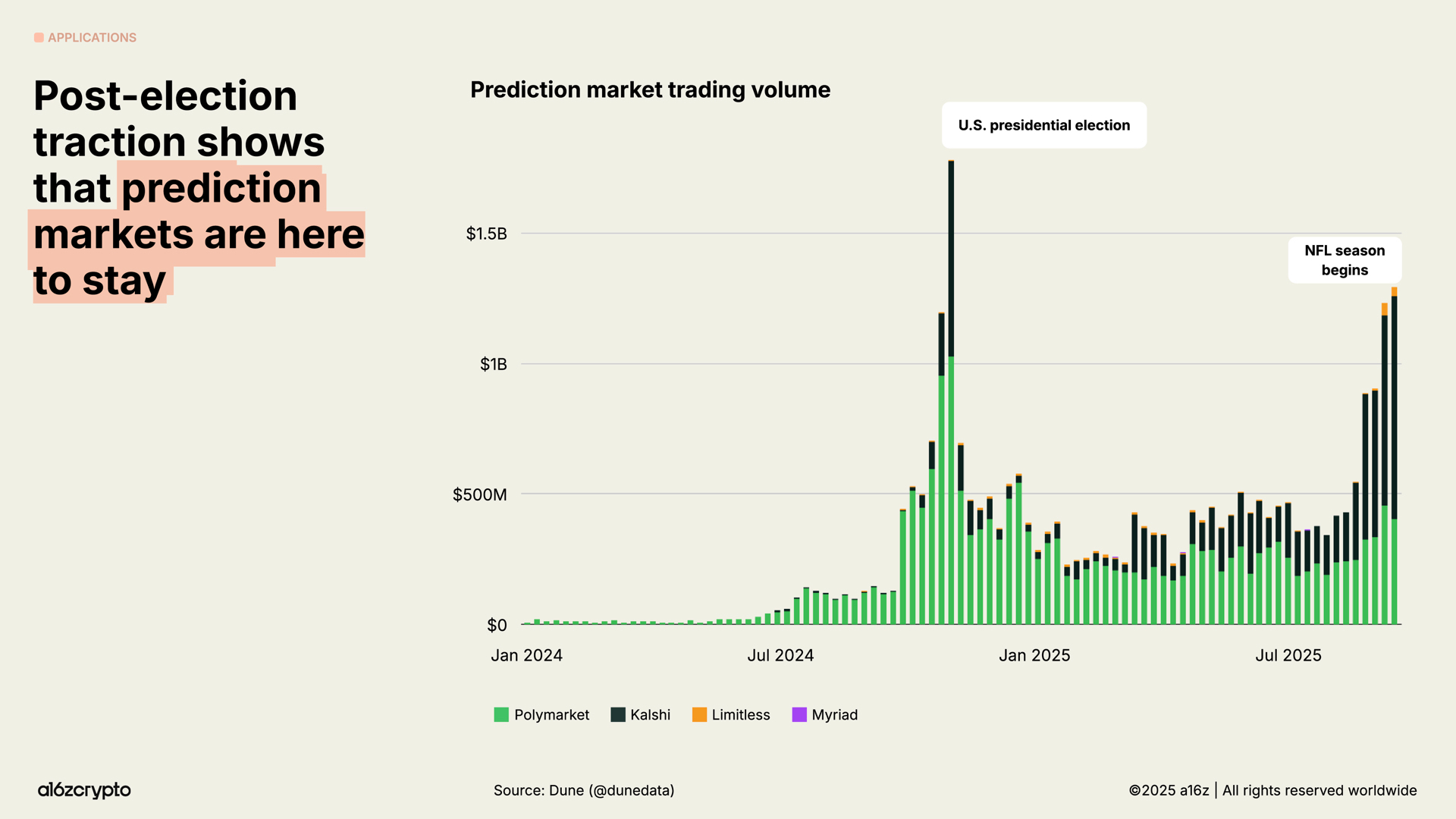

During the 2024 U.S. presidential election, prediction markets are entering the mainstream, with the most popular platforms Polymarket and Kalshi seeing monthly trading volumes totaling billions of dollars. Although there are doubts about whether these platforms can maintain activity beyond election years, their trading volumes have grown nearly fivefold since the beginning of 2025, approaching historical highs.

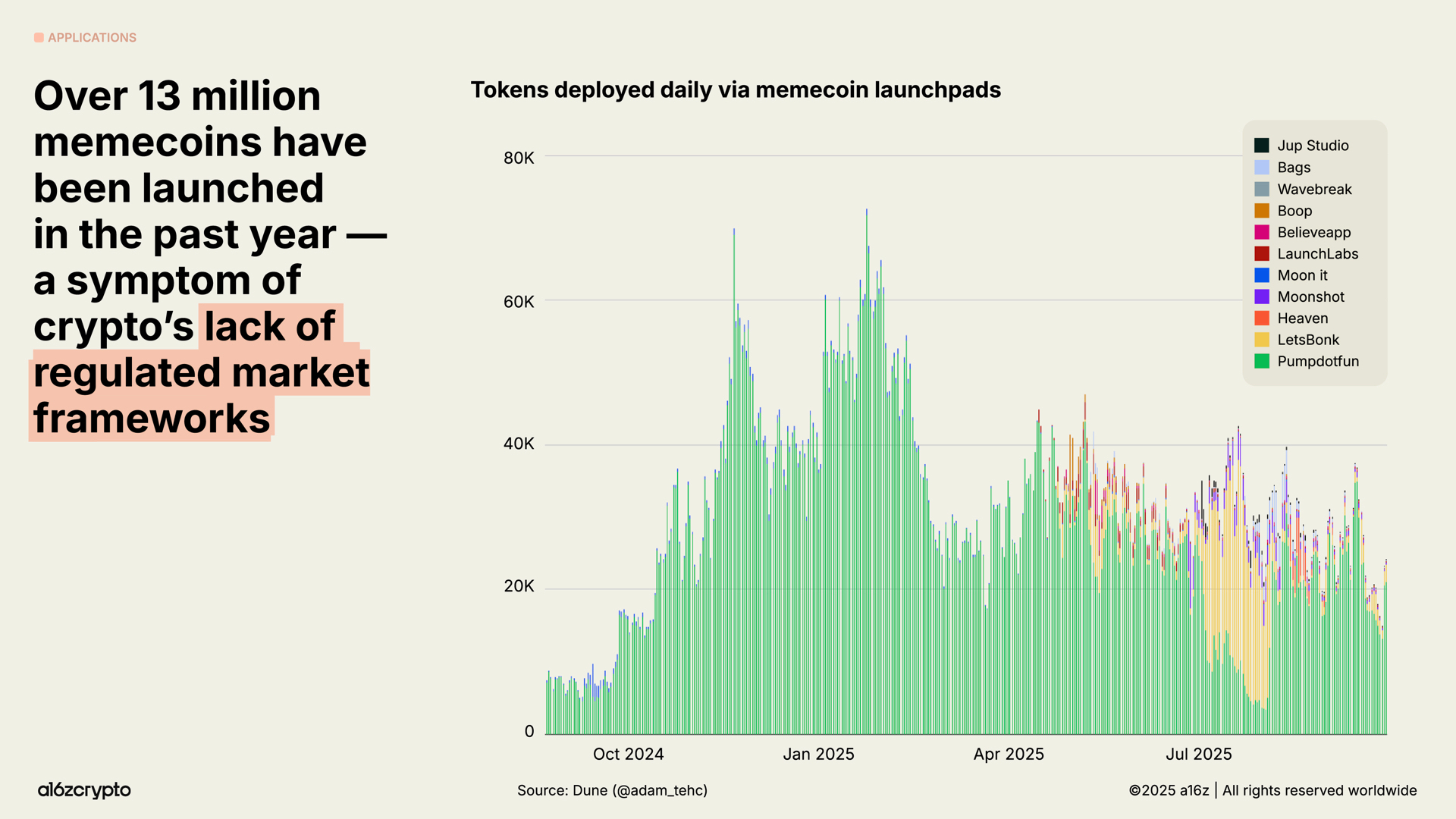

In the absence of clear regulations, meme coins have thrived. Last year, over 13 million meme coins were issued. In recent months, this trend seems to have cooled, with September's issuance down 56% from January. This is also due to sound policies and bipartisan legislation paving the way for more efficient blockchain use cases.

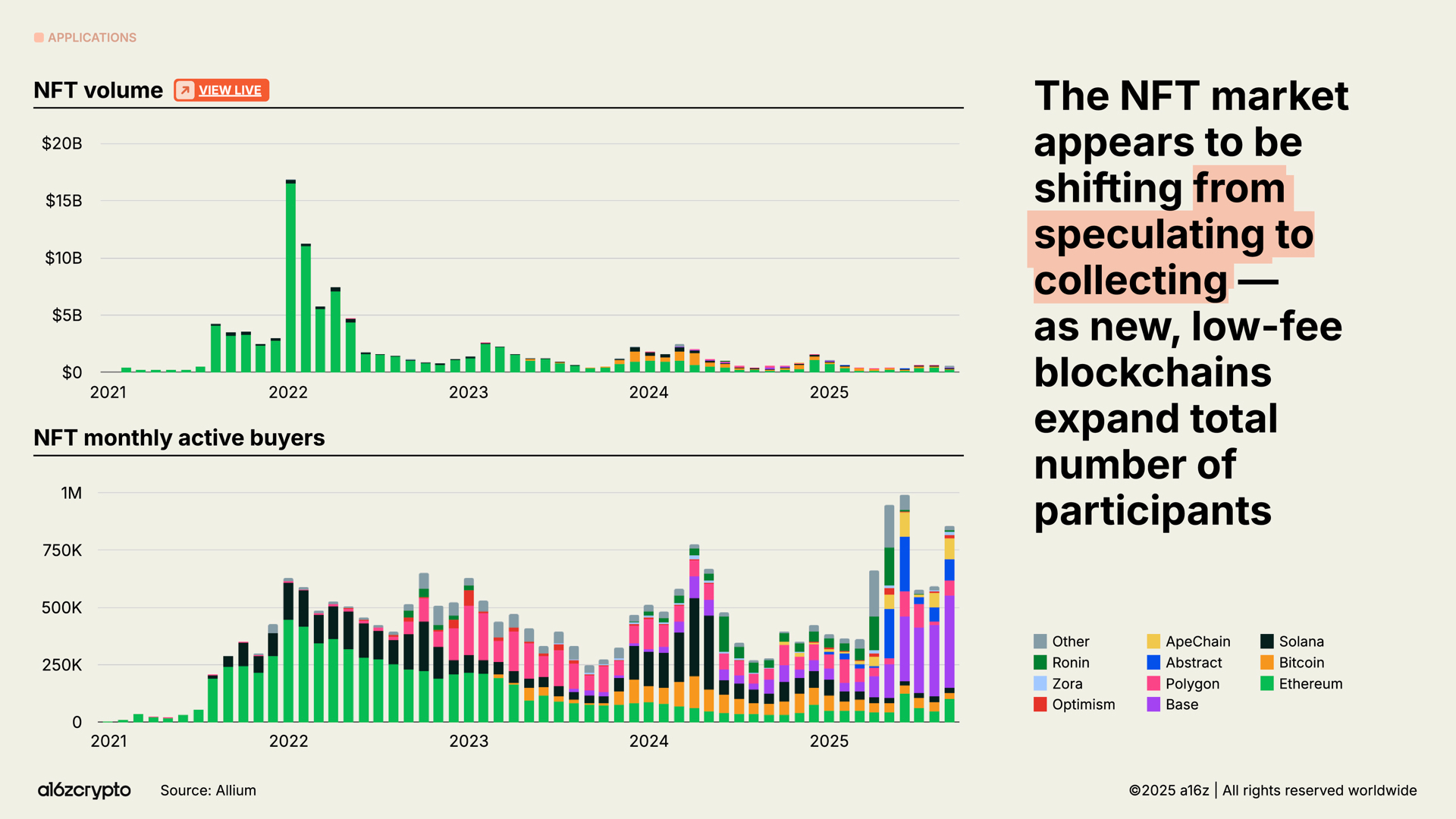

The NFT market size has yet to reach its peak in 2022, but the number of monthly active buyers has been increasing. These trends seem to indicate a shift in consumer behavior from speculation to collecting, aided by the emergence of cheaper cross-chain platforms like Solana and Base.

Blockchain Infrastructure is (Almost) Ready for Prime Time

None of the above activities would be possible without significant advancements in blockchain infrastructure.

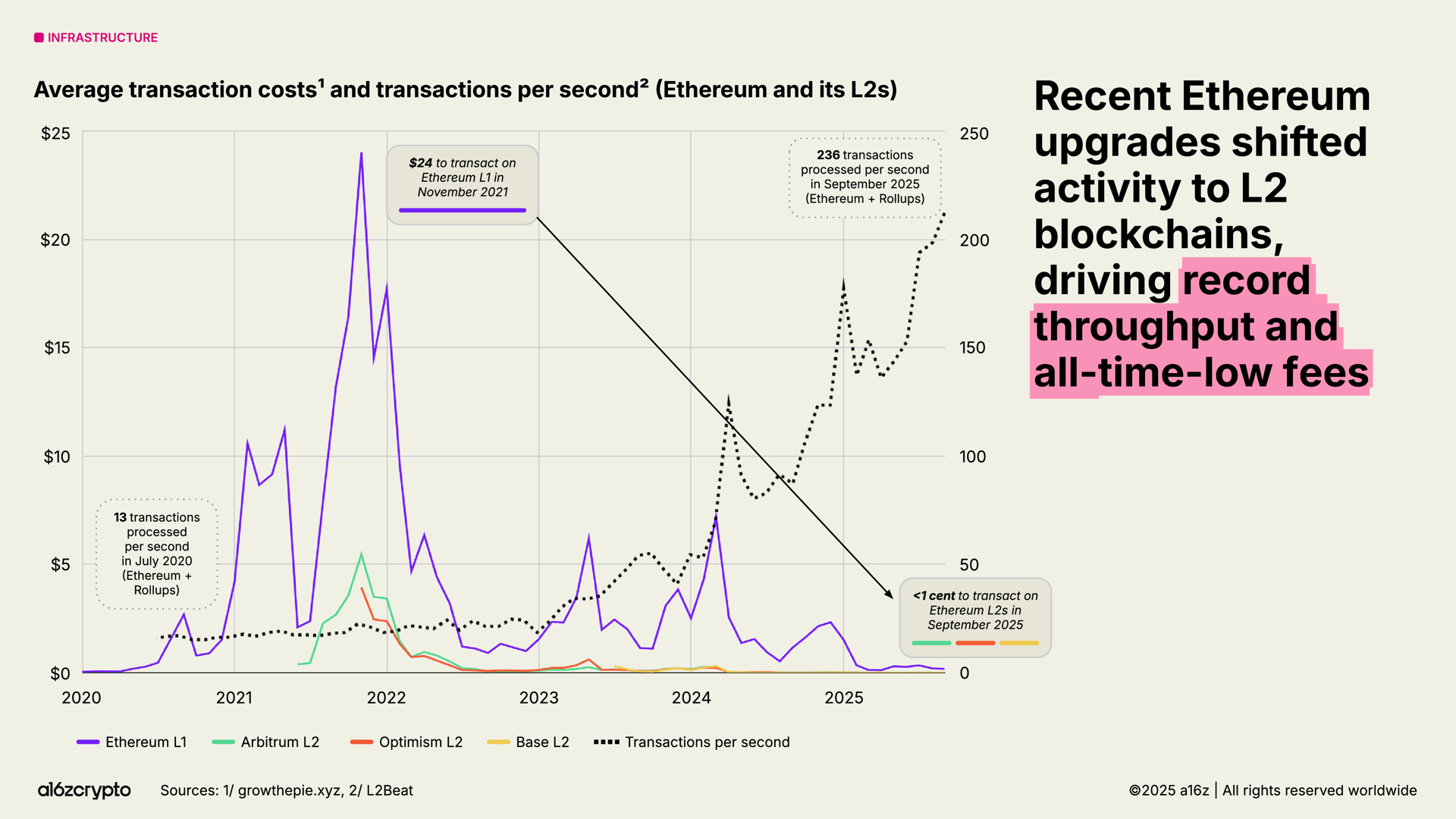

In just five years, the total transaction throughput of major blockchain networks has increased more than 100 times. At that time, blockchains processed fewer than 25 transactions per second. Today, they handle 3,400 transactions per second, comparable to the global throughput of Nasdaq or Stripe on "Black Friday," and at a cost that is only a small fraction of historical levels.

Among the many blockchain ecosystems, Solana has emerged as one of the most prominent. Its high-performance, low-fee architecture now supports a variety of applications, from DePIN projects to NFT markets, with its native applications generating $3 billion in revenue over the past year. By the end of the year, Solana's upgrade plans are expected to double the network's capacity.

Ethereum continues to advance its scalability roadmap, with much of the economic activity migrating to Layer-2 solutions such as Arbitrum, Base, and Optimism. The average transaction cost on Layer-2 has dropped from around $24 in 2021 to less than 1 cent today, making Ethereum-linked block space cheap and abundant.

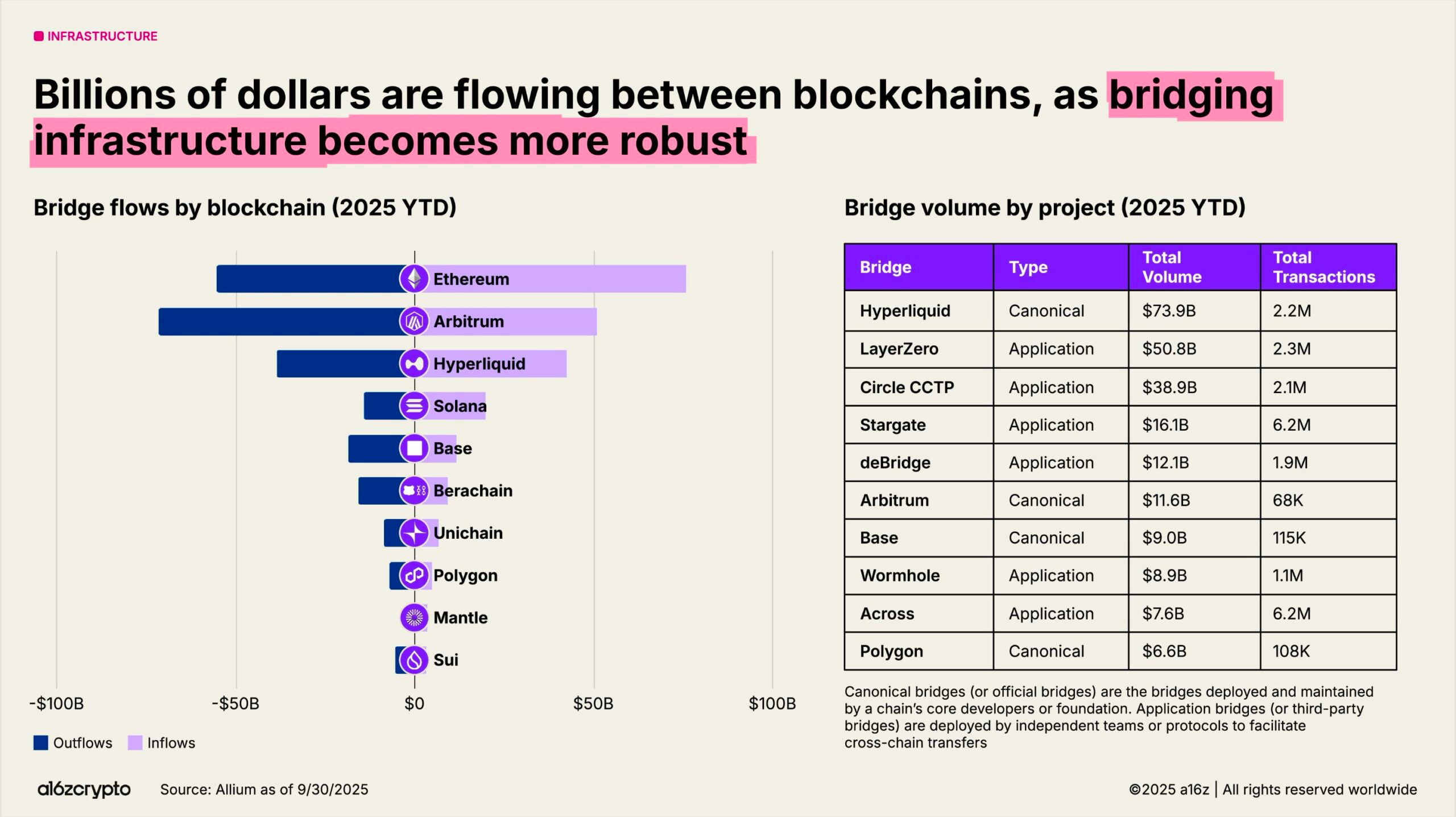

Cross-chain bridges enable interoperability between blockchains. Protocols like LayerZero and Circle's cross-chain transfer protocol allow users to move assets across multi-chain systems. Hyperliquid's standardized cross-chain bridge has also reached a transaction volume of $74 billion so far this year.

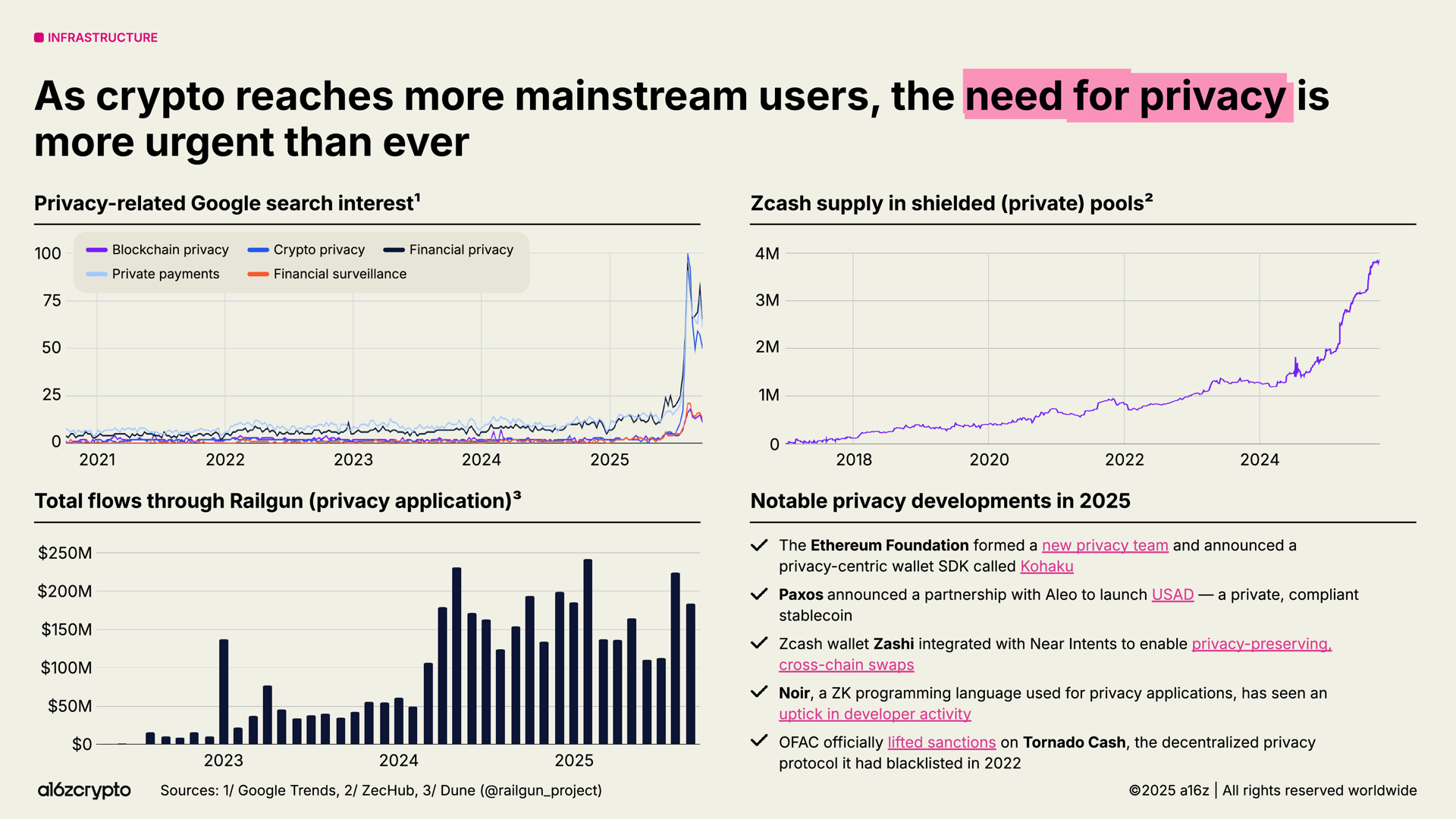

Additionally, privacy issues are regaining focus and may become a prerequisite for broader applications. The following indicators suggest a growing interest in this issue: In 2025, Google searches related to crypto privacy surged; the supply of Zcash's shielded pool grew to nearly 4 million ZEC; and Railgun's monthly transaction volume exceeded $200 million.

More signs of development: The Ethereum Foundation has formed a new privacy team; Paxos has partnered with Aleo to launch a compliant private stablecoin (USAD); and the U.S. Office of Foreign Assets Control has lifted sanctions on the decentralized privacy protocol Tornado Cash. a16z expects that these cases indicate a trend that will gain greater momentum in the coming years as cryptocurrency continues to go mainstream.

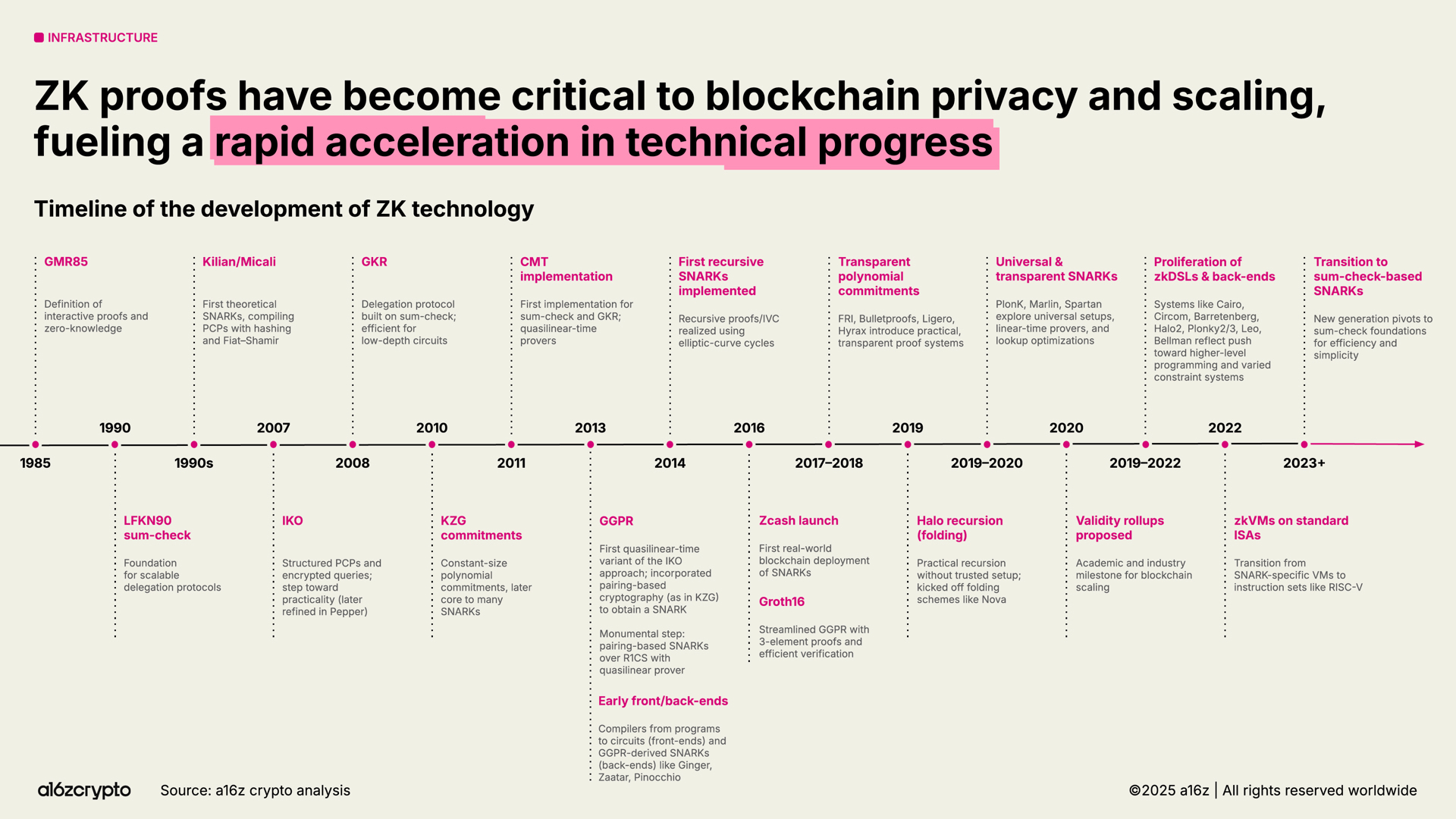

Similarly, zero-knowledge proofs (ZK) and succinct proof systems are rapidly evolving from academic research decades ago into critical infrastructure. Zero-knowledge systems are now integrated into Rollups, compliance tools, and even mainstream web services—Google's new ZK identity system is one example.

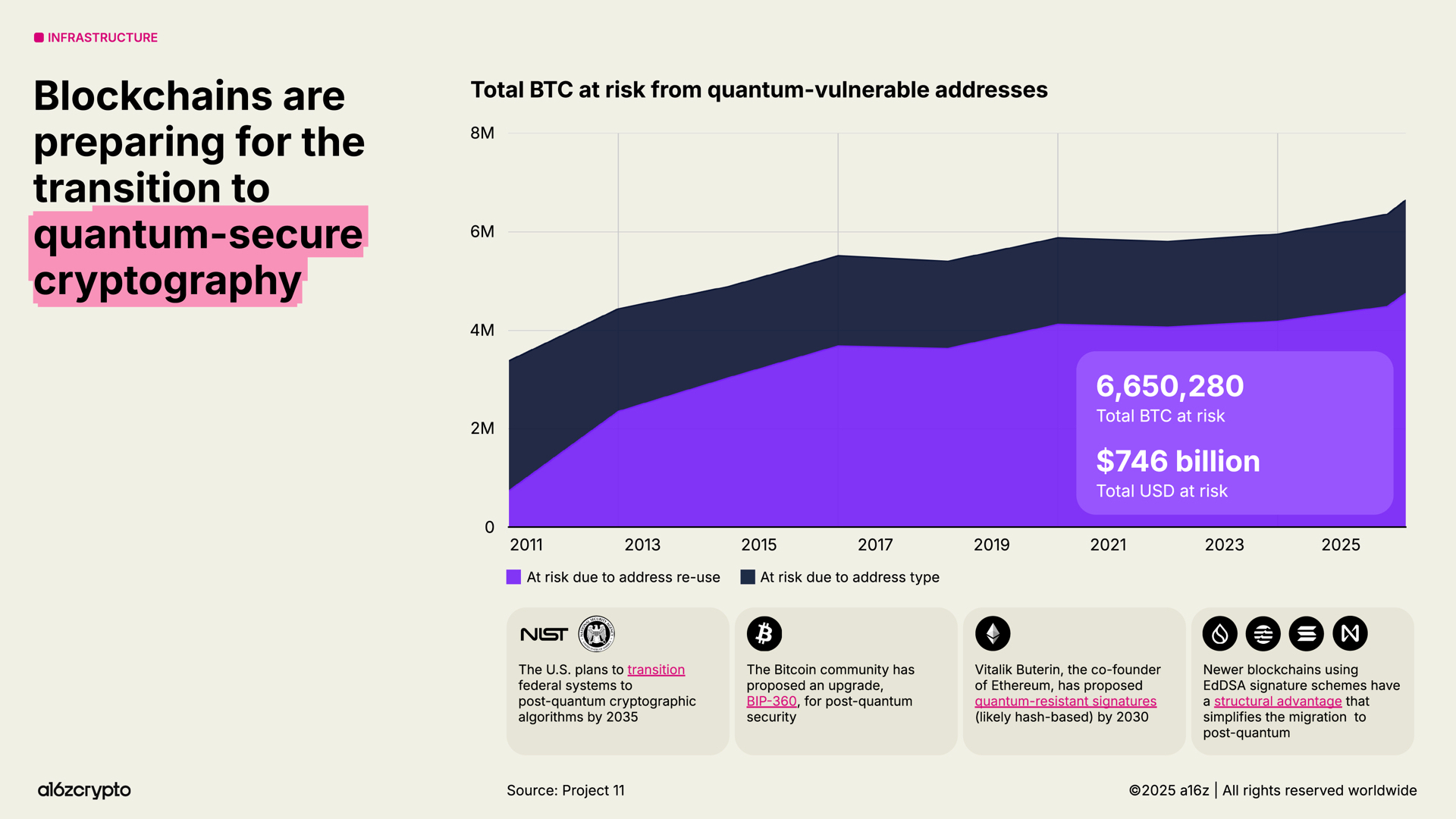

Notably, blockchain is accelerating the advancement of post-quantum roadmaps. Approximately $750 billion in Bitcoin is stored in addresses vulnerable to future quantum attacks. The U.S. government plans to transition federal systems to post-quantum cryptographic algorithms by 2035.

Artificial Intelligence and Cryptocurrency are Merging

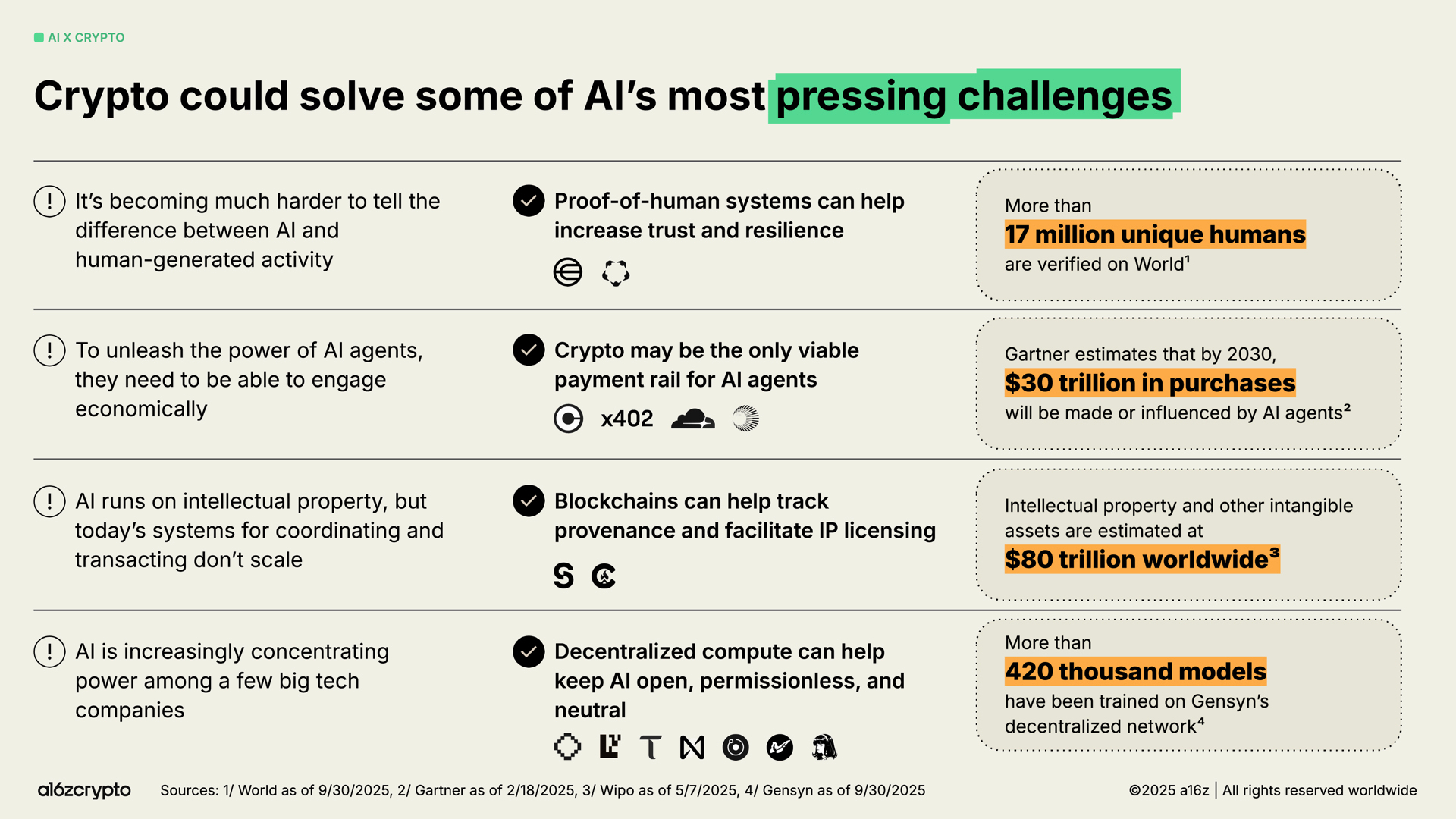

Among other advancements, the launch of ChatGPT in 2022 brought artificial intelligence into the public spotlight, presenting clear opportunities for cryptocurrency. From tracking sources and IP licensing to providing payment channels for agents, cryptocurrency could potentially address some of the most pressing challenges facing artificial intelligence.

Decentralized identity systems like World have verified the identities of over 17 million people, providing "proof of humanity" and helping to distinguish between humans and bots. Additionally, protocols like x402 are becoming potential financial backbones for autonomous AI agents, assisting them in making small transactions, accessing APIs, and settling payments without intermediaries. Gartner estimates that this economic scale could reach $30 trillion by 2030.

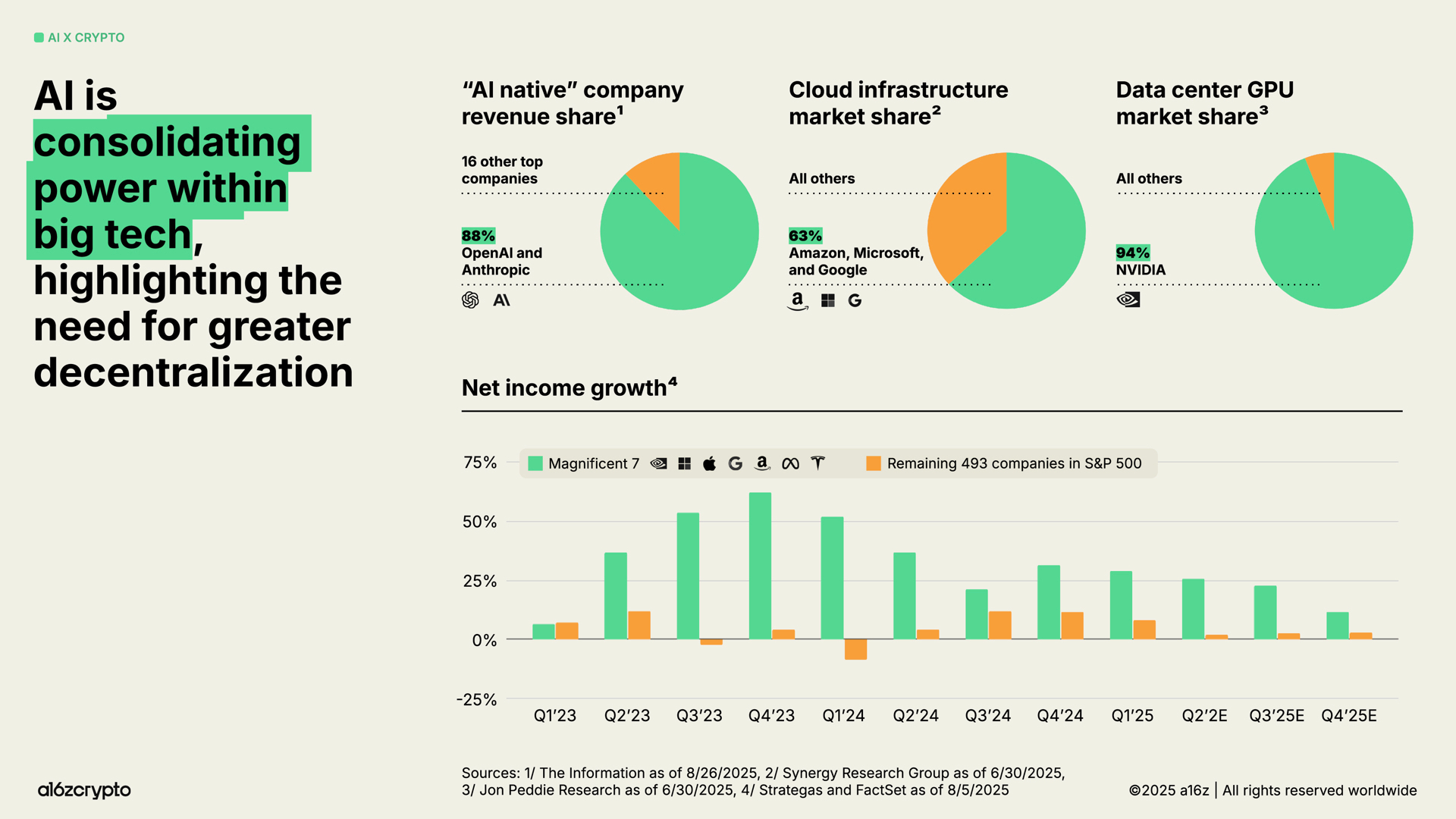

Meanwhile, the computational layer of artificial intelligence is consolidating among a few tech giants, raising concerns about centralization and censorship. OpenAI and Anthropic control 88% of the revenue of "AI-native" companies. Amazon, Microsoft, and Google control 63% of the cloud infrastructure market, while Nvidia holds 94% of the data center GPU market. These imbalances have driven the "Big Seven" to achieve double-digit quarterly net income growth over the past few years, while the overall profit growth of the remaining S&P 493 index constituents has failed to keep pace with inflation.

It is evident that blockchain can balance the apparent centralization of AI systems.

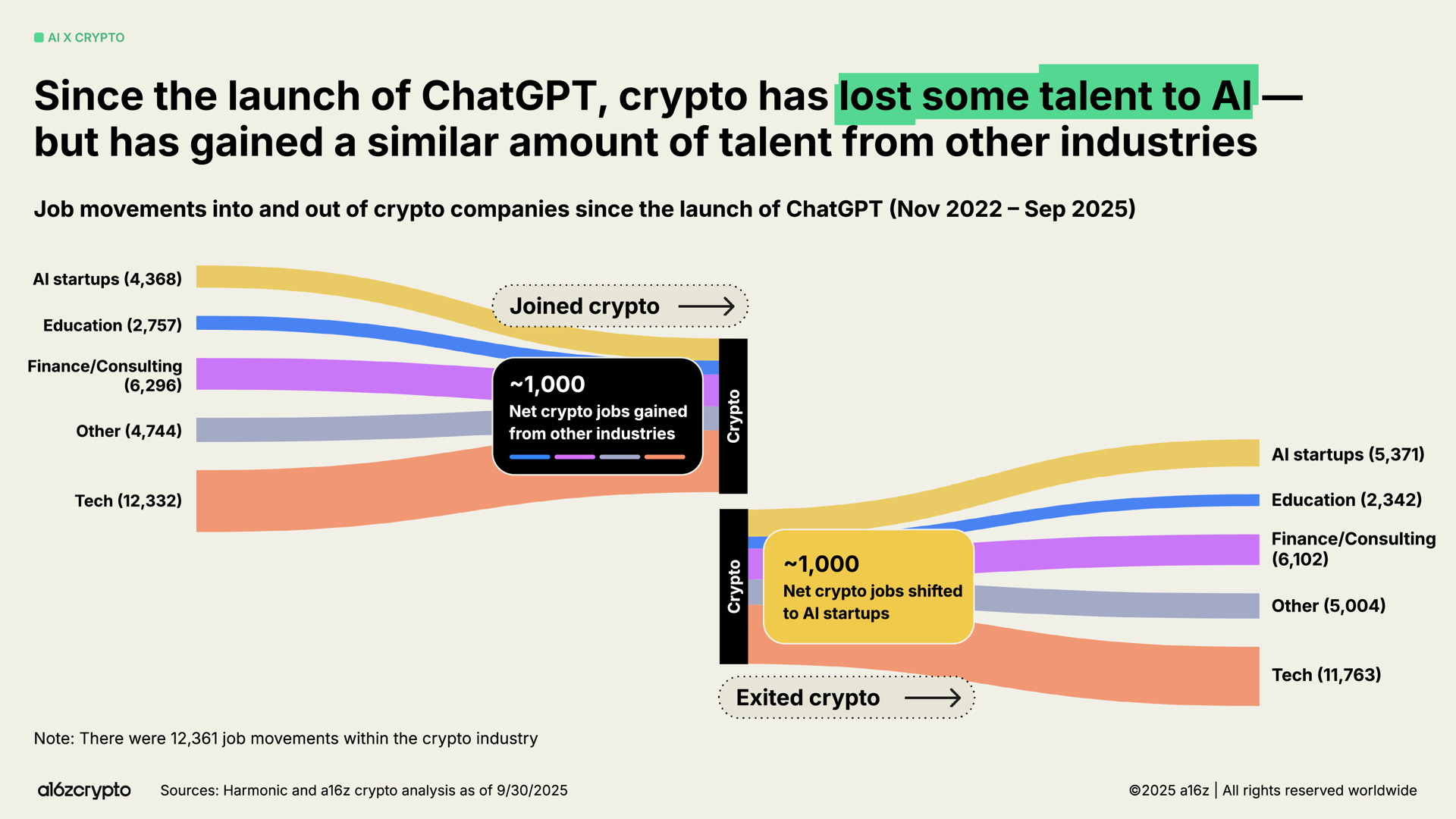

In the wake of the AI boom, some developers have shifted away from the cryptocurrency space. a16z analysis indicates that since the launch of ChatGPT, about 1,000 jobs have transitioned from cryptocurrency to AI. However, this number has been offset by an equal number of developers joining the cryptocurrency space from other fields, such as traditional finance and technology.

Conclusion

What does this mean for us? As regulations become clearer, the path for tokens to generate real revenue through transaction fees is becoming evident. The adoption of cryptocurrency by traditional finance and fintech will continue to accelerate; stablecoins will upgrade traditional systems, democratizing global financial services; and new consumer products will bring the next wave of cryptocurrency users on-chain.

We have the infrastructure, distribution channels, and are hopeful for clear regulations soon, making this technology mainstream. It is time to upgrade the financial system, rebuild global payment channels, and create the internet that the world deserves.

Seventeen years have passed, and cryptocurrency is bidding farewell to its "adolescence" and entering "adulthood."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。