Written by: Chris Beamish, CryptoVizArt, Antoine Colpaert, Glassnode

Compiled by: AididiaoJP, Foresight News

Bitcoin trading is below the key cost basis level, indicating a depletion of demand and weakening momentum. Long-term holders are selling as the market strengthens, while the options market shifts to a defensive posture, with increased demand for put options and rising volatility, marking a cautious phase before any sustainable recovery.

Summary

- Bitcoin is trading below the cost basis of short-term holders, indicating weakening momentum and increasing market fatigue. Multiple failures to recover raise the risk of entering a more prolonged consolidation phase.

- Long-term holders have accelerated their selling since July, now exceeding 22,000 BTC per day, marking ongoing profit-taking that continues to pressure market stability.

- Open interest has reached an all-time high, but market sentiment leans bearish as traders favor put options over call options. Short-term rebounds are encountering hedging behavior rather than new optimism.

- Implied volatility remains high while realized volatility has caught up, ending a period of calm low volatility. Market makers' short positions have amplified sell-offs and suppressed rebounds.

- On-chain and options data both indicate that the market is in a cautious transitional phase. A market recovery may depend on the emergence of new spot demand and a reduction in volatility.

Bitcoin has gradually retreated from its recent historical highs, stabilizing below the short-term holder cost basis of approximately $113,000. Historically, this structure typically signals the beginning of a mid-term bearish phase as weaker holders begin to capitulate.

In this issue, we assess the current profit-taking status of the market, examine the scale and sustainability of long-term holder spending, and finally evaluate whether this pullback represents a healthy consolidation or signals deeper weakness ahead by assessing the sentiment in the options market.

On-Chain Insights

Testing Conviction

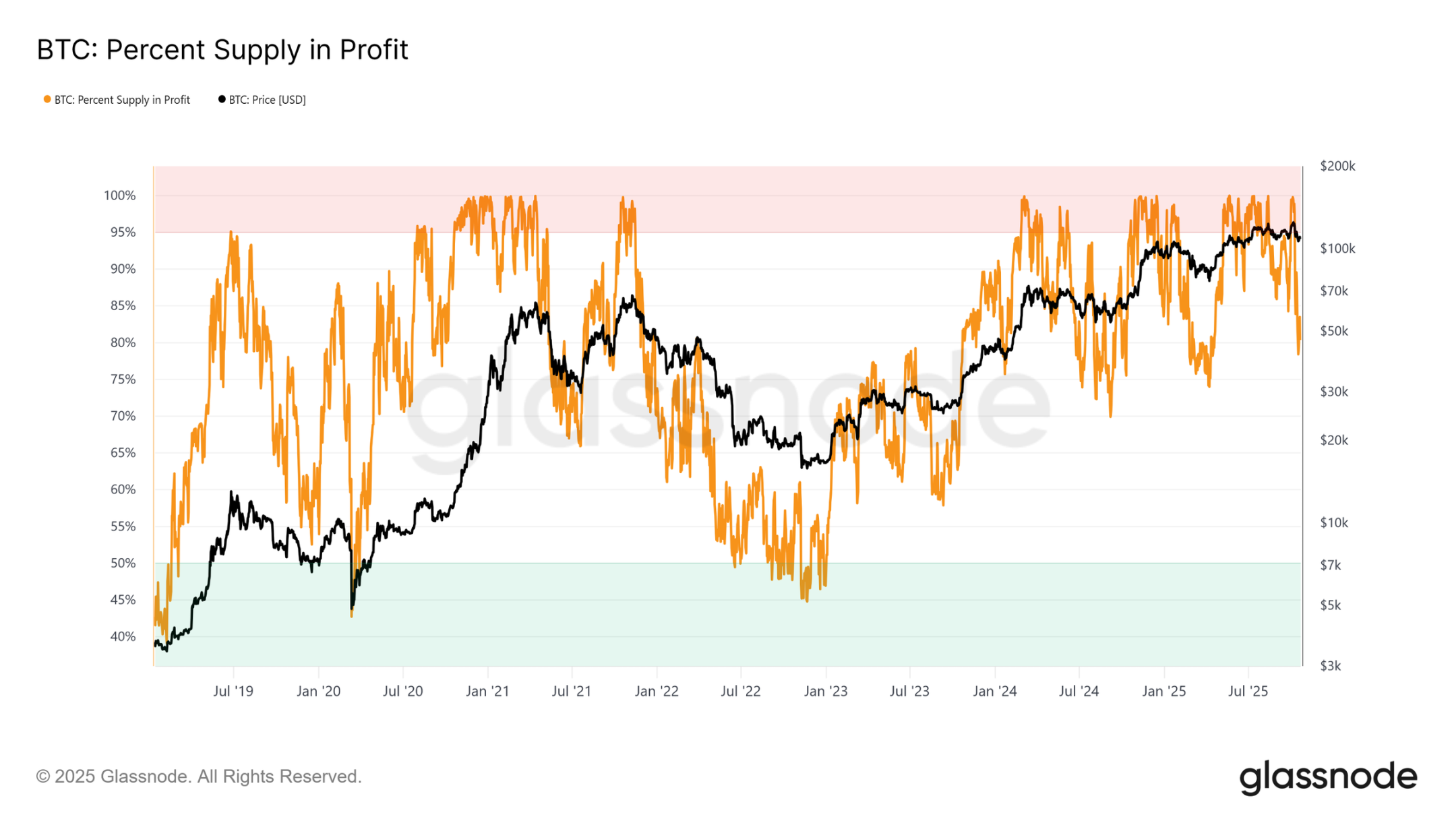

Trading near the cost basis of short-term holders marks a critical phase, testing the conviction of investors who bought near recent highs. Historically, falling below this level after reaching an all-time high has led to a decline in the percentage of profitable supply to about 85%, indicating that over 15% of the supply is in a loss state.

We have witnessed this pattern for the third time in the current cycle. If Bitcoin fails to recover above approximately $113,100, a deeper contraction may push a larger proportion of the supply into loss, intensifying pressure on recent buyers and potentially setting the stage for broader market capitulation.

Key Thresholds

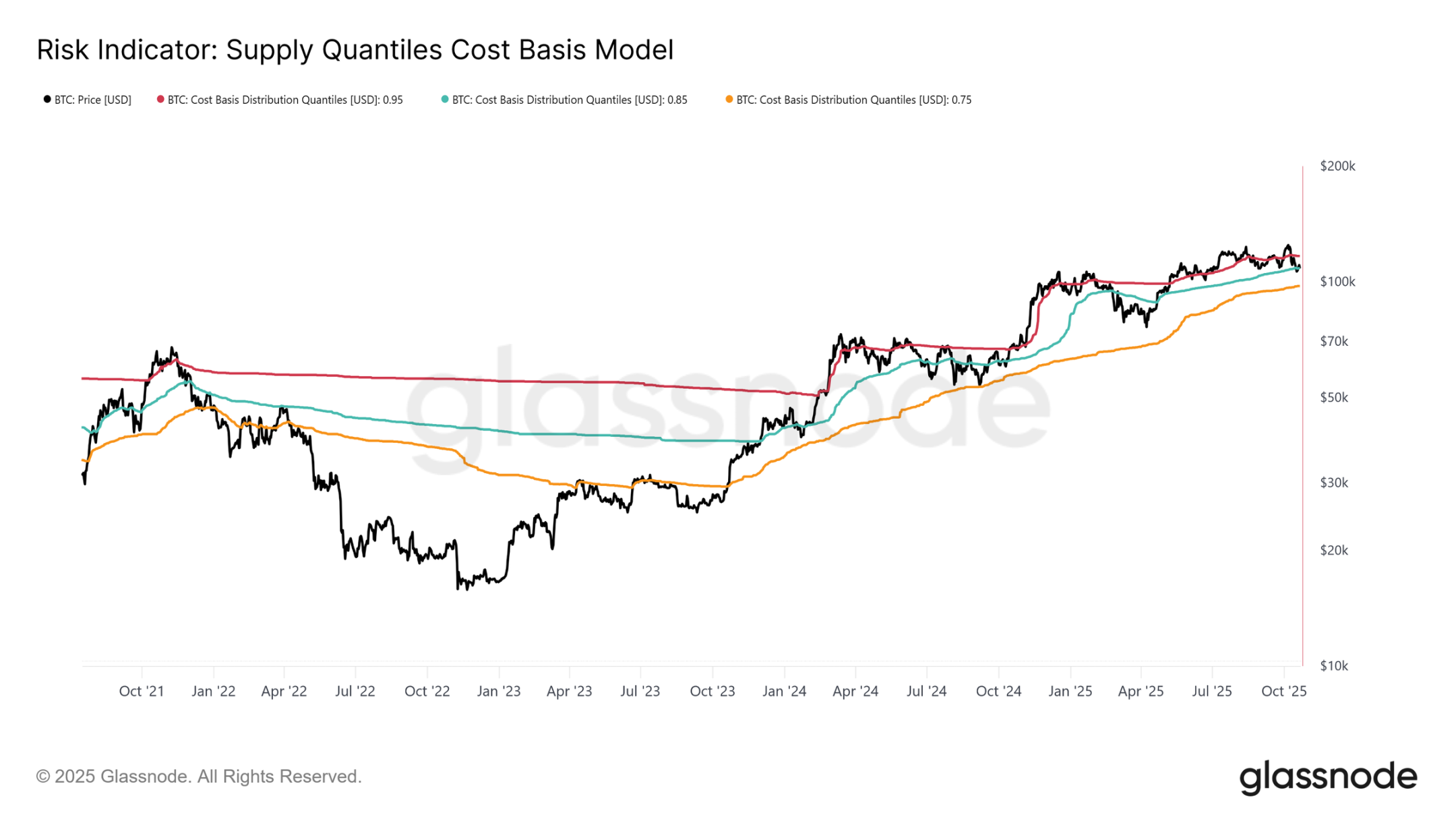

To further understand this structure, it is crucial to grasp why recovering the short-term holder cost basis is vital for maintaining a bullish phase. The supply percentile cost basis model provides a clear framework by mapping the 0.95, 0.85, and 0.75 percentiles, indicating that 5%, 15%, and 25% of the supply is at a loss, respectively.

Currently, Bitcoin is not only trading below the short-term holder cost basis ($113,100) but is also struggling to maintain above the 0.85 percentile at $108,600. Historically, failing to hold this threshold indicates market structure weakness and typically foreshadows a deeper pullback, pointing to the 0.75 percentile, which is currently around $97,500.

Demand Depletion

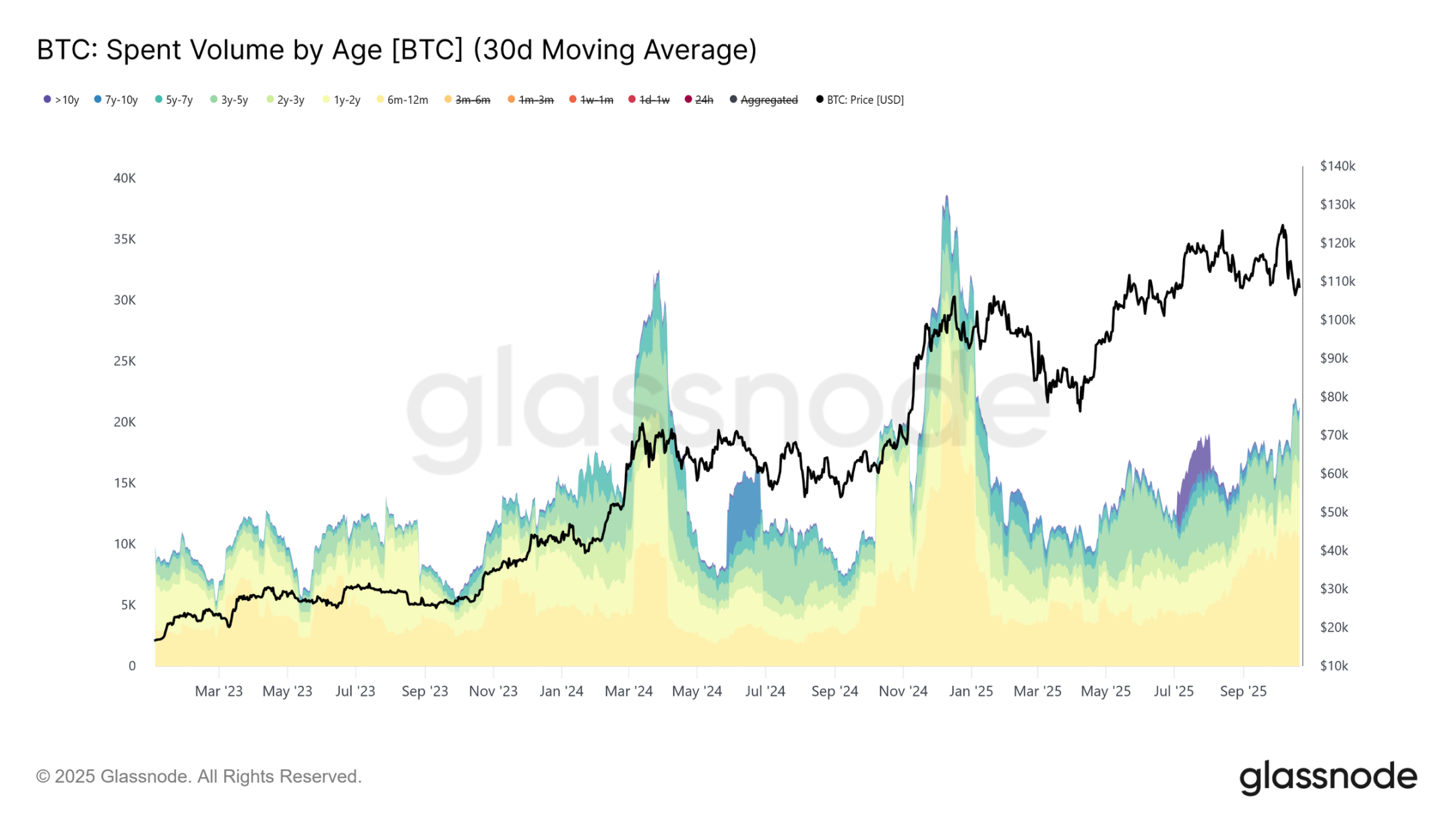

The third contraction below the short-term holder cost basis and the 0.85 percentile in this cycle has raised structural concerns. From a macro perspective, repeated demand depletion suggests that the market may require a longer consolidation phase to regroup.

When examining the spending volume of long-term holders, this depletion becomes clearer. Since the market peak in July 2025, long-term holders have steadily increased their spending, with the 30-day simple moving average rising from a baseline of 10,000 BTC to over 22,000 BTC per day. Such sustained distribution indicates that experienced investors are under profit-taking pressure, a key factor in the current market fragility.

After assessing the risk of demand depletion leading to a long-term bearish phase, we now turn to the options market to gauge short-term sentiment and observe how speculators are positioning themselves amid rising uncertainty.

Off-Chain Insights

Open Interest Rising

Bitcoin options open interest has reached an all-time high and continues to expand, marking a structural evolution in market behavior. Investors are increasingly using options to hedge risk exposure or speculate on volatility rather than selling spot. This shift reduces direct selling pressure in the spot market but amplifies short-term volatility driven by market maker hedging activities.

As open interest grows, price fluctuations are more likely to stem from funding flows driven by Delta and Gamma in the futures and perpetual contract markets. Understanding these dynamics is becoming crucial, as options positions now play a dominant role in shaping short-term market trends and amplifying responses to macro and on-chain catalysts.

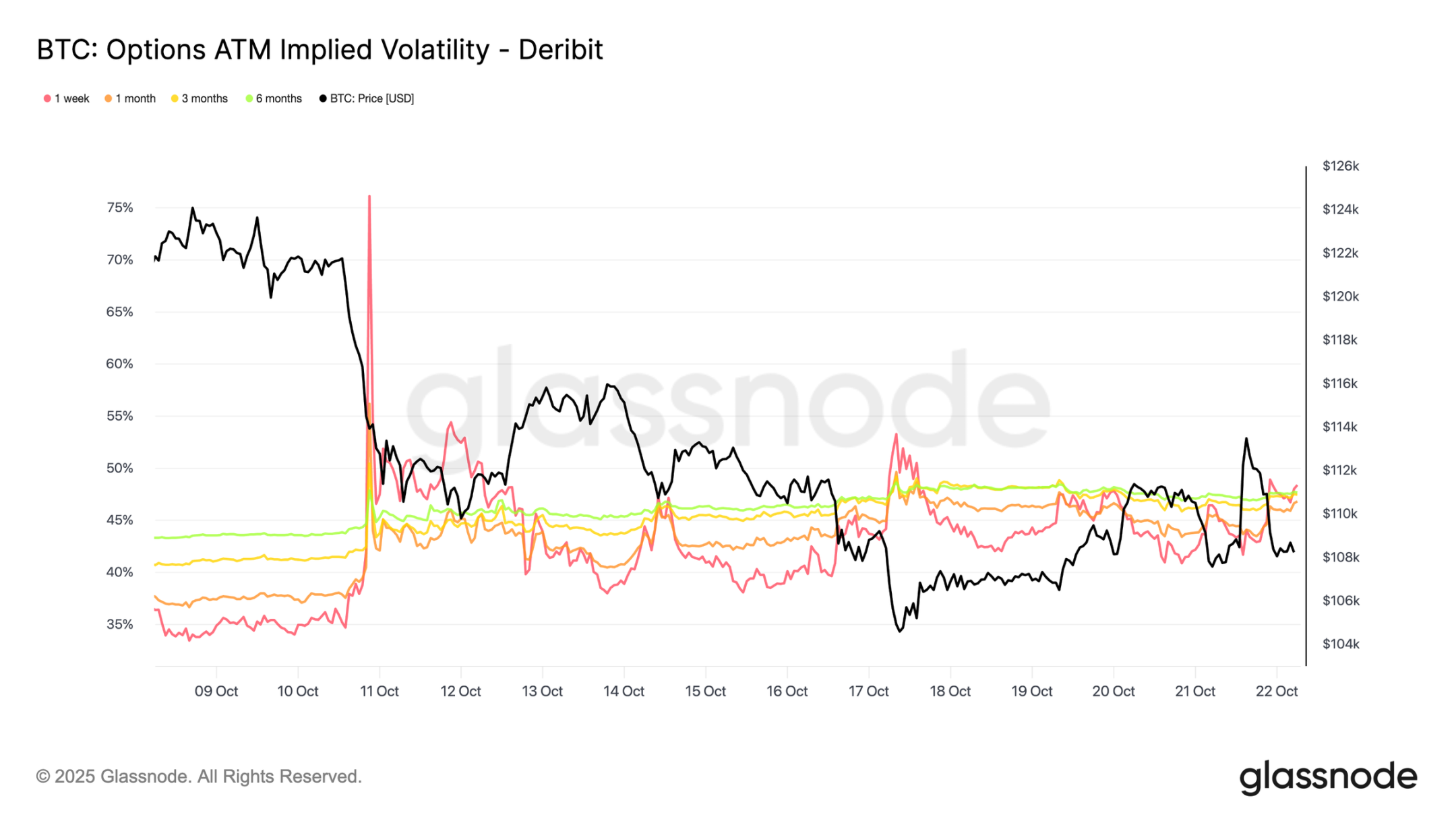

Volatility Mechanism Shift

Since the liquidation event on the 10th, the volatility pattern has changed significantly. Implied volatility is now around 48 across all maturities, up from 36-43 just two weeks ago. The market has not fully digested this shock, and market makers remain cautious, not selling volatility cheaply.

The 30-day realized volatility is at 44.1%, while the 10-day realized volatility is at 27.9%. As realized volatility gradually cools, we can expect implied volatility to decline and normalize in the coming weeks. For now, volatility remains elevated, but this appears more like a short-term repricing rather than the beginning of a sustained high-volatility regime.

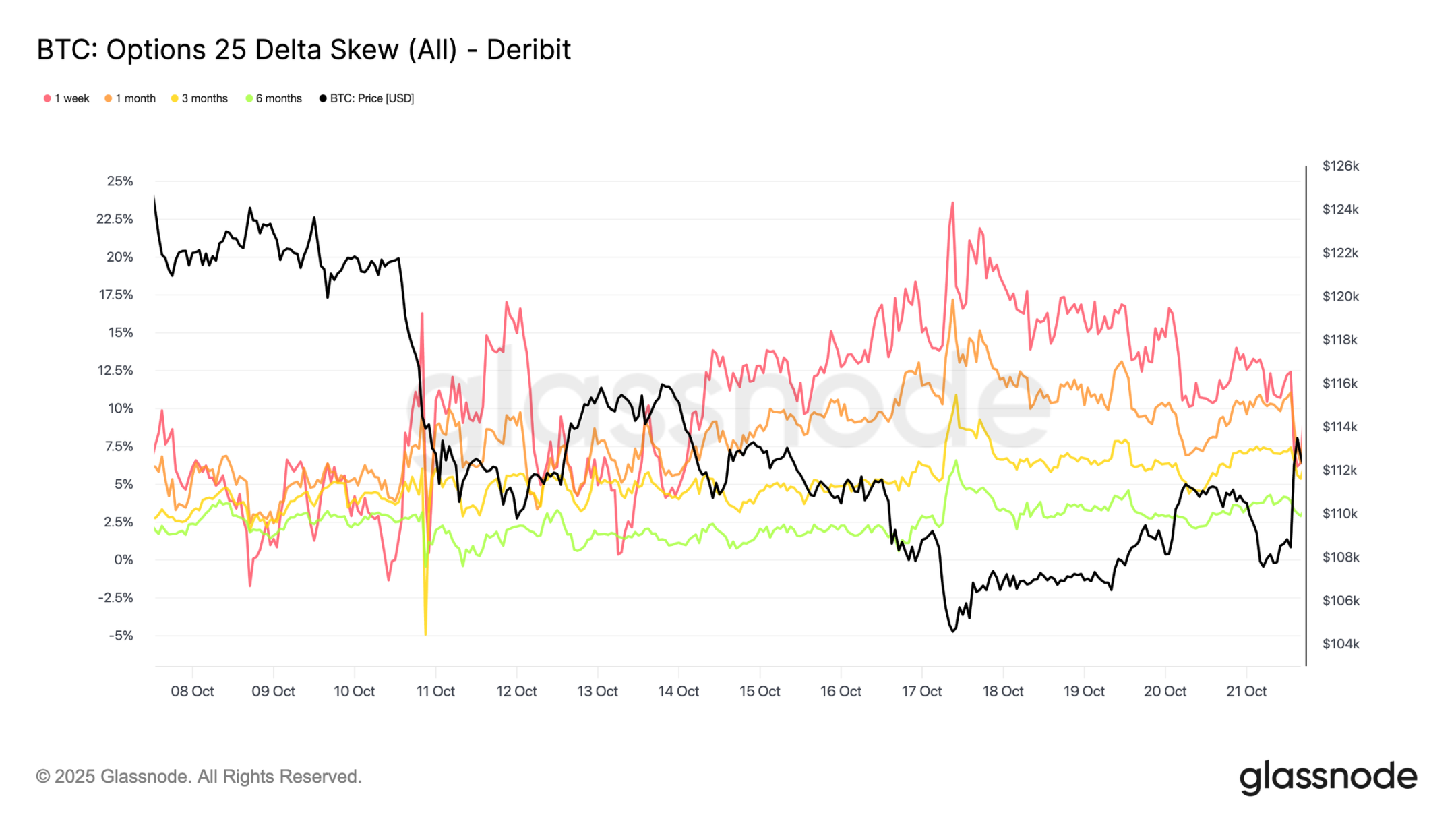

Increased Put Options

Put options have steadily increased over the past two weeks. A surge in large liquidations has driven the put options skew sharply higher; although it briefly reset, the curve has since stabilized at structurally higher levels, indicating that put options remain more expensive than call options.

The skew for one-week expirations has fluctuated but remains in a highly uncertain area, while all other maturities have moved further towards put options by 2-3 volatility points. This cross-maturity expansion indicates that cautious sentiment is spreading across the entire curve.

This structure reflects a market willing to pay a premium for downside protection while maintaining limited upside risk exposure, balancing short-term fears against long-term prospects. The slight rebound on Tuesday illustrates this sensitivity, with put option premiums halving within hours, showing how tense market sentiment remains.

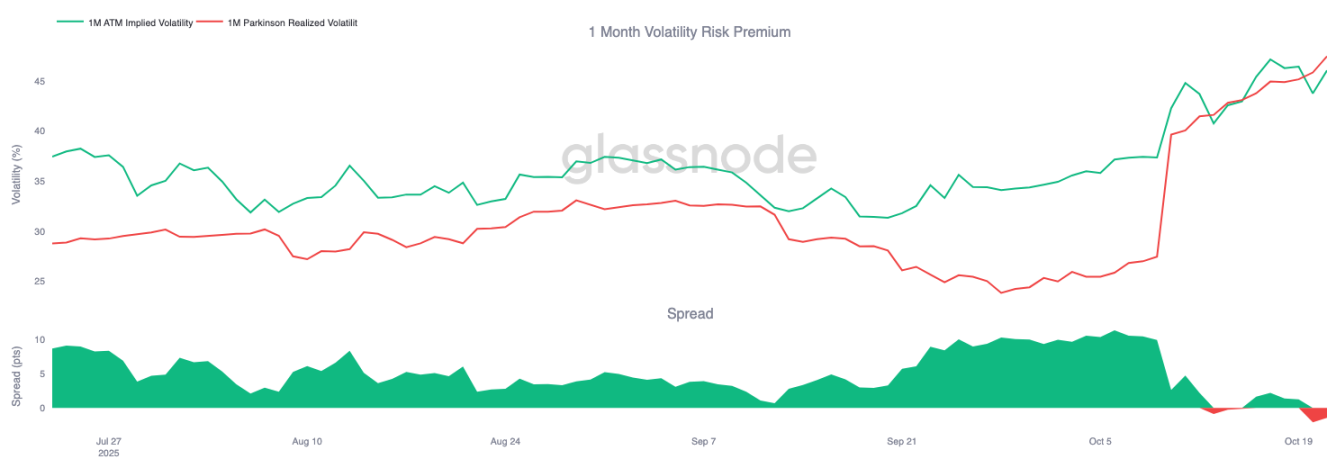

Risk Premium Shift

The one-month volatility risk premium has turned negative. For months, implied volatility remained high while actual price volatility stayed calm, allowing traders shorting volatility to earn steady profits.

Now, actual volatility has surged to match implied volatility, erasing this advantage. This marks the end of the calm mechanism: volatility sellers can no longer rely on passive income and are instead forced to actively hedge under more volatile conditions. The market has shifted from a quiet state of complacency to a more dynamic, responsive environment, with short positions facing increasing pressure as real price volatility returns.

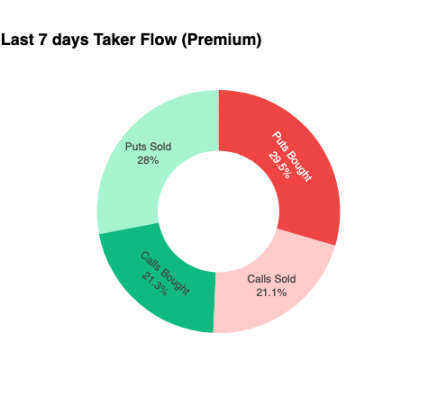

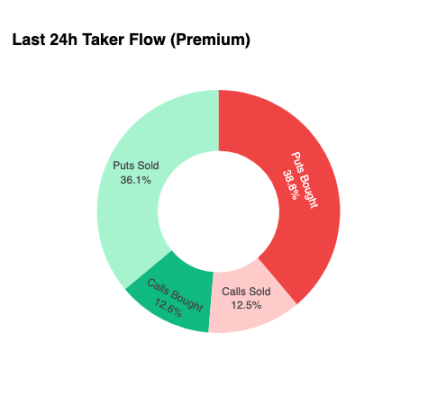

Funds Flow Remains Defensive

To focus the analysis on the very short term, we zoom in on the past 24 hours to observe how options positions responded to the recent rebound. Although prices rebounded 6% from $107,500 to $113,900, buying in call options did not provide much confirmation. Instead, traders increased their put options risk exposure, effectively locking in higher price levels.

This positioning layout leaves market makers short on the downside and long on the upside, a setup that typically leads them to suppress rebounds and accelerate sell-offs, a dynamic that will continue to act as resistance until positions reset.

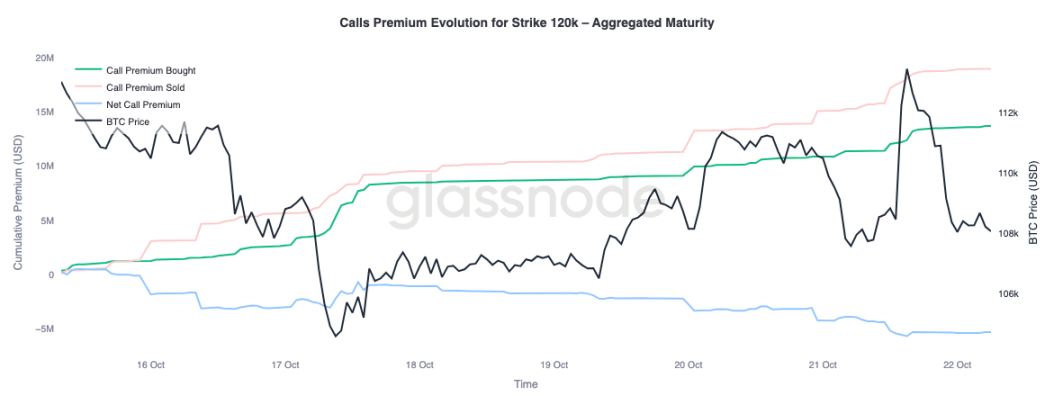

Premiums

Glassnode's aggregated premium data confirms the same pattern when segmented by strike price. At the $120,000 call options, the sold premiums rise with the price; traders are suppressing upward momentum and selling volatility during what they perceive to be a temporary strength. Short-term profit seekers are taking advantage of the spike in implied volatility, selling call options during rebounds rather than chasing prices.

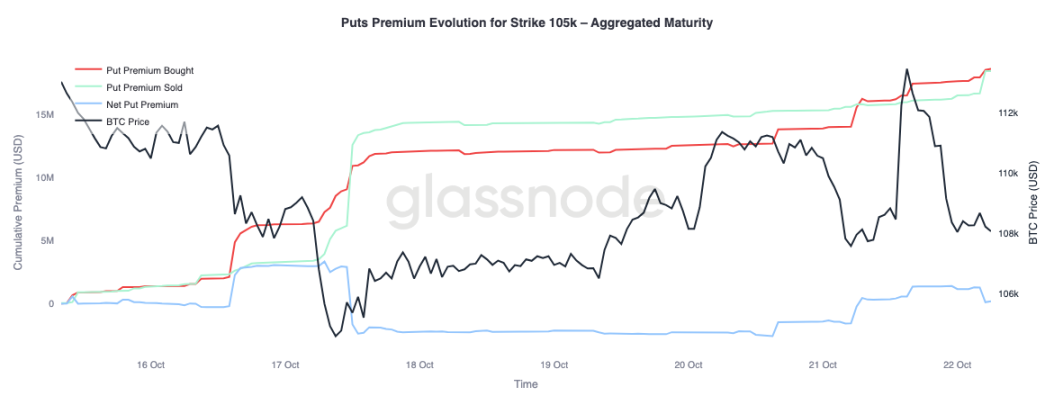

When observing the premiums for the $105,000 put options, the pattern is the opposite, confirming our argument. As prices rise, the net premium for the $105,000 put options increases. Traders are more eager to pay for downside protection rather than purchase upside convexity. This indicates that the recent rebound has encountered hedging rather than conviction.

Conclusion

Bitcoin's recent pullback below the short-term holder cost basis ($113,000) and the 0.85 percentile ($108,600) highlights the growing demand depletion, as the market struggles to attract new inflows while long-term holders continue to distribute. This structural weakness suggests that the market may require a longer consolidation phase to rebuild confidence and absorb the supply that has been sold.

Meanwhile, the options market reflects the same cautious tone. Despite open interest reaching an all-time high, positioning leans defensive; put options skew remains elevated, volatility sellers face pressure, and short-term rebounds are met with hedging rather than optimism. In summary, these signals indicate that the market is in a transitional phase: a period of waning enthusiasm, where structural risk-taking is suppressed, and recovery may depend on the restoration of spot demand and a reduction in volatility-driven flows.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。