It is crucial to pay attention to the correlation between returns and collateral, as this is often the root of the problem.

Author: ✧Panterafi

Translation: Deep Tide TechFlow

There has been much discussion about stablecoins, but relatively little exploration of their risks, which I believe is a core topic worth delving into. This is the content I have organized and am willing to share after months of contemplation.

Summary

The future of stablecoins and past discussions

Main classifications of stablecoins

Comparative analysis of risk indicators

Current development status of the Solana ecosystem

The future of stablecoins and past discussions

Here, I focus on reviewing some important discussions and viewpoints within the industry regarding the development of stablecoins. These discussions mostly revolve around the various paths through which decentralized finance (DeFi) can achieve global adoption via stablecoins.

“On-chain FX is key to global adoption” — @haonan

On-chain foreign exchange (On-chain FX) can enhance the efficiency of global trade settlements. It can handle cross-border payments, remittances, and conversions to local stablecoins or fiat currencies without being restricted by regulatory barriers. On-chain FX is expected to replace the current slow systems, enabling instant and low-cost currency conversions.

To achieve widespread adoption, on-chain FX needs to have deep automated market maker (AMM) pools capable of supporting, for example, $11 billion in trading volume within 30 days. Meanwhile, managing slippage becomes a challenge, and scalable infrastructure and payment systems need to be established. The stablecoin ecosystem must also prioritize strong security in foreign exchange swaps.

“Proxy payments can enhance user experience for small online transactions” — @hazeflow_xyz

x402 is an open-source internet-native payment protocol developed by Coinbase. It utilizes the HTTP 402 status code (“Payment Required”) to facilitate instant micro-payments based on stablecoins (such as USDC). This method can significantly improve the payment experience for users in small online transactions.

Multiple advantages of x402

Autonomous operation: AI agents can independently complete payments for services, data, computation, or tools in real-time without human intervention, enabling economic activities between machines.

Instant settlement: Transactions are confirmed and completed within seconds, eliminating concerns about refunds or protocol fees, making it particularly suitable for high-frequency micro-payment scenarios.

Seamless integration: Agents can attach stablecoin payments to any web request with minimal setup, overcoming barriers such as API keys or intermediaries in traditional payments.

Compliance and security: Built-in verification and settlement functions ensure regulatory compliance while maintaining price stability using stablecoins in a volatile crypto environment.

Scalability of the AI ecosystem: Supports a marketplace for agents, allowing them to autonomously trade resources and promote the growth of stablecoin infrastructure, backed by supporters like Coinbase or PayAI.

Traditional financial institutions, such as Deutsche Bank, as well as auditing firms like Deloitte and EY, have faced serious allegations due to improper audits or money laundering issues. Additionally, many politicians have been convicted of embezzlement.

Blockchain-based stablecoin systems have significant advantages in reducing corruption, illegal transactions, and money laundering. Through blockchain, financial regulators can track the flow of funds, and auditors can gain clearer insights into business operations. This transparency may also give rise to new professional roles, such as wallet trackers or data analysts (e.g., DUNE data analysis platform). With more precise analysis of fund flows and data insights, new economic models and concepts may also emerge.

For me, blockchain is not just a practical revolution from a corporate perspective; it is a social transformation that rebuilds trust by empowering the public to oversee the government and elite classes. The transparency and controllability of blockchain will provide the public with greater visibility, promoting a return to fairness and trust.

“The infrastructure for stablecoins will become invisible” — @SuhailKakar

SuhailKakar emphasizes that blockchain stablecoins will gradually fade from public view. For ordinary consumers, as long as the payment system functions well, they do not care about the underlying technology. He cites the example of Telegram, which started as a messaging app and later integrated the TON network, allowing users to access wallet and payment services without realizing it was related to cryptocurrency or blockchain.

This is precisely the goal that companies like Circle, Tether, Coinbase, and Stripe are striving to achieve: to build a payment infrastructure that allows merchants to accept crypto payments without needing to understand any crypto knowledge. Merchants only need to receive dollars, while the infrastructure handles all blockchain-related matters, providing customers with a seamless checkout experience.

SuhailKakar believes that the greatest success of cryptocurrency will be evident on the day people stop talking about it. When it becomes the “invisible infrastructure” that supports the experiences users truly need, its value will have been realized.

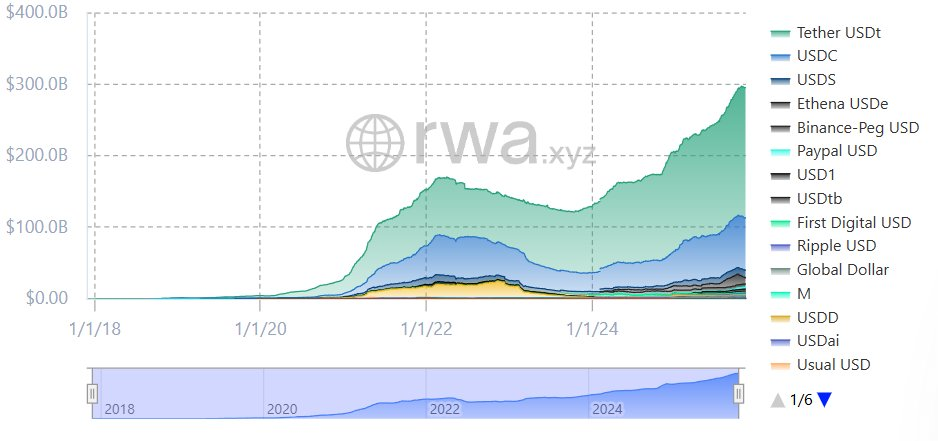

“Explosive growth of yield-bearing stablecoin protocols” — @Jacek_Czarnecki

The total market value of yield-bearing stablecoin protocols surged 13 times in just two years, skyrocketing from $666 million in August 2023 to $8.98 billion in May 2025, peaking at $10.8 billion in February 2025.

Currently, yield-bearing stablecoins account for 3.7% of the overall stablecoin market (totaling $300 billion). There are over 100 types of yield-bearing stablecoins in the market, with leaders including Ethena's sUSDe and Sky's sUSDS/sDAI, which together hold 57% of the market share (approximately $5.13 billion). Since mid-2023, these protocols have distributed nearly $600 million in yields.

The rapid development of yield-bearing stablecoins indicates that stablecoins are not just payment tools but can also become a new option for users seeking stable returns.

Drivers of inflow into emerging stablecoins: Two key factors

Innovation in core mechanisms: The recent growth of stablecoins is largely attributed to breakthroughs in their core concepts. For example, Ethena's USDe employs a delta-neutral hedging mechanism, while Curve's crvUSD introduces soft liquidation mechanisms. These technological innovations not only helped the market recover from the Luna collapse but also propelled the stablecoin market cap to $300 billion.

Government regulation: The recognition of certain types of crypto assets as financial instruments by governments has opened doors for industry innovation. For instance, the U.S. passed the GENIUS Act in July 2025 (requiring 1:1 reserves, anti-money laundering/know your customer (AML/KYC) compliance, and banning uncollateralized algorithmic stablecoins), along with Europe's MiCA regulation, and related frameworks in the UK and Asia. These regulatory advancements not only promote institutional adoption but also enhance market trust, laying the groundwork for further development of stablecoins.

“New revenue models and white-label distribution” — @hazeflow

In a low-interest-rate environment, new reward models can be introduced, such as government intervention. Governments can incentivize users to adopt stablecoins through incentive measures. In a high-interest-rate environment, particularly decentralized stablecoins have advantages, as they can provide yields or incentives through reserve assets. Simply holding stablecoins can yield annual returns for users to offset inflation impacts. These returns can be transformed into cash back or other practical benefits through partnerships with businesses.

Stable infrastructure can achieve mutual benefits with companies (like Apple or Microsoft). Companies can open new revenue streams, while stablecoins can leverage the large user bases of these companies to promote their global development.

The U.S. is a fertile ground for the development of stablecoins, with a gradually improving regulatory framework and a substantial market size. In terms of actual use of stablecoins, economically poorer countries tend to adopt stablecoins as alternative tools due to their weaker local currencies.

Next, let’s delve into the specific characteristics of different types of stablecoins to better understand their risk indicators and return mechanisms. I have specially written and created relevant visual content to help you comprehensively understand which mechanisms are more robust and how they differ in terms of returns.

Stablecoins are a core pillar of DeFi, but concentrating all idle funds into one protocol is not the best choice. While diversification is important, the range of diversification for achieving sustained stable returns is limited, so careful selection of the appropriate type of stablecoin is essential.

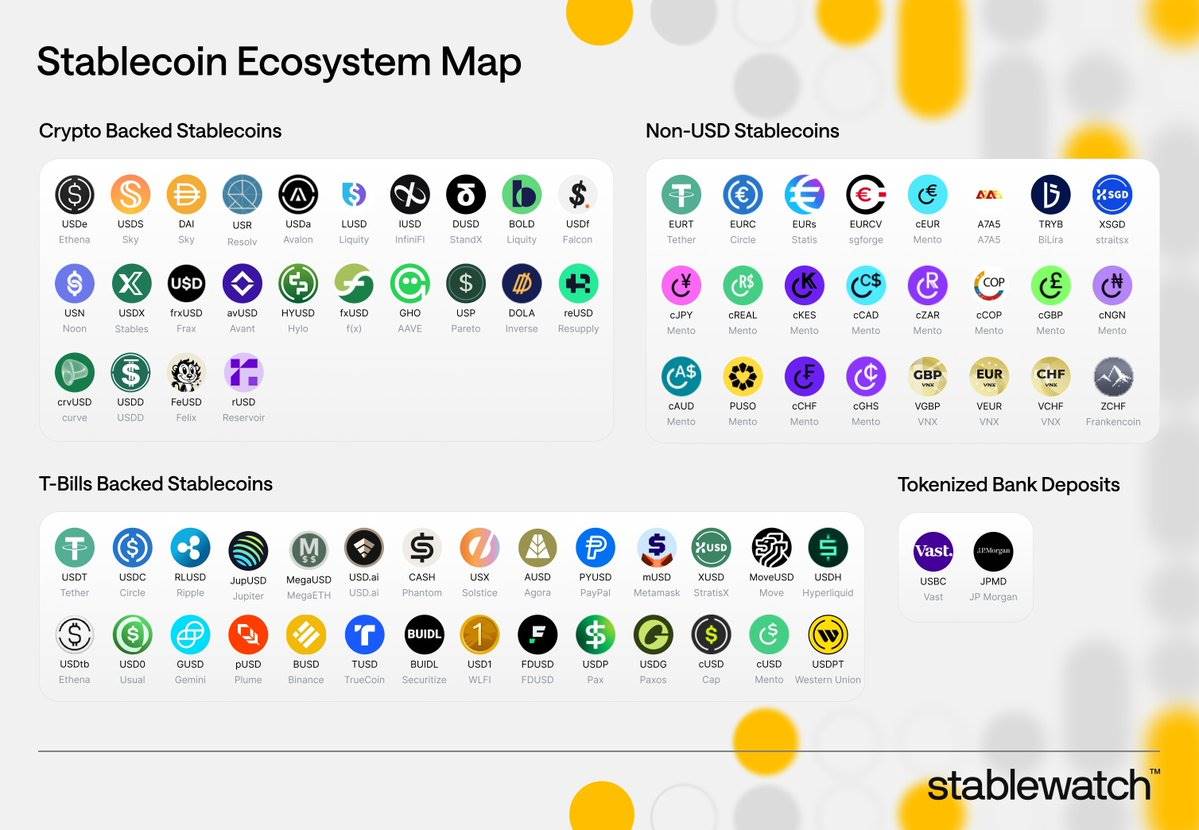

Categories of stablecoins

Collateralized stablecoins (over-collateralized with cryptocurrencies or real-world assets)

Return Mechanism

Users borrow stablecoins by over-collateralizing assets (such as ETH, BTC), where the value of the collateral exceeds the issued stablecoins, thus generating returns. These returns come from:

Borrowing Fees

Interest from Real-World Assets (RWA, such as U.S. Treasury Bonds)

Protocol Profits: The over-collateralized portion acts as a buffer, enhancing the system's stability.

Examples

USDS (issued by Sky): Returns come from real-world assets and lending.

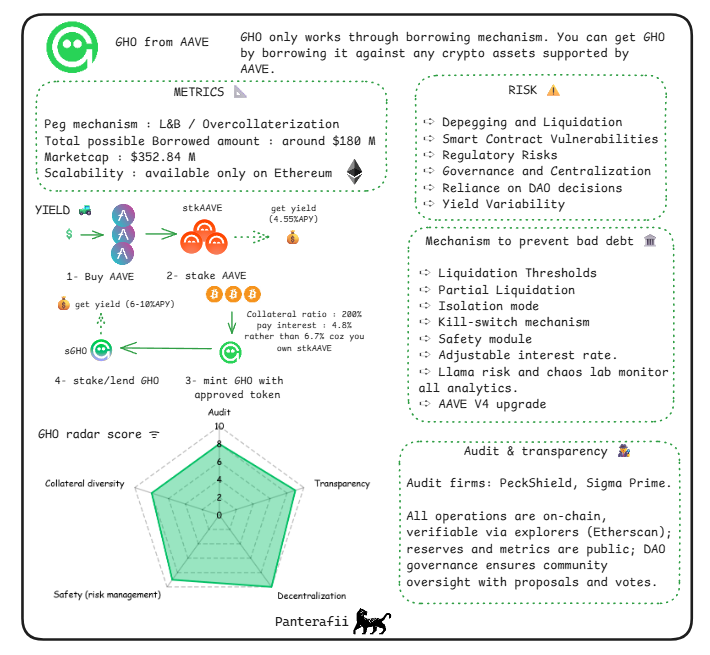

GHO (issued by Aave): Returns come from borrowing fees.

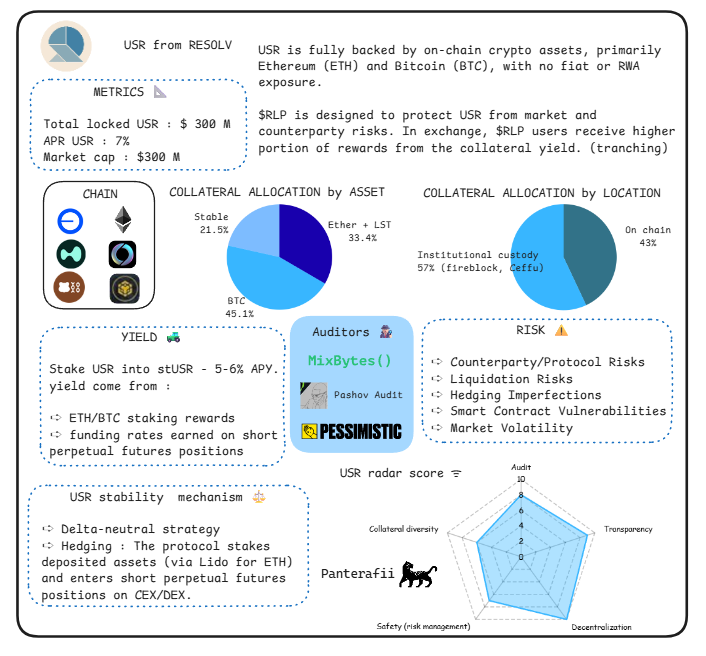

USR (issued by Resolv): Returns come from asset tokenization.

USDe (issued by Ethena): Returns come from staking ETH and futures trading.

USD0 (issued by Avalon): Returns come from interest on real-world assets.

cUSD (issued by Celo): Returns come from natural resource backing.

How Returns are Generated

Interest generated from collateral assets (such as staking rewards or returns from real-world assets) is typically distributed to holders or stakers through modules (like savings rate modules). This mechanism not only provides returns to users but also further enhances the attractiveness and use cases of stablecoins.

Return Mechanisms

Stability is maintained through algorithmic supply adjustments (minting/burning), with returns coming from:

Seigniorage: Fees incurred during minting.

Incentives: For example, governance token rewards.

Examples

USDF (issued by Falcon): A hybrid model that provides returns through perpetual futures.

USDO (issued by Avalon): Combines algorithmic mechanisms with real-world assets (RWA).

How Returns are Generated

Dynamic adjustment mechanisms create opportunities for arbitrage or rewards, and returns are often amplified through DeFi integrations (such as staking or providing liquidity), offering incentives to users.

Fiat-backed or Centralized Stablecoins (for comparison)

Return Mechanisms

Backed 1:1 by fiat or equivalent assets, returns primarily come from reserves (like government bonds). Base returns are typically not distributed to users but are used for corporate operations.

Examples

USDC (issued by Circle)

USDT (issued by Tether)

How Returns are Generated

The low-risk interest from reserves is the main source of returns, but the degree of decentralization is low, with more returns retained for corporate purposes rather than directly distributed to users.

Risk Indicators

Depeg Risk

Depeg occurs when a stablecoin fails to maintain its expected $1 peg. This is often caused by extreme market pressure, supply-demand imbalances, or significant declines in the value of underlying collateral. This risk is an inherent characteristic of stablecoin models, as they rely on economic incentives, algorithmic mechanisms, or reserves, which may fail during a crypto market crash or broader financial turmoil.

Collateralized Stablecoins: If reserves are insufficient or lack liquidity, it may lead to depeg.

Algorithmic Stablecoins: Rely on fragile arbitrage mechanisms that may collapse during panic sell-offs.

Important Supplementary Points

Types of Depeg Mechanisms

Depeg can be categorized into two types:

Temporary Depeg: Triggered by short-term liquidity crunches, usually recoverable.

Permanent Failure: Such as the "death spiral" seen in low-collateral systems. Indicators to monitor include:

Peg Deviation Percentage: Tracking the frequency of price deviations of ±0.5% within 24 hours.

Reserve Transparency: Monitoring reserve ratios through on-chain audits.

Redemption Speed: Efficiency of redemptions during stress tests.

Market Contagion Effects

The depeg of one stablecoin may trigger a chain reaction within the DeFi ecosystem, similar to a "bank run." Since stablecoins are often used as collateral in lending protocols, this situation can amplify losses.

Risk Mitigation Strategies

Regular reserve audits.

Maintaining over 100% over-collateralization.

Adopting a hybrid model that combines fiat support with algorithmic adjustments. However, even well-supported stablecoins cannot be completely immune. For instance, during periods of high market volatility, arbitrageurs may delay intervention due to high gas fees or network congestion.

Recent Developments

As of 2025, with the widespread use of stablecoins, predictive models have prioritized depeg risk, considering collateral volatility, issuance volume, and macroeconomic indicators (such as the impact of interest rate changes on government bond-backed reserves).

Case Event: TerraUSD (UST) Depeg

In May 2022, the UST stablecoin lost its $1 peg, with prices plummeting close to zero. The failure of the algorithmic mechanism and market panic led to the collapse of over $40 billion in the ecosystem. This event highlighted the vulnerability of algorithmic stablecoins under extreme market conditions.

Smart Contract Vulnerabilities

Code vulnerabilities or exploited weaknesses in protocols can lead to hacking incidents or loss of funds. Stablecoin protocols that have been operational for longer typically exhibit stronger resistance to these vulnerabilities, while newer stablecoin protocols face higher smart contract risks due to a lack of practical testing (not having undergone "real-world" testing).

Smart contracts, as the core framework of stablecoin protocols, may contain code vulnerabilities, logical flaws, or exploitable weaknesses, leading to unauthorized access, theft of funds, or failure of protocol functions. In contrast, protocols that have been operational for longer and have undergone extensive audits and validation in real scenarios tend to perform more robustly; newer protocols face higher risks due to unverified code.

Important Supplementary Points

- Audit and Testing Practices

Emphasizing the importance of the following measures:

Independent audits by multiple parties (conducted by organizations such as Quantstamp or Trail of Bits).

Utilizing formal verification tools.

Continuously conducting bug bounty programs to identify potential issues before and after launch. Relevant indicators include the number of audits, the time since the last major update, and whether vulnerabilities have occurred historically.

- Oracle Dependency

Stablecoin protocols often rely on external data sources (oracles) to obtain price information for collateral, which can become a manipulated weak point. For example, through flash loan attacks, attackers can temporarily distort prices, triggering unnecessary liquidations (leading to temporary depeg).

- Ecosystem-Wide Impact

Smart contract vulnerabilities are not isolated. A hack of one protocol may affect integrated stablecoins, triggering a chain reaction of liquidations across the entire stablecoin protocol (as these protocols support each other or use similar collateral), ultimately leading to a crisis of trust and a decline in adoption rates. For instance, the default of SVB (Silicon Valley Bank) led to the temporary depeg of USDC, impacting the entire DeFi ecosystem.

Case Event: Ronin Network Hack

In March 2022, attackers exploited vulnerabilities to steal $620 million worth of ETH and USDC from Axie Infinity's cross-chain bridge.

Regulatory Risks

Stablecoins are facing increasingly stringent government scrutiny regarding anti-money laundering (AML), know your customer (KYC) requirements, securities classification, and transparency of fiat backing. This could lead to operational restrictions, asset freezes, or even outright bans, especially for stablecoins that integrate with real-world assets (RWA) or engage in international business. In jurisdictions with constantly changing crypto policies, this risk is further amplified, affecting their global availability.

Important Supplementary Points

- Global Regulatory Differences

European Union: Under the Markets in Crypto-Assets Regulation (MiCA), stablecoin issuers must hold reserves in licensed banks and maintain liquidity buffers.

United States: Focuses on classifying certain stablecoins as securities, regulated by the U.S. Securities and Exchange Commission (SEC).

Emerging Markets: May implement capital controls that restrict cross-border capital flows. Protocols must comply with regulatory requirements in their jurisdictions to access local users, increasing the complexity of development. Additionally, protocols need to choose jurisdictions suitable for legal operation, with the EU not being a priority choice.

- Compliance Indicators

The following indicators need to be monitored:

The licensing status of the issuer.

The frequency of reserve reporting.

The degree of association with sanctioned entities. Non-compliance may lead to delisting from exchanges, resulting in a loss of user trust and user base.

- Geopolitical Factors

Stablecoins pegged to the dollar face risks from changes in U.S. policy, such as technology export controls or sanctions extending to crypto entities.

Most stablecoins are pegged to dollar assets, but what would happen if the U.S. financial system collapses or its financial influence over Asia or the EU diminishes?

Potential Solution: The Swiss franc, as a relatively strong currency, could become a new option. Developing a stablecoin backed by the Swiss franc may have advantages in diversification, trust, and foreign exchange swaps.

- Positive Aspect

Regulation can enhance legitimacy, but excessive regulation may stifle innovation, forcing users to turn to unregulated alternatives.

Case Event: Tornado Cash Sanctioned

In August 2022, the U.S. Office of Foreign Assets Control (OFAC) sanctioned Tornado Cash, blacklisting its addresses and prohibiting U.S. citizens from interacting with it, while freezing $437 million in assets.

Liquidity Risks

Liquidity Risk

Liquidity risk refers to the situation where users encounter significant price slippage when buying or selling stablecoins due to insufficient market depth. This risk is particularly severe in low-volume markets, during panic sell-offs, or on low-traffic exchanges. In contrast, mature stablecoins with high Total Value Locked (TVL) and deep liquidity pools perform better, as their long-term development brings network effects that reduce slippage risk.

Key Points:

Measurement Indicators:

Use on-chain data to assess liquidity health, such as TVL (which can be queried through DefiLlama), the ratio of 24-hour trading volume to market capitalization, and slippage rates on major decentralized exchanges (DEXs) during periods of high volatility.

A healthy ratio is when daily trading volume exceeds 5-10% of circulating supply.

Market Depth Issues:

- In bear markets, redemption demand may exceed minting capacity, depleting liquidity reserves.

Chain Liquidation Risk:

- Similar to a bank run, when large-scale withdrawals occur, it creates a self-fulfilling prophecy—what was initially perceived as "perceived liquidity insufficiency" ultimately evolves into a real liquidity crisis.

Improvement Measures:

Integration with Automated Market Makers (AMMs) and liquidity incentives (such as liquidity mining rewards, Merkl, Turtle, etc.) can enhance market resilience.

However, over-reliance on incentive mechanisms may lead to "artificial liquidity," which can evaporate quickly during a crisis.

Case Analysis: FTX Collapse

In November 2022, the collapse of FTX triggered an $8 billion liquidity gap, leading to withdrawal interruptions and eventual bankruptcy. This crisis was exacerbated by significant capital outflows, becoming a typical case of liquidity risk.

Counterparty Risk

Stablecoins often rely on third parties, such as custodians managing real-world assets (RWAs), oracles providing price data, or cross-chain bridges enabling cross-chain functionality. These third parties can become potential failure points, introducing risks due to bankruptcy, fraud, or operational errors.

Important Supplementary Points

Custodian and Oracle Failure Risks

Custodians: Custodians may face default risks, leading to the inability to redeem reserve assets.

Oracles: For example, oracles like Chainlink may provide inaccurate data during network outages, resulting in mispricing of collateral.

Assessment Indicators

The degree of diversification of custodians.

The extent of insurance coverage.

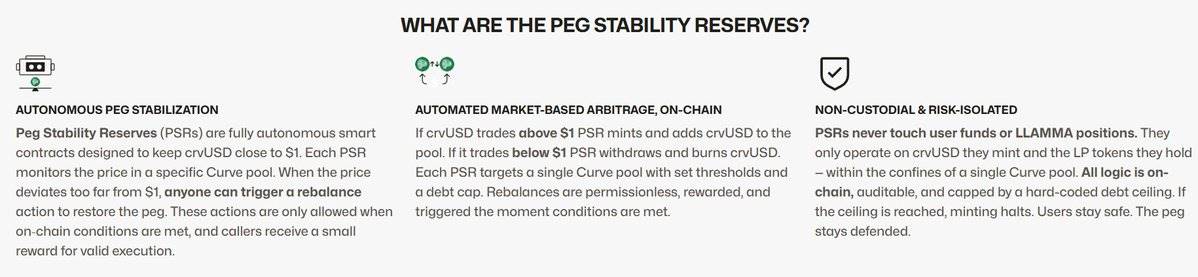

The level of decentralization of oracles. High reliance on centralized APIs may increase risk. For instance, Curve's crvUSD stablecoin calibrates oracle prices using price data from multiple stablecoins to ensure price accuracy.

Managing counterparty risk requires examination from multiple dimensions, including the decentralization of custodians, the reliability of oracle data, and their level of decentralization to mitigate potential crises arising from single points of failure.

Interdependency Risk

In asset tokenization scenarios, chain dependencies between counterparties may amplify issues. For example, if an associated protocol is hacked, it may lead to the freezing of stablecoin redemption functions.

Legal Protection Risk

In bankruptcy situations, holders may be classified as unsecured creditors, with very little recovery of funds. This highlights the importance of having diversified reserves. Some stablecoins operate models that rely on certain types of collateral, which may not even be directly held by them (often short-term government bonds with near-zero default risk). However, other protocols may overly depend on ETH-LST, BTC-LST, or SOL-LST, raising concerns about yield volatility.

Case Event: Celsius Network Bankruptcy

In June 2022, Celsius Network filed for bankruptcy due to liquidity issues in investments and counterparty defaults, freezing $4.7 billion of user funds.

Yield Volatility Risk

The yield of stablecoins typically comes from lending protocols or government bond investments, but these yields can fluctuate with changes in market conditions, lending demand, and interest rates. This volatility reduces predictability for users seeking stable passive income.

Important Supplementary Points

Factors Affecting Yield

In low-volatility environments, reduced lending demand leads to lower yields; conversely, yields may rise during bull markets.

For stablecoins pegged to real-world assets (RWAs), external interest rates (such as the Federal Reserve's fund rate) are also significant factors affecting yields.

Risk Assessment Indicators

Monitor historical yield ranges.

Analyze the correlation between yields and the Crypto Volatility Index (CVIX).

Pay attention to the protocol's utilization rate (a borrowing ratio exceeding 80% typically indicates higher yields, but risks also increase).

Sustainability Issues

High yields may signal potential risks, such as excessive leverage.

Sustainable yield models prioritize "Delta-neutral" strategies (like Ethena), achieving more stable yields by minimizing directional risk, which is part of their success.

User Impact

Yield volatility may lead to opportunity costs: users may miss out on other higher-yield opportunities.

If yields fall below fiat savings rates, users may also face the risk of inflation erosion.

Case Event: Decline in Yields for Aave and Compound

In the winter of 2022, due to weak lending demand, the yields for Aave and Compound dropped from over 10% to below 2%.

Specific Risk Analysis

Smart contract vulnerabilities (due to complex lending modules), regulatory risks (exposure to real-world assets related to U.S. government-supported securities triggering scrutiny), yield volatility (dynamic savings rates may decline).

Sky Dashboard Indicators

Specific Risk Analysis: Lending mechanism vulnerabilities (over-collateralization may trigger a liquidation chain reaction), yield generation failures (if lending demand declines, yields may drop to zero).

GHO Dashboard Indicators

Specific Risks: Insufficient collateral risk (if real-world assets depreciate), liquidation threshold risk (high volatility of underlying ETH/BTC), security module failure (similar to insurance buffers may be insufficient).

USR Dashboard Indicators

Specific Risks: Yield generated through automatically compounding staking rewards makes it susceptible to ETH punitive reduction events or low-yield periods, unlike fully over-collateralized stablecoins.

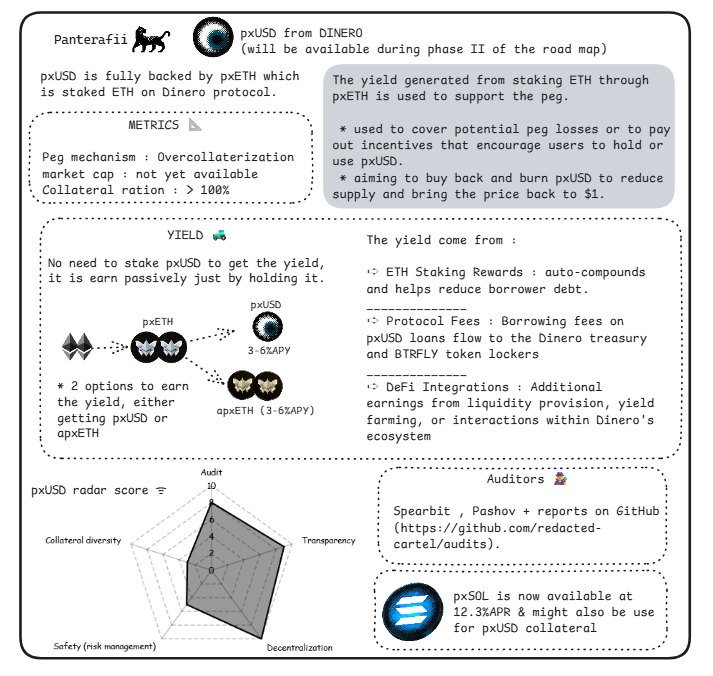

Dinero Dashboard Indicators

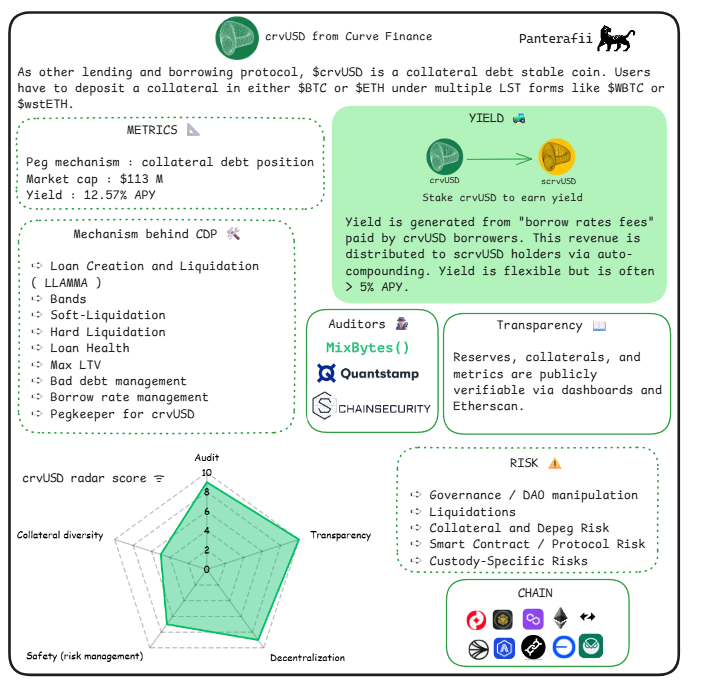

Specific Risks: The CDP model of crvUSD (healthy ratio of 150-167%, backed by BTC/ETH LST) focuses on lending, making liquidation chain reactions a major risk during market volatility, with yields sourced from flexible fees, typically yielding over 3.5% APY.

crvUSD Dashboard Indicators

Specific Risks: Market volatility of underlying assets (futures may lead to rapid losses), regulatory compliance issues (as a stablecoin pegged to PPI), counterparty risks from exchanges.

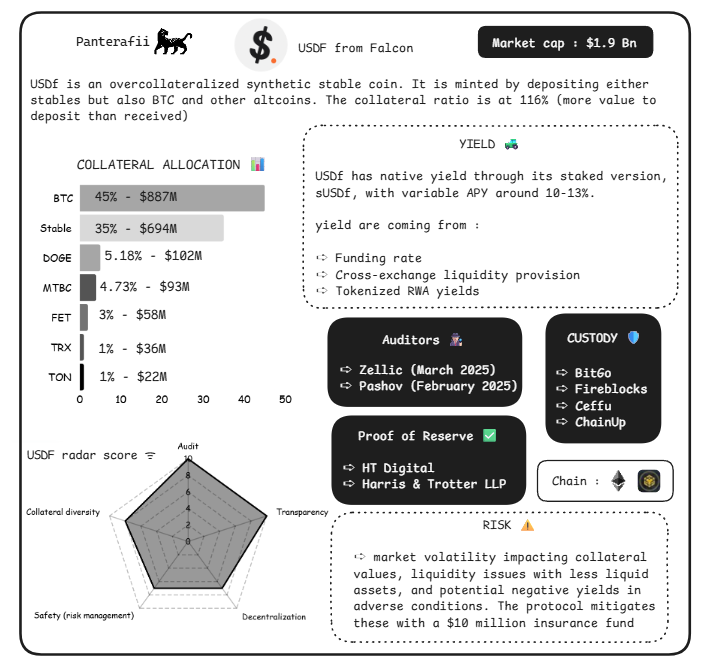

Falcon Dashboard Indicators

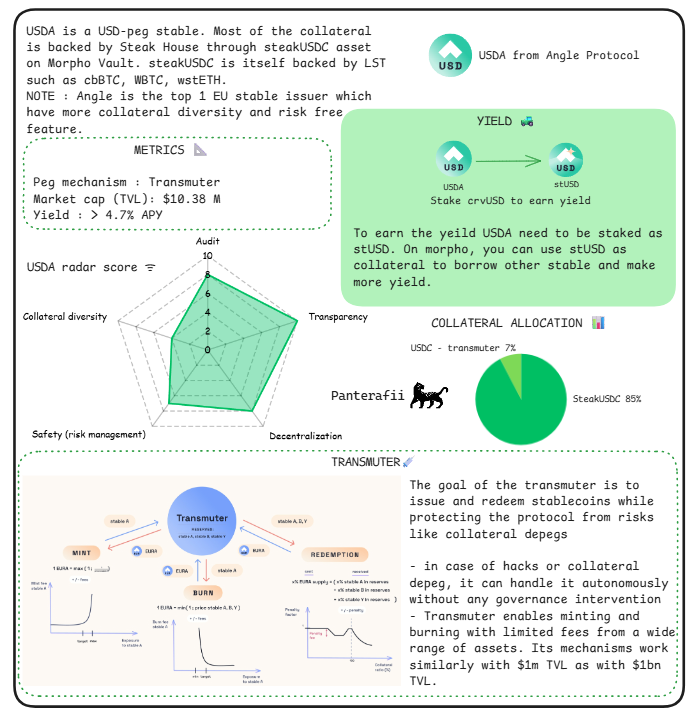

Specific Risks: The converter target of USDA aims to prevent depeg by allowing minting/burning with limited fees (e.g., the same for $1 million TVL and $1 billion TVL), but this also introduces autonomy risks, such as governance operating without intervention, making it vulnerable to hacks or the failure of its 85% steakUSDC-backed collateral.

Angle Analysis Indicators

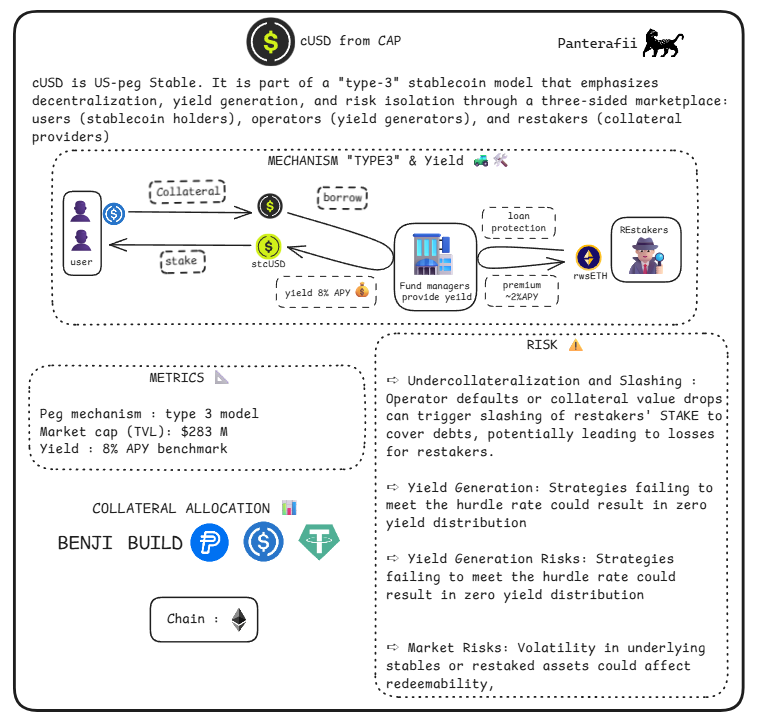

Specific Risks: The tri-party market of csUSD (holders, generators, re-stakers) achieves uniqueness through yield redistribution (sourced from government bonds/T-bills and liquid staking tokens LST), but this mechanism carries risks during balance changes, potentially leading to compatibility issues with DeFi protocols.

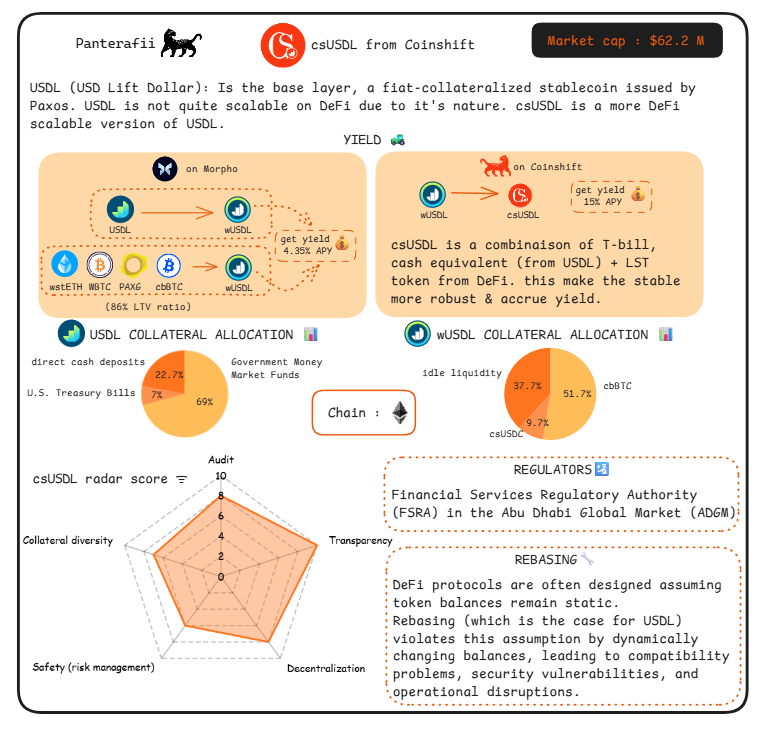

Coinshift Analysis Indicators

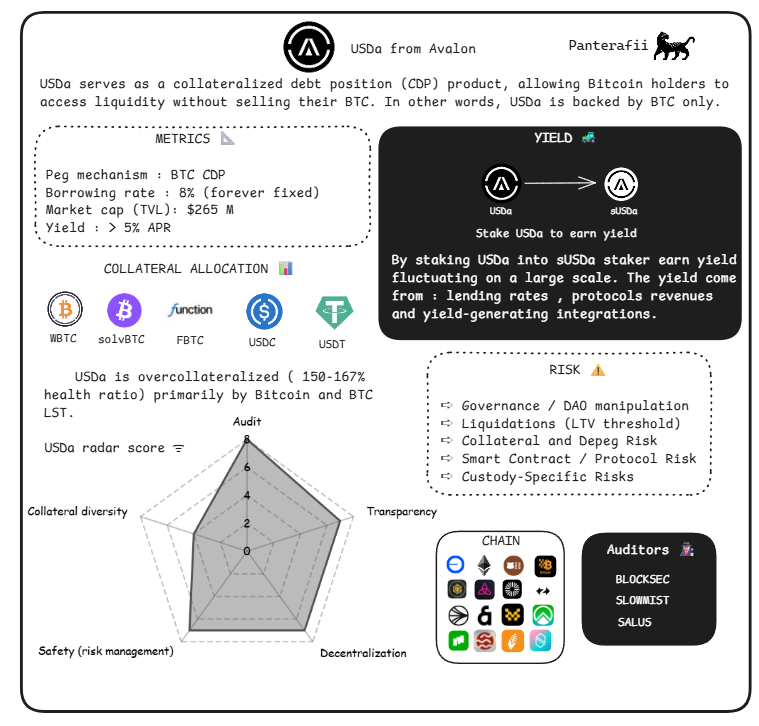

Specific Risks: The fixed lending rate of USDA (8%) and the CDP model that only supports BTC (with yields sourced from an annualized return of over 5%) expose it to the risk of BTC price fluctuations, unlike diversified collateral, which does not mention an over-collateralization buffer mechanism.

Avalon Analysis Indicators

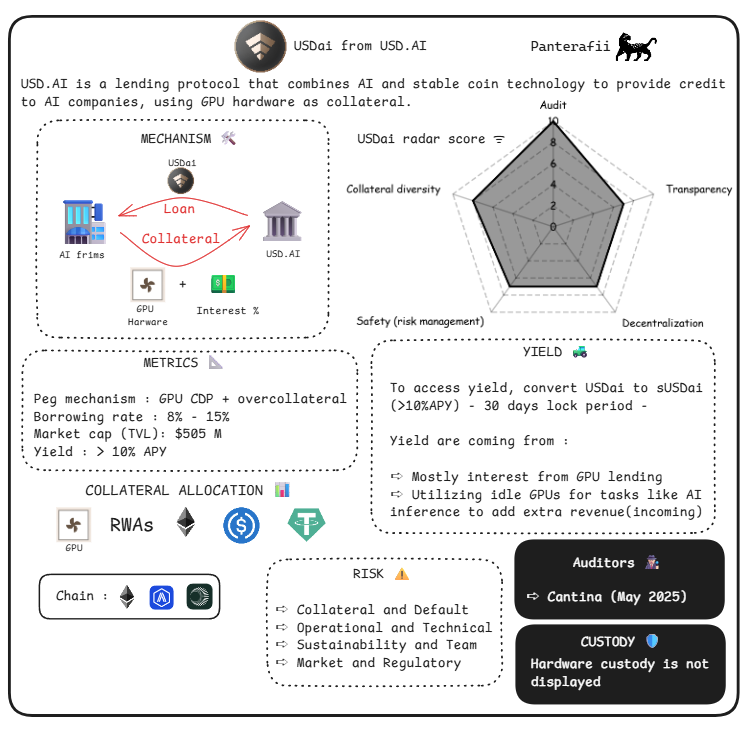

Specific Risks: GPU CDP is a non-liquid asset.

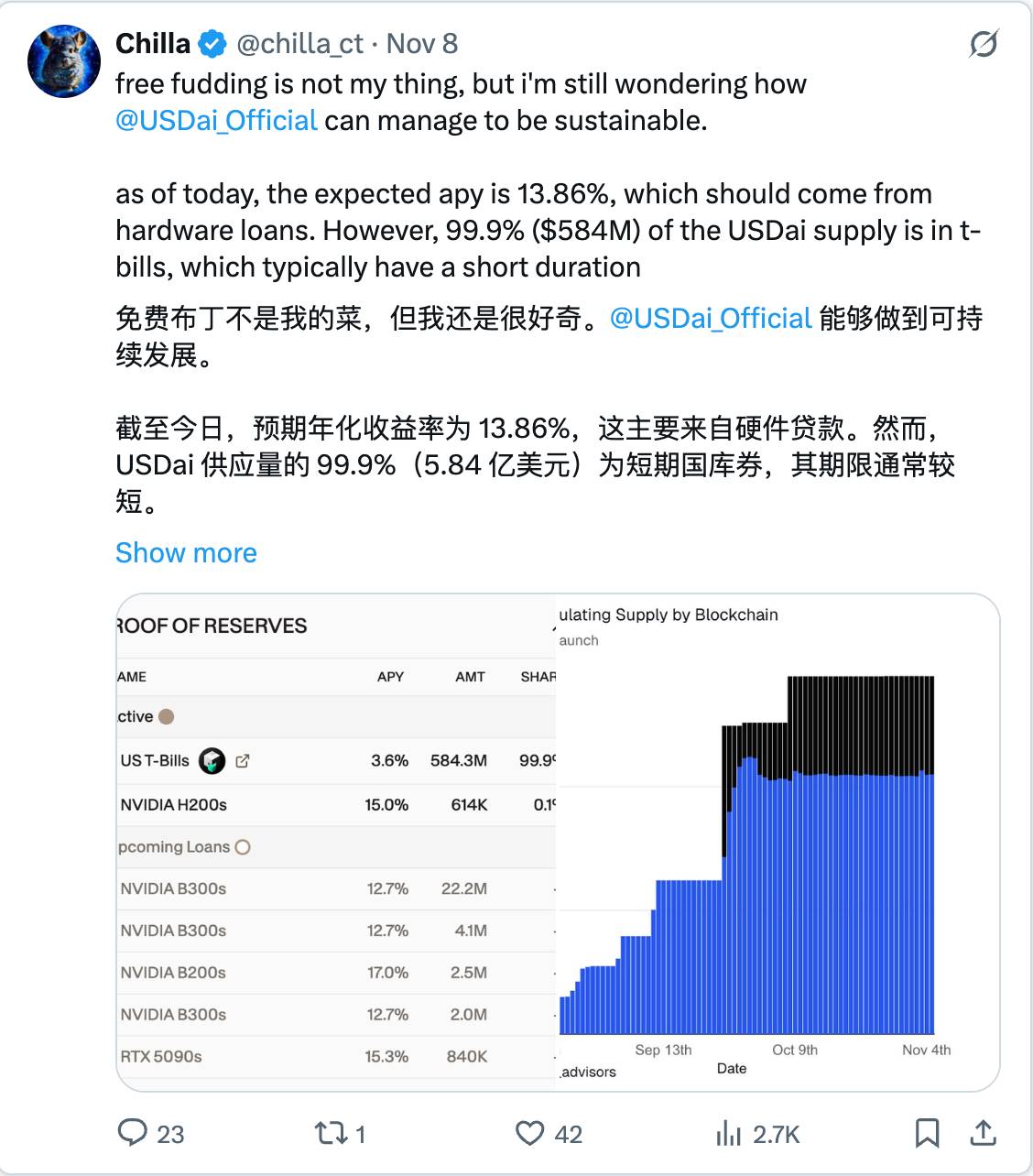

USDai Analysis Indicators

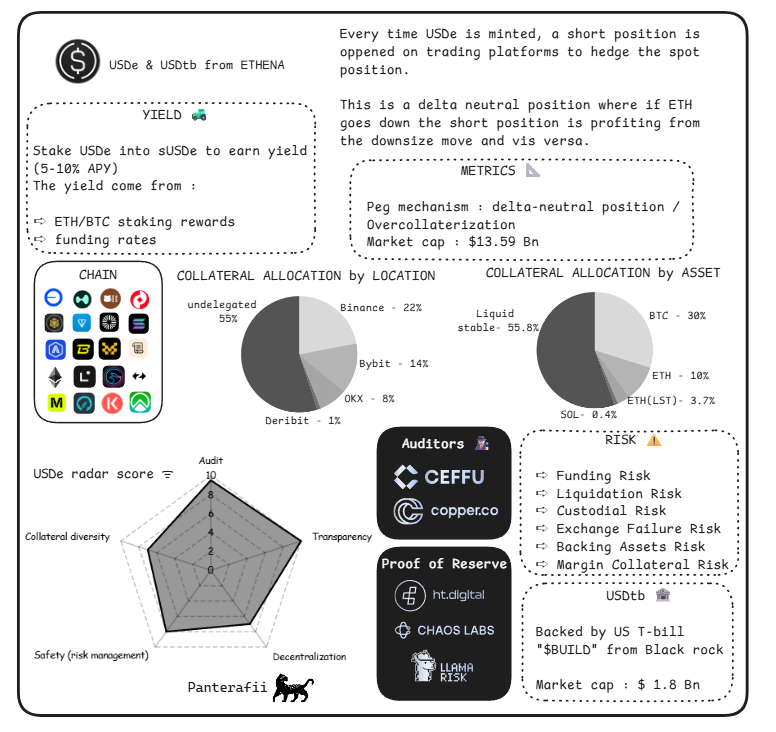

Specific Risks: Sharp interest rate hikes (futures positions may depreciate), funding rate fluctuations (negative rates erode yields), perpetual futures risks (market crashes leading to liquidations).

Ethena Analysis Indicators

Specific Risks: Custodial specific risks (real-world assets RWA managed by "Hashnote").

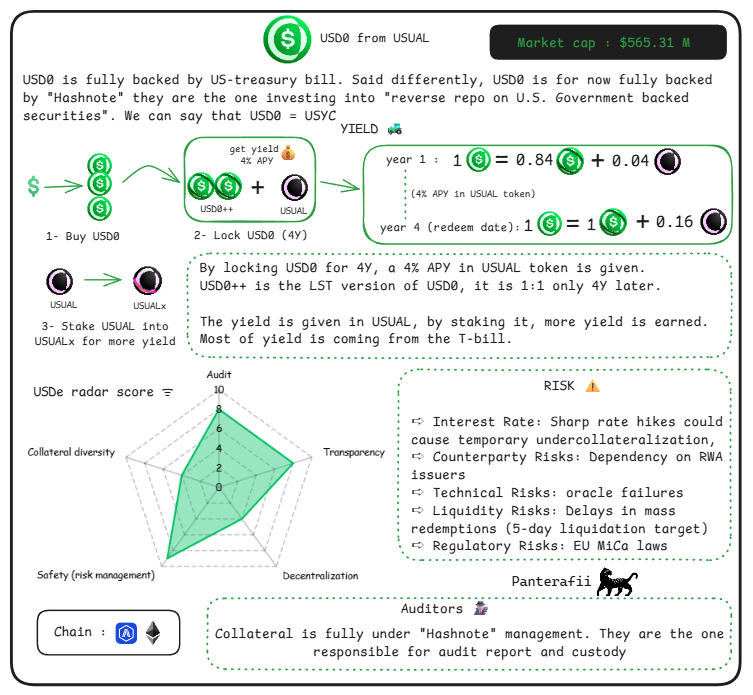

Usual Analysis Indicators

Specific Risks: The hybrid mechanism may exacerbate the risk of peg failure during economic changes.

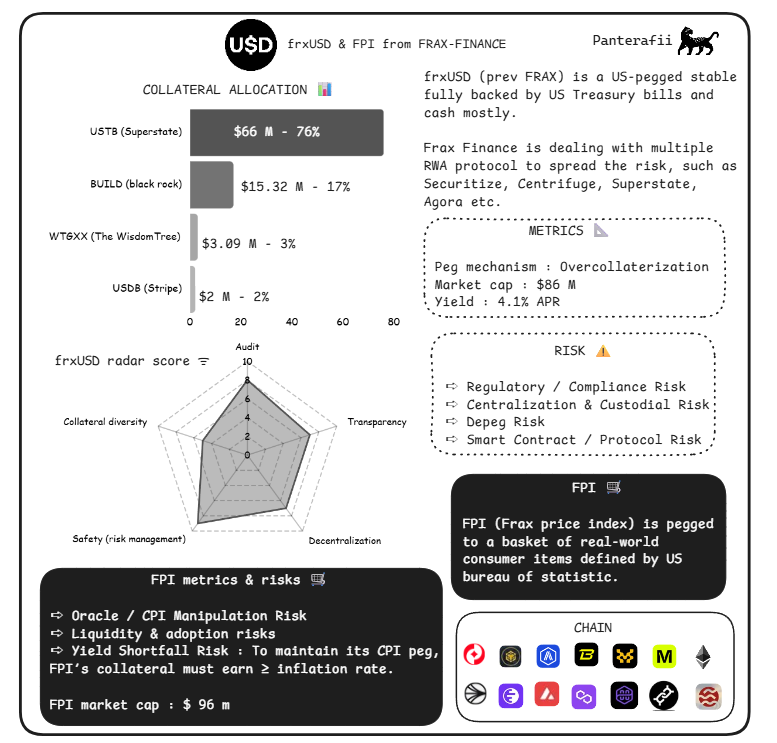

Frax Analysis Indicators

Paxos Transparency Report

Specific Risks: cUSD emphasizes decentralization, yield generation, and risk isolation through a tri-party market (holders, generators, re-stakers), which brings unique reduction risks for re-stakers. Its yield (based on an 8% annualized return) relies on the effectiveness of the loan protection mechanism, facing risks if it fails.

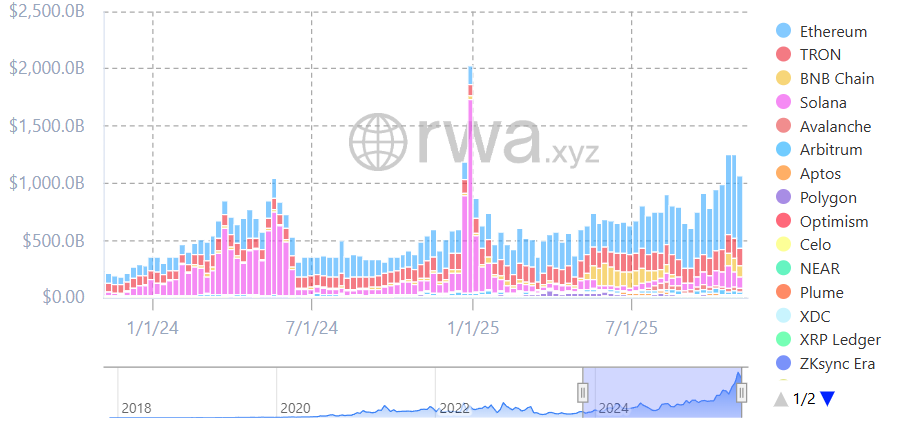

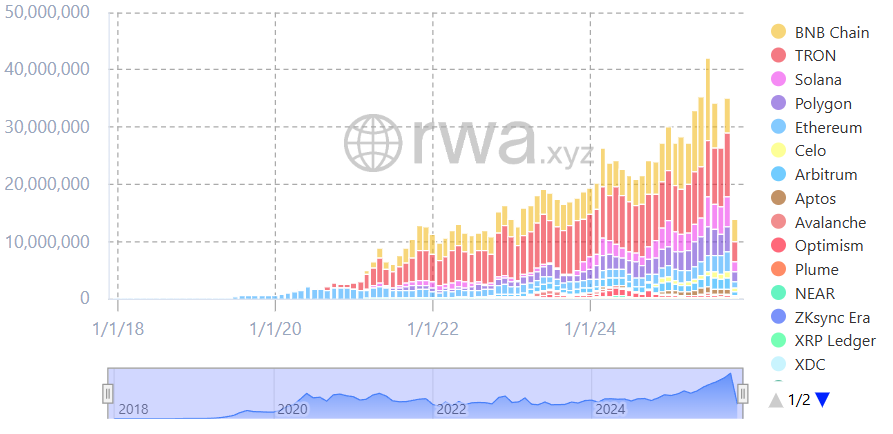

Current Status of Solana Stablecoin Ecosystem

The Solana ecosystem is experiencing rapid development of stablecoins, with market rumors suggesting the potential launch of ETF products, further driving ecosystem growth.

Figure: Stablecoin Transfer Volume

Solana ranks in the top five for on-chain stablecoin transfer volume.

Figure: Active Addresses for Stablecoins

Solana ranks in the top three for active addresses in the stablecoin network.

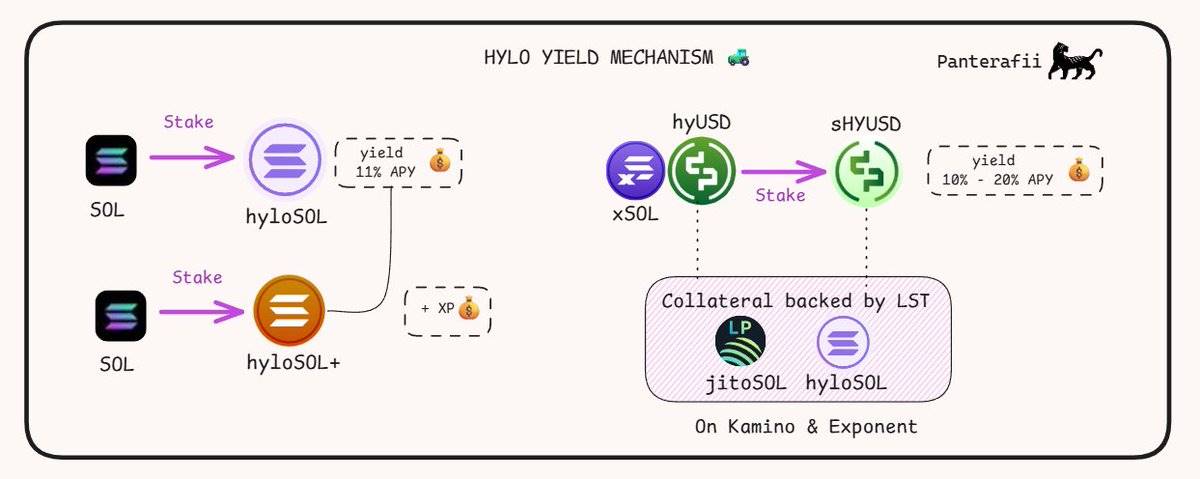

Several native stablecoins with innovative algorithmic mechanisms are emerging, including jupUSD launched by Jupiter, USX launched by Solstice, and hyUSD launched by Hylo.

These stablecoins all employ clever algorithmic mechanisms to maintain their pegs and are worth ongoing attention.

Here is an introduction to the yield mechanism of Hylo hyUSD:

hyloSOL: Hylo's LST (liquid staking token), generates yield through SOL staking rewards.

hyloSOL+: A gamified LST that only earns XP points, with actual yields transferred to hyloSOL holders.

hyUSD: Hylo's stablecoin, supported by various LSTs, backed by Solana DeFi strategies, but does not generate yield itself.

sHYUSD: The staked version of hyUSD, generating yield through DeFi strategies of LSTs.

xSOL: A buffer asset used to absorb volatility and adjust the peg price of hyUSD. This asset is a leveraged position on SOL prices, does not generate yield, but can earn XP points.

Conclusion

Sometimes, the relationship between yield and collateral does not always match. This was exactly what happened during the collapse of Terra Luna, when the APY stabilized at around 20%, but the income was significantly insufficient. Therefore, it is crucial to pay attention to the correlation between yield and collateral, as this is often the root of the problem.

Regarding the USDai stablecoin, our friends raised an interesting point:

USDai has responded to this issue, stating that there are delays in GPU loans. Borrowers hope to obtain USDai, while lenders struggle with the transportation issues of collateral. "NVIDIA B200 graphics cards were held up at French customs after leaving Taiwan," which is a typical case.

I hope you enjoyed this article. I firmly believe that DeFi will one day become the core force driving financial operations. Here, I shared some innovative ideas about strategies, concepts, and protocols.

Thank you for reading, and have a wonderful day!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。