Author: Thejaswini M A

Translation: Block unicorn

Preface

You should know that I often talk about this issue—the philosophical foundations, its history, and the complex agreements humans have reached to assign value to numbers on a piece of paper or a screen. And every time we delve deeper, we ultimately arrive at the same frustrating conclusion: its definition is always changing beneath our feet.

For most of human history, people have used a variety of things as currency: salt, shells, livestock, precious metals, and pieces of paper with promises written on them. What exactly makes something "currency," and what makes something merely "a valuable item" has never received a clear answer. We can usually recognize it at a glance, unless we cannot see it.

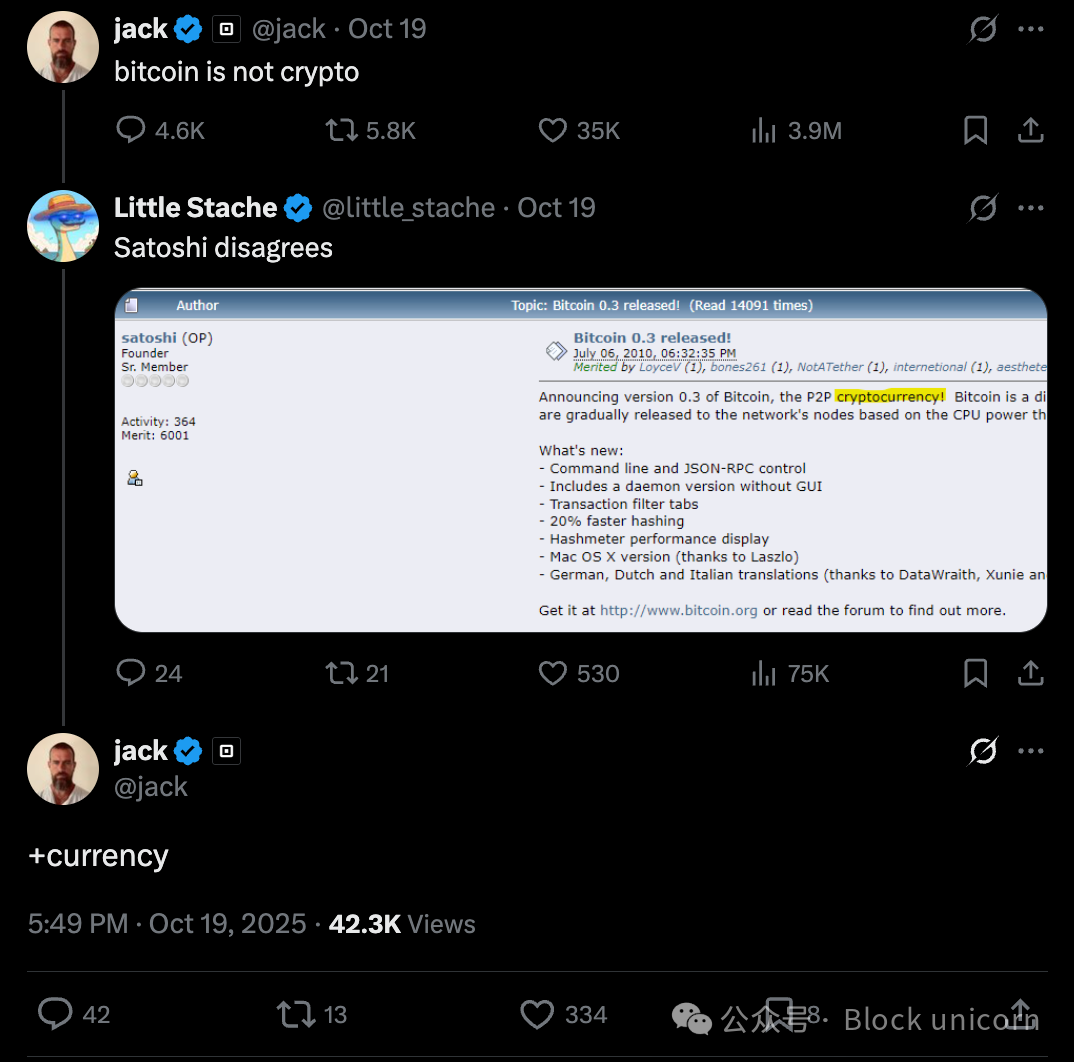

When Jack Dorsey tweeted that "Bitcoin is not a cryptocurrency," it touched a sensitive nerve in this long-standing debate. Because if Bitcoin is not a cryptocurrency, then what is it? If cryptocurrency is not Bitcoin, then what is it? More importantly: why does this matter?

The simplest explanation is that it is just tribalism. Extremists draw lines, and factions take sides. This boring debate makes normal people steer clear, as everyone involved seems a bit unhinged.

But I think there are other factors at play, some important ones that go beyond tribal warfare. I believe the market is slowly and painfully realizing that Bitcoin and cryptocurrency have never been the same thing, even though they have coexisted in the same space for fifteen years. The process of distinguishing them is not a breakup but a specialization.

This distinction is important because specialization is not about conflict; it is about function. The heart and lungs do not compete; they each serve different functions. If you try to make the heart also perform the function of breathing, what you get is not a more efficient organism but a dead one.

The differentiation between Bitcoin and cryptocurrency does not stem from mutual hostility but from their fundamentally different design intentions. One aims to be currency, while the other tries to be everything else. Their success lies precisely in the fact that they no longer attempt to be each other.

This sounds like a war. But wars are fought for victory, while this is merely about distinction.

Dorsey's Tweet Was Just the Spark

Why am I bringing this topic up again?

Listen, when Jack Dorsey tweeted that "Bitcoin is not a cryptocurrency," you have to stop and think about what is really happening here. He is the co-founder of Twitter and Square (now renamed Block), and his advocacy for Bitcoin is almost fanatical; he has even described the Bitcoin white paper as "poetry." He is a bona fide Bitcoin extremist: he believes Bitcoin is the only important digital asset, and everything else is at best noise and at worst a scam.

So when Dorsey made this statement, it felt significant, like announcing a breakup. Extremists cheered, while cryptocurrency developers scoffed. Everyone took sides.

On the other hand, the Czech Republic has just included Bitcoin in its national balance sheet. It is not a large scale, enough to change the landscape. But this follows the establishment of a strategic Bitcoin reserve in the U.S. in March, prompting 45 states to propose their own reserve bills, with Arizona, New Hampshire, and Texas already passing related legislation. Luxembourg's sovereign wealth fund has also fully shifted to Bitcoin investment.

They examined the entire digital asset space and ultimately chose one thing. Why?

For years, Bitcoin and "cryptocurrency" have been conflated. Journalists talk about the "cryptocurrency market," which encompasses everything from Bitcoin to Dogecoin to any new token launched this morning. Regulators discuss "digital assets" and refer to them collectively as "digital assets." Asset management firms allocate "cryptocurrency assets" in their portfolios. Industry insiders track "Bitcoin's market cap share" to measure Bitcoin's proportion of the total cryptocurrency market cap, implying that all cryptocurrencies are competing for the same pie.

But this framework is beginning to crumble. This is not due to ideology or tribalism, but because of how institutions actually treat these things, how the market actually prices them, and how people actually use them.

When Fidelity released research on Bitcoin, it did not refer to it as "crypto assets," but as "monetary assets." BlackRock described it as "digital gold" and "a non-sovereign store of value." This is not just simple marketing language, but a fundamental classification that distinguishes Bitcoin from all other assets. They did not compare Bitcoin to Ethereum as one would compare Coca-Cola to Pepsi; instead, they view Bitcoin as a distinct asset class.

And all of this happened before Dorsey tweeted anything. Hardcore Bitcoin holders had already distinguished Bitcoin from cryptocurrency in their minds years ago. They just did not announce it through a press release.

What Bitcoin Wants

Bitcoin's design revolves around several very clear priorities: security, predictability, decentralization, and monetary credibility. These characteristics make it difficult to change. Bitcoin's development culture is known for being extremely conservative, with any upgrades requiring years of discussion. The entire system is designed to be hard to modify.

You could call this a flaw. Many people do. They point out that Bitcoin's ten-minute block time is laughably slow compared to some emerging blockchains. They also note that Bitcoin cannot run smart contracts, decentralized applications, or the advanced programmability that Ethereum supports. All these criticisms are valid.

But from another perspective: Bitcoin is not trying to do everything. It seeks to excel at one thing: to be a reliable, predictable, censorship-resistant currency.

Predictability is especially important. Bitcoin's total supply cap is set at 21 million coins, a limit that is written into the protocol. Changing the cap would require immense computational power and likely necessitate a hard fork. For many, the 21 million cap represents Bitcoin and is a key feature that distinguishes it from fiat currency and cryptocurrency. Therefore, the cap has remained unchanged and has been maintained for 16 years. The same monetary policy, time and again, without any surprises.

Now look at almost all other cryptocurrencies. Ethereum's mechanisms have undergone significant changes. It transitioned from proof of work (PoW) to proof of stake (PoS). It also plans to achieve deflation of Ether through ERC 1559. These are interesting technical decisions, but they are precisely at odds with predictability. Each change serves as a reminder that the rules could change again at any moment.

Sure, I would tell you these changes have made the system better. But you might ask, in what ways is "better" manifested? If you want to build a neutral, long-term value storage system, then changing the rules is not an advantage; it is a disadvantage. But if you want to build an application platform that can iterate quickly and serve developers, then changing the rules is fantastic. You should constantly change the rules, release quickly, and be bold in experimentation.

The key is: the goals are different.

What Cryptocurrency Wants

The broader cryptocurrency ecosystem, everything outside of Bitcoin, looks more like a tech sector than a monetary system. It pursues speed, programmability, and innovation. New layer two scaling solutions emerge every few months. There is decentralized finance, including lending protocols, derivatives, and liquidity mining. There is decentralized physical infrastructure. There are games. There are NFTs. And various things that may emerge in the future.

The pace is extremely fast, the cycles are very short, and the ambitions are vast.

Cryptocurrency operates similarly to Silicon Valley. Venture capital floods in. Founders raise funds, launch products, pivot when problems arise, and launch products again. Some projects achieve tremendous success, but most fail. There are hype cycles and crashes, with different narratives each quarter. After the summer of DeFi came the NFT craze, after the NFT craze came the Layer 2 boom, and now we have everything that is happening.

Monetary systems do not operate this way. You do not want the money supply to change based on market trends. You do not want foundation members voting on whether to change the issuance plan. You do not want accounting units to iterate frequently.

So cryptocurrency and Bitcoin play different roles. Cryptocurrency wants to develop into a tech industry, while Bitcoin wants to become a currency. This is not a competing vision; it is about playing different roles within the same economic system.

Why This Looks Like a Breakup

From the outside, this split appears quite hostile. Bitcoin maximalists dismiss other cryptocurrencies as scams or distractions. They will tell you that all cryptocurrencies other than Bitcoin are either securities, cumbersome centralized databases, or solutions created to solve a problem that does not exist. Meanwhile, cryptocurrency developers believe Bitcoin lacks flexibility and is outdated. They point out Bitcoin's limited functionality and think the maximalists' mindset is stuck in 2009.

The market's attitude towards them is also starkly different. Bitcoin has its own cycles, its own development trajectory, and its own institutional buyers. When MicroStrategy (sorry, should be "Strategy") spends billions of dollars buying Bitcoin, they do not casually buy some Ethereum to diversify risk. When El Salvador legalized Bitcoin, they did not include the top ten cryptocurrencies by market cap.

Regulators are also increasingly focused on distinguishing these tokens. Bitcoin is generally viewed as a commodity. Most other tokens exist in a gray area, with their classification as securities depending on how they were issued and who controls them. This leads to different regulatory frameworks, different compliance requirements, and different risk profiles.

So yes, it looks like a breakup. Different treatment, different communities, different use cases.

But what if this separation is not hostile? What if they are just doing different things?

Asymmetric Dependency

The demand for Bitcoin from cryptocurrency far exceeds Bitcoin's demand for cryptocurrency.

Bitcoin lends legitimacy to the entire space. It is the entry point for institutional investors, a reference asset for new users, and the benchmark for all digital assets. When people talk about "blockchain technology," they are actually referring to the technology pioneered by Bitcoin. Regulators, when formulating digital asset regulatory strategies, first consider Bitcoin and then explore the differences among other assets.

Bitcoin also determines the liquidity cycle. Bull markets typically begin with Bitcoin. Funds first flow into Bitcoin and then shift to riskier crypto assets. This pattern has persisted across multiple cycles. Without Bitcoin's liquidity and market recognition, the structural weaknesses of the entire cryptocurrency market would become even more apparent.

Bitcoin plays the role of a reserve asset in the cryptocurrency space. Even as these ecosystems become increasingly differentiated, Bitcoin remains the dominant asset for large-scale settlement, long-term storage, and cross-border value transfer. It is the closest thing to digital gold.

The reverse is not true. Bitcoin does not need innovation from the cryptocurrency realm. It does not require smart contracts, DeFi, NFTs, or anything else. Bitcoin can quietly sit there, slowly processing transactions, maintaining its monetary policy, and preserving its consistent nature. That is the key.

This creates an interesting dynamic. Cryptocurrency revolves around Bitcoin. Bitcoin is like the sun. These planets can spin wildly, try new things, and collide with each other, but the gravitational center remains unchanged.

The Real Problem

If Bitcoin wants to be a currency, it faces a problem: people simply do not spend it.

Every Bitcoin holder knows the story of Laszlo's pizza. This story has a certain impact on your brain. It makes you afraid to spend Bitcoin because what if it goes up in price? What if the pizza you bought becomes the next billion-dollar pizza?

This is not a quirk of early users but a fundamental aspect of human nature. When you hold an appreciating asset, you do not spend it; instead, you hoard it. You will spend the underperforming assets first and save the best-performing ones for last. This is known as Gresham's Law: bad money drives out good. If some of the currency you hold might appreciate by 100% next year while others definitely will not, you will prioritize spending the ones that are unlikely to appreciate and save the ones that might.

Thus, Bitcoin's success as a store of value has ironically made it a poor medium of exchange. People view it as digital gold because it is indeed like gold: scarce, valuable, and you definitely do not want to use it to buy coffee.

Moreover, there is the issue of the unit of account. A currency should serve three functions: a store of value, a medium of exchange, and a unit of account. Bitcoin does well as a store of value but performs poorly as a unit of account. And the real problem lies in the unit of account.

No one prices things in Bitcoin. Wages are paid in dollars, euros, or rupees. Rent is paid in fiat currency. Company accounting is also done in fiat currency. Even tickets to Bitcoin conferences are usually priced in dollars. You might be able to pay with Bitcoin, but the price is set in fiat currency first and then converted.

Why? Because Bitcoin is too volatile to price things directly in it. You cannot walk into a coffee shop and see a sign that says "Coffee: 0.0001 BTC," because tomorrow that number might change to 0.00008 BTC or 0.00015 BTC, depending on the overnight market conditions. A currency that is not used for pricing goods cannot function as a medium of exchange. It can only serve as an asset that you convert into real currency before purchasing goods.

Even when merchants "accept Bitcoin," what actually happens is more telling: Bitcoin is immediately converted into fiat currency at the time of the transaction. The merchant receives dollars or euros, not Bitcoin. So, you are essentially using Bitcoin as an unnecessary intermediary—converting your appreciating asset into currency you could have used directly.

In a few specific scenarios, this logic holds. If you are in Turkey, Venezuela, or Argentina, where the local currency is inflating faster than Bitcoin's volatility, then Bitcoin indeed becomes a more stable option. But this does not mean Bitcoin is good money; it indicates that in these specific regions, fiat currency is bad money.

This is why Jack Dorsey's Cash App announced this week that it will support stablecoins, choosing to develop on Solana rather than Bitcoin. For Bitcoin maximalists, this is like a vegetarian opening a steakhouse. But if you understand the true purpose of each thing, it all makes perfect sense.

Stablecoins are the currency people use for payments. They are pegged to the dollar, so there is no consumption risk like with Bitcoin. No one worries that their USDC will appreciate tenfold next year, so they can spend it with confidence. Stablecoins, while dull, are stable and reliable, and they indeed facilitate the transfer of funds.

Bitcoin is a tool for people to store value. It is scarce, hard to inflate, and not controlled by any government. But you would not use your 401(k) retirement account to buy coffee, and you should not use your Bitcoin to buy coffee either.

Layered Model

So, perhaps the digital asset economy is not splitting but rather self-organizing into different layers, each playing its own specialized role:

Layer 1: Bitcoin—Monetary Base Layer

A non-sovereign store of value, with predictable issuance and global neutrality. It grows slowly and steadily, designed to last for decades. Institutions view it as digital gold. People hoard it. This is normal. This is its significance.

Layer 2: Stablecoins—Medium of Exchange Layer

Digital versions of fiat currency that people actually use. They are fast, cheap, but also quite boring. They do not appreciate, so you do not feel guilty spending them. They exist on various blockchains, including Bitcoin's Lightning Network, as well as Ethereum, Solana, Tron, etc., depending on which blockchain is best suited for specific applications.

Layer 3: Crypto Networks—Application Layer

Platforms empowering financial markets, decentralized applications, tokenized assets, and everything that may come in the future. Innovation happens here. This is the tech industry. It is fast-paced, venture-backed, sometimes incredibly foolish, but occasionally bursts forth with astonishing wisdom.

This model reflects how traditional economies operate. Gold is a store of value, fiat currency is a medium of exchange, and financial markets and tech companies develop applications on this foundation. No one expects gold to simultaneously serve as a payment channel and a smart contract platform. Different things serve different functions.

These are not competing investment vehicles.

Bitcoin has not broken up with cryptocurrency; it is simply adapting to its role. Cryptocurrency is doing the same. And stablecoins fill the gap that neither can address.

It is not a breakup; it is specialization.

And this specialization is the cornerstone of the future architecture of digital currency—Bitcoin provides the foundation for a complex, diverse, and rapidly evolving ecosystem.

The question has never been about whether Bitcoin or cryptocurrency will prevail. The real question is how they can coexist in a system where each plays to its strengths and collaborates.

This system is gradually taking shape. The "breakup theory" completely overlooks this.

That’s all for today; see you in the next article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。