Original Author: Biteye Core Contributor viee

Original Editor: Biteye Core Contributor Denise

From the halving in April 2024 to a new high of $120,000 in October 2025, Bitcoin has gone through nearly 18 months. If we only look at this path, it seems to still be operating according to the cycle. Halving leads to a bottom, followed by a peak within a year, and then a correction.

However, what truly confuses the market is not whether there has been an increase, but that it has not increased as it usually does.

There has been no series of explosive rises like in 2017, nor the nationwide frenzy seen in 2021. This round of market activity appears slow, dull, and with converging volatility; the progress of ETFs has been inconsistent, and the rotation of altcoins has been weak. Even after reaching a new high, it fell below $90,000 in less than a month. Is this a bull market or the beginning of a bear market?

Therefore, this article will delve into:

(1) Why many people feel that the four-year cycle has failed

(2) Which parts of the four-year cycle theory are still effective

(3) What factors have disrupted the cycle

1. Why do more and more people feel that the four-year cycle is ineffective?

Although Bitcoin's price has risen after the halving, this round of market activity has felt off from start to finish.

Bitcoin completed its halving in April 2024, and according to historical patterns, the following 12 to 18 months should see a major upward wave and peak in sentiment. This has been somewhat the case, as Bitcoin reached a new high of $125,000 in October 2025. However, the real issue is that this round of market activity lacks the final frenzy and the widespread emotional engagement. Shortly after reaching a new high, the price quickly fell by 25%, briefly dropping below $90,000. This is not the "bubble tail" that should appear in a typical cycle; it feels more like the market was extinguished before it even heated up.

Additionally, sentiment is clearly low. In past bull market peaks, on-chain capital was active, altcoins surged, and retail investors rushed in. Yet, in this round, Bitcoin's market dominance remains close to 59%. This indicates that most capital is still concentrated in mainstream coins, with altcoins lagging behind and lacking explosive rotation. Compared to the tenfold or even hundredfold increases in previous cycles, this round has seen Bitcoin rise only 7 to 8 times from its low at the end of 2022 to its high; from the halving point, the increase is less than 2 times.

The mildness of the market is also reflected in the capital structure. After the launch of ETFs, institutions began to buy continuously, becoming the main force in the market. Institutions are more rational and better at controlling volatility, which has led to a decrease in the amplitude of market sentiment fluctuations and a smoother trading rhythm. The price formation mechanism has changed; it is no longer solely determined by "supply and demand," but is more driven by structural trading logic.

In summary, the various anomalies in this round, including the retreat of sentiment, weakening returns, disrupted rhythm, and institutional dominance, have indeed led the market to intuitively feel that the familiar four-year cycle is no longer effective.

2. Which parts of the four-year cycle theory are still effective?

Despite the chaotic surface phenomena, a deeper analysis reveals that the logic of the four-year cycle theory has not been completely lost. The fundamental factors such as supply and demand changes triggered by the halving are still at play, albeit in a more subdued manner than before.

The following will analyze the effective parts of the cycle theory from three aspects: supply, on-chain indicators, and historical data.

2.1 Long-term Supply Logic of Halving

Bitcoin halves every four years, meaning that new supply continues to decrease. This mechanism remains a key logic supporting price increases in the long run. In April 2024, Bitcoin completed its fourth halving, reducing the block reward from 6.25 BTC to 3.125 BTC.

Although the total supply of Bitcoin is nearing 94%, the marginal changes brought about by each halving are becoming smaller, but the market's expectation of scarcity has not disappeared. After previous halvings, the long-term bullish sentiment in the market has remained evident, with many choosing to hold rather than sell.

This round is no different. Despite significant price volatility, the impact of tightening supply is still present. As shown in the chart, Bitcoin's unrealized market value and realized market value in 2025 have significantly increased compared to the end of 2022, indicating that a large amount of capital has continued to flow into Bitcoin in recent years.

2.2 Periodicity of On-Chain Indicators

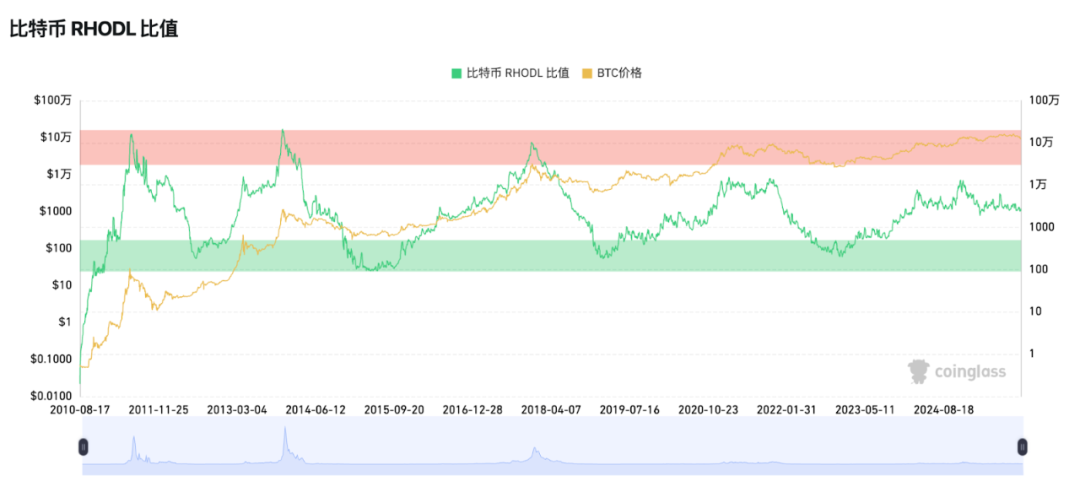

The behavior patterns of Bitcoin investors exhibit a cyclical "hoarding-sell-off" cycle, which is still reflected in on-chain data. Typical on-chain indicators include MVRV, SOPR, and RHODL.

- MVRV is the ratio of market value to realized value. When the MVRV value rises, it indicates that Bitcoin is overvalued. At the end of 2023, MVRV fell to 0.8, rose to 2.8 during the bullish market in 2024, and fell below 2 during the correction in early 2025, indicating that the valuation is neither overvalued nor undervalued, and the overall cyclical rise and fall rhythm is still present.

- SOPR can be simply understood as the price at which an asset is sold divided by the price at which it was bought. According to cyclical patterns, SOPR=1 is seen as the dividing line between bull and bear markets; below 1 indicates a loss on sales, while above 1 indicates most are in profit. In this cycle, SOPR remained below 1 during the 2022 bear market, but rose above 1 after 2023, entering a profit cycle. During the bull market phase from 2024 to 2025, this indicator has mostly remained above 1, consistent with cyclical patterns.

- RHODL measures the ratio of "realized value" between short-term holders (1 week) and medium to long-term holders (1-2 years) to identify market top risks. Historically, when this indicator enters a very high zone (red band), it often corresponds to the peaks of bull market bubbles (such as in 2013 and 2017). In 2021-2022, RHODL surged again, although it did not break historical extremes, it indicated that the market structure was entering its later stages. Currently, this indicator has also reached a cyclical high, which to some extent suggests that prices are at a peak.

In summary, the cyclical phenomena reflected by these on-chain indicators still resonate with historical patterns. Although the specific values may differ slightly, the on-chain logic of bottoms and tops remains clear.

2.3 Diminishing Returns Seem Inevitable

From another perspective, the diminishing returns at each cycle peak compared to the previous cycle are actually a normal part of the cyclical evolution. From 2013 to the 2017 peak, the increase was about 20 times, while from 2017 to 2021, the increase shrank to about 3.5 times. In this round, the rise from $69,000 to $125,000 represents an increase of about 80%. Although the increase has clearly converged, the trend line continues, and it has not completely deviated from the cyclical path. This marginal decrease is also a result of the market's expansion and the weakening marginal push of incremental capital, which does not indicate a failure of cyclical logic.

Ultimately, the logic of the "four-year cycle" is still at work at certain times. The halving affects supply and demand, and market behavior still follows the rhythm of "fear-greed," but this time the market activity is not as easily understood as before.

3. The Truth Behind the Cycle Confusion: Too Many Variables, Fragmented Narratives

If the cycle is still present, why is this round of market activity so difficult to read? The reason lies in the previously singular halving rhythm, which is now disrupted by multiple forces. Specifically, there are several reasons that make this round of cycles different from the past:

1. Structural Impact of ETFs and Institutional Funds

Since the launch of Bitcoin spot ETFs in 2024, the market structure has undergone significant changes.

ETFs represent "slow capital," continuously accumulating during price increases and also seeing some buying during declines. However, it is important to note that in the past week, institutional funds have withdrawn on a large scale; for example, in the past two days, the net outflow from the U.S. Bitcoin ETF reached as high as $523 million, with a monthly total exceeding $2 billion. This indicates that the current moment is not the best time for "entry and accumulation." Accumulation signals should at least wait until the outflow of funds stops and turns into sustained net inflows, with institutional actions primarily focused on buying.

ETFs not only bring in a large amount of incremental capital but also enhance price stability, with average holding costs around $89,000, forming effective support. This has made the rhythm of the Bitcoin market slower and steadier, but once support or resistance levels are breached, volatility can become more intense. This is a rare characteristic in traditional cycles and has reduced market fluctuations.

2. Fragmented Narratives and Accelerated Hotspot Rotation

In the previous bull market (2020-2021), DeFi and NFTs created a clear value narrative, while the current market resembles a collection of fragmented hotspots:

- From the end of 2023 to early 2024, Bitcoin ETFs dominated, later entering a craze for inscriptions;

- In 2024, Solana and meme narratives rose;

- Then Crypto AI and AI agents became hot topics;

- By 2025, InfoFi, Binance alpha, prediction markets, and x402 took turns in the spotlight…

The rapid rotation of narratives and the weak continuity of hotspots have led to high-frequency capital switching, making it difficult to form medium to long-term allocations. Moreover, the previous cycle's pattern of "Bitcoin leading, altcoins following" has become unreliable. The current market resembles a series of small cycles stitched together, with some sectors heating up and cooling down, and some assets peaking early, while Bitcoin fluctuates in between. This layered and interwoven structure has diminished the decisive role of the halving rhythm.

3. Reflexivity Intensified

In addition to ETFs, funds, and narratives, we also face another phenomenon: the cycle itself is "self-influencing," which is reflexivity.

Because everyone knows the halving pattern, they tend to preemptively position themselves and cash out early, leading to an overdrawn market. At the same time, ETF holders, institutional market makers, miners, and others are also making strategic adjustments based on the cycle. Whenever prices approach theoretical peaks, there may be a large number of profit-takers who sell off first, artificially advancing the cycle rhythm.

In summary, breaking down this round of market activity reveals that the so-called cycle confusion is more about the increased driving forces. The market structure has changed, participants have changed, and the way emotions are spread has also changed. This suggests that the past method of watching the timetable to bet on bull and bear markets may be becoming outdated, requiring a deeper understanding of the larger context.

4. Market Perspective Summary

Faced with the uncertainty of the market, different KOLs have provided various judgments. Through these perspectives, we may better understand the current market sentiment.

@BTCdayu believes that the four-year cycle no longer exists, as Bitcoin has shifted from being driven by halving to being driven by institutions, with the weight of retail investors gradually being diluted.

Bitwise CEO @HHorsley also tweeted that the traditional "four-year cycle" model is no longer applicable, as the structure of the crypto market has undergone profound changes. He believes that the market actually entered a bear market six months ago and is now in its final stages, with the fundamentals of overall crypto assets being stronger than ever.

@Wolfy_XBT argues that the halving rhythm has never failed, stating that this bull market ended on October 6, and the current market is entering the early stages of a bear market. The four-year cycle still holds, and the macro narrative and short-term sentiment are merely noise; the cyclical theory born around Bitcoin's halving is the most reliable signal.

@0xSunNFT expresses that whether on a large scale like the four-year halving cycle or on a smaller scale like local market movements, cycles still exist. Every round of market activity has a period of silence, and the key is to understand the rhythm of the cycle. Whether it's ETH, XPL, or meme coins, there are still opportunities for repeated fluctuations within the cycle; the key is not to be swayed by short-term emotions.

@lanhubiji shares a view similar to that of this article, believing that the cycle has not disappeared but has "deformed." With an excess of memes and the dysfunction of altcoins, the market has become fragmented, necessitating new methods for cycle judgment.

From these viewpoints, it is evident that the debate between "the cycle is dead" and "the cycle is still present" is more about different interpretations of changes in market structure. The cycle may not have disappeared; it simply requires a more complex perspective to recognize its existence.

5. Conclusion

So what should we look for in the future?

For ordinary retail investors, the most realistic approach may not be to predict the cycle, but to try to build their own market perception, such as learning to use data to assist in judgment, avoiding the traps brought by emotional fluctuations, and seeking high-cost-performance opportunities rather than chasing every hot trend.

Currently, the cycle is still present, but it is more chaotic and dynamic; we cannot think of the market as "it should rise when the time comes." Many phenomena indicate that the current phase of rising may likely have ended, so now is the defensive phase. The most important thing is to preserve capital and not to go all in easily. The market may experience a volatile rebound, but it resembles a fleeing market rather than a new bull market.

The true bottom usually does not form all at once; it gradually takes shape after repeated fluctuations. Maintaining cautious restraint and keeping some capital available may allow one to wait for the next real opportunity. Surviving is more important than guessing correctly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。