Original | Odaily Planet Daily (@OdailyChina)

The market is sluggish, and investors are on high alert.

In the past week, the frequent large transfers of BTC and ETH from BlackRock to Coinbase have attracted much attention from investors. Many interpret these transfer activities as signals of a market dump and attempt to analyze short-term market trends based on these signals. But is this methodology really valid?

- Odaily Note: BlackRock transferred a large amount of BTC and ETH to Coinbase again last night.

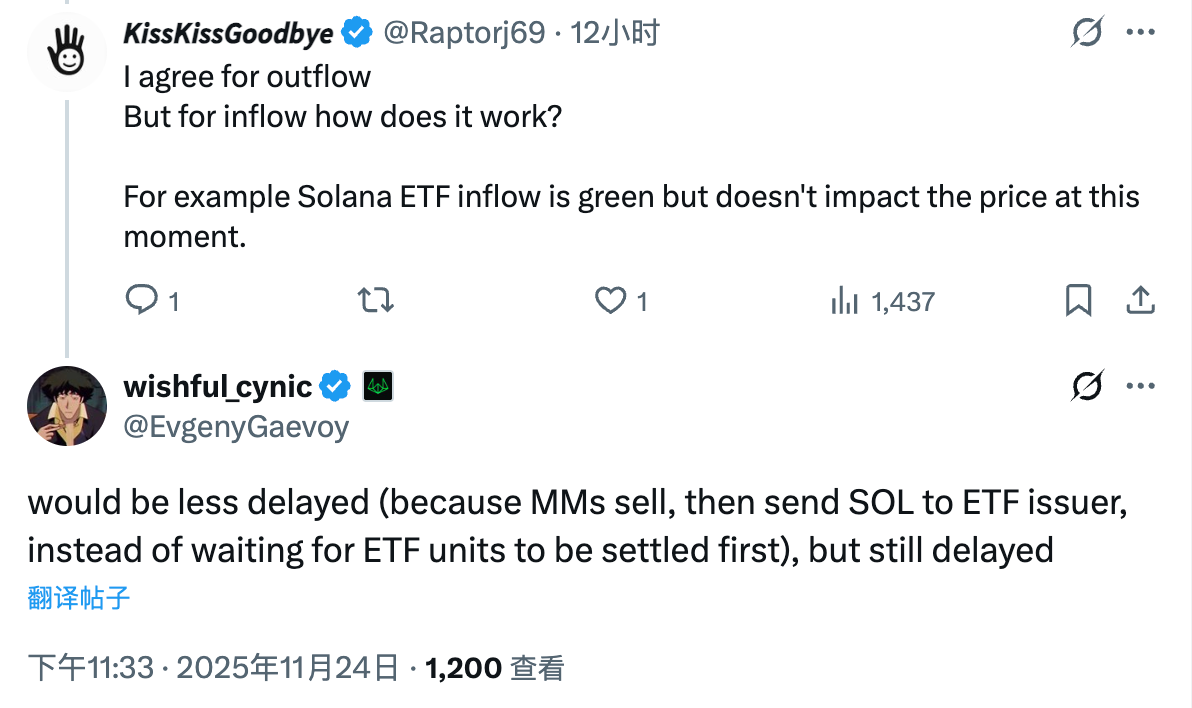

In the early hours of November 25, Evgeny Gaevoy, founder of market-making giant Wintermute, commented on this matter on X, stating: “This (BlackRock's large transfers) is actually a very lagging indicator. The sell-off has already occurred in the ETF. On-chain transfers by market makers often reflect the same situation.”

How should we interpret Evgeny's words? If the transfers are lagging, when did the actual sell-off occur?

First, it is important to clarify that the so-called large transfers from BlackRock refer to the transfers of cryptocurrency from the reserve addresses of BlackRock's spot Bitcoin ETF (IBIT) and spot Ethereum ETF (ETHA) to the Coinbase Prime custody address.

According to Evgeny's subsequent responses to questions from netizens, this actually occurs when there is a net outflow from the ETF, and large market makers are engaged in market-making and hedging around the ETF.

Specifically, market makers buy shares from ETF sellers, then submit redemption requests to BlackRock to exchange ETF shares for BTC (which usually has a 1-day delay). There is no selling pressure in the subsequent steps because market makers have already completed the hedging (selling) operation when purchasing the ETF.

In other words, the real selling pressure does not appear when retail investors see the on-chain transfers, but rather when market makers are accepting ETF sell orders (which is a buy for them) while simultaneously selling in the external market for hedging. Since the redemption process typically has a 1-day delay, the actual selling pressure may have occurred a day earlier.

Additionally, the above describes the market-making process during a net outflow from the ETF. Conversely, when there is a net inflow into the ETF, market makers will sell ETFs to buyers while buying cryptocurrencies (like SOL, which is currently experiencing a net inflow) and sending them to the ETF issuer. Since there is no redemption time limit in this case, the lag time will be shortened, but there will still be some delay.

In summary, the so-called “BlackRock large transfers” are actually just a settlement step in the standard operational process of the ETF, and the selling pressure they represent generally occurs before the transfer, not after. Relevant data will also be presented more clearly and comprehensively in the daily monitoring of ETF inflows and outflows, so there is no need to reinterpret it as an additional bearish signal, which could lead to unnecessary panic.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。