Author: esprit.hl

Compiled by: AididiaoJP, Foresight News

In recent weeks, there has been increasing concern within the industry regarding the future development of Hyperliquid. Market share loss, the rapid rise of competitors, and an increasingly crowded derivatives space have raised a core question: what is really happening beneath the surface? Has Hyperliquid already peaked, or is the current market interpretation overlooking deeper structural signals?

This article will analyze layer by layer.

Phase One: Comprehensive Leading Period (Early 2023 – Mid 2025)

During this period, Hyperliquid's key metrics reached new highs, and market share continued to grow, primarily due to the following structural advantages:

- Incentive system: Effectively attracted market liquidity.

- First-mover advantage in launching new contracts: For example, being the first to launch contracts like TRUMP and BERA, making it the platform with the most liquidity for new trading pairs and the preferred choice for pre-market trading (such as PUMP, WLFI, XPL). Traders had to use Hyperliquid to seize emerging trends, pushing its competitive advantage to the peak.

- User experience: Top-notch interface and user experience in perpetual contract DEX.

- Lower fees: More cost-effective compared to centralized exchanges.

- Launch of spot trading: Opened up new use cases.

- Ecosystem development tools: Including Builder Codes, HIP-2 proposals, and HyperEVM integration.

- Extremely high stability: Maintained zero service interruption even during significant market fluctuations.

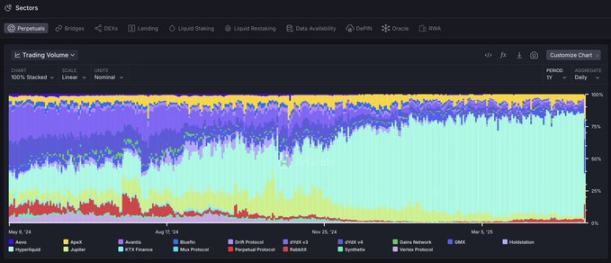

Based on these advantages, Hyperliquid's market share grew continuously for over a year, peaking at 80% in May 2025.

At that time, the Hyperliquid team was far ahead in innovation and execution, with no truly competitive products in the entire ecosystem.

Phase Two: Growth Stagnation Period: "Liquidity AWS" Strategy and Intensifying Competition

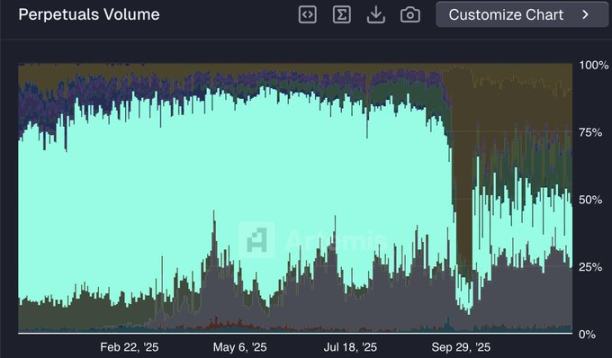

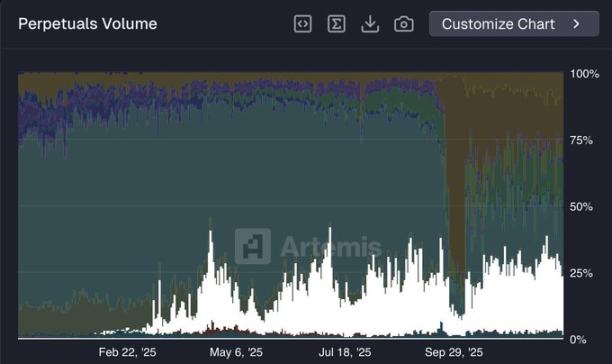

Since May 2025, Hyperliquid's market share has sharply declined, dropping from about 80% to nearly 20% by early December.

This relative loss of growth momentum can be attributed to the following points:

1. Strategic Shift from B2C to B2B

Hyperliquid did not continue to deepen its pure B2C model (such as launching its own mobile app or continuously introducing new perpetual contract products) but instead shifted to a B2B strategy, aiming to become the "AWS of liquidity."

The core of this strategy is to build infrastructure for external developers, such as Builder Codes for front-end use and HIP-3 for launching new perpetual contract markets. However, this shift means handing over some product deployment rights to third parties.

In the short term, this strategy is not optimal for attracting and retaining liquidity. The infrastructure is still in its early stages, market adoption takes time, and external developers currently lack the user reach and trust that Hyperliquid's core team has built over the long term.

2. Competitors Seizing Market Share

Unlike Hyperliquid's new strategy, competitors have maintained a fully vertically integrated model, allowing them to act much faster when launching new products.

By controlling the entire execution process, these platforms can expand quickly while retaining complete control over product releases. This gives them a significant competitive edge in the current phase compared to the first phase.

This directly translates into market share acquisition. Competitors now not only offer a full suite of products available on Hyperliquid but have also launched features that Hyperliquid has yet to introduce, such as the spot market, perpetual stocks, and forex trading that Lighter has already launched.

3. Lack of Incentives and Liquidity Migration

Hyperliquid has not launched any official incentive activities for over a year, while its main competitors have. For example, Lighter, which currently leads in trading volume market share (about 25%), is still in the "incentive season" before its token issuance.

In the DeFi world, liquidity essentially moves for profit. A significant portion of the trading volume flowing from Hyperliquid to Lighter (and other platforms) may be aimed at obtaining incentives and potential airdrops. Similar to most perpetual contract DEXs that operate incentive programs, Lighter's market share is expected to decline after its token issuance.

Phase Three: The Rise of HIP-3 and Builder Codes

As mentioned, building "AWS of liquidity" is not the optimal short-term strategy. However, in the long run, this strategic positioning gives Hyperliquid the potential to become a core hub of global finance.

Although competitors have replicated most of Hyperliquid's current functionalities, the true source of innovation still lies within Hyperliquid.

Ecosystem builders developing on Hyperliquid can focus on specific areas and formulate more targeted product development strategies on the continuously evolving infrastructure.

In contrast, protocols that maintain complete vertical integration (like Lighter) will face more limitations when optimizing multiple product lines simultaneously.

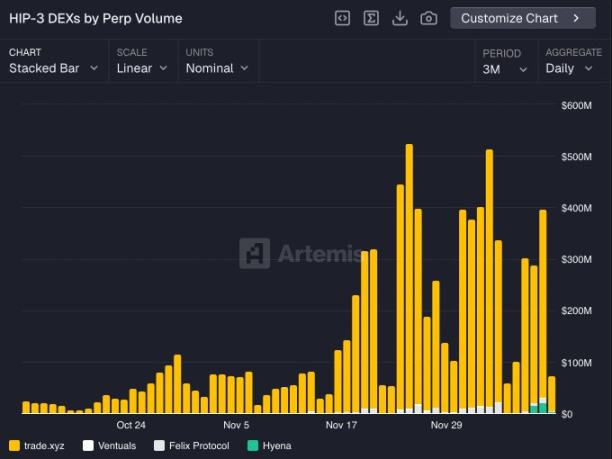

HIP-3 is still in its early stages, but its long-term impact is beginning to show. Major participants like @tradexyz have launched perpetual stocks, and @hyenatrade has recently deployed a terminal for trading USDe. More experimental markets are emerging, such as @ventuals, which provides asset exposure before IPOs, and @trovemarkets, focusing on niche speculative markets like Pokémon or CS:GO assets.

It is expected that by 2026, the trading volume of the HIP-3 market will occupy a significant share of Hyperliquid's total trading volume.

The key to Hyperliquid regaining its dominant position lies in the synergy between HIP-3 and Builder Codes.

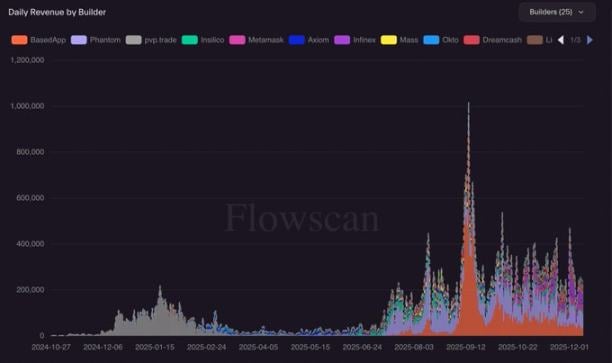

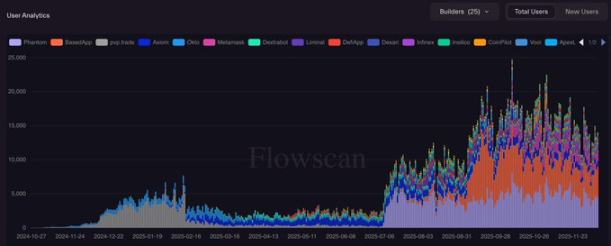

Any front-end integrated with Hyperliquid can immediately access all HIP-3 markets, providing unique products for its users. Therefore, builders have strong motivation to create new markets through HIP-3, as these markets can easily connect to any compatible front-end (like Phantom, MetaMask, etc.), reaching new sources of liquidity—this is a perfect growth flywheel.

The ongoing development of Builder Codes makes me increasingly optimistic about its potential for revenue generation and user growth.

Currently, the main users of Builder Codes are still crypto-native applications like Phantom, MetaMask, and BasedApp. However, I anticipate the emergence of a new type of "super application" built on Hyperliquid, aimed at attracting entirely new user groups that are not crypto-native.

This is likely the path for Hyperliquid to enter the next phase of scale expansion.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。