The answer may need to be found in Tokyo.

Written by: David, Deep Tide TechFlow

On December 15, Bitcoin fell from $90,000 to $85,616, a drop of over 5% in a single day.

There were no major explosions or negative events that day, and on-chain data did not show any unusual selling pressure. If you only look at news from the crypto space, it’s hard to find a "reasonable" explanation.

However, on the same day, gold was quoted at $4,323 per ounce, down just $1 from the previous day.

One dropped 5%, while the other barely moved.

If Bitcoin is truly "digital gold," a tool for hedging against inflation and currency devaluation, then its performance in the face of risk events should resemble gold more closely. But this time, its movement clearly resembled that of high Beta tech stocks in the Nasdaq.

What is driving this round of decline? The answer may need to be found in Tokyo.

The Butterfly Effect from Tokyo

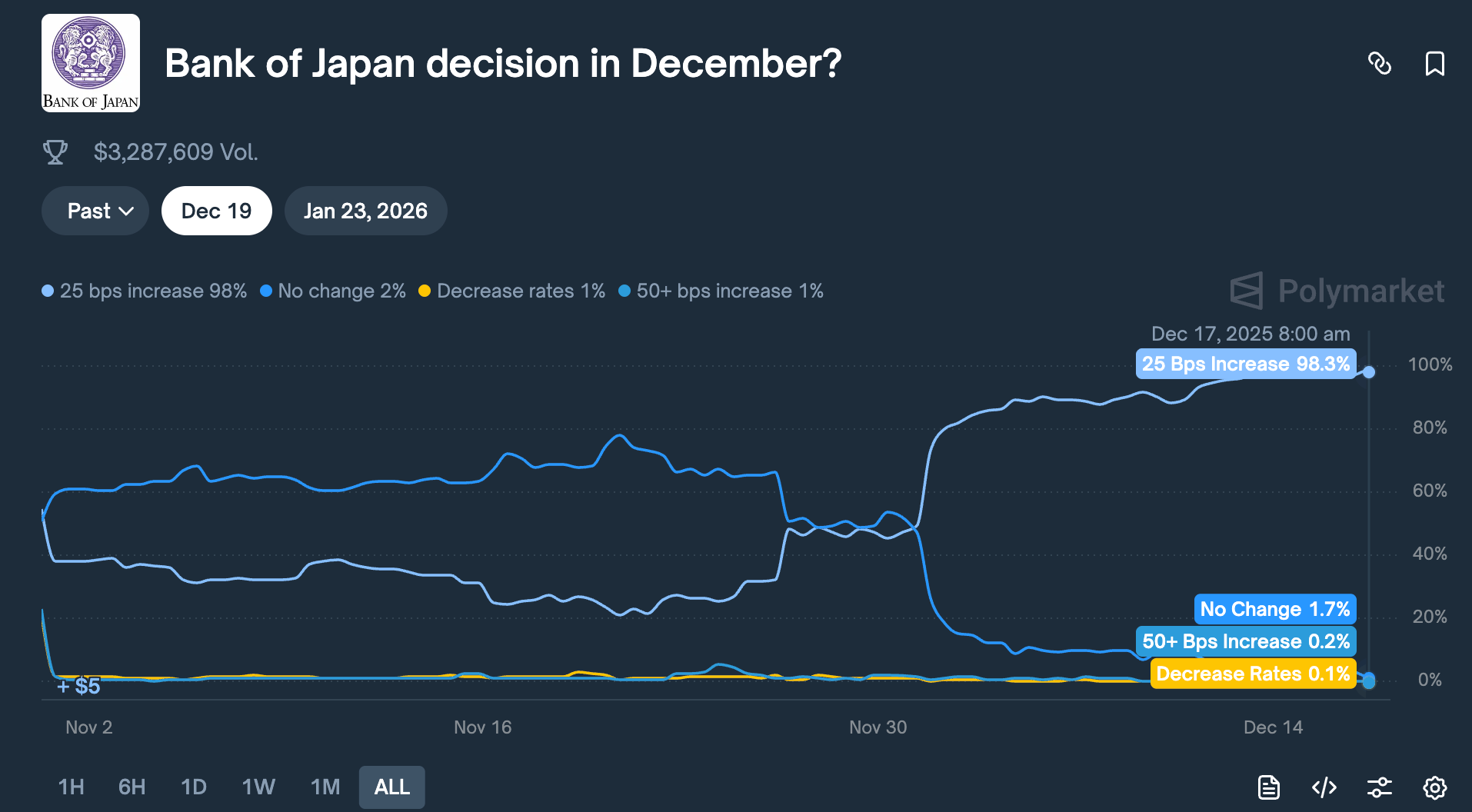

On December 19, the Bank of Japan will hold a monetary policy meeting. The market expects it to raise interest rates by 25 basis points, increasing the policy rate from 0.5% to 0.75%.

0.75% doesn’t sound high, but it is the highest interest rate in Japan in nearly 30 years. In prediction markets like Polymarket, traders are pricing the probability of this rate hike at 98%.

Why would a decision from a central bank far away in Tokyo cause Bitcoin to drop 5% within 48 hours?

This can be explained by something called "Yen carry trade."

The logic is quite simple:

**Japanese interest rates have long been close to zero or even negative, making borrowing *Yen* almost free.** As a result, global hedge funds, asset management institutions, and trading desks have borrowed large amounts of Yen, converted it into dollars, and then invested in higher-yielding assets, including U.S. Treasuries, U.S. stocks, and cryptocurrencies.

As long as the returns on these assets exceed the cost of borrowing Yen, the interest rate differential becomes profit.

This strategy has existed for decades, with a scale so large that it is difficult to estimate accurately. Conservative estimates suggest several hundred billion dollars, and some analysts believe it could be as high as several trillion when including derivatives exposure.

At the same time, Japan has a special status:

**It is the largest foreign holder of U.S. Treasuries, holding $1.18 trillion in **U.S. debt.

This means that changes in the flow of funds from Japan will directly impact the world’s most important bond market, which in turn affects the pricing of all risk assets.

Now, when the Bank of Japan decides to raise interest rates, the underlying logic of this game is shaken.

First, the cost of borrowing Yen rises, narrowing the arbitrage space; more troubling is that the expectation of a rate hike will push the Yen to appreciate, while these institutions initially borrowed Yen and converted it to dollars for investment;

Now, to repay the loans, they must sell dollar assets to convert back to Yen. The stronger the Yen rises, the more assets they need to sell.

This "forced selling" does not choose its timing or the type of asset. The most liquid and easily convertible assets are sold first.

Therefore, it’s easy to see that Bitcoin, which trades 24/7 without price limits and has relatively shallow market depth compared to stocks, is often the first to be hit.

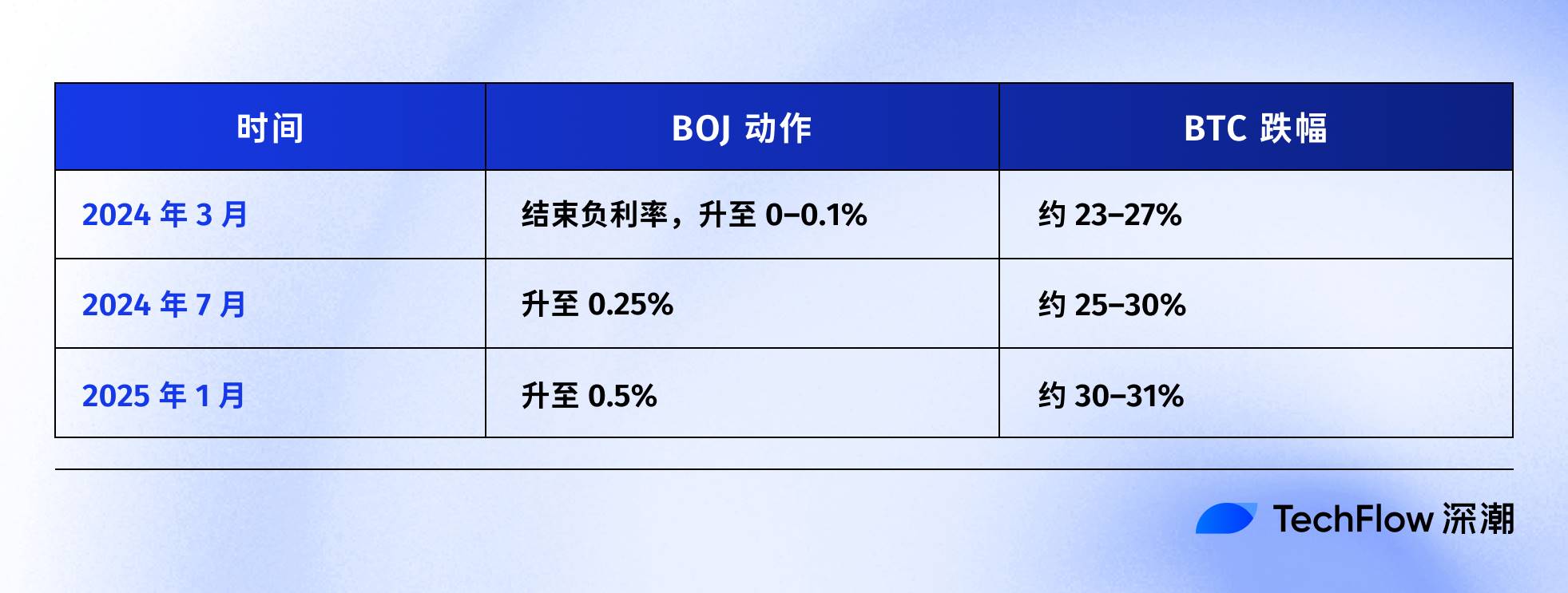

Looking back at the timeline of the Bank of Japan's interest rate hikes over the past few years, this speculation is also supported by data:

The most recent instance was on July 31, 2024. After the BOJ announced a rate hike to 0.25%, the Yen appreciated from 160 to below 140 against the dollar, and BTC fell from $65,000 to $50,000 within the following week, a drop of about 23%, with the entire crypto market evaporating $60 billion in market value.

According to statistics from several on-chain analysts, after the last three interest rate hikes by the Bank of Japan, BTC experienced a pullback of over 20% each time.

The specific starting and ending points and time windows of these numbers vary, but the direction is highly consistent:

Each time Japan tightens monetary policy, BTC is a disaster zone.

Therefore, the author believes that what happened on December 15 was essentially the market "front-running." Before the decision on the 19th was announced, funds had already begun to withdraw in advance.

On that day, there was a net outflow of $357 million from U.S. BTC ETFs, the largest single-day outflow in nearly two weeks; over $600 million in leveraged long positions in the crypto market were liquidated within 24 hours.

These were likely not retail investors panicking, but rather a chain reaction from arbitrage trading closing positions.

Is Bitcoin still digital gold?

The above explains the mechanism of Yen carry trading, but there is still one question unanswered:

Why is BTC always the first to be hurt and sold?

A common explanation is that BTC "has good liquidity and trades 24/7," which is true, but not sufficient.

The real reason is that BTC has been repriced over the past two years: it is no longer an "alternative asset" independent of traditional finance, **but has been welded into Wall Street's **risk exposure.

In January last year, the U.S. SEC approved the first spot Bitcoin ETF. This was a milestone that the crypto industry had waited a decade for, allowing trillion-dollar asset management giants like BlackRock and Fidelity to compliantly include BTC in their clients' portfolios.

Funds did indeed flow in. But with that came a change in identity: the holders of BTC changed.

Previously, BTC was purchased by crypto-native players, retail investors, and some aggressive family offices.

Now, BTC is bought by pension funds, hedge funds, and asset allocation models. These institutions hold U.S. stocks, U.S. Treasuries, and gold simultaneously, managing "risk budgets."

When the overall portfolio needs to reduce risk, they won’t just sell BTC or just sell stocks, but will proportionally reduce all positions.

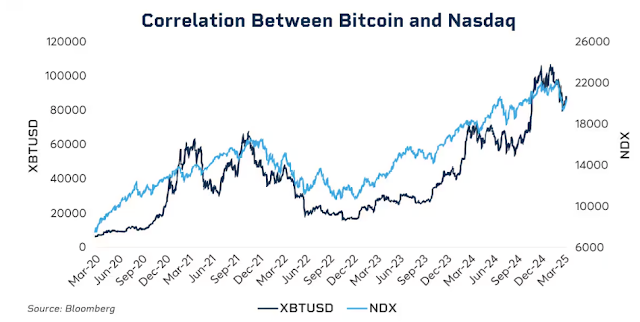

Data shows this binding relationship.

In early 2025, the 30-day rolling correlation between BTC and the Nasdaq 100 index reached 0.80, the highest level since 2022. In contrast, before 2020, this correlation hovered around -0.2 to 0.2, essentially considered uncorrelated.

More importantly, this correlation significantly increases during periods of market stress.

In March 2020, during the pandemic crash, in 2022 during the Fed's aggressive rate hikes, and in early 2025 amid tariff concerns… each time risk aversion rises, the linkage between BTC and U.S. stocks becomes tighter.

Institutions in panic do not distinguish between "this is a crypto asset" or "this is a tech stock"; they only look at one label: risk exposure.

This raises an awkward question: does the narrative of digital gold still hold?

If we look at the longer term, from 2025 to now, gold has risen over 60%, marking its best performance since 1979; during the same period, BTC has pulled back over 30% from its peak.

Both are referred to as assets that hedge against inflation and combat currency devaluation, yet they have moved along completely opposite curves in the same macro environment.

This does not mean that BTC's long-term value is in question; its five-year compound annual growth rate still far exceeds that of the S&P 500 and Nasdaq.

But at this stage, its short-term pricing logic has changed: it is a high-volatility, high Beta risk asset, rather than a safe-haven tool.

Understanding this is key to grasping why a 25 basis point rate hike from the Bank of Japan can cause BTC to drop several thousand dollars within 48 hours.

It’s not because Japanese investors are selling BTC, but because when global liquidity tightens, institutions will reduce all risk exposures according to the same logic, and BTC happens to be the most volatile and easily liquidated link in that chain.

What will happen on December 19?

As I write this article, there are two days left until the Bank of Japan's monetary policy meeting.

The market has already treated the rate hike as a foregone conclusion. The yield on Japan's 10-year government bonds has risen to 1.95%, the highest in 18 years. In other words, the bond market has already priced in the tightening expectations.

If the rate hike has been fully anticipated, will there still be an impact on the 19th?

Historical experience suggests: yes, but the intensity depends on the wording.

The impact of a central bank's decision is never just about the numbers themselves, but the signals they send. If BOJ Governor Kazuo Ueda says at the press conference, "We will assess cautiously based on data in the future," the market may breathe a sigh of relief;

If he says, "Inflation pressures persist, and further tightening cannot be ruled out," that could mark the beginning of another wave of selling.

Currently, Japan's inflation rate is around 3%, above the BOJ's target of 2%. The market is not worried about this rate hike, but whether Japan is entering a sustained tightening cycle.

If the answer is yes, the unwinding of the Yen carry trade will not be a one-time event, but a process that lasts for several months.

However, some analysts believe this time may be different.

First, speculative funds' positions on the Yen have shifted from net short to net long. The sharp drop in July 2024 was partly due to the market being caught off guard, as many funds were still shorting the Yen at that time. Now, the position direction has reversed, limiting the space for unexpected appreciation.

Second, Japanese government bond yields have risen for over half a year, from 1.1% at the beginning of the year to nearly 2% now. In a sense, the market has "already raised rates," and the Bank of Japan is merely acknowledging the established fact.

Third, the Federal Reserve just cut rates by 25 basis points, and the overall direction of global liquidity is easing. Japan is tightening in reverse, but if dollar liquidity is sufficiently abundant, it may partially offset the pressure on the Yen side.

These factors do not guarantee that BTC won’t drop, but they may suggest that this decline won’t be as extreme as in previous instances.

Looking at past trends after several BOJ rate hikes, BTC usually bottoms out within one to two weeks after the decision, then enters a consolidation or rebound phase. If this pattern holds, late December to early January may be the most volatile window, but it could also be an opportunity after being oversold.

Accepted and Influenced

Putting the above together, the logical chain is quite clear:

Bank of Japan rate hike → Yen carry trade unwinding → Global liquidity tightening → Institutions reducing positions according to risk budgets → BTC, as a high Beta asset, being sold first.

In this chain, BTC has done nothing wrong.

It has simply been placed in a position it cannot control, at the end of the global macro liquidity transmission chain.

You may find it hard to accept, but this is the new normal of the ETF era.

Before 2024, BTC's price movements were mainly driven by crypto-native factors: halving cycles, on-chain data, exchange dynamics, regulatory news. At that time, its correlation with U.S. stocks and bonds was very low, and to some extent, it did resemble an "independent asset class."

After 2024, Wall Street arrived.

BTC has been integrated into the same risk management framework as stocks and bonds. Its holder structure has changed, and its pricing logic has followed suit.

BTC's market capitalization surged from several hundred billion to $1.7 trillion. But this also brought a side effect: BTC's immunity to macro events has disappeared.

A single statement from the Federal Reserve or a decision from the Bank of Japan can cause it to fluctuate by over 5% within hours.

If you believe in the narrative of "digital gold," trusting it to provide shelter in chaotic times, then the performance in 2025 may be somewhat disappointing. At least at this stage, the market does not price it as a safe-haven asset.

Perhaps this is just a temporary misalignment. Perhaps institutionalization is still in its early stages, and once the allocation ratios stabilize, BTC will find its rhythm again. Perhaps the next halving cycle will once again prove the dominance of crypto-native factors…

But until then, if you hold BTC, you need to accept one reality:

You are also holding exposure to global liquidity. What happens in a conference room in Tokyo may determine your account balance next week more than any on-chain indicator.

This is the cost of institutionalization. As for whether it is worth it, everyone has their own answer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。