Original Title: Hyperliquid at the Crossroads: Robinhood or Nasdaq Economics

Original Author: @shaundadevens

Translation: Peggy, BlockBeats

Editor's Note: As Hyperliquid's trading volume approaches that of traditional exchanges, what truly deserves attention is not just "how large the volume is," but rather which level of market structure it chooses to stand on. This article uses the division of "broker vs exchange" in traditional finance as a reference to analyze why Hyperliquid actively adopts a low-fee market layer positioning, and how Builder Codes and HIP-3 create long-term pressure on platform fees while expanding the ecosystem.

Hyperliquid's path reflects the core issue facing the entire crypto trading infrastructure: after scaling up, how should profits be distributed?

The following is the original text:

Hyperliquid is handling perpetual contract trading volumes close to Nasdaq levels, but its profit structure also exhibits "Nasdaq-level" characteristics.

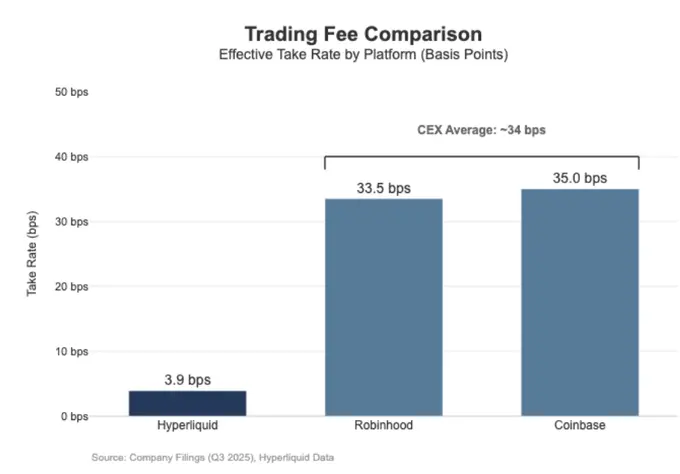

In the past 30 days, Hyperliquid has cleared $205.6 billion in nominal perpetual contract trading volume (annualized at approximately $617 billion), but has only generated $8.03 million in fee revenue, translating to a fee rate of about 3.9 basis points (bps).

This means that Hyperliquid's monetization method is closer to a wholesale execution venue rather than a high-fee trading platform aimed at retail investors.

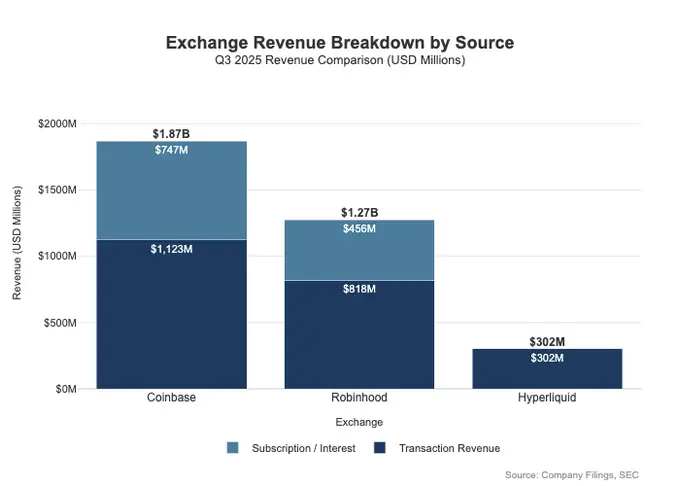

In comparison, Coinbase recorded $295 billion in trading volume in Q3 2025, achieving $1.046 billion in trading revenue, with an implied fee rate of about 35.5 basis points.

Robinhood's monetization logic in its crypto business is similar: its $80 billion in nominal crypto asset trading volume generated $268 million in trading revenue, with an implied fee rate of about 33.5 basis points; meanwhile, Robinhood's nominal stock trading volume in Q3 2025 reached as high as $647 billion.

Overall, Hyperliquid has already entered the ranks of top trading infrastructures in terms of trading volume, but in terms of fees and business model, it resembles a low-fee execution layer aimed at professional traders rather than a retail-oriented platform.

The gap is not only reflected in the fee level but also in the breadth of monetization dimensions. Retail platforms often profit simultaneously across multiple revenue "interfaces." In Q3 2025, Robinhood achieved a total of $730 million in trading-related revenue, along with $456 million in net interest income and $88 million in other income (mainly from Gold subscription services).

In contrast, Hyperliquid currently relies much more heavily on trading fees, which are structurally compressed to single-digit basis points at the protocol level. This means that Hyperliquid's revenue model is more concentrated, more singular, and closer to a low-fee, high-turnover infrastructure role, rather than a retail platform that deeply monetizes through multiple product lines.

This can essentially be explained by positioning differences: Coinbase and Robinhood are broker/dealer-type businesses that rely on balance sheets and subscription systems for multi-layer monetization; whereas Hyperliquid is closer to the exchange layer. In traditional financial market structures, profit pools are naturally split between these two layers.

Broker-Dealer vs Exchange Model

In traditional finance (TradFi), the core distinction is between the distribution layer and the market layer.

Retail platforms like Robinhood and Coinbase are located in the distribution layer, capturing high-margin monetization opportunities; while exchanges like Nasdaq are situated in the market layer, where their pricing power is structurally limited, and execution services are pressured by competition towards a commoditized economic model.

Broker/Dealer = Distribution Capability + Client Balance Sheet

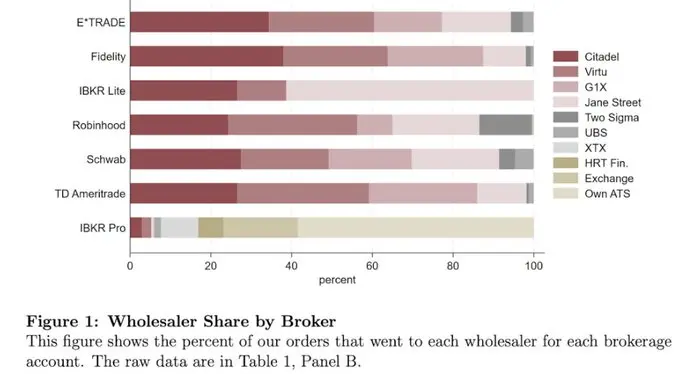

Brokers hold customer relationships. Most users do not directly access Nasdaq but enter the market through brokers. Brokers are responsible for account opening, custody, margin and risk management, customer support, tax documentation, etc., and then route orders to specific trading venues.

It is this "relationship ownership" that allows brokers to monetize in multiple ways beyond trading:

- Funds and asset balances: cash aggregation spreads, margin lending, securities lending

- Product packaging: subscription services, feature bundles, debit card/investment advisory products

- Routing economics: brokers control order flow and can embed payment or revenue-sharing mechanisms in the routing chain

This is why brokers often earn more than trading venues: the profit pool is truly concentrated where "distribution + balances" are located.

Exchange = Matching + Rules + Infrastructure, Limited Fees

Exchanges operate the trading venues themselves: matching engines, market rules, deterministic execution, and infrastructure connectivity. Their main monetization methods include:

- Trading fees (which are continuously driven down in high liquidity products)

- Rebates/liquidity incentives (often returning most of the nominal fee rate to market makers to compete for liquidity)

- Market data, network connectivity, and co-location services

- Listing fees and index licensing

Robinhood's order routing mechanism clearly illustrates this structure: customer relationships are held by the broker (Robinhood Securities), and orders are routed to third-party market centers, with economic benefits distributed along the routing chain.

The true high-margin layer is at the distribution end, controlling customer acquisition, user relationships, and all monetization aspects surrounding execution (such as order flow payments, margin, securities lending, and subscription services).

Nasdaq itself operates at the low-margin layer. The products it offers are essentially highly commoditized execution capabilities and queue access rights, and its pricing power is strictly limited by mechanisms.

The reason is that to compete for liquidity, trading venues often need to return nominal fees in the form of maker rebates; regulatory bodies impose caps on access fees, limiting the fee space; and order routing is highly elastic, allowing funds and orders to quickly switch between different trading venues, making it difficult for any single venue to raise prices.

This is clearly reflected in Nasdaq's disclosed financial data: the net revenue it actually captures in cash equity trading is usually only a few cents per share. This is a direct reflection of the structural compression of profit space for market layer exchanges.

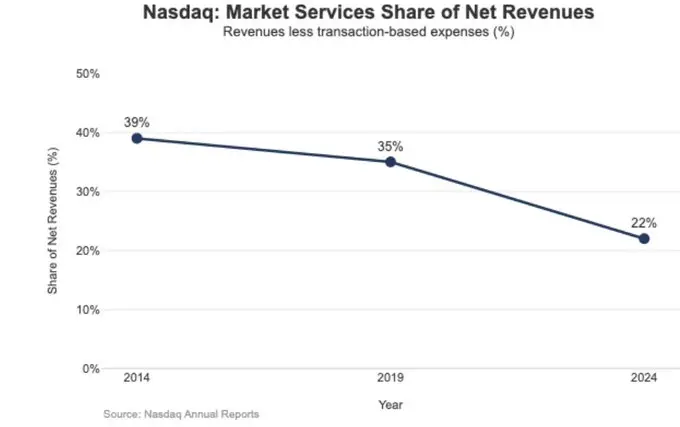

The strategic consequences of this low-margin environment are also clearly reflected in the changes in Nasdaq's revenue structure.

In 2024, Nasdaq's Market Services revenue was $1.02 billion, accounting for 22% of total revenue of $4.649 billion; this proportion was as high as 39.4% in 2014 and still 35% in 2019.

This ongoing downward trend is highly consistent with Nasdaq's proactive shift from a highly volatile, profit-constrained execution business to a more recurring, predictable software and data business. In other words, it is the structurally low profit space at the exchange level that drives Nasdaq to gradually shift its growth focus from "matching and execution" to "technology, data, and service-oriented products."

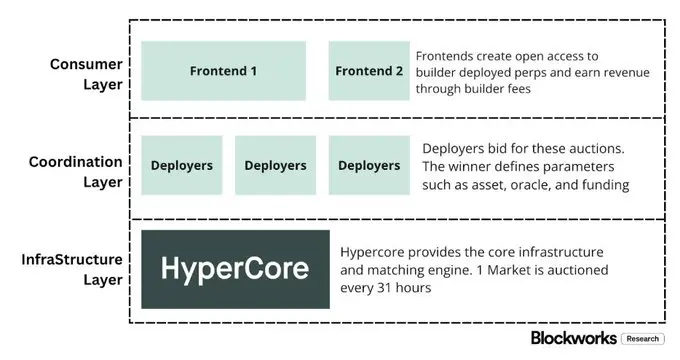

Hyperliquid as the "Market Layer"

Hyperliquid's effective fee rate of about 4 basis points (bps) is highly consistent with its intentionally chosen market layer positioning. It is building a "Nasdaq-style" trading infrastructure on-chain:

With HyperCore at its core, it features high-throughput matching, margin, and clearing systems, employing maker/taker pricing and maker rebate mechanisms, aiming to maximize execution quality and share liquidity, rather than multi-layer monetization aimed at retail users.

In other words, Hyperliquid's design focus is not on subscriptions, balances, or distribution-type revenue, but on providing commoditized yet extremely efficient execution and settlement capabilities—this is a typical characteristic of the market layer and a necessary result of its low-fee structure.

This is reflected in two structural splits that most crypto trading platforms have yet to fully implement but are very typical in traditional finance (TradFi):

First, the permissionless broker/distribution layer (Builder Codes).

Builder Codes allow third-party trading interfaces to be built on top of the core trading venue and to collect economic benefits independently. Here, builder fees have a clear upper limit: a maximum of 0.1% (10 basis points) for perpetual contracts and 1% for spot trading, with fees settable at the individual order level.

This mechanism thus creates a competitive market for the distribution layer, rather than allowing a single official application to monopolize user entry and monetization rights.

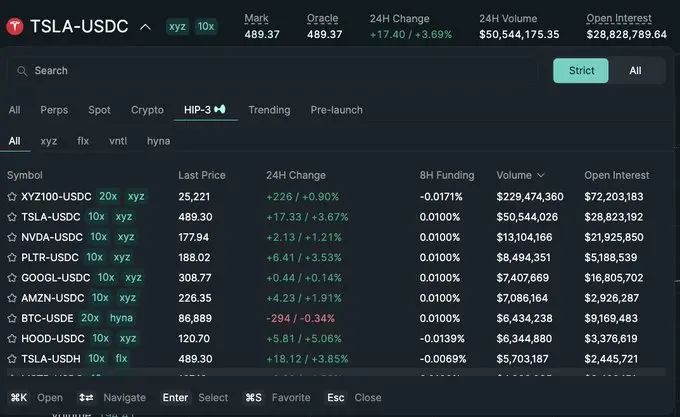

Second, the permissionless listing/product layer (HIP-3).

In traditional finance, exchanges typically control listing approvals and product creation. HIP-3 externalizes this function: developers can deploy perpetual contracts inheriting HyperCore's matching engine and API capabilities, while the specific market definition and operation are the responsibility of the deployer.

Economically, HIP-3 clarifies the revenue-sharing relationship between trading venues and product layers: deployers of spot and HIP-3 perpetual contracts can retain up to 50% of the trading fees for the assets they deploy.

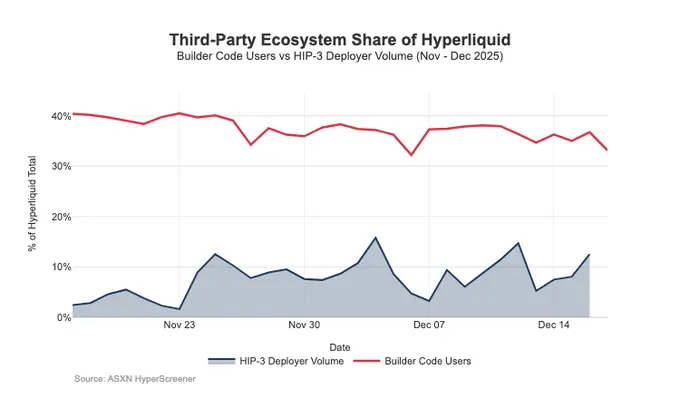

Builder Codes have already shown effectiveness on the distribution side: as of mid-December, about one-third of users are trading not through the native interface but through third-party front ends.

The issue is that this structure, which favors distribution expansion, will also create ongoing pressure on the trading venue layer's fees:

- Pricing is compressed.

Multiple front ends selling the same underlying liquidity will naturally converge competition towards the lowest overall trading costs; and Builder fees can be flexibly adjusted at the order level, further pushing prices towards the lower limit.

- Loss of monetization dimensions.

Front ends control account opening, product packaging, subscription services, and complete trading workflows, thus capturing the high-margin space of the broker layer; while Hyperliquid can only retain a thinner exchange layer fee.

- Strategic routing risk.

Once the front end evolves into a true cross-venue router, Hyperliquid may be forced into competition for wholesale execution, having to defend order flow by lowering fees or increasing rebates.

Overall, Hyperliquid is consciously choosing a low-margin market layer positioning (through HIP-3 and Builder Codes), while allowing a high-margin broker layer to grow above it.

If Builder front ends continue to expand, they will increasingly determine the user-facing pricing structure, control user retention and monetization interfaces, and gain bargaining power at the routing level, creating long-term pressure on Hyperliquid's fee rate structurally.

Defending Distribution Rights and Introducing Non-Exchange Profit Pools

The most direct risk is commoditization.

If third-party front ends can consistently undercut the native interface with lower prices, or even achieve cross-venue routing, Hyperliquid will be pushed towards a wholesale execution economic model.

Recent design adjustments indicate that Hyperliquid is attempting to expand new revenue sources while avoiding this outcome.

Distribution Defense: Maintaining Economic Competitiveness of the Native Front End

A previously proposed staking discount program allowed Builders to receive up to a 40% fee discount by staking HYPE, effectively providing a structurally cheaper path for third-party front ends compared to Hyperliquid's native interface. The withdrawal of this program equates to canceling direct subsidies for external distribution "price cuts."

At the same time, the HIP-3 market was initially positioned to be primarily distributed through Builders and not displayed on the main front end; however, these markets have now begun to be showcased on Hyperliquid's native front end, adhering to strict listing standards.

This signal is very clear: Hyperliquid still maintains permissionless access at the Builder layer, but will not sacrifice its core distribution rights.

USDH: Shifting from Trading Monetization to "Float" Monetization

The launch of USDH aims to reclaim the stablecoin reserve income that would otherwise be captured outside the system. Its public structure features a 50/50 split of reserve income: 50% goes to Hyperliquid, and 50% is used for USDH ecosystem growth. Additionally, the trading fee discounts offered for USDH-related markets further reinforce this orientation: Hyperliquid is willing to concede on the economics of individual transactions in exchange for a larger, stickier profit pool tied to balances.

In effect, this introduces a revenue source similar to an annuity for the protocol, with growth depending on the scale of the monetary base, rather than just nominal trading volume.

Portfolio Margin: Introducing Financing Economics Similar to Prime Brokers

Portfolio margin unifies the margin for spot and perpetual contracts, allowing different exposures to offset each other and introducing a native borrowing cycle.

Hyperliquid will retain 10% of the interest paid by borrowers, making the protocol's economics increasingly dependent on leverage usage and interest rate levels, rather than just trading volume. This is closer to the revenue model of brokers/prime brokers rather than pure exchange logic.

Hyperliquid's Path Towards a "Broker-like" Economic Model

In terms of throughput, Hyperliquid has reached the scale of a top-tier trading venue; however, in monetization, it still resembles a market layer: extremely high nominal trading volume, coupled with a single-digit basis point effective fee rate. The gap with Coinbase and Robinhood is structural.

Retail platforms are located at the broker layer, controlling user relationships and fund balances, allowing them to monetize multiple profit pools simultaneously (financing, idle cash, subscriptions); while pure trading venues sell execution services, which, under liquidity and routing competition, naturally trend towards commoditization, with net capture continuously compressed. Nasdaq serves as a reference for this constraint in TradFi.

Hyperliquid initially leaned towards the prototype of a trading venue. By splitting the distribution layer (Builder Codes) and product creation layer (HIP-3), it accelerated ecosystem expansion and market coverage; the cost is that this structure may also push economics outward: once third-party front ends determine comprehensive pricing and can cross-venue route, Hyperliquid risks being compressed into a low-margin wholesale execution track.

However, recent actions indicate a conscious shift: while not abandoning unified execution and clearing advantages, it defends distribution rights and expands revenue sources into "balance-driven" profit pools.

Specifically: the protocol is no longer willing to subsidize external front ends that are structurally cheaper than the native UI; HIP-3 is more natively displayed; and it introduces balance sheet-style revenue sources.

USDH brings reserve income back into the ecosystem (50/50 split, with rate discounts for USDH markets); portfolio margin introduces financing economics through a 10% cut of borrowing interest.

Overall, Hyperliquid is converging towards a hybrid model: using execution tracks as a base, layering on distribution defense and balance-driven profit pools. This reduces the risk of being trapped in low-basis-point, wholesale trading venues while aligning with a broker-like revenue structure without sacrificing unified execution and clearing advantages.

Looking ahead to 2026, the unresolved question is: can Hyperliquid further move towards a broker-like economy without undermining its "outsourcing-friendly" model? USDH is the clearest litmus test: at around $100 million in supply, when the protocol does not control distribution, the expansion of outsourced issuance appears slow. An obvious alternative path could have been at the UI level—such as automatically converting around $4 billion of USDC reserves into a native stablecoin (similar to Binance's automatic conversion to BUSD).

If Hyperliquid wants to truly capture the broker layer profit pool, it may also need broker-like behavior: stronger control, tighter integration of native products, and clearer boundaries with ecosystem teams in distribution and balance competition.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。