Volatility has been repriced, and the market is pricing in the tail risk of a significant price increase.

Author: Campbell

Translation: Deep Tide TechFlow

It has been 10 days since we last published our analysis on silver.

The market dynamics from 10 days ago seem like a quarter of the past. In this short time, the silver market has experienced a series of significant events:

China announced a licensing system for silver exports starting January 1 next year.

The physical silver price in Shanghai soared to $91, while the COMEX (New York Mercantile Exchange) settlement price was $77.

The London forward curve remains deeply entrenched in backwardation, although not as extreme as in October, it still maintains an inverted structure.

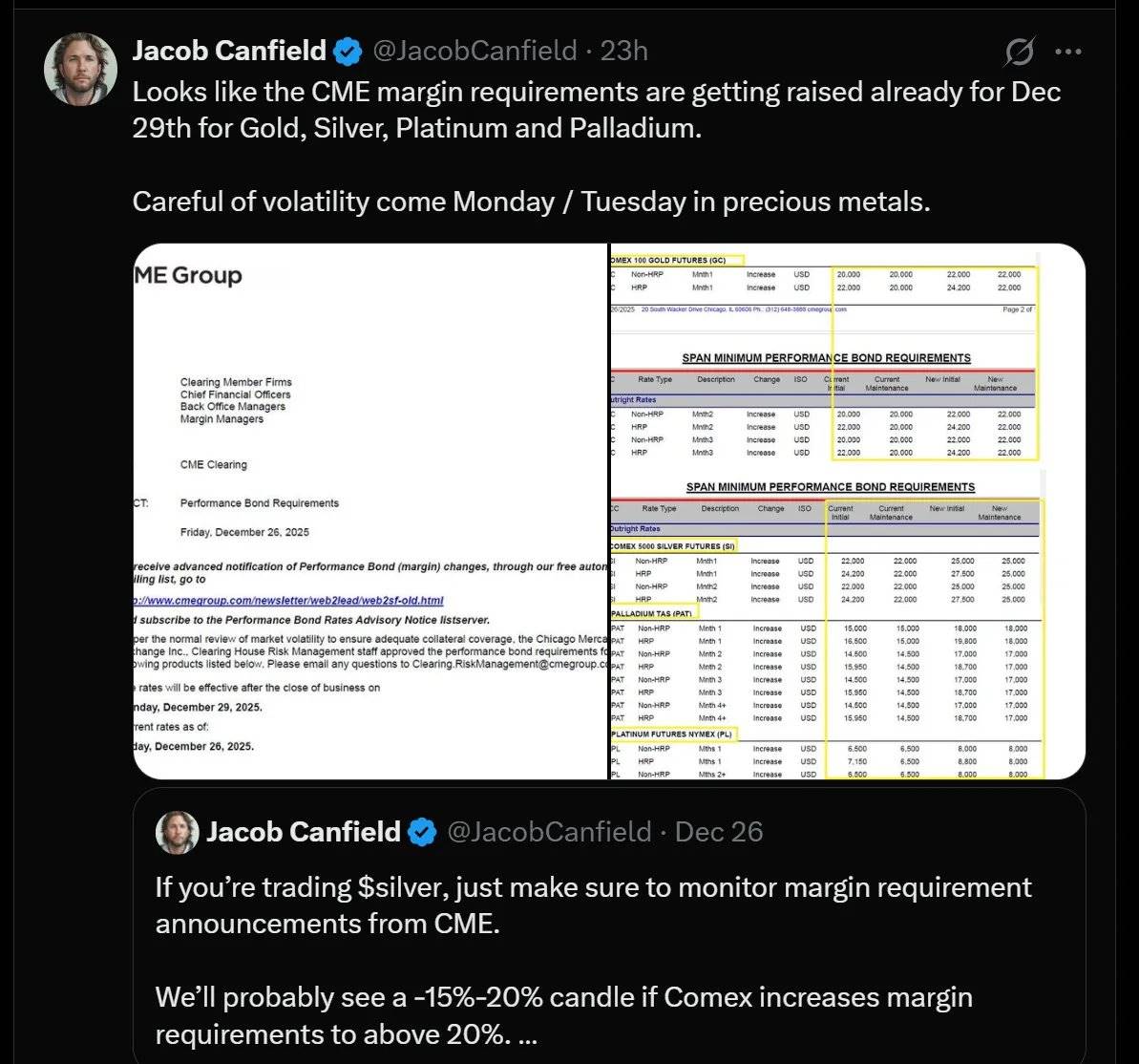

The CME (Chicago Mercantile Exchange) raised the margin requirements for silver.

After undergoing a much-needed digital detox, I spent the entire afternoon staring at Bloomberg and Rose, trying to figure out whether these changes would affect our market outlook.

Short-term conclusion: Now is not a good time for new purchases.

I will wait for the upcoming pullback opportunity to continue positioning and remain flexible when operating through options.

This is precisely the part that trading books won’t tell you—when your investment logic works, or even works too smoothly, you need not only to manage your funds but also to manage your emotional resilience. At this point, the mathematical models you’ve derived on paper are no longer just a probability distribution; they have turned into a call option on "realized gains."

This phase is unsettling because you need to do more homework: recheck your calculations and assess potential adverse narratives against you.

This is the current situation.

Bear Market Warnings (or: Potentially "Deadly" Risk Factors)

In the next two weeks, silver bulls will have to contend with narratives and pressures that could trigger bearish sentiment in the short term.

Do not be surprised by the upcoming "bearish candles"; they are likely to occur. The key is whether you will choose to buy at the lows. We have shifted some of our "Delta" (i.e., price exposure) to gold, rebalancing our trading portfolio to currently hold about 15% gold positions and 30%-40% silver positions, whereas this ratio was previously closer to 10:1.

Additionally, we have purchased some upside butterfly options and significantly bought call options on the dollar. The logic behind these operations will gradually become clearer in subsequent discussions.

In any case, here are the main factors currently likely to bring bearish pressure:

- ### Tax Selling Pressure

The trade you currently hold has made a considerable profit, possibly to the extent that it makes your accountant uneasy. For those who bought silver through exercising long call options, they may be reluctant to sell their positions before December 31.

Especially when these positions have been held for less than a year, as this not only involves capital gains tax but may also face differences in short-term and long-term tax treatment.

This means there will be bullish pressure currently, but after January 2, it will turn into bearish pressure.

- ### Dollar and Interest Rate Issues

The latest GDP data has performed strongly, which may weaken the easing expectations for the 2-year Treasury yield curve, forcing policymakers to choose between a stronger dollar and higher short-term interest rates. Either choice is not good news for dollar-denominated precious metals (like silver and gold) in the short term.

- ### Margin Increases

The CME (Chicago Mercantile Exchange) announced an increase in margin requirements for precious metals starting December 29.

If you are using leverage in the futures market, this change could have a significant impact on you. Higher margin requirements = higher capital demands = forced liquidation for undercapitalized investors. This is similar to the situation during the 2011 silver market crash when the CME raised margin requirements five times in eight days, leading to a collapse in leverage and abruptly halting the silver rally.

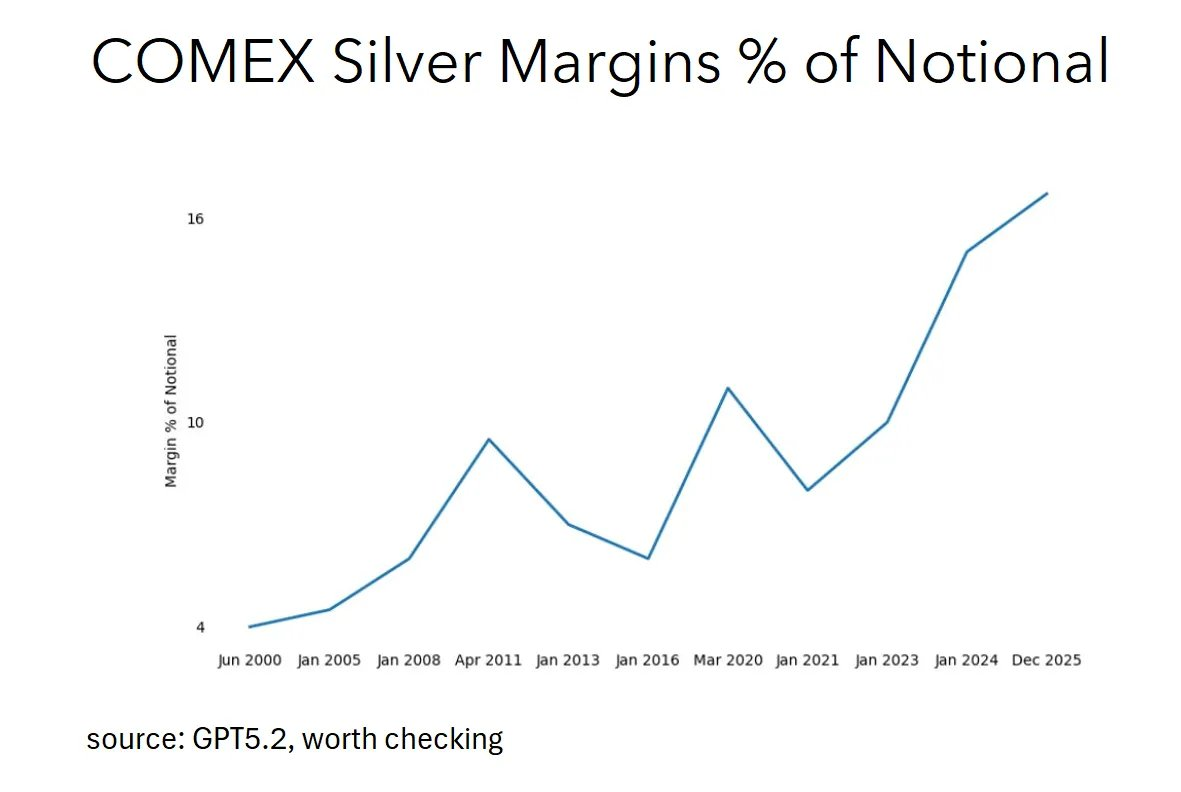

So, is there reason to worry this time? Actually, the situation is not that dire. The reason is that silver's margin requirements have long been above the levels seen in 2011, so while the recent increase has an impact, it is relatively minor. Additionally, most of the current demand in the silver market is primarily physical demand, which is quite different from the situation in 2011.

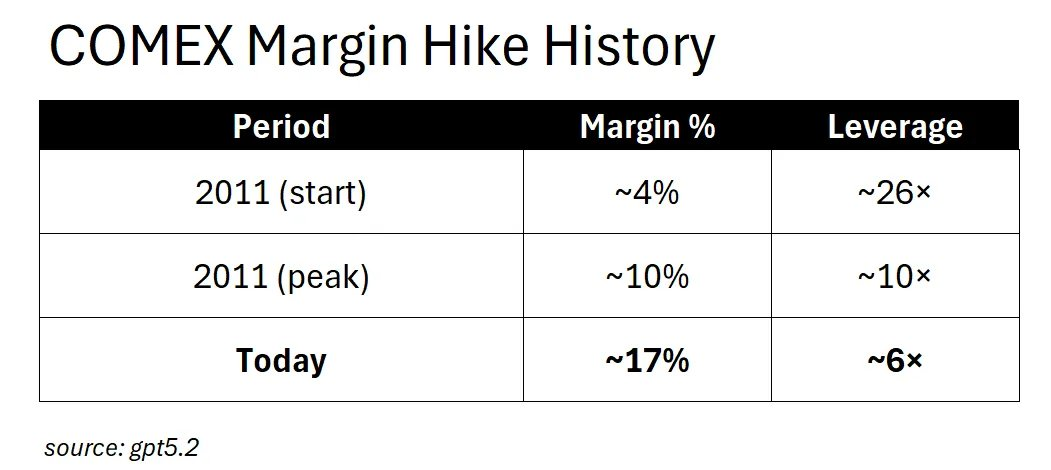

Looking back at 2011, the initial margin requirement for silver was only about 4% of the nominal value, meaning you could control $100 worth of silver with just $4 of capital—equating to 25 times leverage, which is extremely risky. Subsequently, the CME raised the margin ratio to about 10% within weeks, causing leverage to plummet from 25 times to 10 times, and the chain reaction of forced liquidations directly killed that silver rally.

And today? The current margin ratio for silver has reached about 17%, equivalent to 6 times leverage, which is even stricter than the margin requirements during the most stringent periods of 2011.

The current market environment has entered the "post-squeeze" margin phase, so what impact will further margin increases have? The answer is: it will not trigger panic selling from speculators, as there is not much speculative leverage left to clear in the market. Instead, these adjustments will have a greater impact on hedgers, such as producers trying to lock in prices, refiners managing inventory risks, and commercial players relying on the futures market.

If the margin ratio is raised to 20%, you will not see the chain reaction of forced liquidations like in 2011. The real outcome is: **reduced liquidity, wider bid-ask spreads, and commercial players turning to the *over-the-counter (OTC) market*. The operational mechanisms of the market have fundamentally changed.

Therefore, those warning about margin increases are actually fighting a "previous war" (if the above analysis is correct). While this narrative may help construct a "counter-narrative" in the short term, its practical significance is limited.

- ### The Emergence of "Overbought" Commentary

As the aforementioned factors begin to manifest, you will hear those "chart astrologers" on financial Twitter (FinTwit) repeatedly proclaiming "overbought." Technical sell-offs often trigger more technical sell-offs, creating a negative feedback loop.

But the question is, "Overbought" relative to what?

The investment logic for silver fundamentally does not lie in the "lines" of technical charts or "tea leaf readings." The core driver for silver lies in its supply-demand fundamentals: the economic efficiency of solar panels (demand is inelastic, with silver costs accounting for only about 10% of solar panel prices) colliding with the rigidity of silver supply (75% of silver is a byproduct of other metals). These are the real factors driving short-term price fluctuations.

Moreover, silver has just reached an all-time high. Do you know what else is reaching all-time highs? Assets that are still continuously rising.

- ### Copper Substitution Theory

This is one of the most commonly used arguments by opponents: "They will replace silver with copper."

Well, this viewpoint has some merit, but let's do the math carefully.

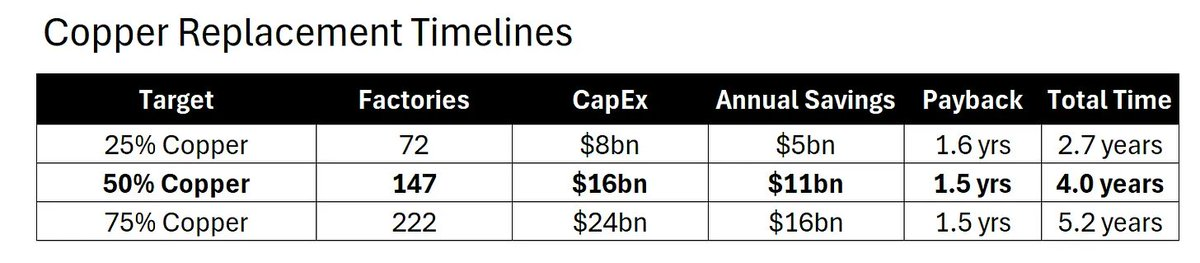

The Reality of Copper Substitution (or: Four Years is a Long Time)

The bearish argument for copper substitution does exist, but the problem is: its speed is very slow.

Here are the actual mathematical calculations, not emotional speculation:

Time is the Key Limiting Factor

Even with unlimited funds, the conversion is still constrained by physical conditions:

There are about 300 solar cell manufacturing plants worldwide;

It takes 1.5 years to convert each plant to copper plating;

The maximum parallel conversion capacity is 60 plants per year;

It will take at least 4 years to achieve a 50% copper substitution rate.

From these return cycles, a 1.5-year conversion time is an obvious capital allocation decision. In other words, CFOs should rush to approve such renovation plans.

But the problem is, even so, it will take at least 4 years to complete half of the conversion work.

Plants need to be retrofitted one by one, engineers need retraining, the copper plating formulas need revalidation, and the supply chains need realignment. All of this takes time.

Calculating Demand Elasticity

Solar manufacturers have actually absorbed the shock of silver prices rising threefold. We can look at the impact on their profits:

When the silver price is $28/ounce (average for 2024), the entire industry's profit is $31 billion;

When the silver price rises to $79/ounce (current price), industry profits drop to $16 billion. Despite profits being halved, they continue to purchase.

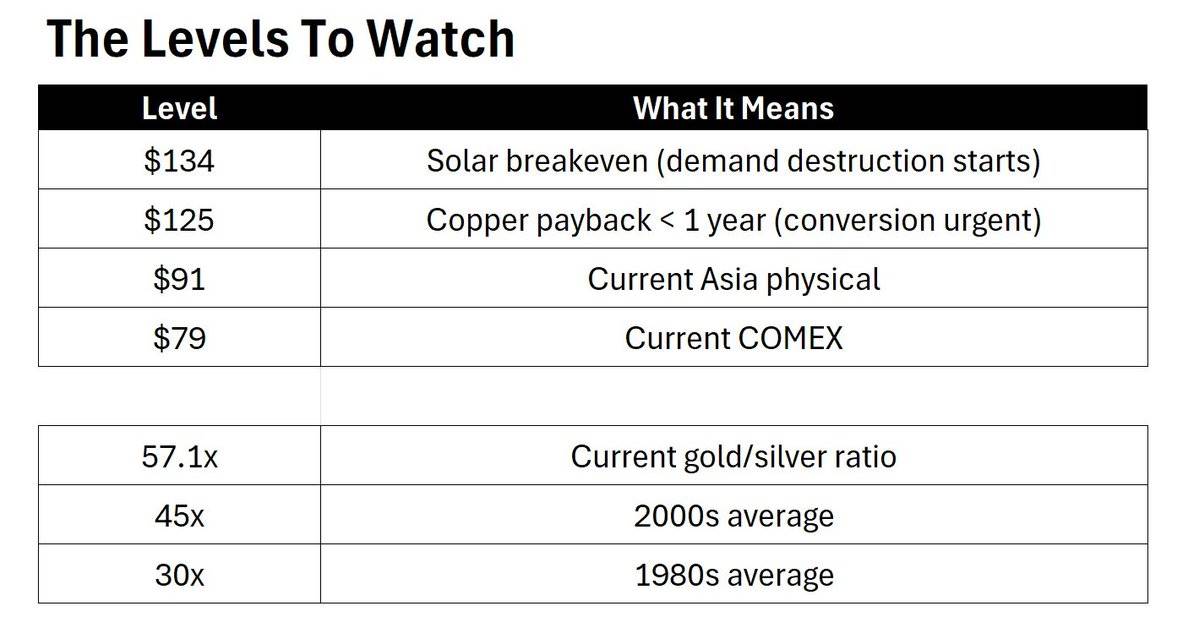

Where is the breakeven point?

Silver prices will only begin to show demand destruction when they reach $134 per ounce, which is 70% higher than the current spot price.

It is important to note that $134 per ounce is not a price target, but rather the starting point for demand destruction.

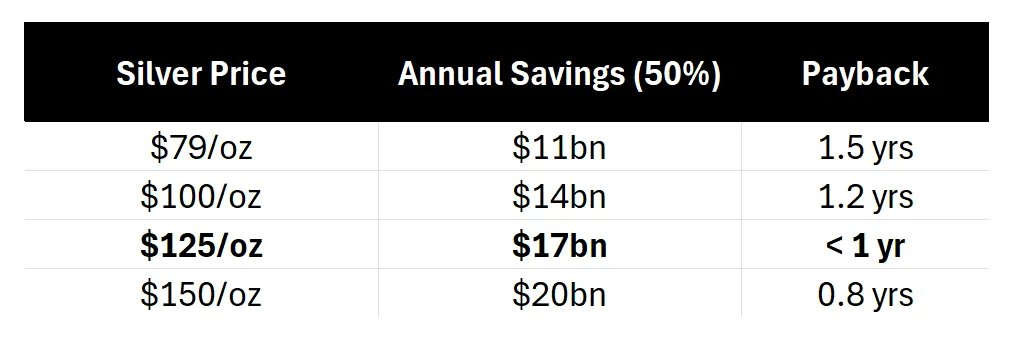

Threshold of Urgency

As silver prices continue to rise, the economics of copper substitution will indeed become more attractive:

When silver prices reach $125 per ounce, the payback period for copper substitution will shorten to less than a year, at which point every board meeting may revolve around copper substitution discussions. However, even if all companies decide tomorrow, it will still take 4 years to achieve a 50% copper substitution rate. Meanwhile, the price of $125 per ounce is still 50% higher than the current spot price.

Funds are "screaming" to "act quickly," while physical reality says "wait."

Intensity Paradox

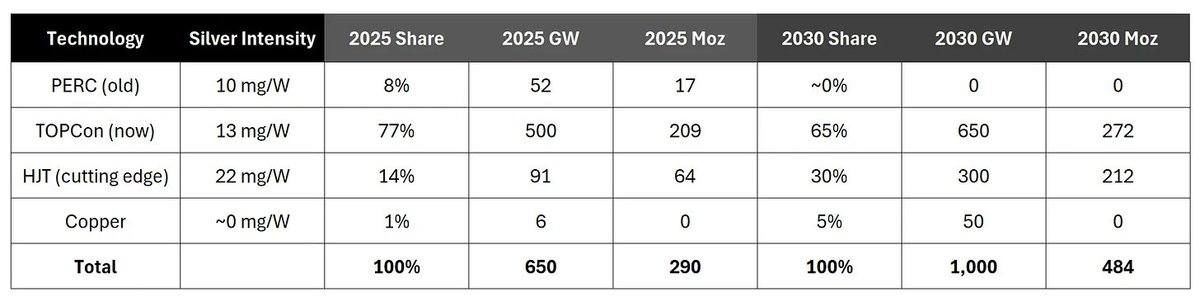

Interestingly, while everyone is talking about "copper substitution," the solar industry is actually moving towards using more silver in panel technology:

Weighted Average Silver Usage:

2025: Approximately 13.5 mg/W

2030: Approximately 15.2 mg/W

The transition from PERC to TOPCon to HJT (Heterojunction) technology has actually increased the amount of silver used per watt of solar panels, even as copper gradually replaces silver in some aspects. However, it is important to note that while the silver usage efficiency of each technology will improve over time, there are no large-scale copper investment plans, and the industry as a whole is moving towards using more silver per watt, not less.

Bears talk about copper substitution, while the industry is actually adopting HJT technology.

Conclusion on Copper Substitution

Time is passing, but it is passing slowly.

The speed of silver price increases is outpacing the speed of factory renovations. The 4-year window is the umbrella for silver bulls' logic: silver prices have 70% upside potential to trigger demand destruction, and even if copper substitution starts today, it cannot catch up with the rise in silver prices in the short term.

Silver Bull Logic (or: Why This Rally Might "Tear You Apart, but Be Pleasurable")

Alright. The bad scenarios have been addressed. Now let’s talk about why I remain bullish.

- ### China is "Weaponizing" Silver

Starting January 1, China will implement a licensing system for silver exports. This is crucial because China is the major net exporter of refined silver globally, exporting about 121 million ounces of silver annually, almost all of which flows to global markets through Hong Kong.

Now, this export flow will require government permission.

A strategic resource game is unfolding.

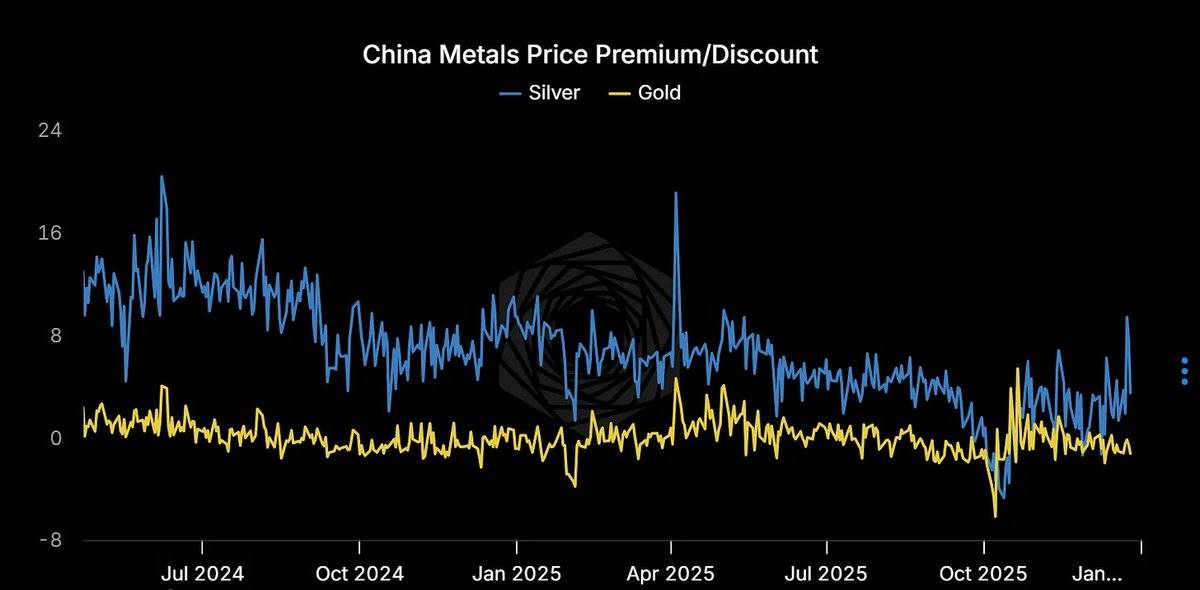

- ### Physical Silver Premiums are Astoundingly High

Shanghai: $85/ounce; Dubai: $91/ounce; COMEX: $77/ounce

You live in a dollar-denominated world, but the marginal buyers do not. They are paying $10-14 premiums and are completely unfazed by it.

When there is such a large divergence between the price of physical silver and paper prices, one side must be wrong. Historically, it is usually not the physical market that is wrong.

- ### The "Scream" of the London Market

The London over-the-counter (OTC) market is the core of physical silver trading among bullion banks, refiners, and industrial users, and currently, this market is experiencing the most severe backwardation in decades.

What is backwardation?

Simply put, it is when the market is willing to pay a higher price for physical silver today rather than the promised price for future delivery. That is, spot price > forward price. This phenomenon is not normal and usually indicates significant market pressure.

One year ago: Spot price was $29, with the price curve gradually rising to $42, which is a normal contango.

Now: Spot price is $80, while the price curve has dropped to $73, resulting in an inverted structure.

Meanwhile, the COMEX paper market still shows a lazy contango, pretending that everything is normal.

Three Markets, Three Narratives:

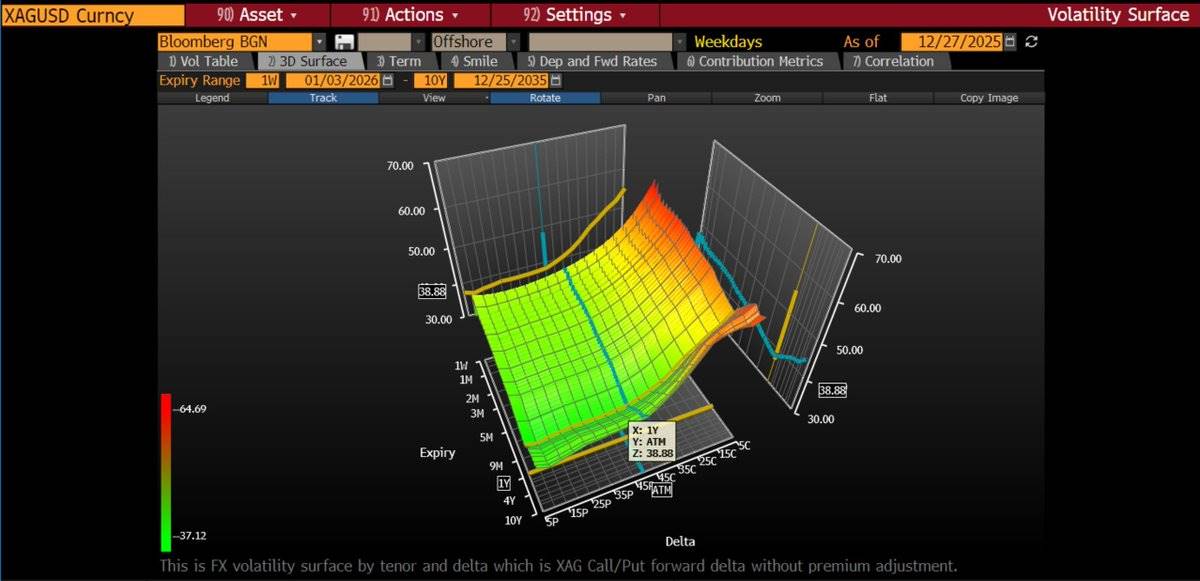

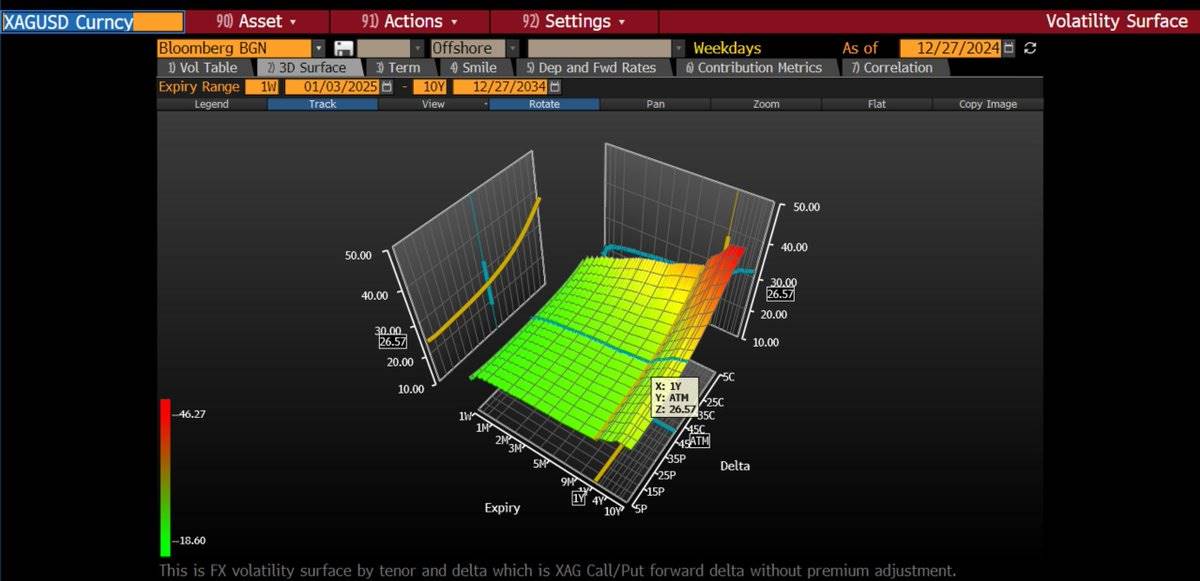

- ### Volatility has been Repriced

The implied volatility of at-the-money options (ATM Volatility) has risen from 27% to 43% year-on-year. The implied volatility of call options is even steeper—out-of-the-money (OTM) strike options have implied volatilities as high as 50-70%. This indicates that the options market is pricing in the tail risk of a significant price increase.

We are gradually positioning ourselves along the volatility curve by continuously buying call spread options, specifically: buying the implied volatility of at-the-money options while hedging costs by selling higher strike call options. Recently, we even adopted a strategy of buying 6-month butterfly options:

Buy 1 call option on SLV (iShares Silver Trust ETF) with a strike price of $70;

Sell 2 call options with a strike price of $90;

Then buy back 1 call option with a strike price of $110.

This strategy reflects our short-term view, hoping to appropriately reduce our delta exposure (sensitivity to price changes) in the event of a significant price increase.

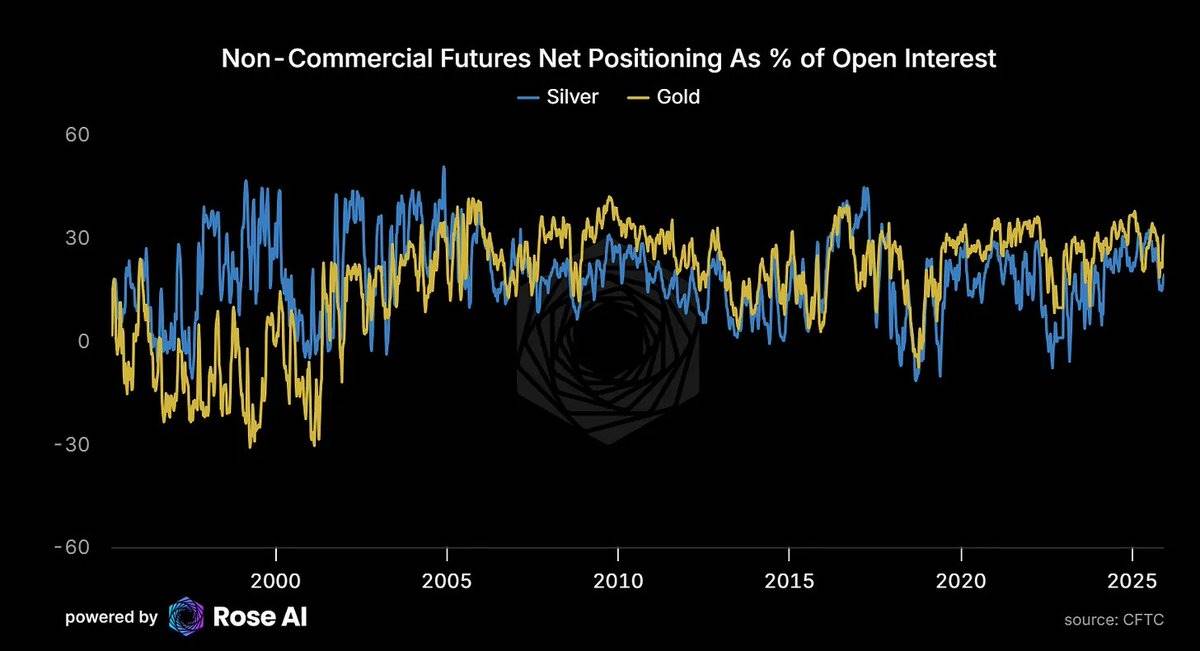

- ### Speculators Have Not Crowded In

Currently, speculative net long positions in the gold market account for 31% of total open interest, while this ratio in the silver market is only 19%. This indicates that despite the rise in silver prices, speculative positions have not reached extreme levels, leaving room for further increases.

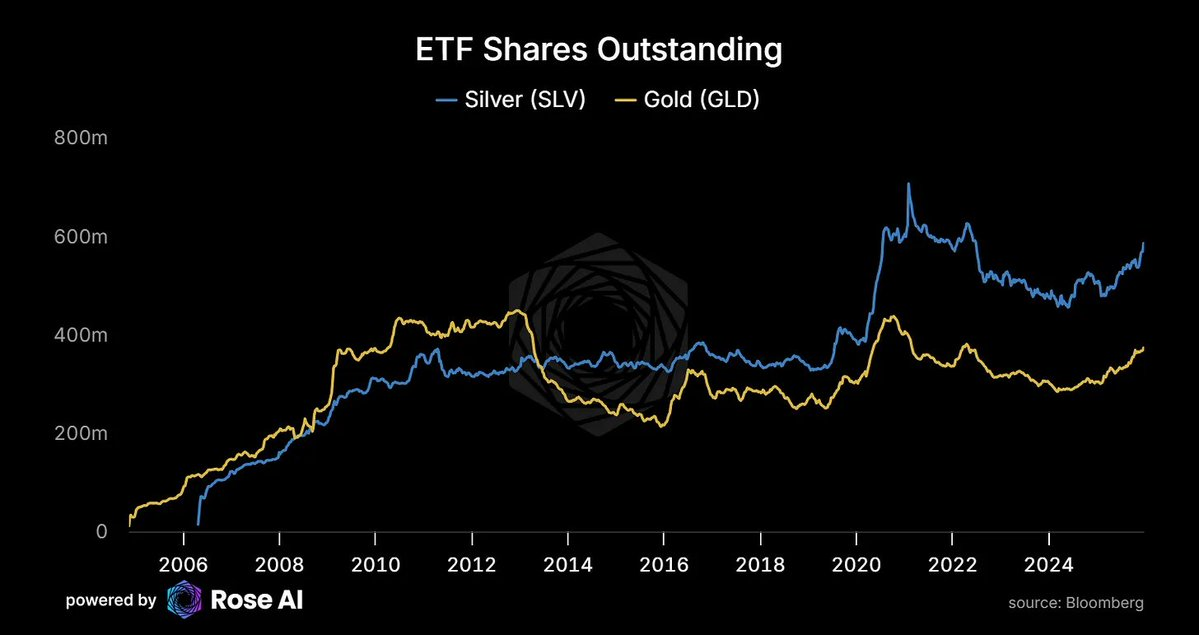

- ### ETF Demand is Catching Up

Investment demand is increasing with rising prices, validating our previous prediction: silver will exhibit characteristics similar to Veblen goods, meaning that the higher the price, the greater the demand.

The number of outstanding shares of the SLV ETF is rising again after years of capital outflows. Demand is increasing alongside price rises.

This is not typical commodity market behavior but reflects the growing demand for silver as a monetary asset.

Meanwhile, the premium for silver in the Chinese market still exists:

Western ETFs are starting to buy silver again;

While the Eastern market's physical demand for silver has never stopped.

- ### The Solar Industry's "Devouring" of Silver

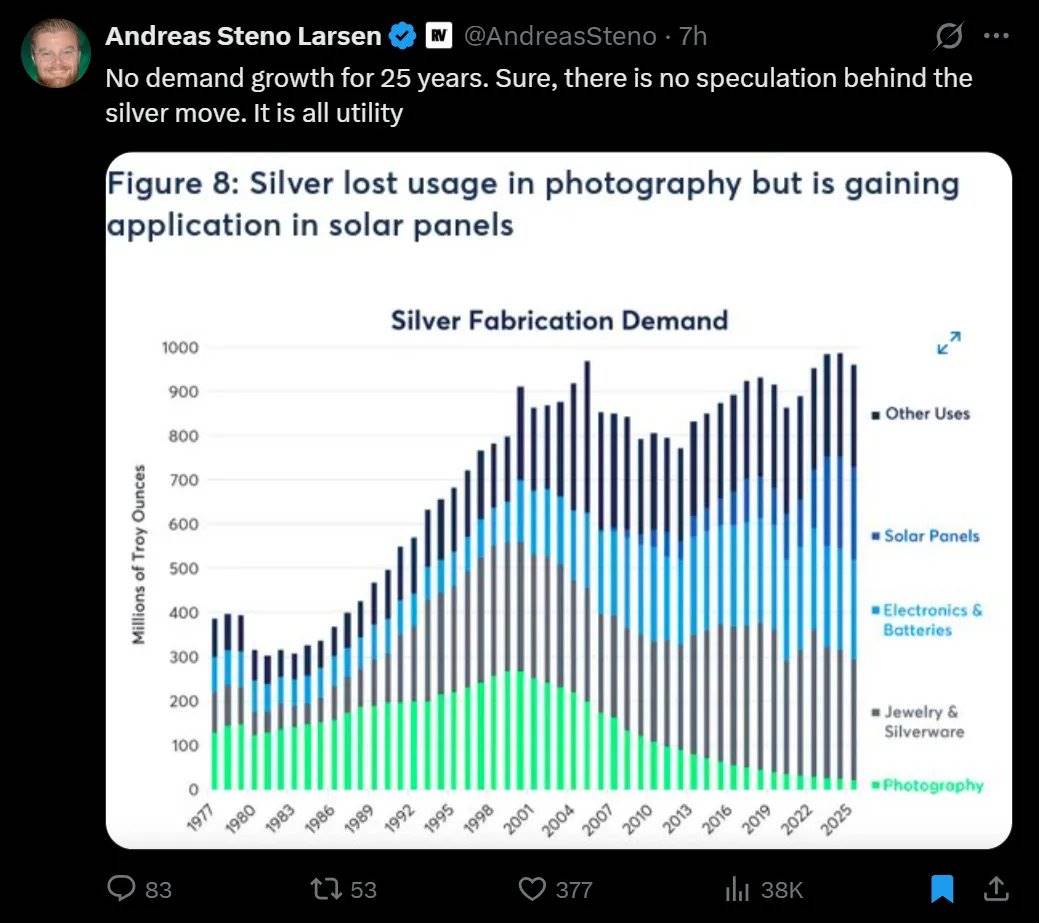

25 Years of No Demand Growth, No Supply Growth, Then Solar Came

In the past 25 years, the demand for silver in the market has hardly grown, and supply has not significantly increased. But everything changed with the rise of the solar industry. The demand for silver in the photography industry gradually disappeared, and the solar industry not only filled this gap but also further propelled explosive growth in silver demand.

Current demand for silver from the solar industry is 290 million ounces;

By 2030, this number is expected to exceed 450 million ounces.

- ### AI → Energy → Solar → Silver

A demand chain from artificial intelligence to silver has formed:

Sam Altman (OpenAI CEO) is reaching out to companies, eagerly seeking power supply;

Data centers have even started installing aircraft engines as emergency power sources to avoid delays in connecting to the grid;

Every AI query requires electricity, and the marginal contribution of new power supply comes from solar energy;

The development of solar energy is also dependent on silver.

This chain has closed.

Key Prices and Signals to Watch

Risks to Watch

January Tax Sell-off: Investors may sell off at the beginning of the year for tax reasons, leading to short-term volatility;

Strong Dollar: A strong dollar may put pressure on silver prices denominated in dollars;

Margin Increases: Although the "kill switch" has been exhausted, further margin increases should still be monitored.

Signals to Watch

Deepening Spot Premium, Price Consolidation: Indicates that the market is accumulating;

Relief of Spot Premium, Price Decline: Indicates that the squeeze is being relieved;

Persistent Premium in the Shanghai Market: Indicates that this is a structural issue, not market noise.

Observation Framework:

Focus on the curve, not the price.

If pressure in the London physical market continues while the COMEX paper market remains indifferent, the arbitrage space will continue to expand until the market experiences a "break":

Either supply suddenly increases (prices soar to release hoarded silver);

Or paper market prices are forced to readjust to reflect the true state of the physical market.

Final Summary

In the short term, there is indeed a bearish logic, and the following factors may impact the market:

Tax Sell-off: Year-end tax-related sell-offs may bring short-term volatility;

Margin Increases: Potential margin adjustments may affect market sentiment;

Strong Dollar: An appreciating dollar may exert pressure on silver prices denominated in dollars.

However, the long-term structural factors supporting silver prices remain strong:

The London market's spot premium is at extreme levels not seen in decades;

Asian market premiums are as high as $10-14;

China will implement silver export restrictions in 5 days;

The demand for silver in solar energy is highly inelastic; even if prices reach $134 per ounce, demand destruction is just beginning;

Copper substitution will take at least 4 years to achieve a 50% transition;

72% of silver supply is a byproduct of other metals, and cannot simply be increased to meet demand;

Speculative positions are not overly crowded, and ETFs are continuously absorbing physical silver;

Volatility has been repriced, and the market is pricing in tail risks of significant price increases.

This is precisely what makes the market most interesting and also the most frightening.

Recommendation: Adjust positions based on the above information and invest rationally. See you next time!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。