Original | Odaily Planet Daily (@OdailyChina)

A flash crash has happened once again.

On the night of January 31, Bitcoin briefly fell below $78,000, hitting a low of $75,700, with a 24-hour decline of 7.6%. This drop not only occurred at an alarming speed but was also deadly as it directly broke through the price range that BTC had been consolidating for nearly three months, retreating to its lowest level since April 2025.

The situation for ETH is even more grim, as its price fell below the $2,400 mark, with a 24-hour decline of 12.28%, almost completely erasing all gains since July 2025. Solana was not spared either, with its price dropping below $100, a single-day decline of 13.74%, returning to the starting point of February 2025.

Mainstream assets collectively declined, seemingly approaching a new critical point.

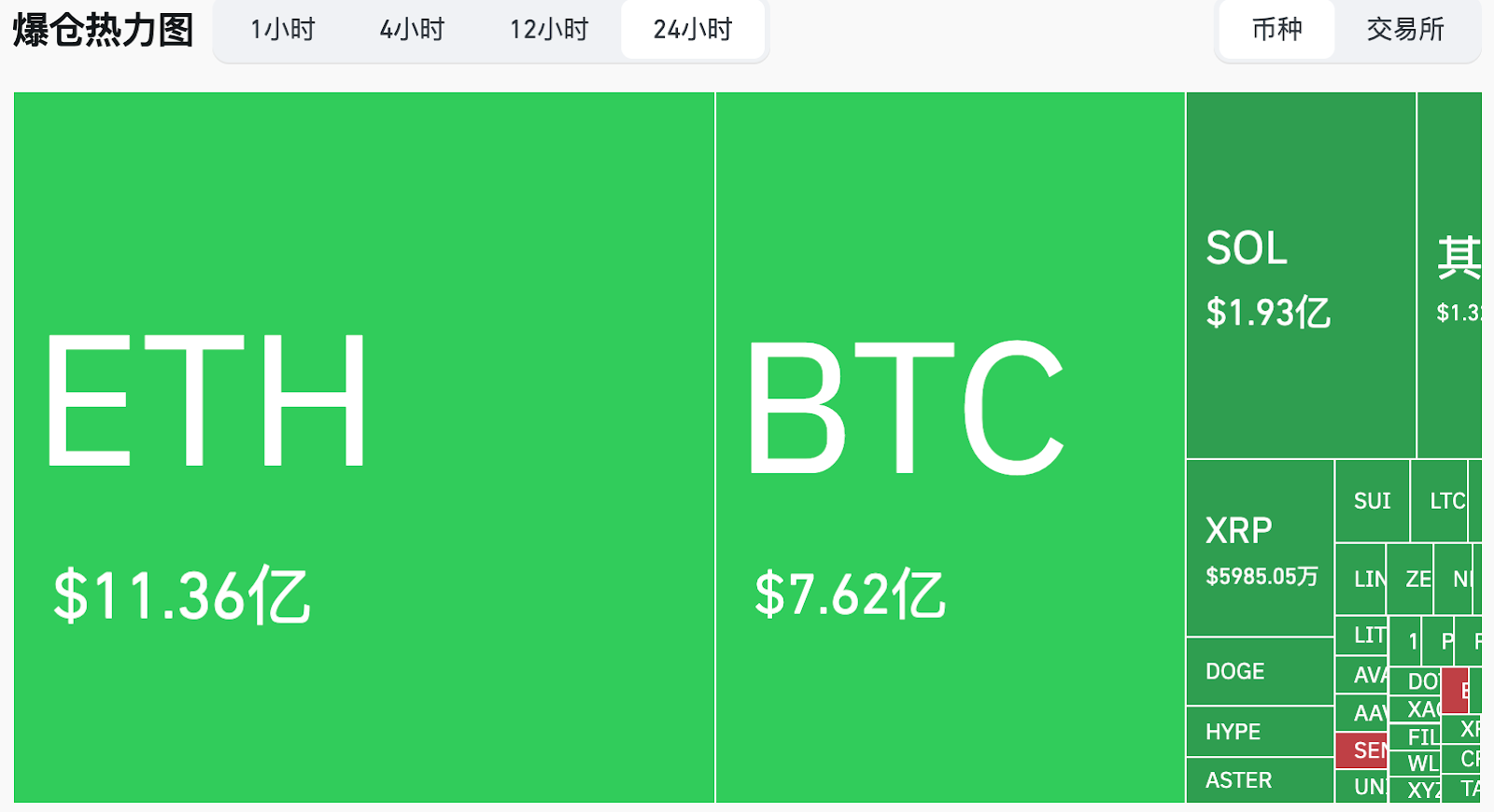

In the derivatives market, $2.522 billion was liquidated in the past 24 hours, with $2.411 billion from long positions and $115 million from short positions. The largest single liquidation occurred on Hyperliquid - ETH-USD, valued at approximately $222 million. Notably, in just the past hour, the liquidation amount reached as high as $1.14 billion.

The starting point of the decline is not just within the crypto market

The first domino in this round of market movement did not fall on-chain.

From the timeline, market tension began to noticeably escalate on January 29. The sudden escalation of geopolitical risks was one of the earliest trigger factors captured by the market. The U.S. aircraft carrier "Abraham Lincoln" and its strike group entered a "full ship blackout" state and interrupted communications, while Iran's statements also clearly shifted to a combat-ready posture. Odaily Planet Daily previously conducted a detailed analysis in "From Geopolitical Tension to Liquidity Tightening, BTC is Dragged into an Out-of-Control Market."

However, even so, the speed of the crypto market's decline far exceeded expectations. What truly caused the risk to spill over rapidly was the simultaneous crash in the precious metals market.

Gold and silver's collapse accelerated the crypto meltdown

On January 29, gold quickly turned downward after briefly breaking above $5,600, falling to about $4,740, with a maximum decline of 15.7%. Silver's adjustment was even more severe, plummeting after breaking $120, hitting a low of $76.6, with a maximum decline of 37%.

Dirk Malaki, Managing Director of SLC Management, pointed out that the crash in gold and silver began with the market's reaction to reports that Trump would nominate Kevin Warsh as the Federal Reserve Chairman. Warsh's background has a distinctly hawkish tone, which somewhat undermined expectations of a "long-term comprehensive depreciation of the dollar," and the market is re-anchoring to a more orderly monetary policy path. Related reading: "Kevin Warsh, the 'Son-in-Law of Estée Lauder,' Takes the Helm at the Federal Reserve; Could the Hawkish Big Shot be a Crypto Ally?"

Seth R. Freeman, Senior Managing Director of GlassRatner Consulting and Capital Group, also believes that the "good news" of this nomination is that the market may no longer have to repeatedly deal with the uncertainties and emotional disturbances caused by Trump's continued pressure on the Federal Reserve. The sharp drop in gold and silver has already reflected the market's repricing for a stronger dollar environment. In his view, if metal prices do not show a significant rebound in this context, it would not be too surprising. On the contrary, traders heavily invested in precious metals without effective hedging may face ongoing pressure, especially silver bulls. Some trading accounts may suffer severe losses next Monday.

Additionally, analysts mentioned that month-end concentrated profit-taking behavior and banks' hedging operations to guard against sudden declines may have amplified the selling pressure in a short time.

Adrian Ash, Head of Research at BullionVault, stated that he has been involved in the precious metals market for 20 years and has never seen a market like this. However, he downplayed the notion of "retail investors concentrating on withdrawal" and pointed out that abnormal volatility has also appeared in the markets for base metals like copper— for example, copper futures fell 4.5% in a single day on Friday. If it were just gold and silver, it could be attributed to retail sentiment, but the base metals market has almost no retail participation.

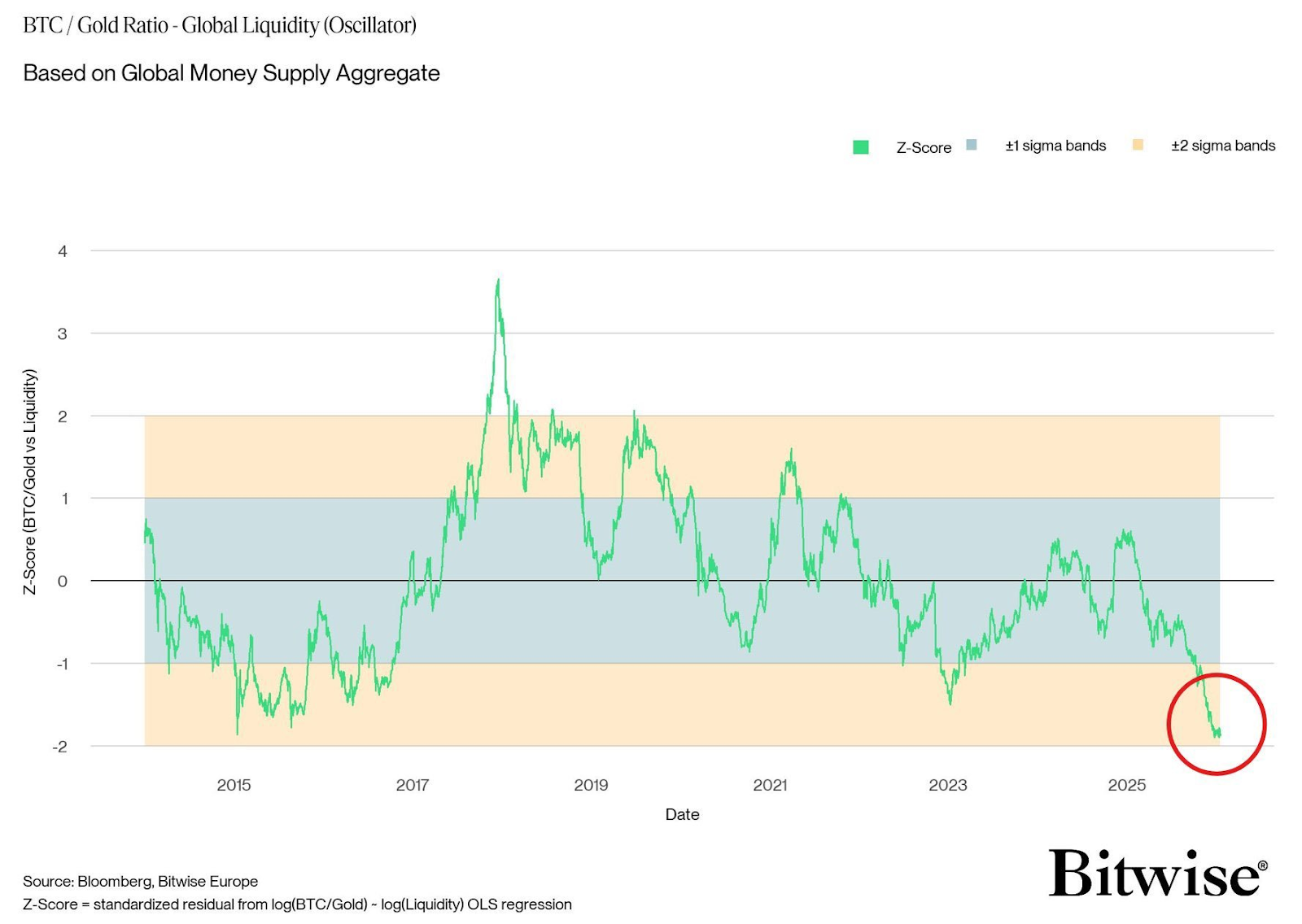

Bitcoin relative to gold has fallen to a historical low

Data from Bitwise Europe shows that the price ratio of Bitcoin to gold has fallen to a historical low. This indicator has appeared near Bitcoin's phase bottoms multiple times in the past.

This indicates two coexisting realities: on one hand, Bitcoin is currently in a clearly weak position relative to gold; on the other hand, this extreme weakness has led some analysts to view the current environment as a potential accumulation zone similar to the pre-bull market period of 2015–2017.

The market has generally observed that long-term holders are gradually absorbing recent selling pressure. As funds rotate between safe-haven assets and risk assets, some traders expect that there may be a phase return from gold to Bitcoin starting in February.

However, there are also more cautious views that point out that fund rotation is not guaranteed to happen and that macro policies, dollar trends, and overall risk appetite changes still need to be continuously monitored.

Transmission of risk and redistribution of chips

The sharp drop in gold and silver ultimately transmitted to the crypto market. It must be said that the crypto market is currently at the bottom of the food chain: when U.S. stocks rise, crypto may not rise; when U.S. stocks fall, crypto often falls deeper; and now, with precious metals falling, crypto has also not escaped the turmoil, seemingly trapped in a "curse" of following the decline without participating in the rise.

In this situation, the "believers" who are long on crypto assets also seem to be losing their chips in this torrent.

Garrett Bullish (@GarrettBullish), who once made the largest profit during the flash crash of 1011, could not escape this disaster either, as his position on Hyperliquid was fully liquidated, with a single liquidation scale exceeding $700 million, leaving only $53.68 in his account, making it the largest single liquidation this time. Data shows that in the past two weeks, his cumulative losses on Hyperliquid have been approximately $270 million.

On-chain records also show that since he began trading with this account in early October 2025, Garrett Bullish's historical cumulative PnL has lost over $128 million.

Behind the liquidation is protocol revenue. After Garrett Bullish's liquidation was completed, Hyperliquid's ecological treasury HLP gained approximately $15 million in revenue. This single event brought about a return of approximately 5.8% to gold depositors, equivalent to an annualized return rate of about 110%. Data shows that HLP currently still holds a long position in ETH valued at approximately $230 million.

The high-profile ETH bulls also seem to be struggling. According to on-chain data monitoring, Trend Research, a secondary fund under Yili Hua, currently has a total of 175,800 WETH collateralized in Aave V3, valued at approximately $445 million, borrowing about 274 million USDT, with an ETH position liquidation price of $1,558 and a loan position health ratio of 1.34. During the market decline, Trend Research has continued to add margin. Yesterday, it withdrew approximately 109 million USDT from Binance to deposit into Aave to reduce the liquidation risk of its Ethereum position.

As of January 29, Trend Research held approximately 651,300 ETH, with an average holding price of about $3,180. At the current price of $2,400, the unrealized loss is close to $500 million.

Conclusion

From the escalation of geopolitical risks to the collapse of precious metals, crypto assets have become the first to be abandoned in this process. Does this indicate that it is not a safe-haven asset and has not truly gained consensus support as a "value anchor," but can only passively bear pressure amid macro emotional fluctuations?

This round of market movement is forcing the market to re-examine a question: in a de-leveraging cycle, what justification is there for holding crypto assets long-term?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。