Original | Odaily Planet Daily (@OdailyChina)

Authors | Mandy (@mandywangETH), Azuma (@azuma_eth)

This weekend, under internal and external pressures, the crypto market has been bloodied again. BTC is currently hovering around the cost price of $76,000 in Strategy, while altcoins are so disheartened that they want to poke their own eyes out just by looking at the prices.

Behind this bleak situation, after chatting with projects, funds, and exchanges recently, a question keeps popping up in my mind: What will the crypto market be trading a year from now?

The more fundamental question behind this is: If the primary market no longer produces "the future secondary," what will the secondary market be trading a year from now? What changes will occur in exchanges?

Although the death of altcoins has long been a cliché, the past year has not lacked projects. Every day, there are still projects queuing for TGE, and as media, we are still frequently connecting with project parties for market promotion.

(Note: In this context, when we refer to "projects," we mostly mean the narrow sense of "project parties," simply put, projects that benchmark Ethereum and the Ethereum ecosystem—underlying infrastructure and various decentralized applications, and they are "token issuance projects," which is also the cornerstone of what we call native innovation and entrepreneurship in our industry. Therefore, platforms emerging from Meme and other traditional industries venturing into crypto will be set aside for now.)

If we pull the timeline a bit forward, we will discover a fact that we all tend to avoid discussing: These projects about to TGE are all "existing old projects." Most of them were financed 1-3 years ago and have only now finally reached the token issuance stage, even under internal and external pressures, they have no choice but to proceed to token issuance.

This seems like a form of "industry destocking," or to put it more harshly, queuing to complete their life cycle, issuing tokens to give teams and investors an explanation, and then they can lie flat and wait for death, or spend the money on hand hoping for a miraculous turnaround.

The Primary Market is Dead

For those of us who entered the industry during the ICO era or even earlier, experienced several rounds of bull and bear cycles, and witnessed the industry’s dividends empowering countless individuals, there is a subconscious feeling: As long as enough time passes, new cycles, new projects, new narratives, and new TGEs will eventually emerge.

However, the reality is that we have already strayed far from our comfort zone.

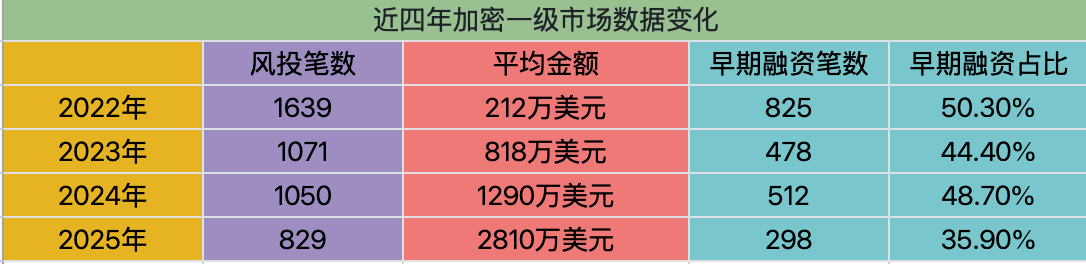

To get straight to the data, in the most recent four-year cycle (2022-2025), excluding special primary market activities such as mergers, IPOs, and public fundraising, the number of financing deals in the crypto industry has shown a significant downward trend (1639 ➡️ 1071 ➡️ 1050 ➡️ 829).

The reality is even worse than the data; the changes in the primary market are not only a shrinkage in overall amounts but also a structural collapse.

Over the past four years, the number of financing deals in early rounds (including angel rounds, pre-seed rounds, and seed rounds), which represent fresh blood for the industry, has shown a larger decline than the overall trend (825 ➡️ 298, a decrease of 63.9%), indicating that the primary market's ability to supply blood to the industry has been continuously shrinking.

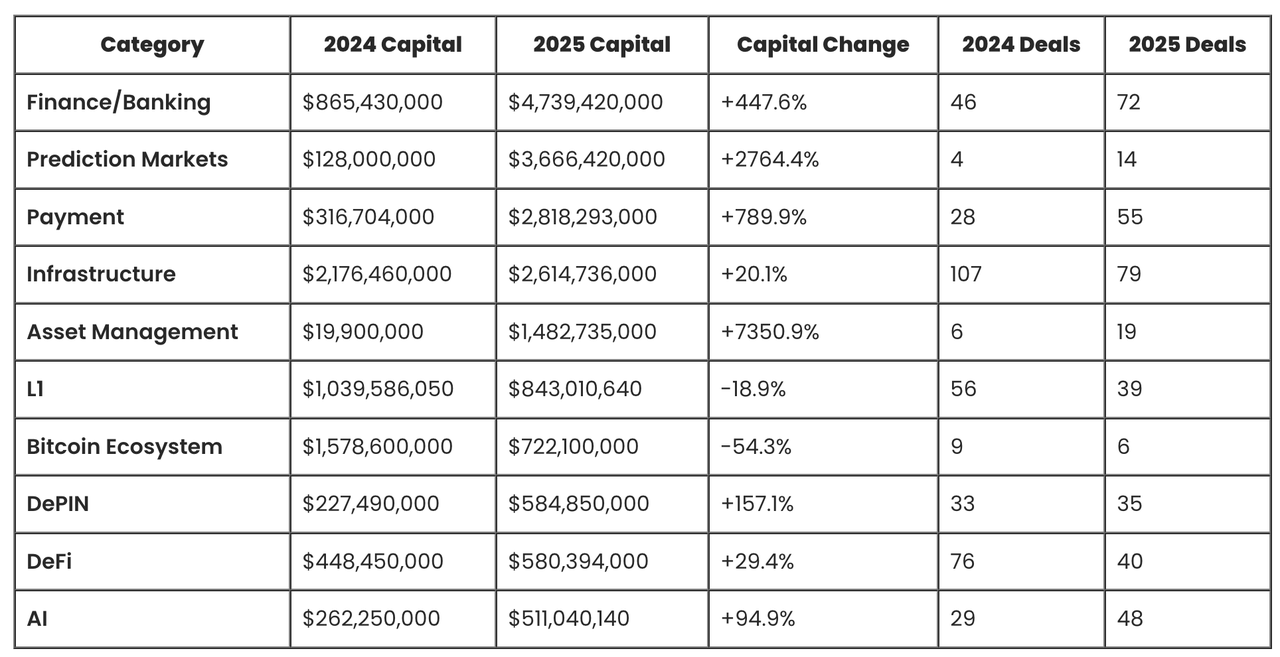

The few sectors with an upward trend in financing deals are financial services, exchanges, asset management, payments, AI, and other applications of crypto technology, but they have limited relevance to us. In simple terms, the vast majority will not "issue tokens." In contrast, the decline in financing for native "projects" such as L1, L2, DeFi, and social applications is even more pronounced.

Odaily Note: The chart is sourced from Crypto Fundraising.

A commonly misinterpreted data point is that while the number of financing deals has drastically reduced, the amount of each financing deal has increased. The main reason for this is the aforementioned "large projects" capturing a significant amount of funds from traditional finance, which has greatly raised the average; additionally, mainstream VCs tend to double down on a small number of "super projects," such as Polymarket's multiple rounds of billion-dollar financing.

From the perspective of crypto capital, this top-heavy vicious cycle is even more pronounced.

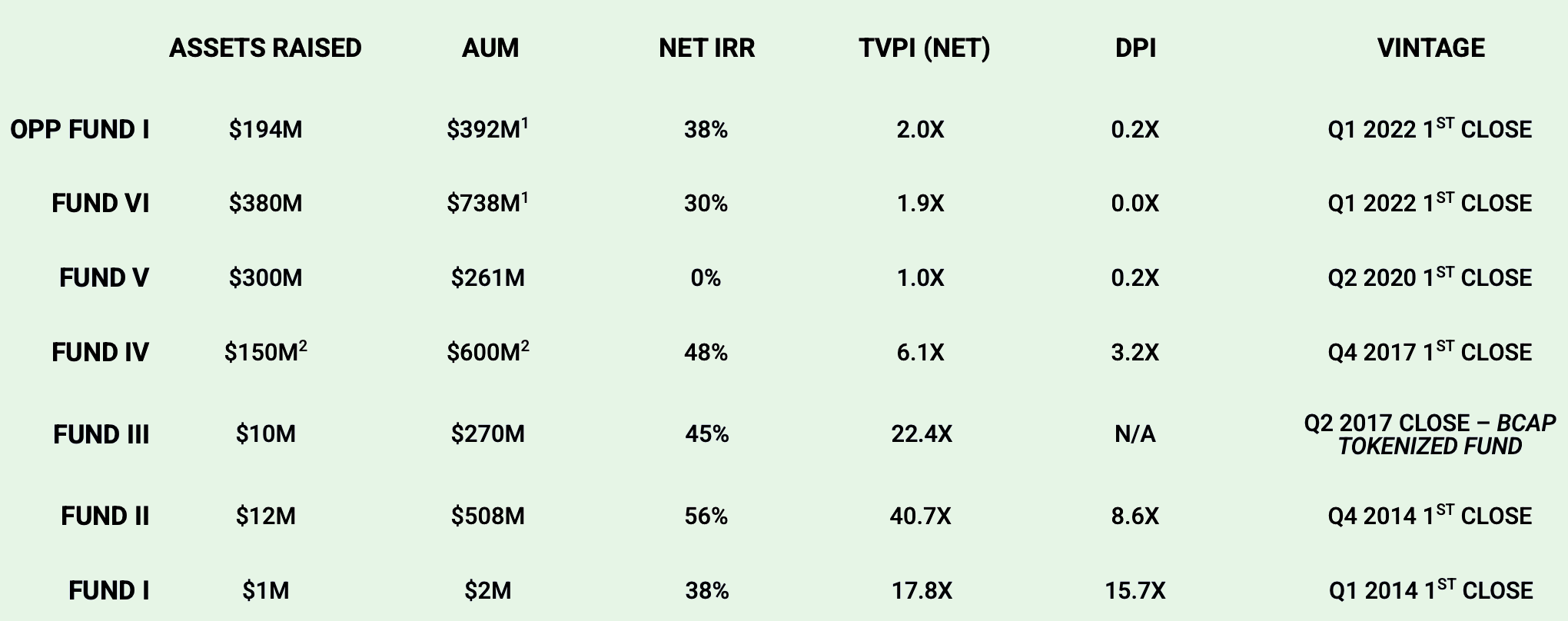

Not long ago, a friend outside the industry asked me about a well-known, long-established crypto fund that is currently raising funds, but after reviewing their deck, he was puzzled and asked me why their returns were "so poor." The table below shows the real data from the deck; I won't mention the fund's name, but I will extract its performance data from 2014 to 2022.

It is clear that between 2017 and 2022, this fund's IRR and DPI underwent significant changes—the former represents the fund's annualized return level, reflecting more of its "paper profit capability," while the latter represents the cash return multiple that has actually been returned to LPs.

From different vintage years, this set of fund returns shows a very clear "cyclical dislocation": funds established between 2014 and 2017 (Fund I, Fund II, Fund III, Fund IV) have significantly outperformed, with TVPI generally in the range of 6x-40x, and Net IRR maintained at 38%-56%. They also have a high DPI, indicating that these funds not only have high paper profits but have also completed large-scale cashing out, benefiting from the early crypto infrastructure and the first-mover advantage of leading protocols.

In contrast, funds established after 2020 (Fund V, Fund VI, and the 2022 Opportunity Fund) have clearly downgraded, with TVPI mostly concentrated in the 1.0x-2.0x range, and DPI close to zero or extremely low, meaning that returns mostly remain at the paper level and cannot be converted into real exit profits. This reflects that under the backdrop of rising valuations, intensified competition, and declining quality of project supply, the primary market cannot replicate the excess return structure driven by "new narratives + new asset supply" as in the past.

The real story behind the data is that after the DeFi Summer boom in 2019, the primary market valuations of crypto-native protocols became inflated, and when these projects finally issued tokens two years later, they faced a lack of narrative, industry tightening, and exchanges temporarily modifying terms that control the lifeblood, resulting in generally unsatisfactory performance, even leading to market cap inversions, with investors becoming the disadvantaged group and funds finding it difficult to exit.

However, this mismatched funding cycle can still create a false appearance of prosperity in certain areas of the industry, until in the past two years, when some large star funds raised capital, the harsh reality of the data became visually apparent.

The fund I mentioned currently manages nearly $3 billion, which further illustrates that it is a mirror for observing industry cycles—doing well is no longer just a matter of individual project choices; the trend has shifted.

While established funds may now find fundraising challenging, they can still survive, lie flat, collect management fees, or pivot to AI, many other funds have already shut down or turned to the secondary market.

For example, the current "Ethereum milk king" in the Chinese market, Yi Lihua, who used to be a representative figure in the primary market, investing in over a hundred projects annually, is now a distant memory.

The Alternative to Altcoins Has Never Been Meme

When we say that crypto-native projects are exhausted, a counterexample is the explosion of Memes.

In the past two years, there has been a saying in the industry: The alternative to altcoins is Meme.

But looking back now, this conclusion has actually been proven wrong.

In the early wave of Memes, we played Memes by "playing mainstream altcoins"—sifting through a large number of Meme projects for so-called fundamentals, community quality, and narrative rationality, trying to find the one that could survive long-term, continuously evolve, and eventually grow into Doge, or even "the next Bitcoin."

However, today, if someone tells you to "hold onto Meme," you would definitely think they have lost their mind.

Currently, Meme is an instant monetization mechanism of heat: it is a game of attention and liquidity, a product manufactured in bulk by Devs and AI tools,

an asset form with an extremely short life cycle but continuous supply.

It no longer aims for "survival," but rather for being seen, being traded, and being utilized.

We have a few long-term profitable Meme traders on our team, and it is evident that they are not focused on the future of the projects, but rather on rhythm, diffusion speed, emotional structure, and liquidity paths.

Some say that Meme is no longer playable, but in my view, after Trump's "final cut," it has precisely allowed Meme, as a new asset form, to truly mature.

Meme was never a substitute for "long-term assets," but rather returns to the essence of attention finance and liquidity games; it has become purer, more brutal, and less suitable for most ordinary traders.

Seeking Solutions Externally

Asset Tokenization

So when Meme becomes specialized, Bitcoin moves towards institutionalization, altcoins languish, and new projects are about to face a gap, what can we ordinary folks who enjoy value research, comparative analysis, and judgment, have speculative attributes but are not purely high-frequency probability gamblers, and want sustainable development, do?

This question does not only belong to retail investors.

It is also posed to exchanges, market makers, and platforms—after all, the market cannot always rely on higher leverage and more aggressive contract products to maintain activity.

In fact, when the entire inherent logic begins to overturn, the industry has long started seeking solutions externally.

The direction we are all discussing is to repackage traditional financial assets as on-chain tradable assets.

Stock tokenization and precious metal assets are becoming the top priority for exchanges. From a host of centralized exchanges to decentralized platforms like Hyperliquid, this path has been seen as the key to breaking the deadlock, and the market has responded positively—last week, during the craziest days for precious metals, Hyperliquid's single-day silver trading volume once exceeded $1 billion, with assets like coin stocks, indices, and precious metals occupying half of the top ten trading volumes, boosting HYPE to surge 50% in the short term under the narrative of "all-asset trading."

Indeed, some current slogans, such as "providing new choices for traditional investors, low thresholds," etc., are still premature and unrealistic.

But from the perspective of crypto natives, it may solve internal problems: With the supply and narrative of native assets slowing down, and old coins languishing while new coins are in short supply, what new trading rationale can crypto exchanges provide to the market?

Tokenized assets are easy for us to grasp. In the past, we studied: public chain ecosystems, protocol revenues, token models, unlocking rhythms, and narrative spaces.

Now, the subjects of our research have begun to shift to: macro data, financial reports, interest rate expectations, industry cycles, and policy variables. Of course, many of these aspects we have already started to study.

Essentially, this is a migration of speculative logic, rather than a simple category expansion.

The launch of gold tokens and silver tokens is not just about adding a few more currencies; what they are truly trying to introduce is a new trading narrative—bringing the volatility and rhythm that originally belonged to traditional financial markets into the internal crypto trading system.

Prediction Markets

In addition to bringing "external assets" onto the chain, another direction is to bring "external uncertainties" onto the chain—prediction markets.

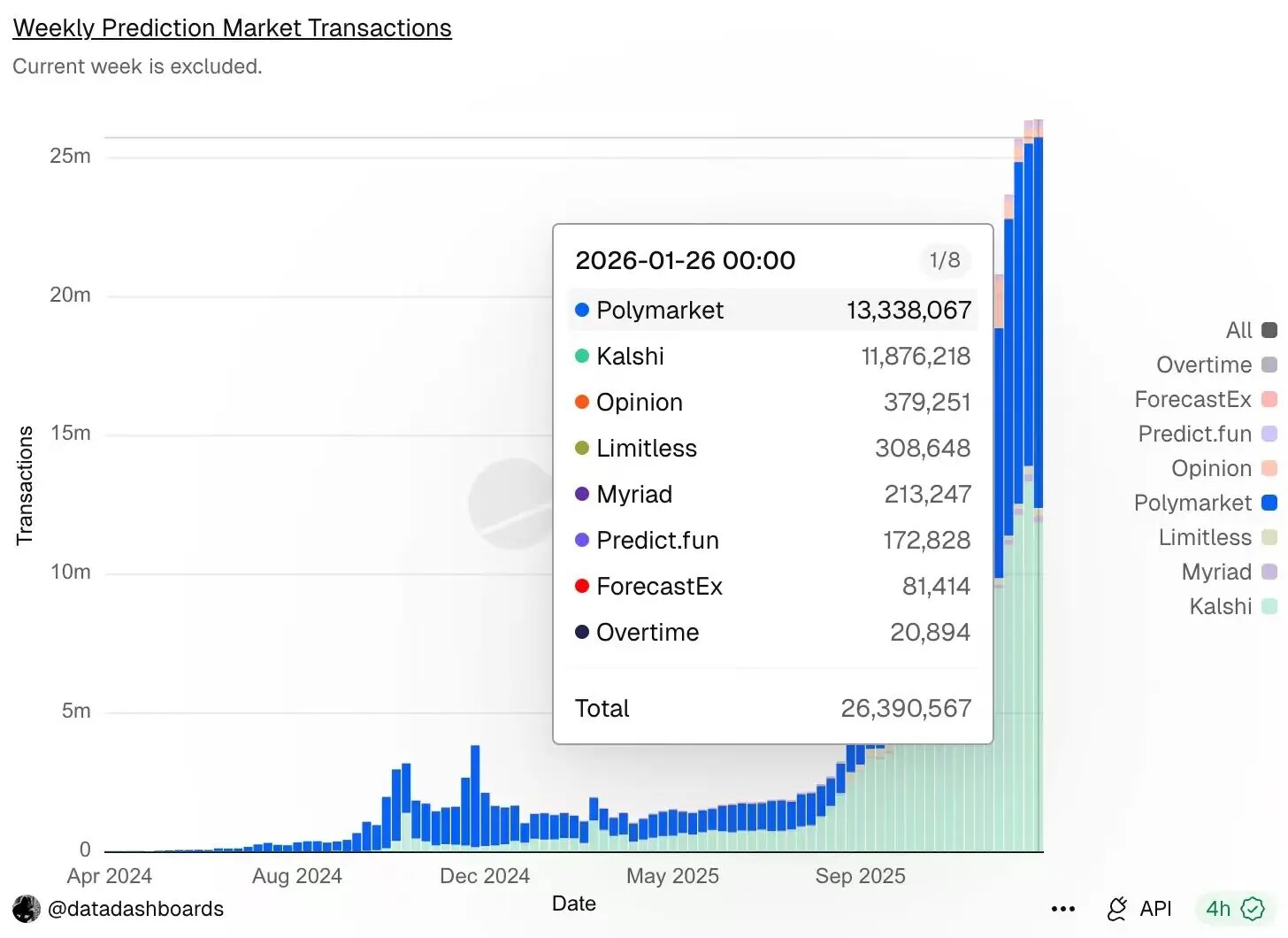

According to Dune data, although the crypto market plummeted last weekend, the trading activity in prediction markets remained active, even increasing, with weekly trading volume reaching a historical high of 26.39 million transactions. The leading platform, Polymarket, recorded 13.34 million transactions, followed closely by Kalshi with 11.88 million transactions.

We won't elaborate on the development prospects and scale expectations of prediction markets in this article; Odaily has been writing more than two articles daily analyzing prediction markets… You can search for them yourself.

I want to discuss from the perspective of crypto users why we engage in prediction markets. Is it because we are all gamblers?

Of course.

In fact, for a long time, altcoin traders were not essentially betting on technology but on events: whether a coin would be listed, whether there would be a partnership announcement, whether a token would be issued, whether new features would be launched, whether there would be regulatory benefits, and whether they could ride the next narrative wave.

Price is merely the outcome; events are the starting point.

Prediction markets, for the first time, have taken this from "implied variables in price curves" and broken it down into a directly tradable object.

You no longer need to indirectly bet on whether a certain outcome will occur by buying a token; instead, you can directly bet on "whether it will happen."

More importantly, prediction markets are well-suited to the current environment of "new projects in short supply and scarce narratives."

As the number of tradable new assets decreases, market attention becomes more focused on macro factors, regulation, politics, the actions of major players, and significant industry milestones.

In other words, while the number of tradable "underlyings" is decreasing, the number of "events" that can be traded has not diminished; in fact, it has increased.

This is also why the liquidity that has truly emerged in prediction markets over the past two years has almost entirely come from non-crypto native events.

It essentially brings the uncertainties of the external world into the internal crypto trading system. From a trading experience perspective, it is also more user-friendly for original crypto traders:

The core question is simplified to one—Will this outcome happen? and, Is the current probability expensive?

Unlike Meme, the threshold for prediction markets lies not in execution speed but in information judgment and structural understanding.

With that said, doesn’t it feel like this is something I could try too?

Conclusion

Perhaps the so-called crypto circle will ultimately disappear in the not-so-distant future, but before it does, we are still striving. As "new coin-driven trading" gradually exits the stage, the market will always need a new speculative vehicle that has a low participation threshold, possesses narrative dissemination, and can sustain itself.

In other words, the market will not disappear; it will only migrate. When the primary market no longer produces the future, what can truly be traded in the secondary market are these two things—the uncertainties of the external world and the trading narratives that can be repeatedly reconstructed.

What we can do is perhaps to adapt in advance to yet another migration of speculative paradigms.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。