Author: Tiezhu Ge in CRYPTO

Years later, facing the newly appointed Kevin Walsh and the continuous public pressure from Trump, Powell may recall the morning he first walked into the Federal Reserve Chairman's office.

It was a time when everything seemed manageable, even though the world's rightward shift was already inevitable.

At that time, 64-year-old Powell did not know that he was about to become the longest-serving chairman in the Federal Reserve's history to be in a state of emergency: he would face a pandemic, unprecedented fiscal expansion, uncontrollable inflation, asset bubbles, and geopolitical rifts, and would be forced to push the Federal Reserve into the spotlight time and again during one crisis after another.

I. Redefining the Federal Reserve: Farewell to the safety net, is it dove or hawk?

For a long time, the Federal Reserve was no longer just a central bank. It became the market's last buyer, a shadow ally of fiscal policy, the last lender to banks, and a safety net provider.

Powell gradually transformed from a technocrat known for stability and adept at managing expectations into the guardian of this large and bloated system shaped by the times.

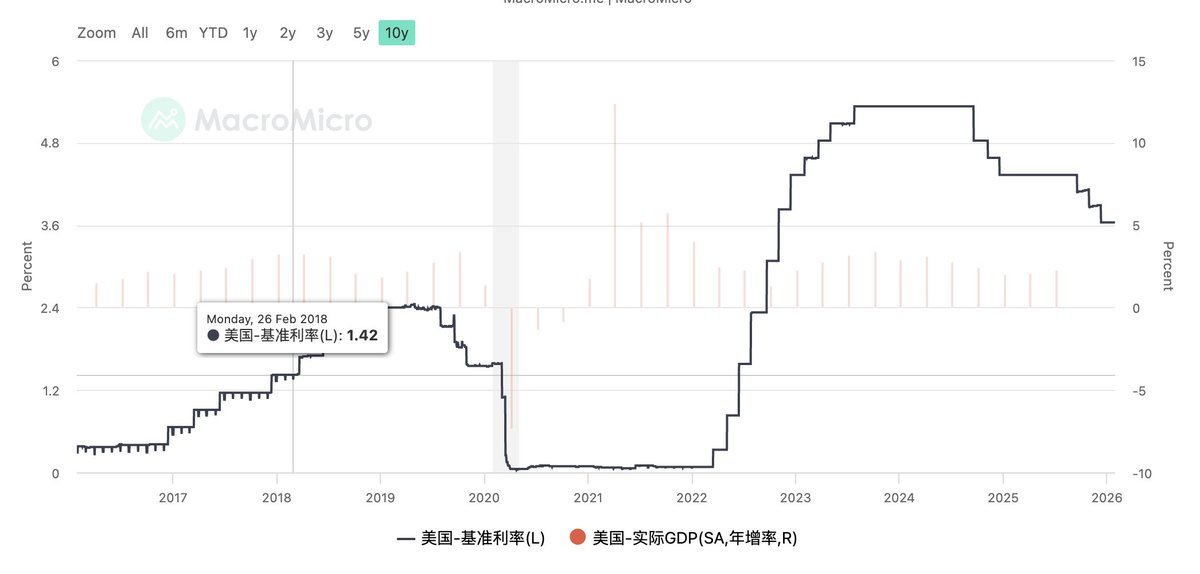

The ups and downs of interest rates during Powell's eight-year tenure

Until today.

As Kevin Walsh's name is about to be put forward as the next Federal Reserve Chairman, what has truly changed is not just the label of a so-called hawk or dove, but a redefinition of the Federal Reserve's role in an era.

Walsh is neither a traditional hawk obsessed with balance sheet reduction nor a dove that only knows how to cut rates to support the market, nor is he simply an anti-establishment figure.

What he truly represents is a response to the growing skepticism in the market regarding the sustainability of massive national debt, and the question that the Federal Reserve must answer in this new era: Should the Federal Reserve still bear the responsibility of being a safety net for all debt issues?

In Walsh's advocacy, he repeatedly mentions the need for thorough reform, which is not just about changes in interest rate paths or adjustments in balance sheet size, but a systematic reflection on the monetary policy logic of the past fifteen years. This extreme form of deform Keynesianism is approaching its end.

The history centered on demand management, which masked productivity stagnation with asset price booms, has reached a dead end.

For Trump, Walsh is a controllable reformer: he is willing to cut rates, understands the reality of debt, and unlike Hassett, does not carry a strong political patronage color, preserving the necessary independence of the central bank.

For Wall Street, Walsh is a rules-oriented person: emphasizing monetary and fiscal discipline, opposing unconditional QE, and preferring to manage the market through institutional adjustments rather than monetary policy interventions.

As mentioned in a previous Space discussion, the Fed Put may no longer exist in the next four years. Instead, there may be a more restrained central bank, clearer boundaries of responsibility, and more frequent and genuine market fluctuations. All of this will bring an uncomfortable adjustment period for all market participants.

II. The gravitational field of reality: How long until a true return, is it possible?

Before Walsh takes office, there is widespread pessimism. After all, according to Walsh's philosophy, there will be significant balance sheet reduction and a strong fight against inflation.

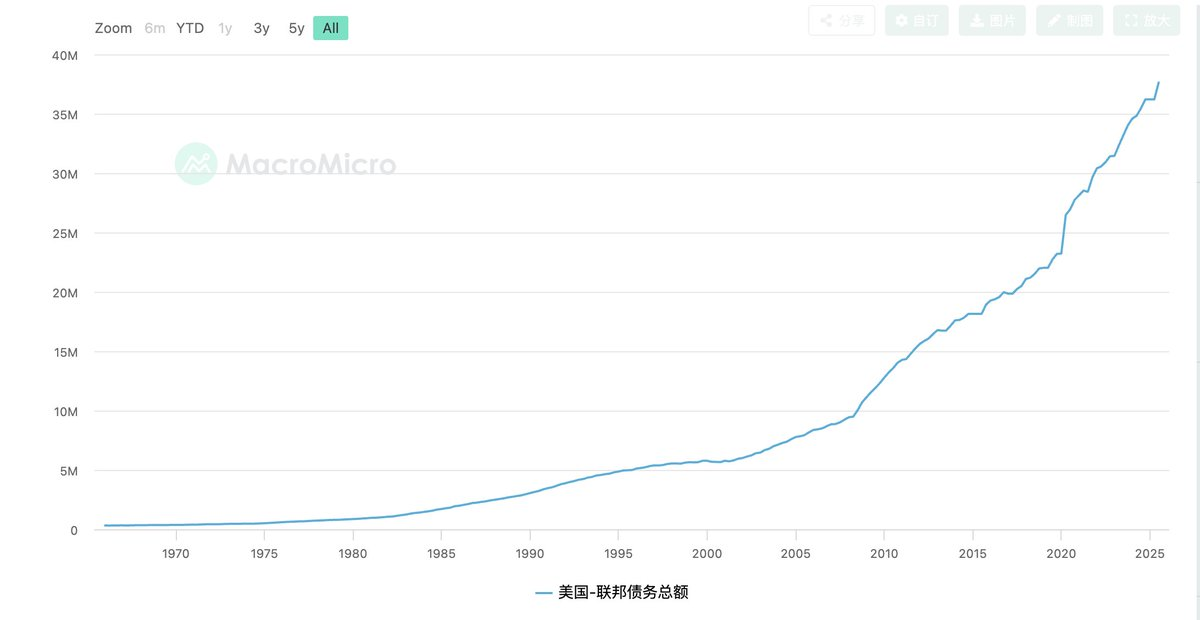

However, the current U.S. economy is in a highly fragile state that is extremely dependent on stable narratives: high fiscal deficits, debt interest payments nearing uncontrollable levels, real estate and medium to long-term financing heavily reliant on long-term interest rates, and capital markets have long been accustomed to policy safety nets.

What Walsh advocates—rate cuts + balance sheet reduction + a smaller central bank—means: it requires fiscal policy to face costs again and impose discipline; it requires the market to bear risks independently; and it requires the Federal Reserve to abandon the safety net powers accumulated over the past fifteen years.

This path is not impossible; it is logically sound and aligns with common sense. However, from a realistic perspective, the margin for error left for Walsh is actually quite limited and highly tests the control of rhythm.

Once balance sheet reduction raises term premiums and pushes up medium to long-term interest rates, it will suppress housing, investment, and employment;

Once the market experiences severe fluctuations in the absence of a central bank safety net; once voters feel the real costs brought by the so-called return to discipline.

The political system's pressure on the Federal Reserve will quickly revert to familiar directions: stop balance sheet reduction, slow down reforms, and prioritize stable growth.

Over the past years, both voters and capital markets have formed a strong path dependency through repeated crises. This inertia cannot be completely broken by a mere personnel change.

A more realistic judgment is that Walsh may push for a directional change, but a true return is unlikely to happen all at once.

III. From Trump's perspective: Another interpretation of Walsh's rise

It is well known that Trump has always needed low interest rates.

However, at the same time, in the early days of his presidency, he also publicly initiated Musk-style efficiency reforms, attempting to drastically cut government spending and reshape fiscal discipline. These two goals—low interest rates and spending cuts—are inherently conflicting within a traditional framework.

Thus, a more interesting question arises: if Trump is unwilling to fully rely on a dovish central bank for support and is aware that the fiscal situation is nearing a breaking point, then choosing Walsh may itself be a non-traditional solution?

At this stage, the U.S. fiscal deficit rate and debt size are approaching a critical turning point. Continuing along the dovish path of the past fifteen years—more aggressive rate cuts, more direct central bank interventions, and more ambiguous boundaries between monetary and fiscal policy—may seem to bring temporary market stability, but in reality, it is continuously over-drawing the dollar's credit and inflation issues.

This path has a very short political comfort period and a high probability of failure. Once inflation rebounds and long-term interest rates spiral out of control, the responsibility will almost inevitably return to the White House itself.

We must always understand that Trump has always been a master of high-stakes maneuvering. The value of Walsh lies not in his apparent ineffectiveness, but in his ability to use Walsh's hand to pressure Congress.

If the Federal Reserve, under Walsh's leadership, clearly refuses to continue providing a safety net for fiscal policy and rejects unconditional suppression of term premiums, then rising interest rates, exposed financing costs, and visible fiscal pressures will no longer be direct consequences of political decisions but rather the natural results of market discipline.

What will this bring? For Congress, continuing unconstrained spending expansion will quickly become unsustainable; for the fiscal system, cutting benefits and compressing deep budgets will finally have a forced reality basis; rather than relying on Musk-style various patchwork solutions.

Even if this path does not work, even if the market reacts excessively and the pace of reform is forced to slow down, Walsh will still be a perfect scapegoat.

Or, Walsh does not even need to succeed in reform; he only needs to expose the problems sufficiently to change the current game state between Trump and Congress, and the Democrats.

This may be the most realistic and cruel political significance of Walsh's rise.

IV. Facing the future of debt: Time for space, there is no one-size-fits-all solution

If we raise our perspective a bit higher, we will find that whether it is Walsh's reform vision or Trump's political layout, they cannot escape the same reality constraint: the United States has entered an era dominated by debt.

The scale of debt determines a harsh reality: the United States no longer has the policy freedom to completely correct mistakes, leaving only the choices of how to delay and how to shift.

This is also why "time for space" will become the only feasible but also the most undignified path. Cutting rates is using future inflation risks to exchange for current interest pressure relief; balance sheet reduction attempts to use institutional discipline to restore the credibility of the central bank; fiscal reform uses political conflict and electoral costs to smooth the debt curve temporarily.

But these choices conflict with each other and hinder one another; none can independently complete a closed loop.

What Walsh truly faces is not the question of whether to reform, but rather:

In a highly financialized, politically polarized, and debt-expanding system, how much real cost can reform bear?

From this perspective, no matter who comes to power, they cannot provide a one-size-fits-all solution.

This also means that in the next four years, what the market needs to adapt to is not a single policy shift, but a more long-term and repetitive state. Interest rates will not return to the comfort zone of zero, but it will also be difficult to maintain high levels for a long time; the central bank will no longer provide unconditional safety nets, but it will also be impossible to truly let go; crises will not be completely avoided, but will only be postponed and fragmented.

In such a world, macro policy will no longer solve problems but will only be responsible for managing them.

And this may be the ultimate point in understanding Kevin Walsh and Trump's layout: they are not competing for a better answer, but are vying for who gets to decide the costs of the past and how they are distributed in the present in an era without good answers.

This is not a story about prosperity.

It is merely the beginning of an era where reality, debt, and supply constraints are re-emerging.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。