Author: 137Labs

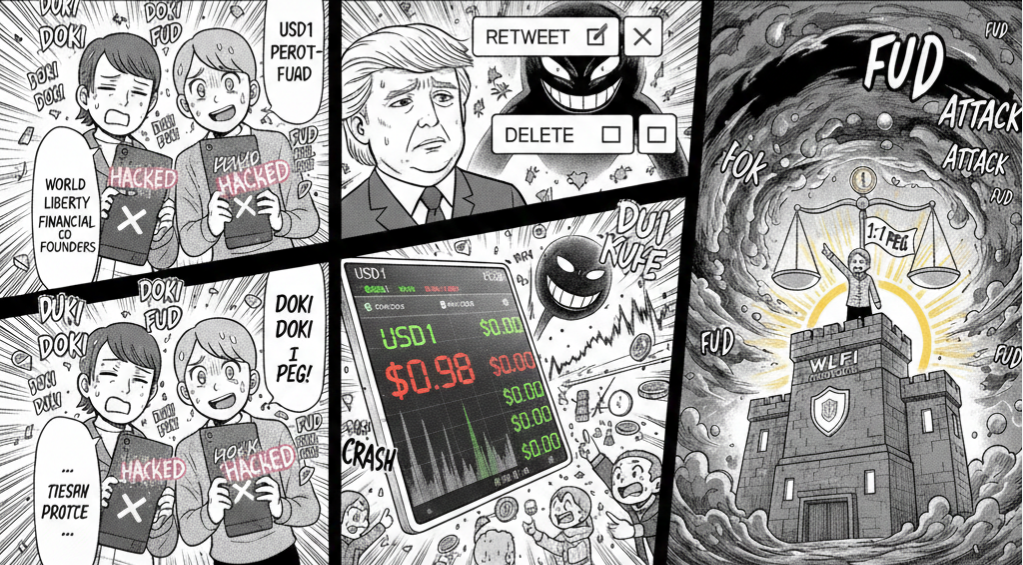

On February 23, a stablecoin calledUSD1 suddenly appeared at a significant discount in the secondary market.

On-chain quotes briefly dropped to around 0.98 USDT, and social media quickly amplified the issue.

The project partyWorld Liberty Financial (WLFI) subsequently publicly stated that this was a “coordinated attack” and emphasized that the reserves and redemption mechanisms were unaffected.

The price then recovered.

But the problem has emerged—

When a “stablecoin” starts to show a discount, is it merely liquidity friction, or a sign of cracks in the credit structure?

I. Timeline: From the Spike to the “Attack Theory”

According to reports from CoinDesk, The Block, Decrypt, Wu said blockchain, PANews, and Chain Catcher, the events unfolded approximately as follows:

1️⃣ Abnormal Fluctuation in the Secondary Market

USD1 quickly dropped to around 0.98 in some trading pairs

The discount lasted for a short duration

The price then corrected

Unlike the brief decoupling ofUSD Coin in 2023 due to banking risks, there was no clear systemic shock to the banking system this time.

2️⃣ Official Response from WLFI

WLFI stated:

This is an organized short attack and coordinated media attack

Reserve assets have shown no abnormalities

Redemption function is normal

The 1:1 peg structure has not changed

This assertion was subsequently reported by Chinese media including Wu said blockchain and Chain Catcher.

3️⃣ Amplifying Effects on Social Media

The incident quickly spread on the X platform.

Some related tweets were deleted, triggering further speculation in the market.

In the current highly emotional market environment, “deletion behavior” is often interpreted as a signal rather than a random act.

Thus, the question shifted from “Is the price decoupling?” to:

Is there a reserve risk?

Is there a concentrated run on the reserves?

Is there insufficient information disclosure?

II. The Nature of Decoupling: A Liquidity Issue, or a Solvency Issue?

Determining a stablecoin decoupling hinges on distinguishing between two entirely different risk structures.

The first is a liquidity shock.

In this scenario, reserves remain sufficient, the redemption mechanism remains intact, but a temporary imbalance in the secondary market occurs due to insufficient trading depth, withdrawal of market makers, or concentrated sell pressure. Once the arbitrage mechanism is activated, prices typically rebound quickly.

The second is a solvency crisis.

If there are issues with the reserve assets themselves, or if there is a maturity mismatch or inability to liquidate quickly, then decoupling shifts from a trading-level fluctuation to a repricing of the balance sheet. At this point, discounts tend to widen continuously, often accompanied by delayed redemptions or a collapse of trust.

Based on the information currently disclosed, USD1 appears closer to the former.

It is completely different from the algorithmic death spiral ofTerraUSD in 2022. The collapse of UST stemmed from a mechanism failure, while the spike of USD1 seems more like a sudden imbalance in liquidity.

However, even so, this incident still holds significance.

Because the true anchor of a stablecoin is not just the reserve assets, but market trust.

Once trust is questioned, prices will react before the fundamentals.

III. The Credit Structure of Stablecoins: Where Are They Really “Stable”?

Stablecoins are essentially the “base currency” of the crypto market.

Their credit support generally comes from three models:

Algorithmic

Collateralized

Centralized Custodial Reserve

USD1 belongs to a semi-centralized reserve structure.

The risks of this model do not lie in the algorithm, but in:

Reserve Transparency

Asset Liquidity

Maturity Structure

Market Depth

Whenever the market suspects that reserves may be undervalued or have liquidity risks, prices tend to decline first.

This is highly similar to the “shadow banking run” in traditional finance—once depositors begin to doubt, the act of withdrawal itself amplifies the risk.

IV. Why Was the Market Response Particularly Sensitive This Time?

The fear index of the day was already at an extremely low level.

In an environment where liquidity was already tight:

Leverage levels decreased

Risk appetite weakened

The market was highly sensitive to uncertainty

Stablecoins are not just trading tools; they are also the cornerstone of lending and liquidity.

Once discounts appear, the chain reaction may include:

Collateral Rates Declining

Triggering Liquidations

Leverage Further Compressed

Funds Flowing Out of the Market

Therefore, even if prices recover quickly, the psychological shock has not disappeared simultaneously.

V. Is the “Attack Theory” Valid?

WLFI attributed this fluctuation to a “coordinated attack.”

In the crypto market, short-selling and media resonance are not uncommon.

When trading depth is insufficient and market sentiment is weak, prices can easily exhibit amplified fluctuations.

However, whether such an attack can be sustained depends on one core factor:

Whether the market believes the reserves are real, redeemable, and sustainable.

If the reserve structure is transparent and redemptions are ongoing smoothly, attacks are often difficult to maintain in the long term;

if the reserves are insufficiently disclosed, panic is more likely to self-amplify.

VI. Differences Between USD1 and USDC, USDT, and the Real Meaning of This Decoupling

Historically, USDC dropped to $0.88 in 2023 due to banking risks, stemming from the exposure risk of the custody bank and limits on reserve liquidity.

Meanwhile, Tether has seen several slight decouplings, typically occurring during extreme panic or concentrated withdrawal pressure, but the key to recovery lies in the consistent opening of the redemption mechanism and the verification of reserve liquidity.

USD1 currently seems to be undergoing a “trust stress test.”

This incident is more akin to a liquidity shock than a solvency crisis.

The rapid price correction indicates that a systemic run has not yet formed.

However, the real concern is not just the temporary price of 0.98, but whether the market begins to reassess the risk premium of “stability.”

Stablecoins are the monetary foundation of the crypto market.

When the market questions their safety, the effects will propagate along the credit chain:

Decreased Leverage

Constricted Lending

Repricing Collateral Assets

Funds Flows Back to Mainstream Assets or Exit

Even if the event itself is merely a short-term fluctuation, it can raise future financing and liquidity costs.

Decoupling is never just a price issue, but a credit pricing issue.

Prices can recover rapidly,

but the recovery of trust takes time.

USD1’s recent decoupling may not necessarily evolve into systemic risk,

but it reminds the market—

During a phase of liquidity contraction,

credit always changes before price.

And once credit starts to be revalued,

the entire risk structure will also change accordingly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。