Author: danny

The risk control of contract trading on centralized exchanges is undergoing a indiscriminate sweeping of open interest (OI) and account freezes. Professional players urgently need a place that can withstand collateral damage risk control, support deep ambushes, conceal their identity, and strategize in a new trench. Can Aster, the protocol that is highly anticipated, become the new battleground for large funds in on-chain contract trading during this structural vacuum in the industry, supported by its permissionless nature and the robust BNBchain ecosystem?

The flame has ignited, the smoke has not yet risen, let’s see how you all respond?

“Everyone has to go through this stage. When you see a mountain, you just want to know what’s behind it?”

1. Core Operating Elements of a Contract Harvesting Scheme

A successful contract harvesting scheme must possess two key factors: 1. Absolute control over the spot market 2. Sufficient open interest (OI).

1.1 Spot Control: The Remote Control for Manipulating Index Prices

Market makers control the circulating supply of the target token, transforming the spot market into a “data盘” that can be manipulated at will. Since the contract’s reference price (Index Price) mostly derives from the spot price, and the Index Price is a key component of the Mark Price, controlling the spot effectively means controlling the Mark Price.

Once the market maker controls the spot circulating supply, they can significantly raise or dump prices in a liquidity-deficient spot market with minimal capital costs. This fluctuation in spot prices is immediately relayed to the contract market through oracles, thereby altering the profit and loss status of contract holders.

1.2 Huge OI: The Basic Condition for Realizing Profit

In situations where it is impossible to liquidate through spot (other than when the spot is locked in or closely monitored, and the spot market currently has virtually no liquidity, liquidating will damage the price and is easily traceable on-chain), contracts become the only effective means for market makers to realize profit.

Assuming the market maker invests $10 million in operations, their cost on the spot side is rigid, this includes fees, funding costs, slippage, and pump costs. If they cannot cash out in the spot market, the market maker must profit at least $30 million through contracts to cover costs and make a profit.

This explains why such a market requires a large OI. Only when the contract open positions are sufficiently large can small fluctuations on the spot side generate enough profits on the contract side to cover operating costs.

2. The Tears of the Times: Tightening Risk Control of CEX, Unable to Open Huge OI

The limitations and account risks of centralized exchanges

As global regulatory compliance requirements increase, CEX such as Binance have enhanced monitoring of account anomalies. For large funds, high-intensity trading on CEX faces multiple obstacles:

Account bans and fund freezes: Due to anti-money laundering and compliance review, frequent large fund inflows and outflows along with abnormal trading frequencies can easily trigger risk control systems, leading to account bans or long-term asset freezes.

Open position limits (OI Cap): Centralized exchanges set strict limits on the open interest of single accounts or individual tokens to prevent systemic risk, making it increasingly difficult for market makers to establish huge positions capable of influencing market expectations.

Assuming risk: Under extreme volatility, CEX’s forced liquidation engine and insurance fund mechanisms may lead to the market maker's positions being automatically taken over or forcibly reduced (ADL), turning the original harvesting plan to nothing.

3. Aster: The On-chain Derivative Battlefield of the Binance Ecosystem and Permissionless Stronghold

With strong endorsements from Yzi and CZ, combined with the ecological overlap of Bnbchain and Binance’s trading users, Aster has opened its new battlefield in the PerpDEX track with no shortage of active traders and market makers.

Aster’s API interface is essentially consistent with Binance's interface, reducing learning and migration costs significantly.

For operators, the Bnbchain ecosystem and Aster offer advantages that other CEX cannot match. It is permissionless, meaning anyone can trade merely by connecting their wallet, and there is no risk of account bans. On Aster, market makers can “recklessly” open large positions without fear of intervention from centralized platforms or "black box risk controls."

This environment has given rise to a new narrative of “contract harvesting schemes,” where, in less liquid PerpDEX environments, profit is obtained through information gaps and capital advantages, turning the contract market into a “cash machine” where profits cannot be achieved in the spot market.

4. Anomalous OI Phenomenon Exemplified by Pippin

Pippin ($PIPPIN), an active AI-driven meme token at the beginning of 2026, exhibits the characteristics of this trading model. On-chain data suggests that internal holders of Pippin allegedly control about 80% of the supply through 27 associated wallets, which is typical of high control.

On Aster, Pippin has demonstrated an enormous OI that is completely disproportionate to its daily trading volume. Pippin's OI reached 71 million (should actually be 35.5 million), while the 24-hour trading volume was only 7.6 million, with a trading volume/OI ratio of only 0.214, a highly bizarre phenomenon.

The logic behind this phenomenon is that market makers have accumulated a large number of positions in Aster without needing real turnover. When the market maker pumps or dumps the price on the spot side (index price rises/falls), their contract positions on Aster will generate massive unrealized profits, and due to the lack of centralized institutional monitoring, this behavior of “self-pumping and self-promoting” can continue until a sufficient opposing side is found for profit realization.

5. Although Liquidity is Poor, See How I Transform Positions into Profit: Price Transmission and the Role of Market Makers

On less liquid and less active PerpDEXs (like Aster), the market maker's core challenge is how to smoothly exit positions, that is, “liquidate.” However, on a relatively weak liquidity platform like Aster, price smoothness and transmission highly depends on market makers and algorithms. How is this achieved?

Note: Aster’s liquidity for specific trading pairs is actually quite good, in no way inferior to CEX.

5.1 Cross-Exchange Price Transmission Mechanism

After accumulating a large OI position on Aster, the market maker triggers price fluctuations by controlling the spot; these fluctuations not only generate unrealized profits within Aster (as well as position liquidations within Aster), but will also transmit through the following paths:

Oracle trigger: Spot price change -> Oracle update -> Aster Index Price change.

CEX contract follows: Since Binance is the liquidity center, the market maker creates fluctuations simultaneously on Binance Alpha and Binance Perp.

Price difference control and transmission: The market maker manually controls the price difference between Aster and Binance through market making robots. To avoid unilateral risks, market makers will transmit price pressure from Binance to Aster, while the market maker waits for this liquidity on Aster, ultimately achieving profit realization.

Assuming the market maker is net long on Aster, they create an “arbitrage opportunity” with a higher price on Aster and a lower price on Binance.

According to the theory of price regression, once arbitrageurs capture this opportunity, they will short Aster and long Binance. Thus, the market maker can smoothly transfer their positions (closing shorts) to the arbitrageurs for profit, and vice versa.

For example:

When the market maker raises the spot, they will deliberately control the price difference between Aster and Binance (or other major exchanges).

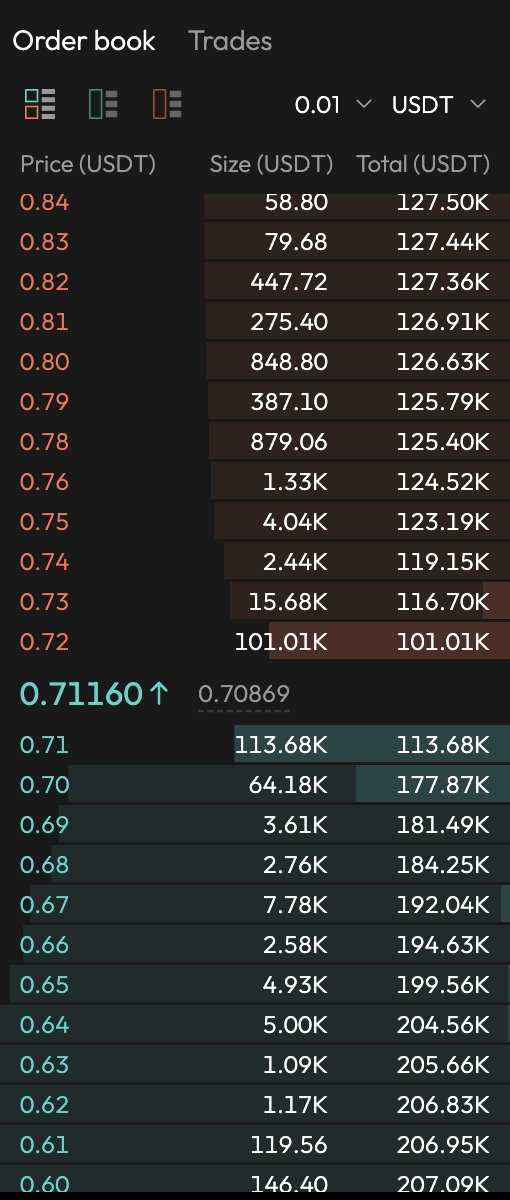

(The above image shows Aster's quotes, the below shows Binance's quotes. Please ignore the formatting; the screenshots are here to indicate this is an observable opportunity.)

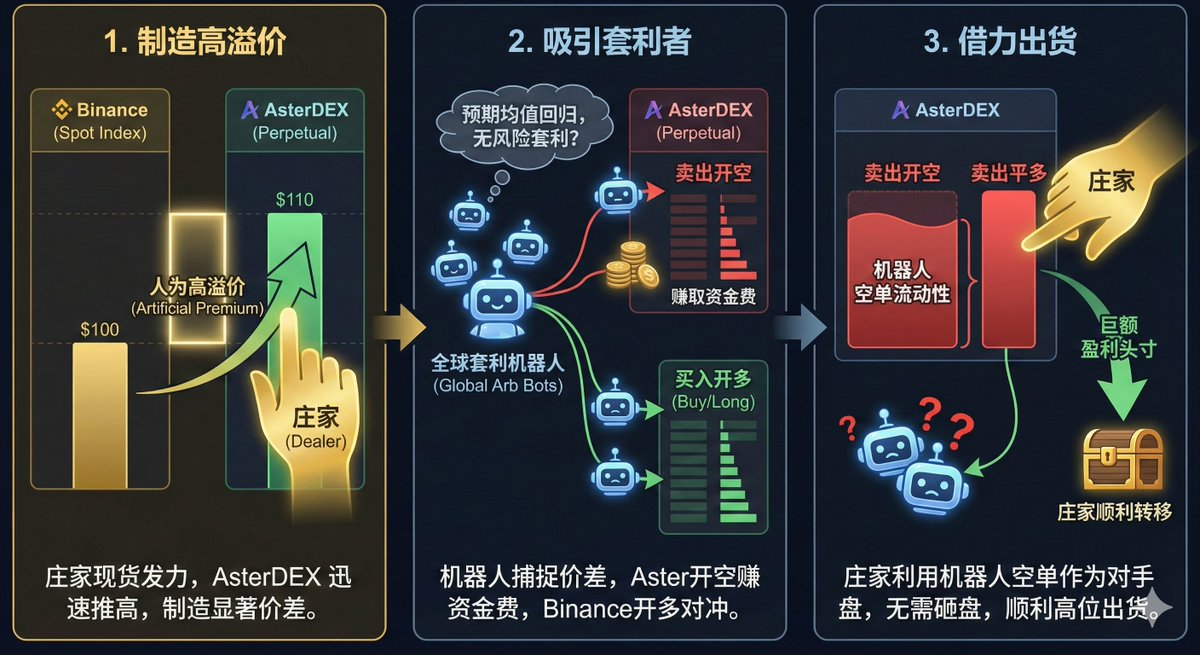

Creating High Premiums: The market maker first exerts force in the spot market, while rapidly driving up prices on Aster, resulting in Aster's price significantly surpassing Binance's index price. (Aster's order book is relatively thin, as shown in the image below)

Attracting Arbitrageurs: Arbitrage robots worldwide will quickly capture this price difference. According to the traditional logic of mean reversion, these robots will expect Aster’s price to eventually fall back and anchor to Binance’s price.

Thus, these robots will short Aster (also earning funding fees) while going long on Binance, attempting to profit from the price difference.

Leveraging Positioning/Reducing Positions: At this point, the robots’ short positions conveniently become the opposing positions that the market maker wants to close out their long positions. The market maker utilizes this “market inertia” to smoothly transfer their massive profit positions to these robots that think they are engaging in risk-free arbitrage.

Additionally, the robots' short positions can become the ideal fuel for the market maker, as these shorts explode, becoming the opposing positions for closing the long positions. With this “market inertia,” the market maker attracts more arbitrage robots and retail investors, ultimately pocketing their massive profit positions.

5.2 Price Transmission and Cooperation with Market Making Robots

By controlling the spot, the market maker not only profits within the market but also creates linked fluctuations in Binance Perp. Since market making robots typically adjust their quotes based on prices from multiple exchanges, the market maker’s actions on Aster will influence the inputs to the oracle, thus impacting global index prices.

This “price transmission” effect enables market makers to launch attacks on a smaller, more controllable battlefield (Aster), attracting players from larger, more liquid battlefields (Binance) into this carefully prepared venue for liquidity harvesting.

5.3 Data盘 and Real Activity

Analysis agencies such as Coinglass have pointed out the mismatches between transaction volume and open interest, as well as extremely low liquidation data on Aster. This further confirms Aster’s attributes as a “data盘.”

Market makers do not need Aster to provide excellent organic liquidity; they just require it to offer a stable, non-bannable, high-leverage settlement platform.

6. Limitations and Operating Costs

Although market makers possess great freedom on Aster, this mode of operation is by no means without cost. In addition to high funding rates (settled hourly), slippage due to inadequate liquidity also poses substantial cost outlays.

6.1 Funding Rate Expenditure

On Aster, the OI established by market makers often far exceeds that of natural traders, severely disrupting the balance of longs and shorts. As the major long position holder, the market maker must continuously pay funding fees to counterparties.

At certain extreme times, the annualized funding rate may exceed 200%. This means the market maker must complete the whole process of raising the price, inducing arbitrageurs, and liquidating within a very short time, otherwise, the massive interest expenditures will swiftly erode their operating capital.

The above image shows that in the case of opening a long position on Aster, the daily funding fee is 0.64% higher than that on Binance and 0.81% higher than that on Bybit. If we take an OI of 30 million (the nominal OI on Aster needs to be halved), that means a daily payment of nearly $96,000 more in funding fees to the short party compared to Binance.

6.2 Liquidity Friction and Spread

While Aster's liquidity performs well in the PerpDex, its overall liquidity depth still has a significant gap when compared to Binance. Large positions will create substantial slippage when entering and exiting.

Aster orderbook

Binance orderbook

It is noteworthy that some trading pairs on Aster adopt dynamic slippage, with the extent of slippage proportional to the current OI and the size of newly opened positions.

To cope with slippage situations, market makers typically do not directly close their positions on the order book all at once, but instead introduce market makers (passive), engage in off-market OTC trades, or utilize the aforementioned arbitrage-inducing strategies to liquidate in batches, minimizing slippage (twap).

What?! You ask me, which direction should Aster develop next?

With the launch of Aster Chain's mainnet and the application of its ZK privacy technology, future trading behaviors will become more concealed and untraceable—perhaps for Aster, this is the essence of privacy.

Compared to trade subsidies, volume inflation, and zero fees, this is the real necessity. If Aster can seize this window of tightening risk control from Binance and other CEXs to create its own contract trading derivative battlefield, and grasp this opportunity, a promising future awaits.

“I want to tell him, maybe after crossing the mountain, you’ll find there’s nothing special, looking back you might feel this side is better, but he won’t believe it; with his personality, he wouldn't be satisfied without trying it himself.”

The East Is Red and West Is Poison

Epilogue

The overlooked cruel follow-up: The second phase of the game

This script has a more brutal second half...

After the market maker completes their liquidation, the market landscape changes to: the market maker exits, and arbitrage robots hold large short positions, with prices still in a high premium state.

There are two scenarios coming up:

Scenario A: Boiling a Frog in Warm Water (Funding Rate Trap)

Arbitrageurs expect the price will quickly return. But what if the market maker (or new main force) chooses not to actively dump the price, instead letting it hover high for a long time to maintain some interest?

Although the robots holding short positions should receive funding fees, the market maker during the raising phase may have already accumulated enough profit to cover the initial funding fees. What’s scarier is, if market sentiment is extremely crazy, even if the market maker exits, retail buying pressure could sustain high prices. Their long positions opened on Binance may face ADL due to market fluctuations, but there won’t be enough liquidity on Aster to offload.

Scenario B: Hunting (Squeeze)

After successfully passing down long positions to the robots (converting to the robots' short positions), the market maker sometimes conducts reverse operations.

The market maker knows that the largest shorts in the market right now are those mechanized arbitrage robots.

If the market maker (or in collaboration with other funds) sharply increases prices again in the spot and derivatives markets, the short positions of the arbitrage robots would instantly face huge unrealized losses. Due to the strict risk controls and stop losses (or insufficient margin) of the robots, they will be forced to buy at market prices to close their shorts.

The massive stop-loss buying from the robots will drive prices even higher, triggering more robots to stop-loss. Utilizing these robotic stop-loss “buy orders,” the market maker conducts secondary harvesting at even higher levels (for example, opening new short positions).

In the end, after all this tug-of-war over Pippin, how much do you think the market maker earned???

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。