Authors: Joel John, Siddharth, Saurabh Deshpande

Translated by: Felix, PANews

Under the impact of AI, the cryptocurrency field is experiencing a period of pessimism, with venture capital moving away and founders considering a shift to AI. Is it worth holding on in the cryptocurrency industry? Recently, Decentralised.co analyzed data to dissect the revenue of protocols, indicating that the valuation of crypto assets is returning to rationality, while the era of high premiums for infrastructure tokens has ended. Founders must abandon hollow narratives, establish business models based on real income and moats, and provide actual rights for tokens. Below are the details:

The "fear and greed index" of the crypto market is at a historic low. Meanwhile, its profitability has reached unprecedented heights. Since 2018, DeFiLlama has tracked that crypto-native protocols generated $74.8 billion in fees, with nearly half ($31.4 billion) generated within the 18 months from January 2024 to June 2025.

Why is an industry that has delivered its best performance in the past eight years still entrenched in fear?

Twelve projects, including Entropy Protocol, Milkyway Protocol, Nifty Gateway, Rodeo, Forgotten Runiverse, Slingshot, Polynomial, Zerelend, Grix Finance, Parsec Finance, Angle Protocol, and Step Finance, have successively shut down in the past two months. These products had been operating for years, created by passionate founders. Additionally, OKX, Mantra, Polygon Labs, Gemini, and Binance have also conducted layoffs.

Fewer and fewer people are attending industry conferences, venture capital is shifting to AI, and developers are flocking to AI in droves. This apocalyptic pessimism is real. "If you are still in the crypto industry, you should shift to AI" has become the mainstream view.

But should you really do that?

In the past few weeks, we have been pondering this question. When a new technology emerges, the market initially gives it a premium due to its novelty and grand vision. In the 19th century, nearly 6% of the UK's GDP was invested in railroad stocks. By 2026, capital expenditures by cloud service giants will account for 2% of US GDP. But when reality sets in, technological trends return to more rational valuations. The key is whether an industry can prove its value after returning to rationality.

This article will analyze the historical evolution of cryptocurrency revenue, the user stickiness of generated funds, and the essence of moats in the industry.

Research Ledger

Since the birth of the cryptocurrency industry, crypto-native enterprises have been generating revenue. Exchanges like Bitmex, Binance, and Coinbase are profitable enterprises. They are centralized, owned by a few, and their revenues are not public. However, DeFi-native infrastructures like decentralized exchanges (Uniswap) and lending platforms (Aave) have changed this situation, allowing users to view the daily profits of protocols.

People once expected the trading valuation of tokens to reflect the economic activity facilitated by these infrastructures.

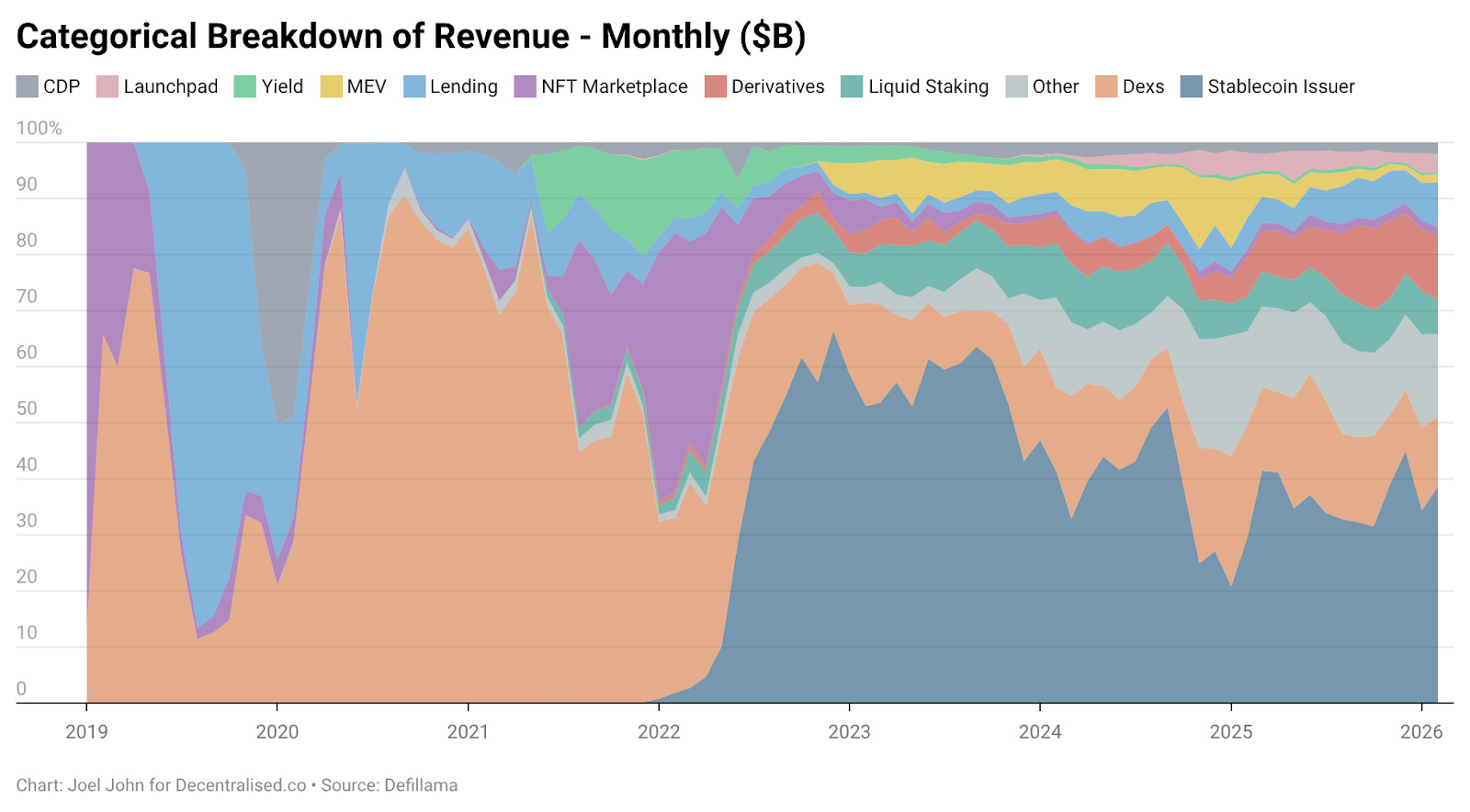

By 2022, DEX revenue accounted for as much as 28.4%, with total revenue reaching $2.27 billion that year. The lending sector is similarly concentrated, with Aave and Compound accounting for 82% of all lending fees. While there are leaders, expectations remain high for protocols that are growing and striving for market share.

The technology itself is novel enough to warrant a high valuation.

The expansion of cryptocurrencies into the consumer space has also followed. NFTs represent a hopeful vision: bringing cultural value on-chain. Well-known celebrities are changing their avatars (PFP) on X, leading people to believe this would translate into large-scale applications. OpenSea generated $1.55 billion in revenue, accounting for 71.7% of all NFT market revenue. In retrospect, the app's $13 billion valuation doesn't seem so absurd; it could potentially grow into a long-term monopoly.

However, fate and the market had other plans. By 2025, NFTs accounted for less than 1% of total revenue. We experienced a "Beanie Baby moment" without keeping any physical memorabilia. In contrast, though DEX developed rapidly, its valuation struggled to grow. Last year, DEX generated $5.03 billion in fees and lending platforms generated $1.65 billion. Together, these sectors accounted for 22.9% of total fees, down from 33.1% in 2022.

Their share of economic activity within the larger pie shrank, leading to a significant decrease in their valuations.

So, what sectors have achieved growth? How has the crypto-native business model changed since 2022?

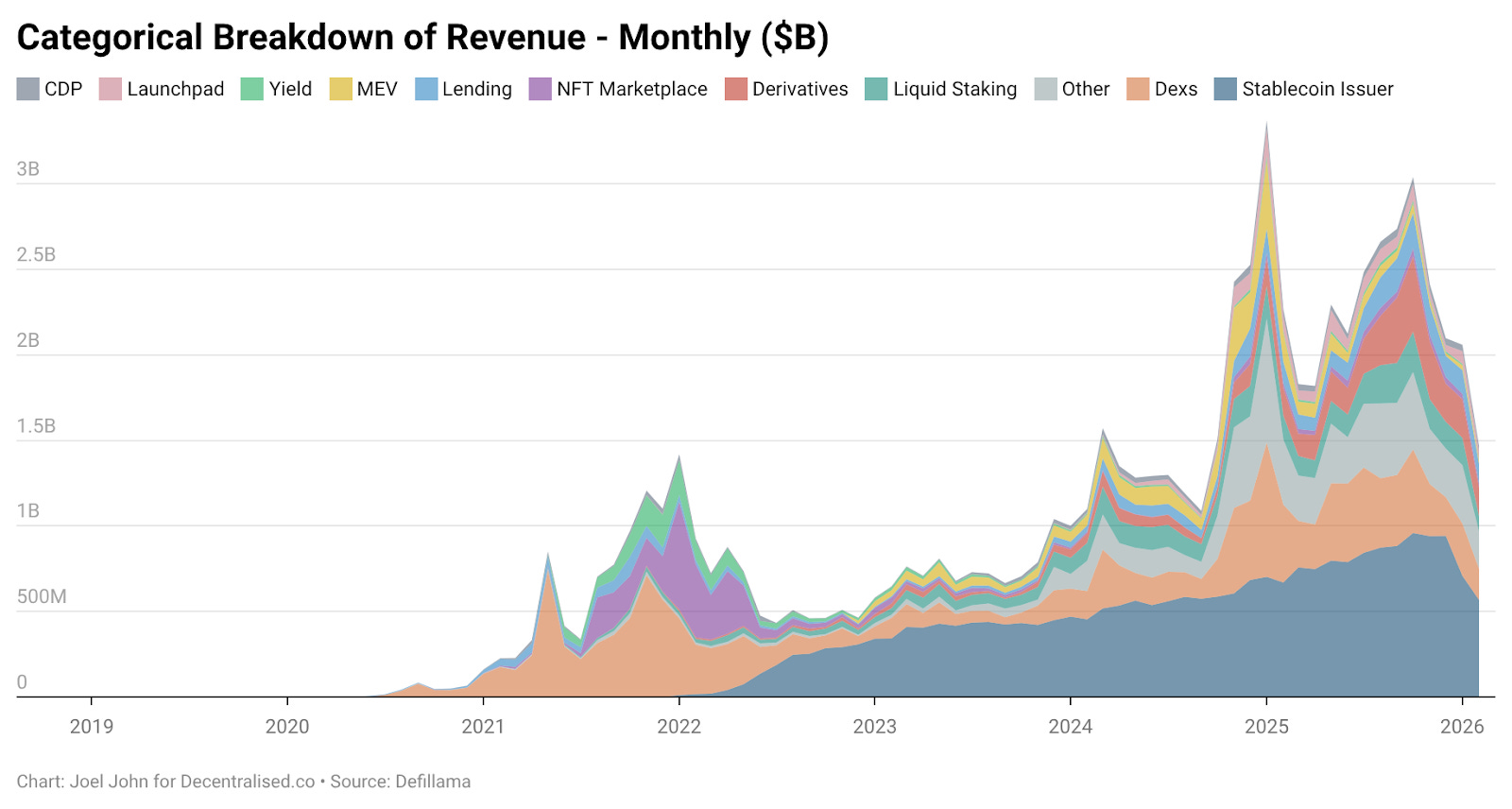

The following diagram offers some clues.

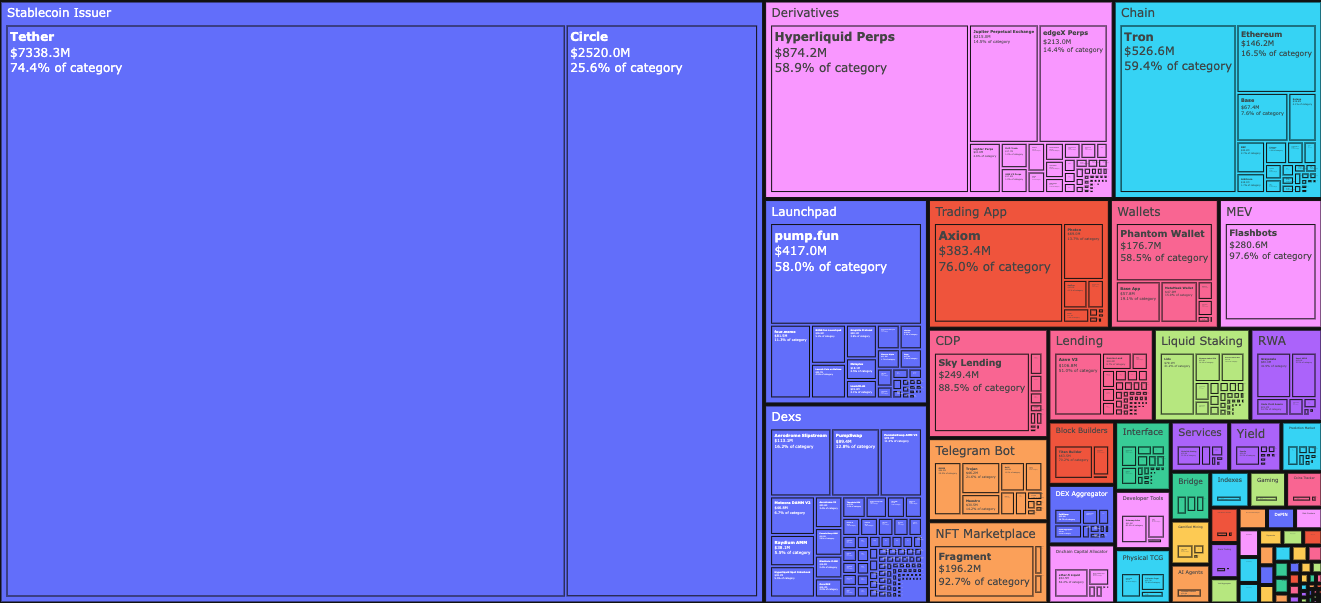

In January 2026, stablecoin issuers Tether and Circle accounted for 34.3% of all fees. In other words, for every dollar earned by the industry, $0.34 flowed to these two companies. Driven by US Treasury bills (T-bills), their income grew from $4.95 billion in January 2023 to $9.89 billion in 2025. For bank-level financial products, this represents startup-level growth. Tether's income is nearly three times that of Circle.

Their rise can be attributed to two main factors.

The first is demand. Countries in the Global South have consistently needed tools to hedge against local inflation and achieve free movement of capital. The dollar, even digital dollars, fill this gap, which local currencies cannot achieve. Capital outflows are an inevitable trend.

The second is cost structure. Blockchains bear all costs needed to operate stablecoin businesses. Unlike traditional banks or fintech companies, Tether and Circle don't need to hire employees based on the scale of stablecoin issuance on-chain. The marginal cost of issuing the next $1 billion on-chain and transferring the next $100 billion is almost zero.

These two forces intertwine. On one hand, demand drives stablecoin issuance, with citizens voting with real money; on the other hand, the cost curve flattens. Together, they make stablecoin issuance one of the most capital-efficient businesses in financial history.

The stablecoin business needs to build moats in liquidity, compliance, and the Lindy effect (PANews note: The Lindy effect states that for things that do not naturally disappear, such as a technology or an idea, their expected lifespan is proportional to how long they have already existed; the longer they survive, the greater their remaining expected lifespan increases). Few issuers can withstand multiple cycles. Tether and Circle dominate nearly 99% of the stablecoin issuance revenue. Why is that? Both assets benefit from their first-mover advantage. The network effects created by multiple exchange integrations give them "legitimacy," which pure technology cannot achieve.

Tether was initially launched as a sidechain on the Omni platform. It ran slowly and awkwardly but could be accessed through common channels used by over-the-counter trading platforms and exchanges. This is a distribution moat, not a technological moat. Crypto-native founders often struggle to replicate this kind of moat solely through code.

Stablecoins benefit from the Lindy effect.

Soon after, another category of cryptocurrency will also benefit from a distribution moat.

The market now only needs a touch of liquidity

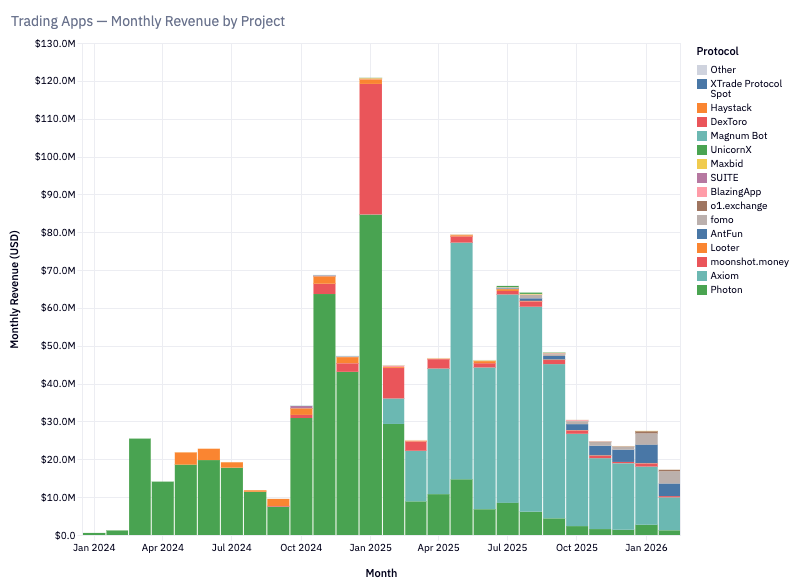

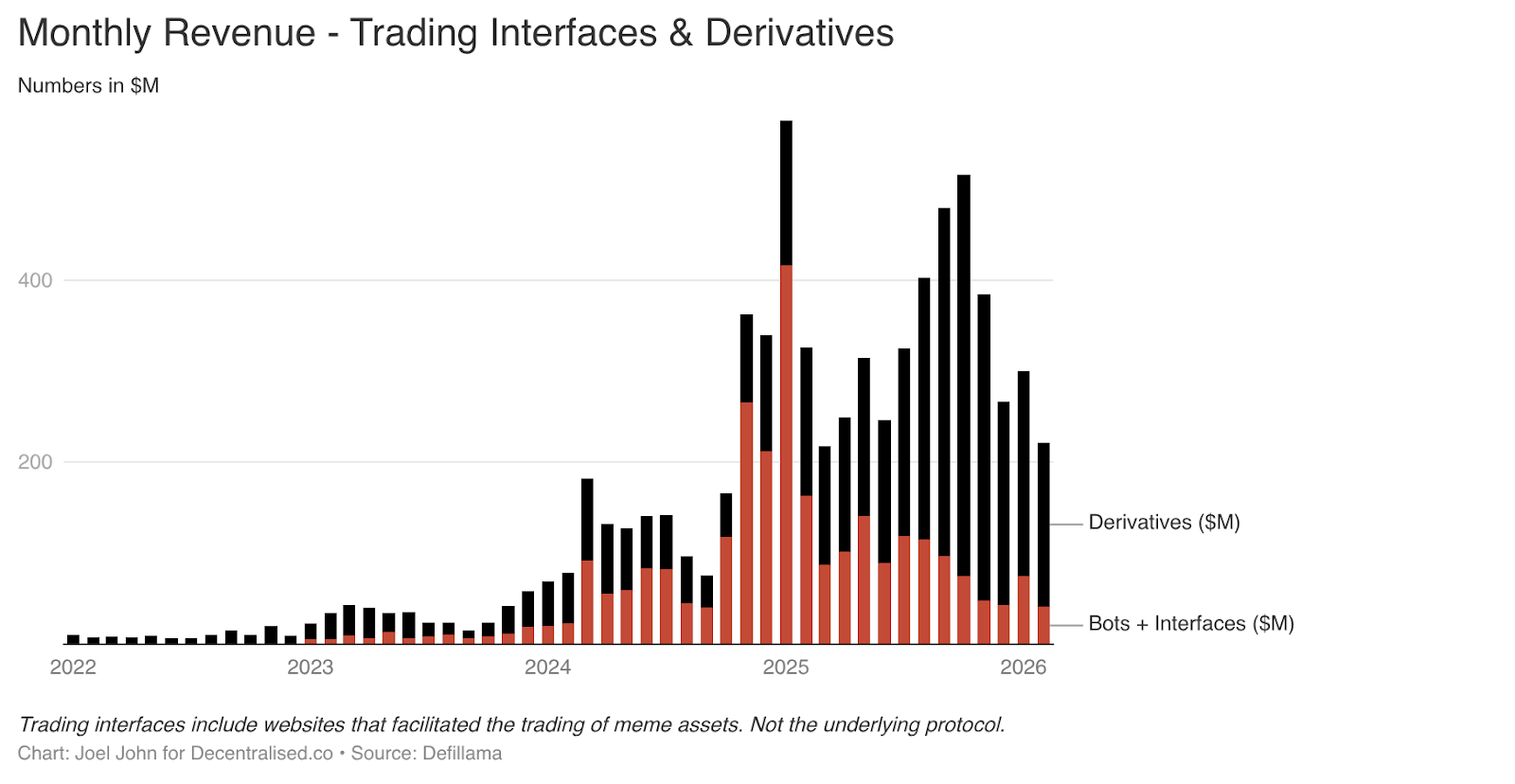

In the previous two articles, we examined the idea that "cryptocurrency is a trading economy." One focused on "the flow of funds," while another, written last year, was "everything is a market." What went unpredicted was how rapidly trading products built around Telegram trading bots and interfaces could grow.

In just these two areas, by January 2025, they contributed $575 million in fees. Considering consumer demand, this is not hard to understand. Meme coin trading and perpetual contracts allow users to profit quickly. To pursue rapid returns, they are willing to pay high fees. This category grew from 1% of total revenue to just above 15% between 2022 and 2025.

Products like TryFomo and Moonshot have generated millions in revenue by focusing on the end-user. These products are not technically complex. Instead, their advantage lies in aggregating crypto-native underlying components and bundling them for a better user experience. Thanks to the maturity of tools like Privy, developers no longer need to incentivize liquidity or manage wallets manually.

The native features we were excited about in 2022 have now matured. Applications like BullX and Photon are built on these features. This sector alone generated approximately $1.93 billion in trading fees between January 2024 and February 2026.

Meme assets have a fatal flaw: they are functionally thin and exhibit significant cyclicality. Does this feel familiar? It’s because NFTs and Web3 games have also experienced similar explosive growth followed by collapse. This cyclicality is both a defect and a characteristic of the crypto industry. We will revisit this topic later. But for now, let's clarify where the revenue is going.

Perpetual contract exchanges (and later prediction markets) represent new pathways with longevity. PumpFun democratizes asset issuance through meme coins, but this game is not fair.

Ultimately, the market realizes that meme coins will eventually fade away. The dreams of becoming a millionaire by buying tokens named "ShibaInuYouShouldShareThisNewsletter" also evaporate. People do not want to manage random token portfolios; they want to take risks. Perpetual exchanges exactly meet this need.

You can trade Bitcoin, Solana, or Ethereum with extremely high leverage. Market makers and traders needing alternatives to centralized trading channels flocked to the space. The core product of this category is liquidity. Hyperliquid holds a dominant position because its order book depth is comparable to that of centralized exchanges. Without such parity, users have no reason to migrate. Over the past three years, Hyperliquid and Jupiter have accounted for most of the fees in this category.

Perpetual contract exchanges and trading platforms have completely unveiled the mystique of cryptocurrency. They clearly indicate: earning a small fee from high-frequency trading is the true path to profitability. These "meme trading platforms" and perpetual contract exchanges act like dopamine machines that package and sell risk.

One of them will evolve into core financial technology, allowing people worldwide to trade commodities, stocks, and digital assets even on weekends. Blockchain-native applications replicate the functions long provided by Robinhood and Binance: venture capital channels.

The Demise of Protocols

Noticed yet that protocols haven't been mentioned until now? The very layer that records all internet capital flows? That’s because their stories are entirely different (but equally important). They are the victims of novelty premiums, which are gradually fading.

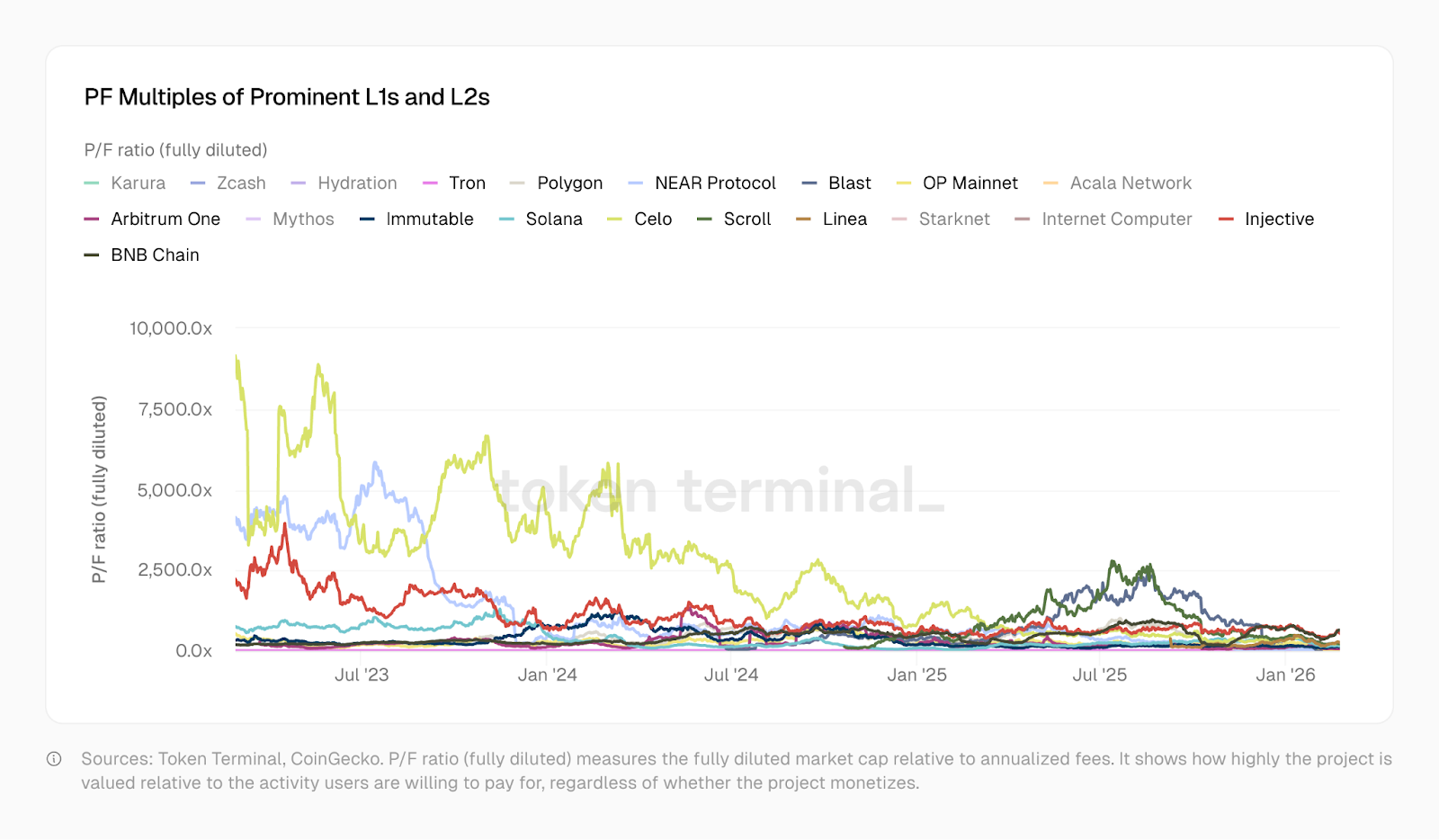

In January 2023, Optimism had a price-to-fee (P/F) ratio of 465 times, Solana 706 times, and Arbitrum and BNB around 206 times. Today, Solana is at 138 times, Arbitrum 62 times, and OP 37 times. Polygon's trading price is more akin to that of a fintech firm, at 20 times. Tron supports the stablecoin ecosystem and has a P/F of 10.2 times. Since then, Optimism, Solana, Arbitrum, and Polygon have each developed more complex products. They each have more users, better liquidity, and more sophisticated financial application suites built upon them.

The discount on their P/F reflects the market's view of them.

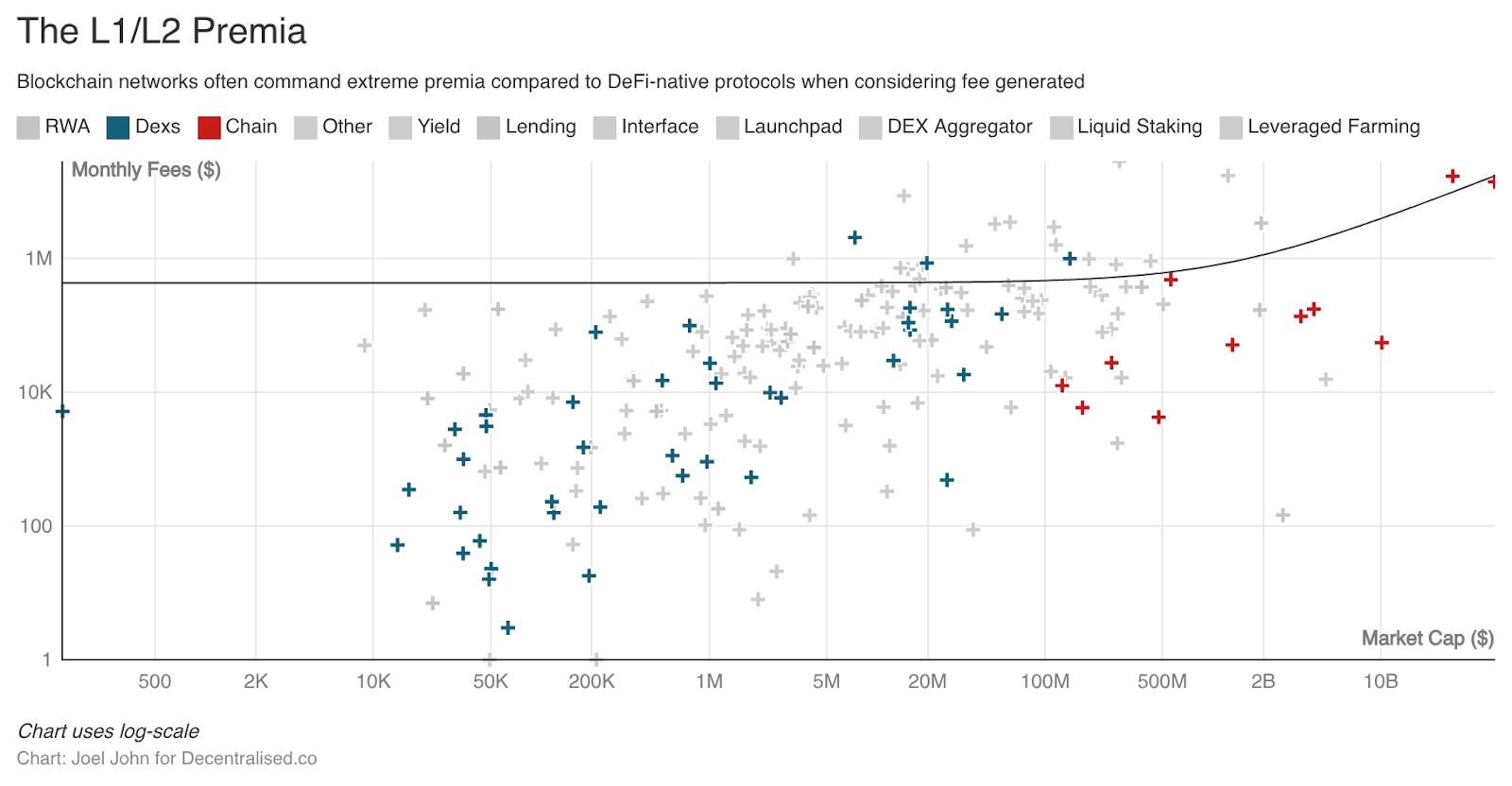

Historically, L1 and L2 have always traded at extremely high premiums compared to independent underlying facilities or projects. If that premium had been well invested, it could have created new economic systems. It could have funded developers to build truly meaningful applications for ordinary people outside the industry. However, the open-source nature of products and the ease of tokenization have led to the presence of fifty identical product copies across thirty networks, thus damaging composability.

That's fine, as we have cross-chain bridges, cross-chain messaging, and numerous other capital transfer mechanisms. Yet the value of all these mechanisms continues to decline.

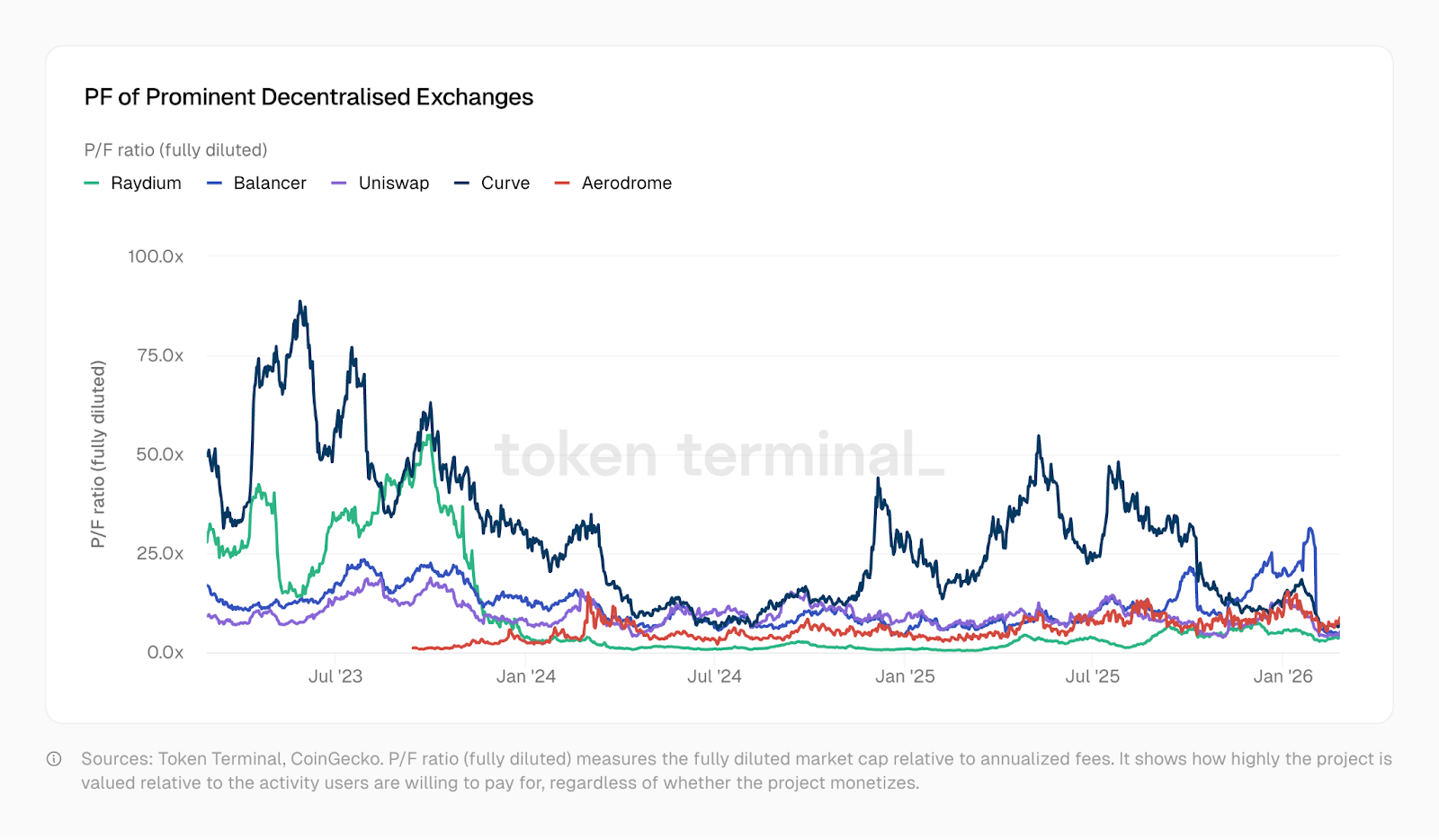

Take the fate of DeFi foundational projects as an example. Overcrowding of options for investors and lack of novelty have led to a plummet in valuations, even though these foundational projects indeed drove more economic activity. These markets are highly fragmented, and investors have numerous options to bet on. The novelty of “decentralization” or “blockchain-based” has long since faded. Projects like Kamino, Euler, Fluid, Meteora, and PumpSwap have emerged, but their price-to-fee ratios are all below the levels of protocols in 2022. As shown in the TokenTerminal chart below, DEX price-to-fee multiples have significantly decreased between 2023 and 2025. Some exchanges' price-to-fee multiples are now even as low as 1.

In other words, the market valuations of these protocols are lower than the fees they are expected to generate over the next year. A strange paradox has emerged: even though the valuations of underlying protocols (whether DeFi or L1 itself) are declining, applications built upon these protocols are generating higher revenues in shorter timeframes.

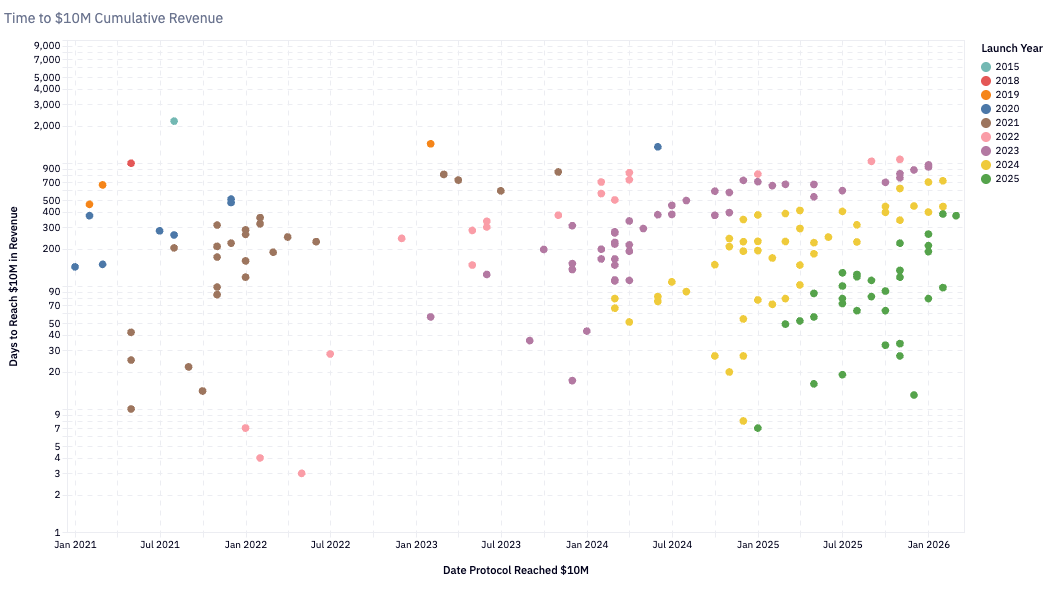

Since early 2020, the number of teams generating over a million dollars in revenue each quarter has steadily increased, surpassing a hundred. In 2020, protocols that took 24 months to reach $10 million in annual revenue were considered rapidly growing. By 2024, the time for protocols to reach this milestone has shortened to about six months. Pump.Fun launched in early 2024 and reached $10 million in revenue in just about two months, setting a record for the fastest growth.

This accelerated growth reflects not only the maturity of underlying infrastructures (faster chains, lower transaction costs) but also the constant expansion of on-chain capital pools (seeking yields and entertainment). If you are a developer or founder, consider the following facts:

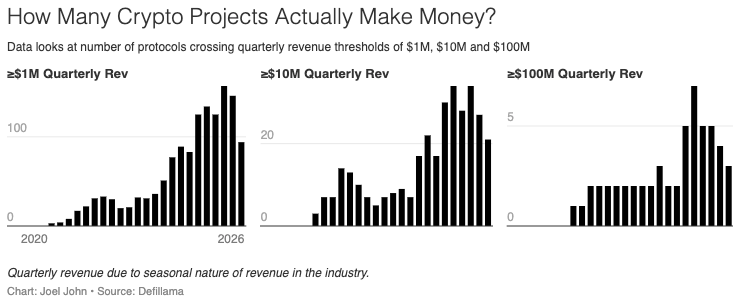

Today's crypto market has nearly 900 protocols generating revenue.

Each protocol is competing for a declining median share of revenue, but from a broader trend, there are more and more teams generating revenue. For reference, the number of protocols generating revenue has increased nearly 8 times, from 116 to 889.

The median monthly revenue has fallen to $13,000.

Blockchain-native enterprises possess three forms of moats. When examining their revenue models, each becomes apparent.

First-mover advantage: Tether and Circle's network effects gained from early advantages are hard to replicate. Although new players continually emerge, they have gone through multiple cycles and established a dual oligopoly position. As it stands, these entities have not yet been tokenized and are heavily financialized. Tether is a centralized entity whose revenue primarily comes from US Treasury bills.

Liquidity moat: In industries historically oriented towards utilitarianism, Aave has managed to maintain liquidity depth across cycles. Hyperliquid seems to have achieved this as well, but it is too early to conclude. These protocols are incentivized to return funds to liquidity providers and align token adjustments towards governance functions.

Distribution moat: Cyclical applications (such as meme coin trading platforms) rely on the velocity of capital turnover and consumer demand. Web3 games and NFTs are excellent examples. AI-powered productivity means that lean small teams can launch consumer-facing products faster now. Where does the advantage come from? Ultimately, it's about guiding and retaining the most users during market peaks.

Products built upon distribution moats may be highly valuable, but they are exceptions rather than the rule. Traditionally, a startup's value comes from its experiences being replicable. Y Combinator's success partly stems from the "Lindy effect" of past successful ideas. However, the pace of cryptocurrency development is too rapid to replicate these experiences based on the Lindy effect, which partly explains why few founders successfully replicate their consumer goods expertise in other areas. Factors that initially helped businesses scale may not be replicable.

This does not mean that founders should not seize these opportunities. Segments such as data providers for prediction markets or proxy economic products may generate substantial cash flow in the short term. But it's crucial to understand that these are all high-volatility, short-term games that may not endure. The pitfall these products face is blindly raising venture capital or being trapped by tokens issued long after the initial "meta (core narrative)" that gave life to that product faded away.

So, what really gives tokenized businesses value? Are their valuations rational?

Data may provide some clues.

Questioning Governance

In 1999, many tech companies had price-to-sales (P/S) ratios of 10 to 20 times. Content delivery network company Akamai even had a P/S ratio of 7434 times. By 2004, Akamai's P/S ratio fell to 8 times. Many companies saw their P/S ratios plummet from 30 to 50 times to below 10 times. The bursting of the internet bubble evaporated trillions in speculative value. However, many companies ultimately survived because their underlying businesses were real. Amazon's stock price dropped 94% from the peak of the internet bubble but eventually became one of the most valuable companies in history.

The crypto industry is experiencing a similar shrinking of market capitalization, and at a faster pace. In 2020, when DeFi was still experimental, the total annual revenue generated by the crypto industry was only about $21 million. At that time, the average P/S ratio of all tracked protocols was as high as 40400 times. The market was then speculating entirely on the future: "What might cryptocurrency be?" By 2021, as the "DeFi summer" arrived, protocol revenue transformed into actual earnings, and the P/S ratio plummeted to 338 times. Now, with annualized revenue hitting $18 billion, the P/S ratio is about 170 times. The P/S ratio compressed from 40400 times to 170 times in just five years.

However, there is a problem. When Visa's P/S ratio is 18 times, shareholders can receive dividends and buybacks. They have legal rights to the company's earnings and enjoy governance seats under securities law. But when Aave's P/S ratio is 4 times, token holders have governance rights but until recently, they had no direct economic rights. Hyperliquid utilized its support fund for buybacks, making HYPE holders the closest existence to equity holders in the DeFi space. Aave approved a $50 million annual buyback plan in 2025.

Do you think I can turn these terrible charts into art?

These initiatives are significant, but they are merely exceptions. In the broader market, most protocols lack mechanisms to return value to token holders. These P/S ratios appear low, and the rights of holders are weaker than those in traditional markets. These multiples have become possible because the crypto industry creates revenue at a scale and efficiency unmatched by traditional business.

Those protocols pulling down cryptocurrency P/S ratios aren’t large organizations with thousands of employees. They are small teams running global financial infrastructures with marginal costs close to zero and no physical offices. How thin can these costs get? How much trust can holders have in the reasonable use of protocol income by these teams?

Segmenting by track can give a clearer picture of market conditions. Aave, the largest lending protocol in DeFi, has a P/S ratio of about 4 times. Hyperliquid controls about 80% of the decentralized perpetual futures market, with a P/S ratio of about 7 times. These are not bubble ratios. They can be said to even be lower than those of the closest traditional financial counterparts. The only publicly traded large crypto exchange, Coinbase, has a P/S ratio of about 9 times. The Chicago Mercantile Exchange (CME Group) is the largest derivatives exchange globally, with a P/S ratio of about 16 times. Visa, as a payment infrastructure, has a P/S ratio of about 15 times.

Crypto analyst Will Clemente mentioned in a podcast that cryptocurrency is the purest form of capitalism. No successful enterprise in any industry can achieve a per capita profit estimated at up to $100 million, as is the case with Tether. For perspective, Nvidia's per capita revenue is $5.2 million, Apple's $2.4 million, and Google's $2 million. Tether has 125 employees and an annual revenue of about $12.5 billion, indicating the highest per capita profit in corporate history.

Although the overall figure of a 170 times P/S ratio seems crazy, the market is not irrational regarding protocols that genuinely generate revenue. Its pricing is equal to or lower than traditional financial infrastructures.

This raises the next question: what use do tokens really have? In many areas, tokens are powerful tools for concentrating capital and striving towards a common vision. Cryptocurrency is at a stage where entrenched dual oligopolies have become the norm. Traditionally, founders had to go into debt (using equity as collateral) or raise funds to inject capital into financial products. Hyperliquid, Uniswap, Jupiter, and Blur have all proven that with token incentives, people will invest capital in new products. If tokens come with governance rights, those contributing can make larger inputs. In this regard, tokens may evolve two functions:

To coordinate capital and resources from the right crowd;

To grant them the power to govern the protocol.

Tokens no longer hold inherent value; even stocks are being tokenized now. These tools must have claims over economic activities and the ability to guide governance. Many Layer1 and Layer2 tokens struggle to achieve both. Teams and VCs often hold the majority of the tokens, leaving retail holders in disarray. This means ordinary investors have no reason to care about newly listed digital assets.

Today, these attempts show a trend towards differentiation. MetaDAO allows holders to receive full refunds when teams make false statements. No large protocols have adopted this model yet. The core issue in cryptocurrency is that traditional tokens provide very few rights to holders. Nowadays, various protocols are trying to answer a long-standing question: why should people hold these assets? Future articles will explore the relationship between holder rights and valuations.

At the Crossroads

Over the past two decades, the intertwining of capital markets has grown increasingly tight. This is largely due to technological advances. We can trade commodities, overseas indices, digital assets, and soon even computational resources (GPUs). Blockchain makes trading in these markets possible globally, anytime and anywhere. The Nasdaq and New York Stock Exchange are now moving towards an around-the-clock trading model, demonstrating how technology changes eras.

We live in a highly financialized world; ironically, news of wars makes us rush to find the best prediction markets to bet on.

For founders, this means rethinking the products they build and how they build them. If this article’s data can explain anything, it is that all blockchain products will eventually achieve profitability through two core principles.

By extracting a small commission from high-frequency trading, or

By extracting large fees in transactions focused on verifiability and trust assumptions.

The advantage lies either in transaction speed or in verifiable transparency.

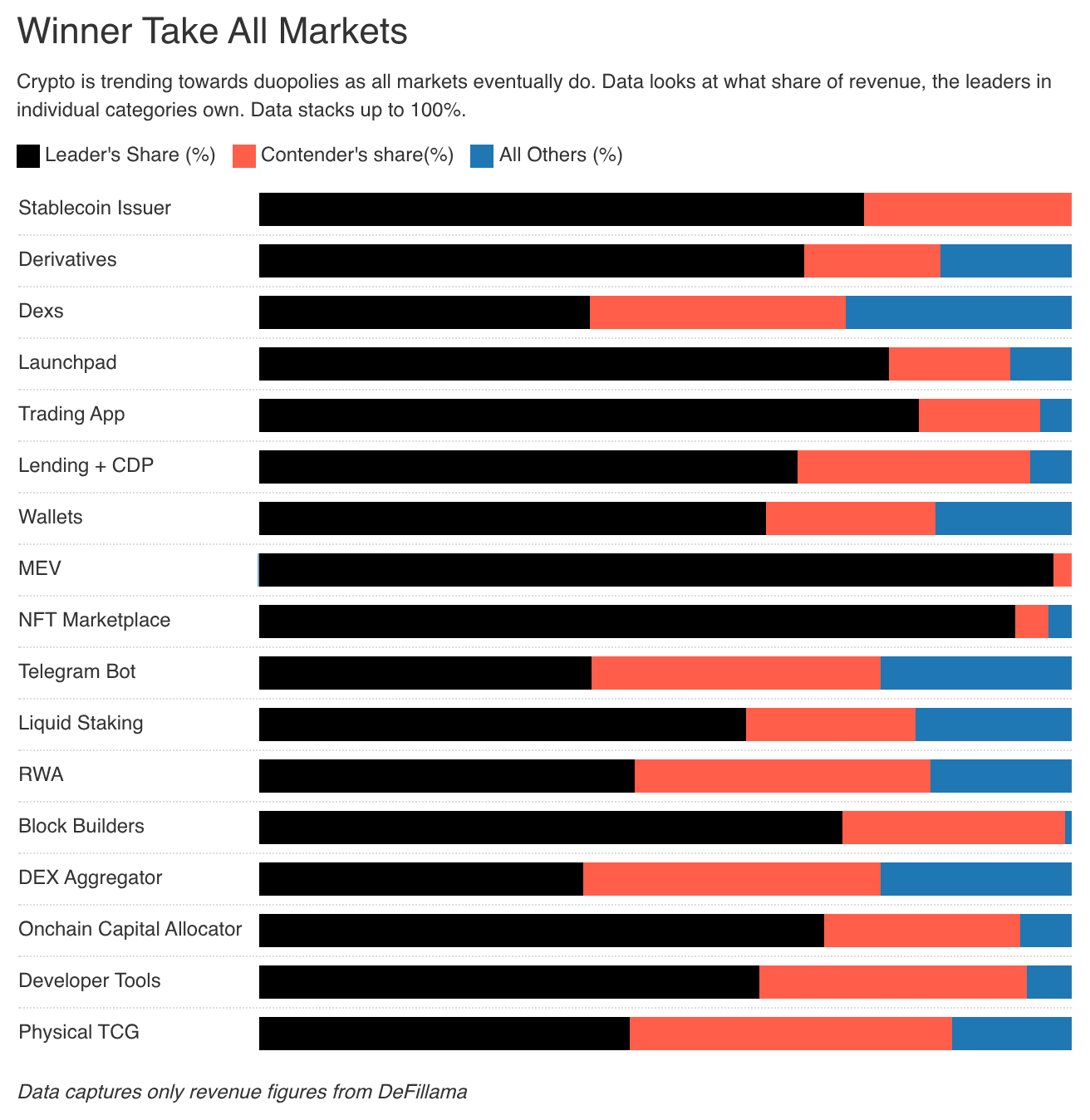

Profit motive is the purest driving force for participants in capital markets. It is generally believed that markets will ultimately move toward extreme efficiency. We see manifestations of this trend in industry leaders. For example, the charts we observe show that 70% of shares in multiple market segments are held by two key companies. This is a harsh reality that we all have to face and a brutal aspect of market operations. For founders, it means that the funds that once flowed to their tokens are now being redistributed to assets with higher volatility or higher capital returns.

Long-term capital does exist and may even pay premiums, but only if it recognizes the value of the underlying businesses. Investors in Google and Amazon do not need to rush to exit because their underlying businesses are valuable in themselves.

In an era where the value of even software is being questioned, blockchain-native applications will have to find new ways to demonstrate value. We can reorganize tokens. Perhaps we can even have startup equity traded on-chain. But this is not solely a token issue but also a business model issue. The vast majority of long-tail blockchain applications, such as Web3 social, identity, and gaming products, struggle to scale and fail to create meaningful differentiation from traditional competitors. These experiments are not without value, but we struggle to effectively monetize them.

The era of building cryptocurrency infrastructure is over. In the future, it will merge with the internet. At that point, there will be no more discussions of "online" business; you will exist within the internet itself. No one will call themselves a "mobile application developer"; you will simply be a developer.

Long live the age of blockchain enthusiasts! We are merely advocates of ledger maximization, pondering how best to utilize these ledgers.

Related Reading: 36 Years, 4 Wars, 1 Script: How Capital Prices the World in Conflict?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。