Written by: Nishil Jain

Translated by: Block unicorn

Preface

Historically, finance has developed alongside the networks that carry it.

The trading routes of Rome gave birth to the insurance industry, allowing merchants to expand their businesses across geographic boundaries. Colonial shipping created a demand for remittances and foreign exchange. The advent of the internet required new payment channels to drive the booming growth of e-commerce.

The internet also established a model for open network operations.

However, these networks require a trust infrastructure to operate. SWIFT is effective because of how the banking network reconciles transactions without actually transferring funds. The value of the New York Stock Exchange lies in its ability to frequently sort trade orders and maintain the integrity of transactions. In all these cases, the value of the network lies in ensuring that trust is conveyed frictionlessly with every transaction. A financial network lacking intrinsic trust will ultimately decay.

However, the cost of maintaining this trust has always been a bottleneck. Each layer of verification—auditors, fund administrators, custodians, compliance officers—adds costs, time, and an additional layer of licensing. In traditional asset management, for example, the reliance on human auditing means staffing increases as the assets under management (AUM) grow.

Blockchain significantly reduces costs. In a blockchain network, anyone can continuously verify transactions, asset positions, and liabilities at nearly zero marginal costs. You don’t need a fund administrator to verify asset allocations quarterly—all information is on-chain and visible in real time. You also don't need a custodian to hold assets—the smart contract itself serves as the custodian.

When you can verify the capital deployment situation and how returns are generated without relying on a fund administrator or quarterly reports, you can build investment structures that are difficult to operate in a closed environment.

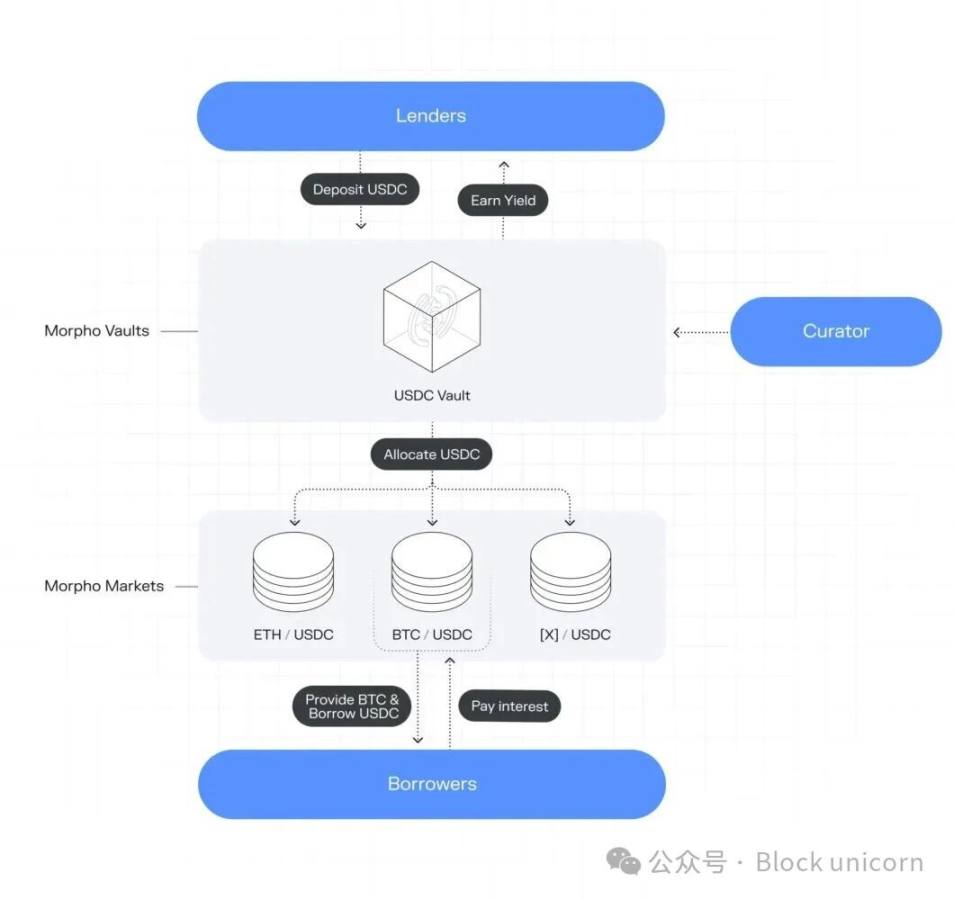

One of the most eye-catching structures is vaults—custodial funds fully executed through smart contracts. The core function of a vault is to pool funds and programmatically allocate them to various yield sources in decentralized finance (DeFi), continuously returning accumulated interest to depositors.

Vaults have existed in some form since 2020. What has changed in the past 18 months is the infrastructure built around vaults.

Protocols like Morpho now operate as open platforms—any asset management firm can build strategies on them, any risk management company can manage vaults, and any exchange or wallet can distribute them to users.

This openness allows specialized participants to independently access the same infrastructure, each showcasing their strengths. This ultimately formed a composable, verifiable financial network, attracting substantial capital.

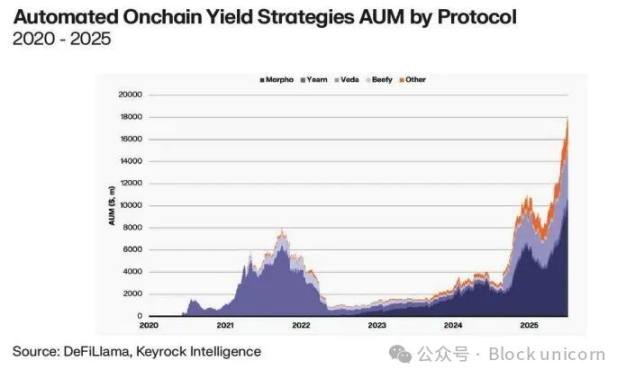

In just the past year, more than $6 billion flowed into on-chain vaults. In comparison, tokenized government bonds—undoubtedly the heavyweight product in the on-chain yield asset category—grew from $3.3 billion to $6.96 billion during the same period. In terms of growth rate, on-chain vaults have actually begun to rival the most mature asset classes in the institutional digital finance space.

Specifically regarding the two main vault platforms, Morpho and Spark, their assets under management (AUM) have skyrocketed from $2.46 billion to $7.64 billion today.

If we broaden our view to encompass the entire ecosystem of automated yield strategies, accounting lending, liquid staking, and hybrid approaches, the total assets under management currently hover around $17.5 billion, significantly surpassing the historic high of 2021.

How Vaults Reached This Stage

Essentially, the core operation of a vault is similar to that of a mutual fund. Investors deposit funds (usually stablecoins) and receive a receipt token that shows their share of the funds. The managers then allocate these funds to various DeFi lending markets according to specific strategies. As the funds generate interest, the yields are returned to depositors. It’s that simple.

But the difference between a vault and a conventional custodial account lies in how you can use the receipt token. It is not just stored in your wallet.

With the ERC-4626 standard, this token can interface with other DeFi applications. It can serve as collateral for loans on the Aave platform, pair with liquidity pools on the Curve platform, or be used to create more advanced yield strategies. ERC-4626 allows for the output of one financial product to easily be translated into the input of another financial product.

Composable nature is certainly one of the reasons we see such large-scale growth today, but the underlying product stack also plays a crucial role in making the construction and distribution of vaults possible.

As early as the DeFi summer of 2020, Yearn Finance first proposed the concept of automated yield. They proved that a fund-like structure could completely operate on-chain. Users do not need to manually transfer funds among Aave, Compound, or Uniswap to chase the highest yield; Yearn vaults encode these strategies within smart contracts to programmatically reallocate funds.

However, Yearn simultaneously acted as both the infrastructure provider and strategy operator—from the foundational smart contracts to fund allocation to user distribution, all aspects were handled by one entity. As the market expanded, this singular model gradually revealed its limitations. Risk management, software engineering, and user distribution require fundamentally different skill sets. Bundling them into one entity instead created bottlenecks and concentrated risks.

To scale securely, today’s vault ecosystem has split into three distinct tiers. When infrastructure builders, risk managers, and retail platforms operate independently, each tier can focus on its area of expertise without being hindered by other tiers.

We can disaggregate financial services because the underlying blockchain system is transparent and programmable.

In traditional financial systems, ensuring that professionals in different fields (like managers and recorders) perform their tasks entails expensive legal contracts, strict regulations, and continuous audits. But on the blockchain, smart contracts can automatically enforce rules, and anyone can immediately verify the outcomes.

Because code takes on the role of "trust," coordinating different experts becomes much easier. This is why the vault stack can support five intermediaries in the chain without incurring excessive overall expenses, thereby ensuring the product's economic viability.

The protocol layer provides the infrastructure for smart contracts. Morpho dominates in this area, with an AUM of approximately $9.6 billion.

With its completely non-permissioned design, Morpho is more of a neutral infrastructure rather than a single product. It attracts numerous strategies. Apollo Global Management, which holds $940 billion in traditional assets, understands the importance of Morpho in empowering on-chain strategies. Therefore, the firm acquired 9% of Morpho's token supply, indicating that institutional capital recognizes the underlying value.

The curation layer is where strategy and risk management reside. Curators are akin to general partners (GP) in on-chain finance. They define the authorization scope of the vault, select eligible assets, set risk limits, and manage daily asset reallocations.

They establish buffer mechanisms by setting loan-to-value (LTV) ratios to guard against market fluctuations and set a threshold where the system will automatically liquidate when negative assets occur, thereby protecting the interests of depositors. To prevent the vault from growing larger than its underlying asset liquidity, custodians will also impose strict supply limits.

Furthermore, they design algorithmic interest rate curves based on the capital situation within the pool. When lending demand surges and liquidity tightens, smart contracts automatically increase capital costs, thereby naturally reducing system leverage and attracting new deposits. This helps simplify underlying complexities and provides stable and predictable yields for both institutional and retail users.

By separating from the protocol layer, custodial institutions are forced to compete on performance. The annual percentage yield (APY) of custodial Morpho vaults consistently hovers around twice that of the current conventional lending market, as managers actively allocate funds rather than allowing them to sit idle in pools.

Today, an increasing number of professional curators are competing to attract deposits on these platforms.

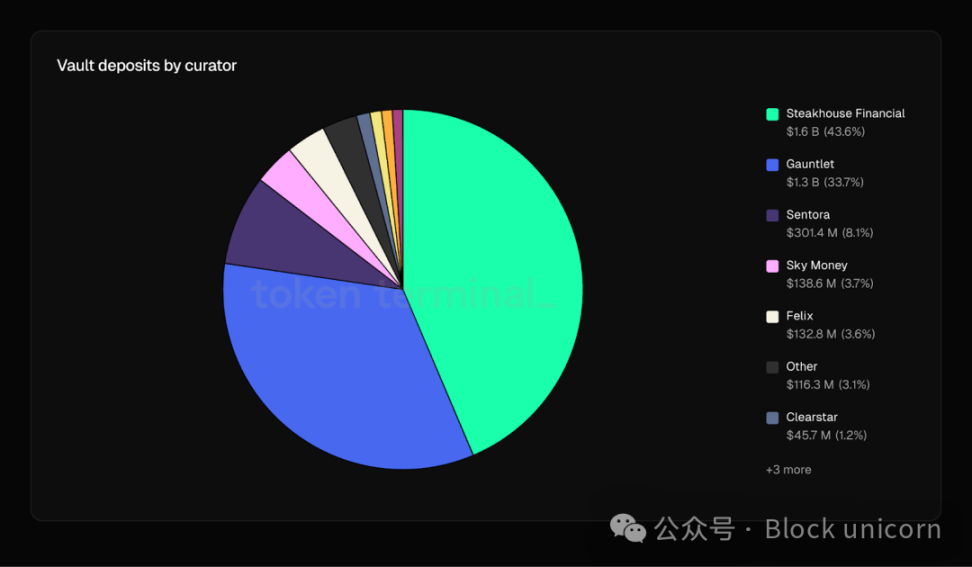

Steakhouse Financial is the largest custodial institution on the Morpho platform, managing over 50 vaults for six major restaurant chains, with total deposits of around $1.5 billion, and is also the first custodial entity to manage over $2 billion in total assets on the protocol. Gauntlet operates more than 70 vaults, managing approximately $1.37 billion in assets.

Steakhouse achieved this with a team of fewer than 20 people. This was made possible because the underlying network shifted the validation requirement to the blockchain, while the system's openness allowed the protocol to rely on companies like Coinbase for distribution and on firms like Morpho for code enforcement.

Recently, Bitwise joined the Morpho platform as a curator—this move is significant not for the initial capital it brings but for the insights it provides to the entire technology stack. Bitwise is an off-chain asset management firm managing $15 billion, with existing distribution channels aimed at institutions. By becoming a curator, Bitwise can penetrate the entire vault technology stack, leveraging its own capital relationships and compliance credentials to derive value at both the custodial and distribution levels.

The distribution layer is the part that transforms this complex system into consumer products. Platforms with large user bases like Coinbase, Crypto.com, and Gemini now route user deposits directly into these well-managed vaults.

Coinbase users depositing USDC into the basic “earn” product are, in fact, unknowingly interacting with DeFi infrastructure. The front end features a sleek fintech interface while a decentralized infrastructure runs in the back end.

These seemingly simple applications hide a vastly complex flow of funds.

Assuming a retail user on Crypto.com deposits dollars into a yield product. These dollars flow into the Morpho vault operated by Grove Finance. Grove, in turn, holds tokenized AAA CLO funds worth $712 million, which were on-chain by Centrifuge and managed by the traditional giant Janus Henderson. The end-user earns 4.82% on their stablecoins but is completely unaware that their returns come from a credit fund on Wall Street.

Each intermediary in this chain adds a specific and necessary layer of specialization.

Centrifuge is responsible for wrapping traditional credit funds into tokens recognizable by DeFi protocols and handling the associated legal and technical work. Grove Finance offers risk frameworks and capital allocation strategies to determine the risk exposure taken on specific instruments. Morpho provides borrowing infrastructure, including smart contracts, market parameters, and vault architecture. Crypto.com is responsible for distribution, compliance, and user interface.

This is a clear example of how financial complexity can scale on an open network through composable specialized intermediaries instead of a single entity attempting to do it all.

Sources of Demand

This three-tier unbundled structure explains how vaults operate today. But how did the $6 billion influx of capital occur last year?

Let’s first take a look at who is allocating the funds.

Data shows that among these vault participants, 63% are retail users with account balances under $10,000. Notably, these retail users account for only 6 basis points of the actual funds. The real money comes from whales and institutional investors—addresses with deposits exceeding $100,000—accounting for 99.2% of the funds in automated yield strategies.

These participants include crypto-native funds, DAO vaults, and family offices. Depositing funds into vaults provides them with a way to store large cash reserves without needing to manage them personally, all while keeping risks manageable.

The main driver pushing institutional capital into the space is the massive expansion of stablecoins and their increasing acceptance as savings tools—thus generating passive income.

During 2025, the supply of stablecoins will grow from about $200 billion to $300 billion. Crucially, regulatory initiatives like the “GENIUS Act” are accelerating this growth, while also presenting a unique challenge. Under these new frameworks, stablecoin issuers are legally prohibited from directly paying interest to token holders. As native stablecoins cannot generate any yield by law, this $300 billion of stablecoins is forced to seek returns through alternatives like lending protocols.

Vaults have become the default parking spots for these idle funds, which is why over 90% of the assets under management (AUM) in Morpho and Spark vaults are stablecoins.

Moreover, in terms of pure yield, automated on-chain yield strategies have consistently outperformed. Today, their average gross annualized yield (APY) is 7.95%, whereas traditional short-term fixed income and money market fund annualized yields are only 4.67%.

We have enough capital seeking yields, and we have attractive annual yields to draw them in; what’s needed next is a distribution method to reach those looking for yields but who won’t directly interact with DeFi protocols.

This is indeed a barrier. A survey report by Ernst & Young indicates that 62% of institutional investors prefer to obtain cryptocurrency investment opportunities through registered instruments rather than directly on-chain buying assets. Currently, only 24% of surveyed investors have participated in DeFi. The demand for yield remains, but they lack the willingness to navigate wallets, smart contracts, and paying gas fees.

In retail, another report by Ernst & Young found that 51% of non-DeFi investors cited lack of expertise as the main reason for their non-engagement.

The distribution layer solves this issue by wrapping vault infrastructure in interfaces familiar to users. For these users, the “earn” button on Coinbase routes funds into the backend Morpho vault, thus completely removing barriers.

Coinbase routes USDC deposits through a specially crafted Morpho vault by Steakhouse (located on the Base platform)—this Steakhouse currently manages over $1.5 billion in deposits. Crypto.com, Gemini, Bitget, Ledger, and Trust Wallet have also built similar integration solutions. For institutions unable to hold assets in self-custody wallets or directly interact with smart contracts, depositing through Coinbase means that the necessary compliance, KYC, and custodial requirements are handled by Coinbase at the interface level. They gain vault yields without having to deal with the complexities of a vault.

For traditional asset management companies, this creates a distribution channel for a global audience, with compliance burdens managed by the platform rather than the protocol.

Hindering Factors

While the numbers are compelling, the risks are equally undeniable.

Smart contract vulnerabilities remain the most direct threat to the entire ecosystem, and the past record serves as a stark warning.

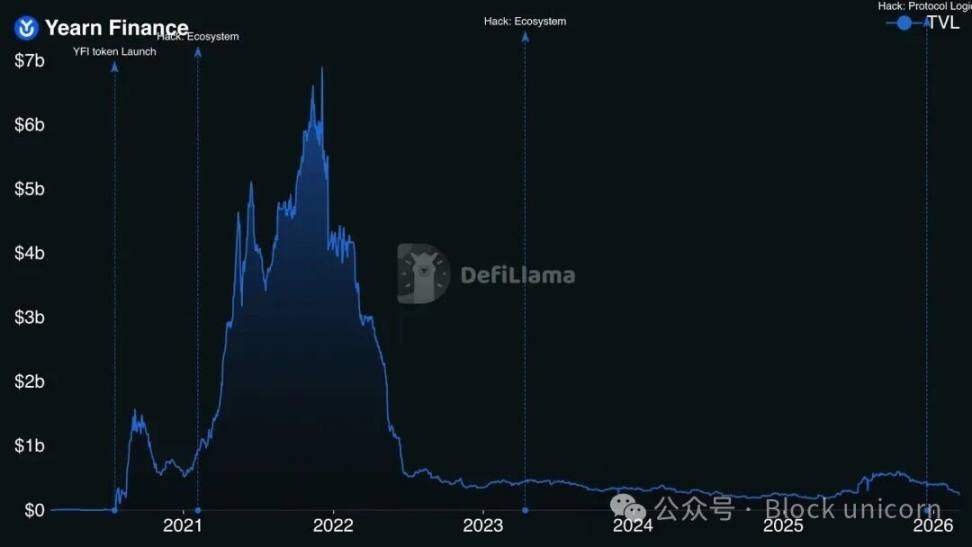

Consider the severity of these losses: In 2021, Yearn lost $11 million due to flash loan manipulation. By the end of 2025, it lost another $9 million due to an infinite minting bug. The market responded accordingly, and the protocol’s total locked value (TVL) has now fallen to $250 million, far below its historical peak of $6.3 billion.

In 2023, Euler also faced a similar fate, where a missing “health check” in the Euler Finance code allowed hackers to steal $197 million from four different asset pools in just 15 minutes.

The shocking commonality among these events is that almost all the exploited code had undergone thorough audits by top security firms like OpenZeppelin and Trail of Bits. While auditing is necessary, it is far from sufficient.

Because vaults are composable, integrating each new protocol creates new attack vectors. The industry has been addressing this challenge by building robust security measures, such as using time locks to delay sudden parameter changes; utilizing real-time monitoring tools like Hypernative to detect abnormal traffic; establishing automatic circuit breakers; and adopting decentralized veto mechanisms that allow depositors to block suspicious actions.

While these mitigation measures are meaningful, they cannot guarantee absolute safety. Vulnerabilities in the protocol layer can destroy an entire vault in seconds, no matter how prudently the curators allocate funds.

In addition to the intrinsic security risks of code, there is another fundamental difference in how actual financial products operate compared to traditional fixed income products.

DeFi vaults charge significantly higher fees—around 1.50%—whereas Vanguard money market fund fees can be as low as 0.08%.

However, this gap largely reflects a difference in scale; a smart contract worth $70 million cannot defray operational costs like a Wall Street giant with a market cap of $360 billion. Even accounting for these higher fees, on-chain asset allocators still yield about 186 basis points higher than traditional finance (6.45% vs 4.59%).

But as past vulnerabilities have shown, the extra yield is not a free excess return; it comes with existent risks. This is precisely the market-priced premium for bearing technical risks. There are no Federal Deposit Insurance Corporation (FDIC) insurances on deposits in this chain, no government guarantees, and no ultimate lenders. Asset allocators demand higher returns to compensate for the real risks that losses in their positions could stem from oracle failures or smart contract vulnerabilities.

This structural premium remains highly attractive for crypto-native funds, DAO funds, and traditional institutions with appropriate risk tolerances.

How these contradictions are resolved will determine the future trajectory. But the structural advantages of vaults—also the reason they are developing faster than any previous on-chain financial product—lie in the cost of trust.

Traditional asset management methods sustain trust between participants by adding costs. Each layer of cost ultimately gets passed down to investor returns. Yet based on verifiable mechanisms, the ledger itself can provide this layer of trust—continuous, permissionless, and with marginal costs close to zero.

This is why Steakhouse can manage $1.5 billion in assets with 20 people, why five intermediaries can form a yield chain without paying excessive fees, and why Coinbase can offer vault-supported yield products to 100 million users without building proprietary fund infrastructure.

Risks do exist, and regulatory issues remain unresolved. But the trust economics on a verifiable network are structurally different. If this cost advantage can be sustained, then the $17.5 billion investment might just be the initial input.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。