Author: Yuan Chuan Investment Review

The recent market trends of South Korean stocks are comparable to a "ten-ring roller coaster" of Changlong.

At the end of February, the conflict between the US and Iran broke out, and global stock markets withstood the first trading day on March 2 under the anticipation of "Chuan Chuan Rapid Passage to Iran." However, the South Korean stock market was closed for the entire day due to a holiday.

When it reopened on March 3, the expectation of a "quick resolution" in the Middle East had completely reversed, and the blockade of the Strait of Hormuz led to chaos in the global oil and gas market, with the KOSPI index, which was hot since the beginning of 2026, plummeting into a relentless decline.

On March 3, the KOSPI index once fell to a circuit breaker, eventually dropping over 7%. The next day, it continued to fall to a circuit breaker, closing with a daily drop of 12.06%, the largest drop ever recorded.

On the night of March 4, the South Korean Financial Commission announced the immediate injection of 100 trillion won (approximately 68 billion USD) into a financial market stabilization fund to rescue the market, and the next day the KOSPI violently rebounded by 9.63%.

However, the volatility did not stop. This week, South Korean stocks continued to swing dramatically as if experiencing bipolar disorder, falling nearly 5.96% on Monday and then rising by 5.35% on Tuesday, still losing money in between, teaching all investors expecting a violent rebound a lesson in "volatility decay" from the fundamentals of investment.

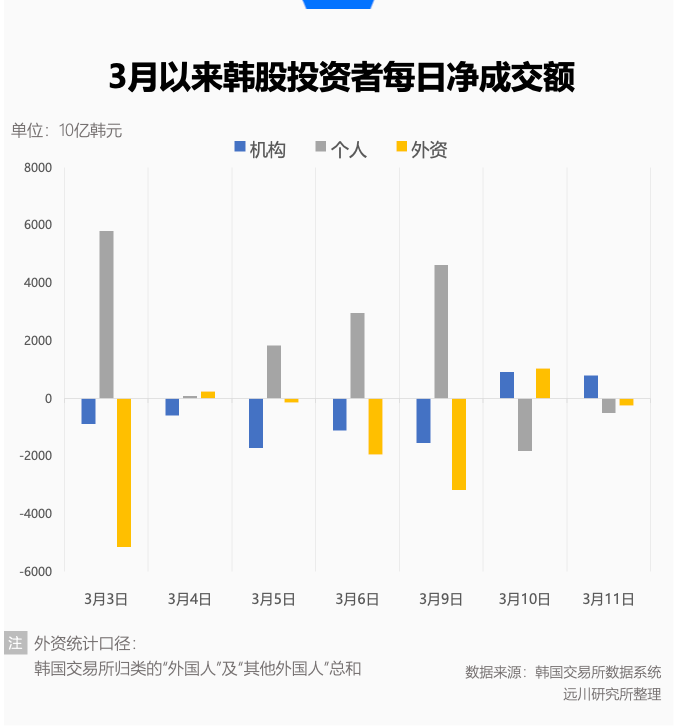

Meanwhile, statistics from the Korean Exchange revealed an interesting phenomenon. Since March, local retail investors in South Korea have been net buyers, while foreign capital has been net sellers, reminiscent of the phenomenon during the pandemic storm of 2020, where greater volatility led to more fear among foreign investors and more stubbornness among retail investors.

Before the recent wild fluctuations, the South Korean stock market welcomed an unprecedented rising cycle, with the KOSPI rising over 160% from 2025 to the end of February this year, making it the MVP of the global market. In this so-called "bull market," the KOSPI doubled from 3000 to 6000 points in a time frame even shorter than the historically fastest record of the NASDAQ.

This astonishing explosiveness and the extreme volatility during the crisis together form the complex face of South Korean stocks.

The Night Before the Black Swan

The curve intuitively shows that the rise of South Korean stocks actually began after the tariff war bottomed out in April last year.

At that time, the global market trembled under Trump's last round of tariff TACO trading, and the KOSPI began to climb out of the pit after a cumulative drop of over 7% at the beginning of April. Even with a brief correction in November, it was viewed by the fervent market sentiment as a signal of "picking up passengers."

The resurgence of the Korean market became unstoppable after the beginning of 2026, with the KOSPI nearly completing a year's KPI in just January, and although volatility increased in February, the rise was still accelerating.

On the first trading day of February, the KOSPI corrected by 5.26%, the largest drawdown during this round of rise, but at that time the external environment was relatively stable; this "stress test" was quickly rectified with subsequent upward fluctuations. On February 25, the KOSPI first stood above the 6000 points, and on the last trading day of February, it hit an intraday high of 6347.41 points, followed by a correction, with a total decline of 1%.

The rapid rise is not without reason, which aligns well with the fundamental principle of higher concentration and greater elasticity.

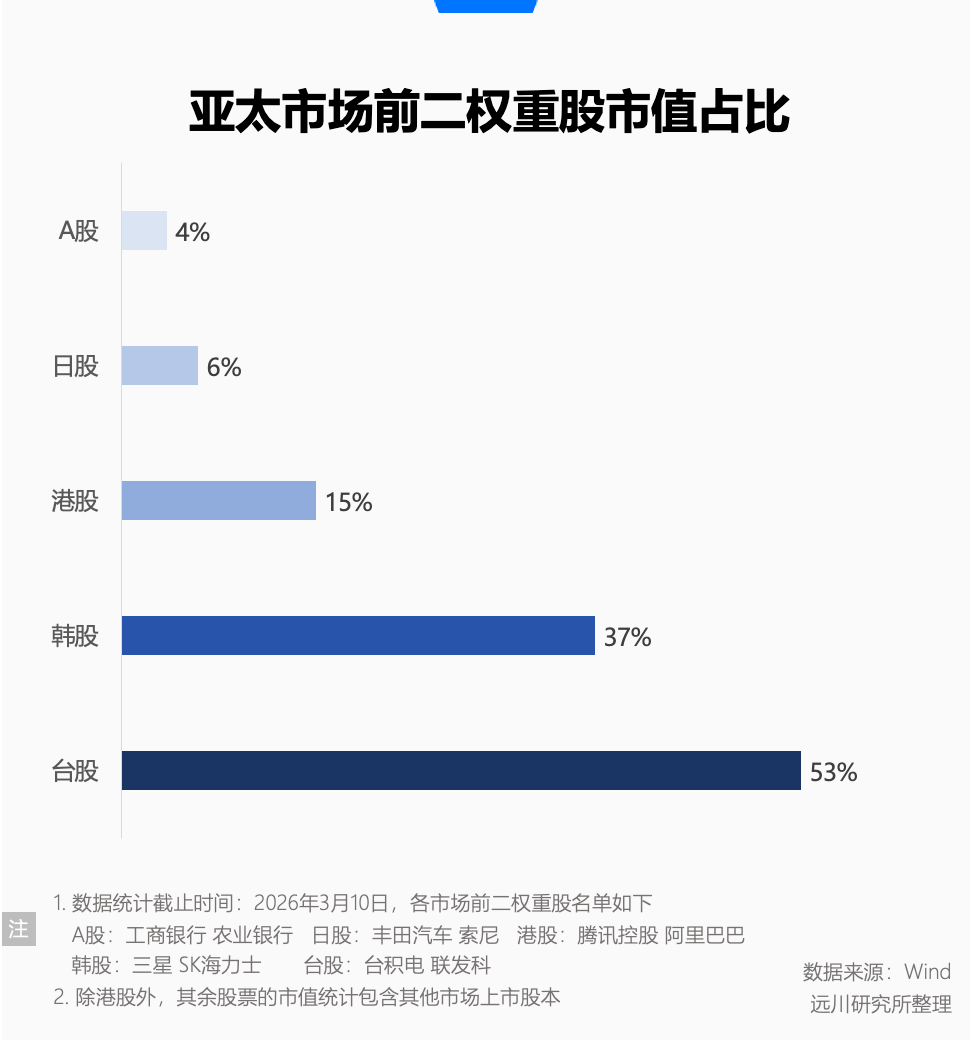

From the perspective of index composition, although the KOSPI is officially called the Korea Composite Stock Price Index, it is essentially a highly concentrated "track gambler," with the combined market capitalization of the two storage chip giants, Samsung and SK Hynix, accounting for one-third of the South Korean stock market; the rise of the KOSPI is almost entirely reliant on these two core heavyweight stocks.

Before March, the KOSPI was a highly pure AI mapping; as long as there was a shortage of chips while simultaneously ramping up Capex, Samsung and SK Hynix were as if they held the new oil of the AI era.

Whether it was the continuously surging demand for high-end products HBM (high bandwidth memory) required for producing AI large models, or the shrinking supply faced by DRAM/NAND needed for traditional consumer electronics as capacity was consumed, both turned storage into the most popular wealth key of 2026.

From the end of 2025 to the beginning of 2026, Samsung and Hynix's main external work was announcing price hikes—DRAM/NAND contract prices were significantly raised for three consecutive quarters from Q3 2025; while HBM4, still in the mass production ramp-up phase, was a more thorough seller’s market, with 2026's production capacity already completely divided among AI giants, leaving money only able to wait in line for 2027's allocation.

However, when the whole world discovered that the troubled Gulf would cut off the stable supply of real oil, the grand narrative of the future was quickly overshadowed by the immediate energy supply crisis. Especially for South Korea, which is heavily dependent on Middle Eastern oil and gas resources, it went overnight from a "king of AI mapping" FOMO narrative to the HALO anxiety of a "victim of high oil prices."

In the first two trading days of March, Samsung and Hynix plunged around 10% for two consecutive days.

In fact, before this round of "black swan," there was already a divergence between local funding and foreign capital in South Korea. In February, the average daily trading volume of South Korean stocks reached 32.23 trillion won (approximately 149.2 billion RMB), up 19% MoM, with both the index and trading volume hitting historical highs.

From the perspective of technical analysis enthusiasts, breaking out to new highs with increased volume is a classic "mutual X" signal.

Since May last year, foreign capital has generally maintained a net buying trend in the South Korean stock market, but started to cash out in large quantities after the KOSPI reached 6000 points. The net selling of foreign capital in February also hit a historical high, amounting to 21.1 trillion won (approximately 9.98 billion RMB). On the very day of February 27, when the KOSPI refreshed its historical high, foreign capital net sold 7 trillion won (approximately 32.4 billion RMB).

However, these profit-taking funds likely did not expect that the structurally imbalanced South Korean stock market would pay such a heavy price due to the "epic fury" and "real commitment" from far away in the Middle East.

Self-Rescue of a Specialized Student

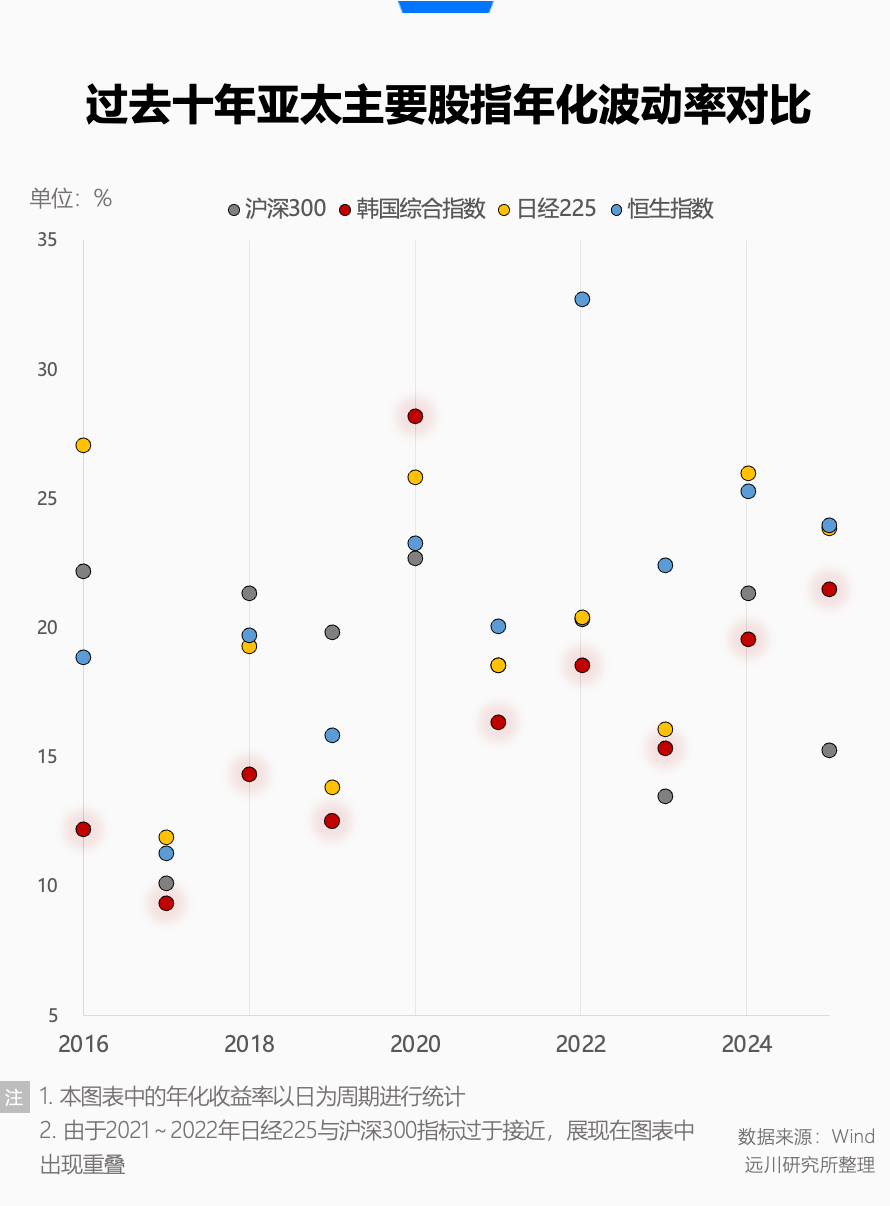

Such wild fluctuations prompt the question, what is the historical volatility of South Korean stocks?

In fact, in the past decade among the four major Asia-Pacific stock indices (CSI 300, Hang Seng Index, Nikkei 225, and Korea Composite Index), the annualized volatility of the CSI 300 is 18.12%, the KOSPI is 18.90%, while the Nikkei 225 ranks second with 20.50%. The Hang Seng Index leads with a volatility of 21.79%, which is not surprising.

Before 2025, the KOSPI only experienced one significant volatility event in 2020, when the storyline mirrored that of March this year—South Korean stocks were smashed to low points by a large foreign capital sell-off, while local retail investors came in to buy the dip, pulling the market back up.

Along with South Korea's years of low volatility has been the awkward "Korea Discount."

Over the past decade, the overall price-to-book ratio of the South Korean stock market has long hovered around 1x, occasionally rising slightly but eventually returning to low levels, until it reached a high of 2x in February this year after a vigorous rise last year.

Even though it is said that the overall attractiveness of the South Korean stock market is limited, with the market willing to pay only for Samsung and Hynix, the overall price-to-book ratio of the Taiwanese stock market, which is also an "index of semiconductor stocks," usually hovers around 2.4.

The "Korea Discount" can also be understood as a collective negative review from global investors regarding the South Korean stock market; the issue is not just that the index is too specialized, but also that the governance models of large listed companies do not meet the aesthetic standards of contemporary investors.

Whether it is Samsung or SK, both are typical family-run chaebol companies in South Korea, with opaque governance practices. Many times they choose to suppress stock prices, avoid high inheritance and dividend taxes, or use their cash reserves for blind diversification. All of this has led South Korean stocks to be famous for being "stingy" towards minority shareholders.

The last three South Korean presidents have also made tackling the "Korea Discount" one of their agenda items during their tenure.

Former President Moon Jae-in encouraged institutional investors like the National Pension Service (NPS) to actively participate in corporate governance, attempting to address the long-standing issue of low valuations at its root by limiting chaebols' cross-holding and enhancing minority shareholder rights.

Former President Yoon Suk-yeol introduced the "Corporate Value Enhancement Plan," attempting to revitalize the market through tax cuts, encouraging voluntary disclosure, and dividend distributions. However, he left office due to political upheaval in April 2025, with the "Korean Special Valuation" effectively fizzling out.

In June 2025, current President Lee Jae-myung took office. During his campaign, he called for drastic reforms in the capital market, with one of his campaign slogans being to elevate the KOSPI to 5000 points.

As a former retail investor (in loss), Lee Jae-myung has always been haunted by the unfair transactions of large shareholders, which magnified ordinary investors' losses.

After taking office, he vigorously promoted a series of reform measures, including but not limited to: forcing the cancellation of treasury shares used by chaebol families to maintain control; strengthening accountability in the board of directors; reforming the dividend tax to encourage listed companies to distribute dividends; and promoting the relocation of residents' wealth, delineating a shift for the South Korean public to allocate assets from overly high real estate speculation to more financial assets.

Lee Jae-myung likes to emphasize in public that he was once a retail investor and claims that when his political career ends, he will return his energy to stock market trading.

Whether due to top-level design needs or personal experiential preferences, Lee Jae-myung’s enthusiastic commitment to reforming the South Korean stock market confirmed that he fulfilled his campaign promise of the index reaching 5000 points. In reality, even considering the significant fluctuations in the last two weeks, the KOSPI has risen over 100% during his tenure of less than a year.

Before the Gulf crisis arrived, Lee Jae-myung's stock market reforms received considerable attention, with Bloomberg specifically publishing an article titled “How the Korean President is Making the Korean Stock Market the Best in the World,” stating that this bull market made Lee Jae-myung a hero in the eyes of 14 million retail investors in Korea.

Of course, this article was published on February 22, 2026, when ships were still passing through the Strait of Hormuz normally, investors were still debating the future of AI around Citrini's article "2028 Smart Crisis," and oil prices were still at peace at over 60 dollars.

Epilogue

If Lee Jae-myung's stock market reforms aim to address the issues of "rules" and "distribution," trying to fix the long-term low valuation problem, then the war in the Middle East has instantaneously destroyed the profit expectations that serve as the denominator, pulling the market's attention abruptly from long-term dividends and governance back to short-term inflation and survival.

This feeling of tearing exposes a harsh reality: the reform bull is actually built on a relatively stable global macro assumption. Once the timeline of the Gulf conflict extends, it directly strikes against South Korea's weaknesses as a resource-poor export country, where the economic structure is overly concentrated in a few industries.

In an open market, regardless of whether the "live water" flowing in was due to industrial advantages or reform expectations, it can reverse and flow out during a crisis. Especially when global risk aversion erupts, and foreign capital holds large profit chips, systematically reducing holdings of the most increased and liquid assets is also an instinct for institutional arbitrage.

To some extent, this is a volatility that a highly open market cannot avoid, and it is also a new issue of expectation management.

If you don't believe it, just look at the neighboring Hong Kong stock market, with a relatively rich industrial structure and more progressive corporate governance, but when treated as an "ATM," it also drops without holding back.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。