Written by: FinTax

1 Introduction

On February 26, 2026, Consensys' crypto wallet MetaMask announced a partnership with one of the world's leading card organizations, Mastercard, to launch the "self-custodied" crypto payment card—MetaMask Card—in the United States. Users can make daily purchases in the real world at over 150 million merchants that support Mastercard. During the payment process, users retain control over their on-chain assets without needing to pre-custody funds in centralized exchange accounts, while also earning cashback rewards in the form of MetaMask's stablecoin, mUSD.

The launch of MetaMask Card has garnered significant attention in the crypto payment sector. However, it is not the first product in the realm of crypto debit cards under the category of crypto payment cards. Previously, several cryptocurrency exchanges like Coinbase and Binance had launched crypto debit cards that could complete transactions using Visa for everyday purchases. In contrast, what innovations does the MetaMask Card have, and what impact will it have on the crypto payment market? This article will provide a comprehensive overview of the market waves generated by the MetaMask Card by examining its product features and comparing it with mainstream crypto payment methods and similar products.

Figure 1 MetaMask and Mastercard Collaboration Landscape

2 Analyzing MetaMask Card: How Does "Self-Custody" Relate to Everyday Spending?

2.1 The Product Logic of MetaMask Card

From the perspective of product design, MetaMask Card is not the first crypto payment card on the market, but unlike most custodial crypto cards that require users to pre-transfer assets to centralized platform accounts, users retain control over their wallet assets before payments occur, and authorization and settlement are completed through regulated infrastructure during payments. The core of this product is not to make merchants on-chain recipients, but to allow users to use crypto assets that have been committed to the card's spending functionality for real-world payments within traditional card networks. In other words, the merchant side still sees a familiar card payment process, while the user side gains a stronger sense of control compared to traditional custodial crypto debit cards.

According to official materials, this product currently has at least four notable features:

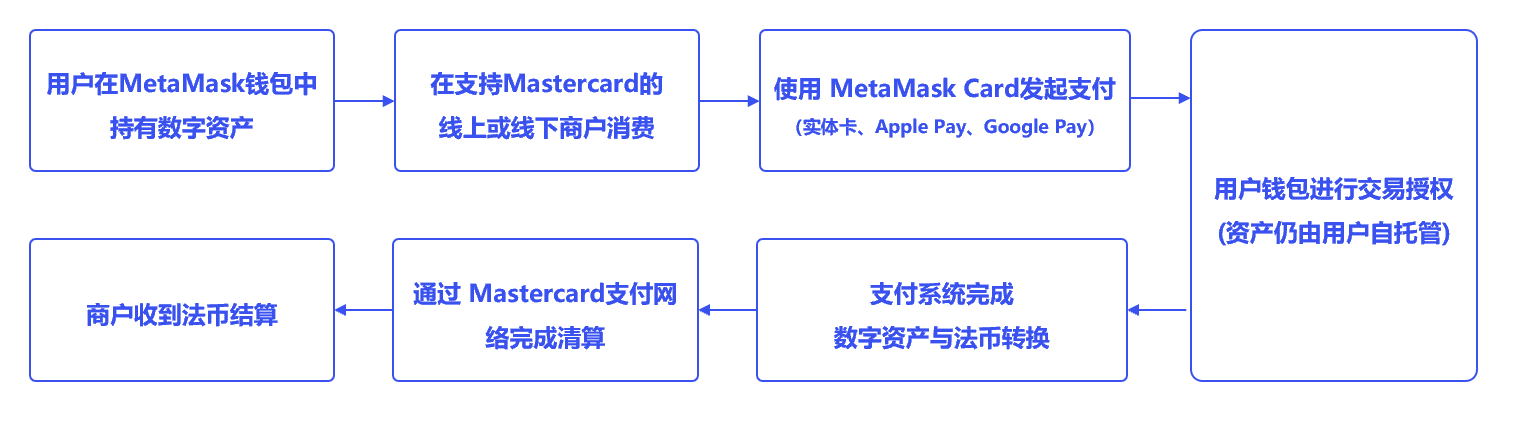

First, self-custody: As mentioned, users retain control over their crypto assets before payments, without needing to pre-load funds into a centralized exchange account.

Second, cashback mechanism: Each purchase can earn rewards on-chain—standard card purchases can earn up to 1% cashback in mUSD, while physical cardholders can earn up to 3% cashback in mUSD for the first $10,000 in yearly spending.

Third, global payment network coverage: Leveraging Mastercard's global payment system, this card can be used for everyday spending at over 150 million online or offline merchants worldwide, covering all spending scenarios such as supermarkets, dining, travel, and e-commerce, and it is compatible with mainstream mobile payment methods like ApplePay and GooglePay.

Fourth, near-instant usage: Cardholders can quickly add cards to mobile wallets and start spending online, in-app, and offline after approval.

Figure 2 User Payment Process with MetaMask Card

2.2 Comparison of MetaMask Card with Other Crypto Payment Methods

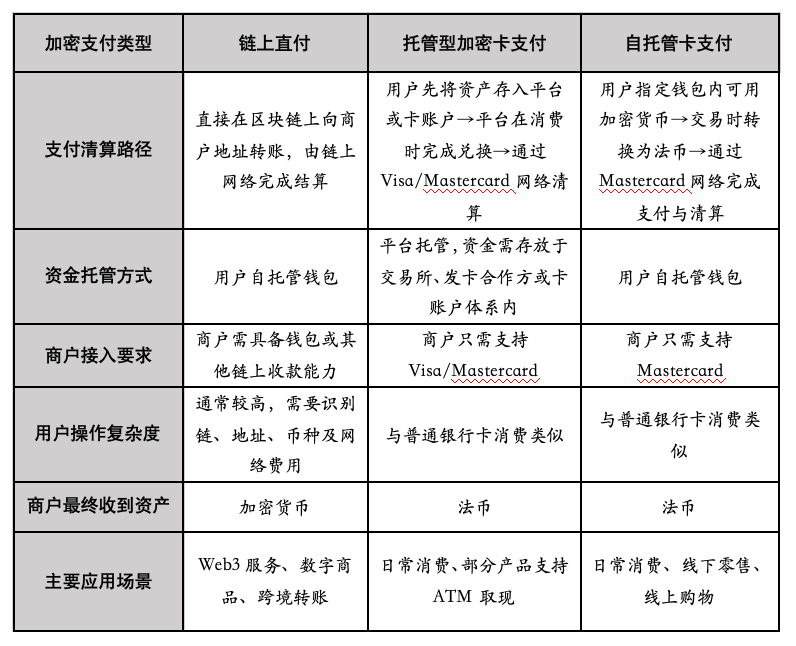

Cryptocurrency payment refers to transactions conducted using cryptocurrencies like Bitcoin, Ethereum, or USDT instead of fiat currency. If we roughly categorize existing crypto payment methods, we can see at least three approaches: the first is on-chain direct payments, where users transfer crypto assets directly to merchant addresses; the second is custodial crypto payment cards, where users deposit assets into a platform, which then clears fiat currency through networks like Visa and Mastercard; and the third is a model where self-custody wallets connect to card organization networks. In terms of user experience, the third type of product attempts to combine the self-custody attributes while offering users a payment experience closer to everyday bank cards. This model not only reflects the further integration of crypto payment tools into real-world consumption scenarios but also indicates that Web3 wallets are gradually becoming an important entry point for users to manage digital assets, reflecting the industry's trend from exchange-centric models towards wallet ecosystems.

Table 1 Comparison of MetaMask Card with Other Mainstream Crypto Payment Methods

3 The Background of the MetaMask Card Launch: Why Now?

In recent years, the rise of PayFi (Payment Finance) has driven the integration of crypto payment from mere on-chain value transfer to real-world consumption, forming a powerful combination with stablecoins and existing on-chain payment tools, showcasing advantages in speed and cost in areas like cross-border remittances and instant settlements, thus becoming an important bridge connecting crypto assets with real payment systems. In this context, the MetaMask Card, focusing on self-custody wallet real-world payments, has at least four driving factors for its pilot and promotion:

First, product-level piloting and feasibility verification have been completed. According to MetaMask, after the initial pilot of the card at ETHDenver in 2025, it has accumulated real usage experience from multiple markets, with tens of thousands of users globally using it for various scenarios from daily coffee to large purchases. Its official launch covering the entire U.S. indicates that its initial piloting, product refinement, and compliance integration have reached a stage suitable for scalable replication.

Second, market demand and product logic are gradually maturing. Unlike traditional custodial crypto payment cards, the "self-custody wallet" model of the MetaMask Card allows users to retain control over their wallet assets before payments while completing authorization and payment through a regulated issuer and the Mastercard network during the consumption phase. This design essentially seeks to find a balance between on-chain asset control and real-world payment convenience, addressing crypto users’ long-standing demand of wanting "neither to revert completely to centralized custody nor give up the experience close to everyday bank cards."

Third, the external payment infrastructure and regulatory environment have significantly changed from before. On one hand, the U.S. has made its regulatory framework for stablecoins and banks participating in crypto-related activities much clearer within the past year: the GENIUS Act establishes a federal regulatory framework for payment stablecoins and brings issuers under the scope of the Bank Secrecy Act; the FDIC has also clarified in 2025 that institutions it regulates can engage in permissible crypto-related activities under controlled risk conditions. For market participants, the clarity on the regulatory front seemingly increases compliance burdens, but actually reduces many uncertainties in market operations, delineating compliance boundaries for various commercial activities.

Finally, as a leading decentralized crypto wallet globally, MetaMask needs to achieve offline utility of wallet assets, linking the Web3 ecosystem with real-world consumption; as a traditional payment giant, Mastercard can expand its ecological boundaries by entering the crypto payment space and capture the payment market dividends from crypto assets, making their collaboration a "mutual benefit" in the industry.

4 How MetaMask Card Affects the Crypto Payment Landscape

4.1 On the Convenience Level: From "Technical Tool" to "Everyday Payment"

If the crypto payment industry continues to linger in the "high support, low usage" bottleneck, it will become increasingly difficult to integrate into the mainstream payment landscape. A GoMining 2026 survey shows that nearly 80% of crypto asset holders support the widespread adoption of crypto payments, yet only 12% use it for everyday consumption. The emergence of MetaMask Card strengthens a trend: crypto payment products aimed at real-world consumption scenarios are increasingly inclined to combine on-chain asset entry with regulated payment infrastructure, reducing barriers to use and learning costs, driving crypto payments from "exclusive use" to "common option," and continually expanding the user market. Aside from Mastercard, Visa also announced on March 3 this year its plans to collaborate with Bridge to expand stablecoin-linked cards to over 100 countries, indicating that card network giants are actively promoting similar directions.

4.2 On the Security Level: New Ideas for Risk Control from Self-Custody Models

In terms of security design, previous crypto payments have often adopted a centralized custody model, concentrating the primary responsibility for asset security on the platform side, which has buried risks such as platform moral hazards and funding chain breaks. The security design of the MetaMask Card, centered on self-custody, allows users to have control over their digital assets, fundamentally reducing the inherent risks of centralized custodianship and pushing the industry to pay more attention to the distribution of security responsibilities, leading to an innovative path that combines platform custodianship with user self-management. Additionally, for various types of assets, the platform has set differential conversion fee rates that reflect the volatility risk costs of different assets in the fees, allowing users to incur costs for higher-risk payment scenarios, where "security" manifests as a perceivable control factor, guiding the industry towards establishing a payment pricing logic that matches risk and cost.

4.3 On the Compliance Level: Reconnecting Payment Innovations with Regulatory Frameworks

The compliance logic of the MetaMask Card lies in embedding traditional financial compliance requirements into the crypto asset payment process, ensuring user identity traceability through KYC and AML measures, and guiding current crypto payment projects that are innovating payment formats to meet basic regulatory requirements. In the future, competition in crypto payments will not just be a debate over technology or fees but also a contest of compliance ecosystems. The evolution of the compliance landscape will encourage other crypto payment projects to reassess their compliance structures, whether seeking similar collaborations or increasing technological investments to meet international standards such as the FATF's "Travel Rule." However, while MetaMask provides a compliance template for the industry, this model will still face long-term challenges amid tightening regulations that increase compliance costs, necessitating a finer balance between global compliance and localized operations.

5 Conclusion

The MetaMask Card is not the starting point for crypto payment cards, but it does present a new case worth observing: as self-custody wallets evolve from mere storage and signing tools to connecting real consumption scenarios through regulated issuers and card organization networks, the focus of crypto payments will shift from "whether payments can be made" to "how to redistribute the boundaries between control, usability, and compliance." This may very well be the true reason to pay attention to this card.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。