Written by: David Christopher

Translated by: Saoirse, Foresight News

BlackRock's iShares Staked Ethereum Trust Exchange-Traded Fund (ETHB) officially listed on the Nasdaq on March 12. This is the first Ethereum staking fund launched by BlackRock, quietly addressing the core issue that has lingered over the institutional development narrative of Ethereum since the launch of the Ethereum spot ETF.

This means that for the first time, Wall Street can engage with Ethereum in its touted true form — viewing it as a productive asset capable of generating stable income.

Core Product Launch: Filling the Institutional Investment Gap

The highly anticipated Staked Ethereum ETF is now live. This fund deeply integrates Ethereum spot exposure with staking rewards, providing institutional investors with an unprecedented compliant channel.

From its inception, the Ethereum spot ETF has suffered from a fatal product mismatch.

For a long time, Ethereum has been positioned as a "native Internet bond" for institutional promotion — it possesses scarcity (annual issuance cap of only 1.5%), income-generating capability (annual compound yield of about 3%-5%), and is deeply embedded in the settlement layer of the new financial system composed of stablecoins and tokenized assets.

Even if this concept seems a bit "avant-garde," it has still gained market recognition. However, the actual products launched have failed to match this vision.

After the spot ETF was listed, the core element of "income" was completely missing. Investors could only gain exposure to price fluctuations, completely unable to touch the economic engine of Ethereum. What we pitched to institutions was an income-generating asset, but what was delivered was a revenue-less shell.

Bitcoin does not face this issue. Its value proposition is centered on "value storage," with a simple and direct logic: holding the spot means receiving all the value. But Ethereum's logic is entirely different, staking is an inseparable part of its asset attributes and is the fundamental way holders benefit from the network economy and gain compound returns. The spot ETF cannot provide this functionality.

This is not the only reason, but it is undoubtedly a key factor leading to the serious lag in institutional capital inflows into Ethereum. BlackRock's Bitcoin spot ETF (IBIT) currently manages over $55 billion, while the Ethereum spot ETF (ETHA) is only about $6.5 billion. Certainly, Bitcoin’s first-mover advantage and simpler narrative are part of the reason, but the product's inherent flaws are the core issue. Institutions received the narrative of Ethereum's price increase but ended up with a neutered asset.

Wall Street Has Already Entered, Infrastructure Value Recognized

The poor performance on the asset side has obscured the rapid growth of Ethereum in institutional adoption since the launch of the spot ETF in July 2024.

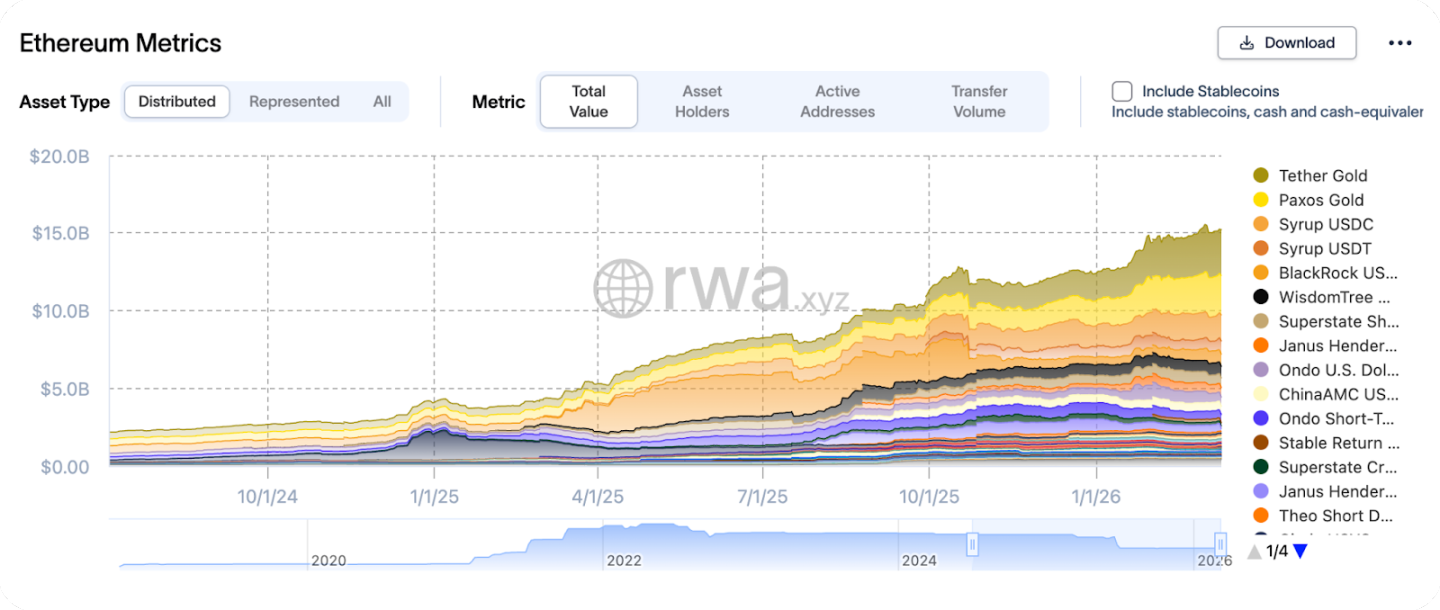

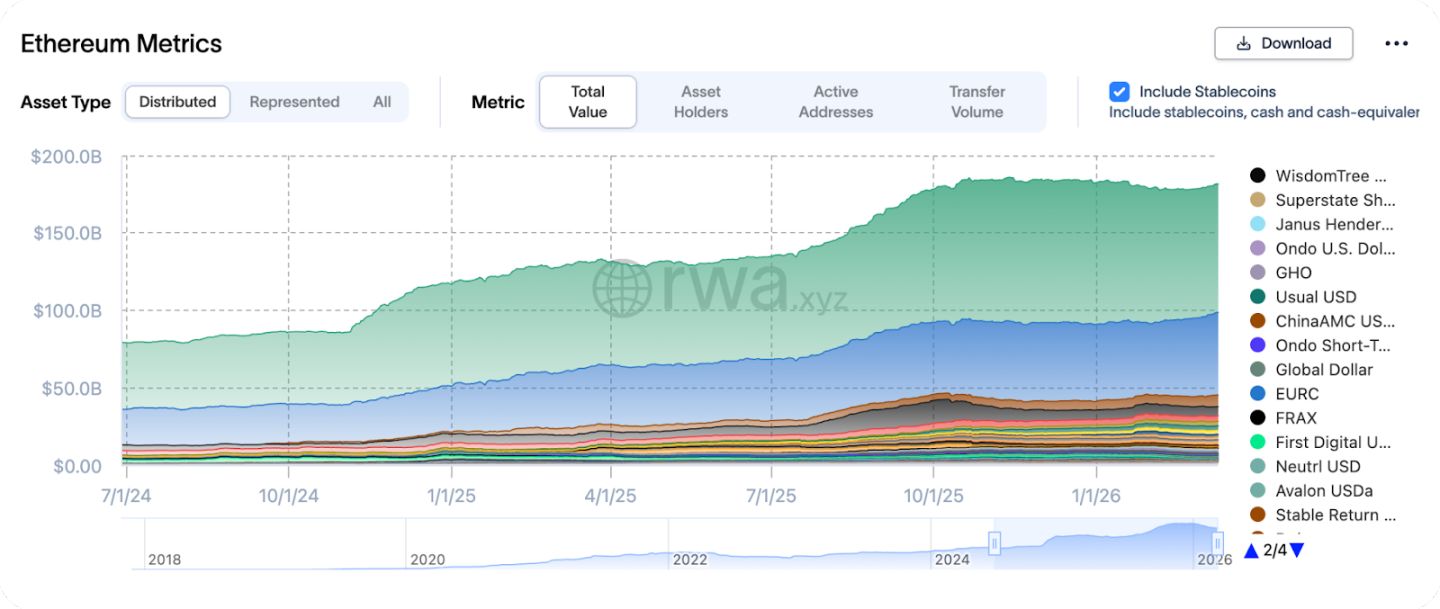

During this period, the supply of RWAs on Ethereum has increased about 7 times, and the supply of stablecoins has doubled. Wall Street is increasingly viewing Ethereum as infrastructure - the operating track for stablecoins and tokenized finance, rather than a mere trading asset.

Growth of RWAs on Ethereum since July 2024

BlackRock's BUIDL Fund, Franklin Templeton's FOBXX Money Market Fund, and the increasing number of tokenized products are all settling on Ethereum or its Layer 2 (L2) networks. Major banks are testing on-chain settlement capabilities, including SWIFT. Despite the unsatisfactory inflow of ETF funds, Ethereum's institutional landscape is indeed continuing to expand.

The essence of the problem is that while institutions can hold exposure to Ethereum’s price, they cannot compliantly participate in the Ethereum network economy, which they increasingly rely on. The emergence of ETHB has completely addressed this pain point.

Growth of stablecoins on Ethereum since July 2024

Structural Impact: Redefining Institutional Investment Logic

This impact extends far beyond the ETHB product itself.

Prior to this, institutions that are not native to crypto could only obtain income-generating Ethereum exposure through workaround structures like Digital Asset Trusts (DAT). While these structures could participate in staking, re-staking, and the DeFi ecosystem, the value of the fund had no direct correlation to the underlying assets.

The existence of such structures stems from institutional regulatory restrictions that prevent direct participation in staking. With the launch of the staking ETF, the rationale for this intermediary path has been significantly weakened. Funds that previously had to flow through intermediary channels to workaround structures are poised to flow directly back to Ethereum's native assets.

Market Valuation and Fundamentals: Value in a Deep Valley

At the time of ETHB's launch, Ethereum's current valuation is in a reasonable to deeply undervalued range based on several cycle indicators.

Its MVRV (Market Value / Realized Value) metric is below 1, indicating that the market is overall in a state of unrealized loss; the profitable supply is lower than during the crash period of 2022; this cycle's price has not breached the historical high of 2021 and is stuck in previous box ranges, which offers excellent compressibility of price from a historical perspective.

Of course, the poor performance is also due to factors related to Ethereum's own development. The roadmap for Layer 2 networks (L2) prioritizes scale and user experience over Layer 1 fee capture. Blob data block technology has significantly reduced the anchoring costs of Rollups (Layer 2 scaling solutions), and diminished the scale of fee burning that once supported deflationary narratives, making investment logic harder to model.

However, it is worth noting that Ethereum’s monetary system has not been harmed. Its annual issuance is about 0.8%, which is roughly on par with Bitcoin's inflation rate. Now, all factors are beginning to reassemble: institutional demand is accelerating, the ecosystem applications like RWA, stablecoins, and tokenized funds are steadily growing on Ethereum, staking yield channels have finally been opened, and prices are situated in a value trough.

Future Outlook: Wall Street's Value Litmus Test

For many years, Ethereum has been selling itself to institutions as a "yield-generating reserve asset" and the settlement layer of the tokenized economy. This narrative has been continuously polished, formalized, and emphasized — it is now presented to those institutions that have long recognized the network value but could not participate in the Ethereum economic proposition.

Now, the product design finally aligns perfectly with the value proposition. The market performance of ETHB will be a key litmus test to determine whether Wall Street truly recognizes the asset value of Ethereum.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。