Written by: Yangz, Techub News

If last week Bitcoin breaking through the $70,000 mark was still like "the early warmth of spring," then today's rise to $76,000 seems like "the scent of spring becoming strong." The continuous 8 bullish candlesticks on the K-line chart seem to be swallowing the market's concerns one by one.

This surge came suddenly, but it is not without signs. Against the backdrop of the Middle East conflict not yet fully subsided, Bitcoin this time neither avoided risks like the traditional theory of "digital gold" nor completely followed the fluctuations of risk assets. By sorting out recent contexts, it can be found that the core driving force of this market trend is gradually shifting from purely macro emotional gambits to two more specific variables: the expectation gambit under geopolitical changes and the ongoing "DAT" buying power from enterprises.

Bitcoin's Unique Rhythm Amidst the Middle East Conflict

Since the conflict erupted on February 28, the Israel-Palestine war has entered its third week. According to past logic, such a level of geopolitical conflict should push up gold and suppress risk assets. However, this time, Bitcoin has found its own rhythm. After initially following the decline of the U.S. stock market, Bitcoin began to repair independently. One possible explanation is that the market's pricing logic for this conflict has changed.

If the market was initially worried about the conflict spiraling out of control and even escalating into a full-scale war, then after the Trump administration issued a "hope for negotiation" signal last week, funds began to reassess the situation. Of course, Trump is still the same Trump.

According to CCTV News's latest reports, two senior White House officials stated that Iran has recently attempted to contact the Trump administration through various channels, hoping to reopen diplomatic negotiations, but Trump currently refuses to resume talks and wishes to continue military operations. Additionally, Iranian Foreign Minister Amir-Abdollahian denied recent contact with Whittaker, stating on social media that his last contact with Whittaker occurred before the new U.S. military operations against Iran. White House officials also indicated that some U.S. allies in the Middle East had proposed to assist in promoting negotiations, but this has also been temporarily rejected by the U.S.

This fluctuating attitude has been interpreted by the market as an alternative "controllable signal"—both sides are drawing red lines, but also leaving back doors open. The Iranian foreign minister, while denying recent contact, specifically emphasized that the last contact occurred "before the U.S. launched new military actions"; Trump publicly states that negotiations will not occur, but previously also expressed that "there are virtually no targets left to strike." In other words, what the market is trading is no longer "the war itself," but "the war will not escalate indefinitely."

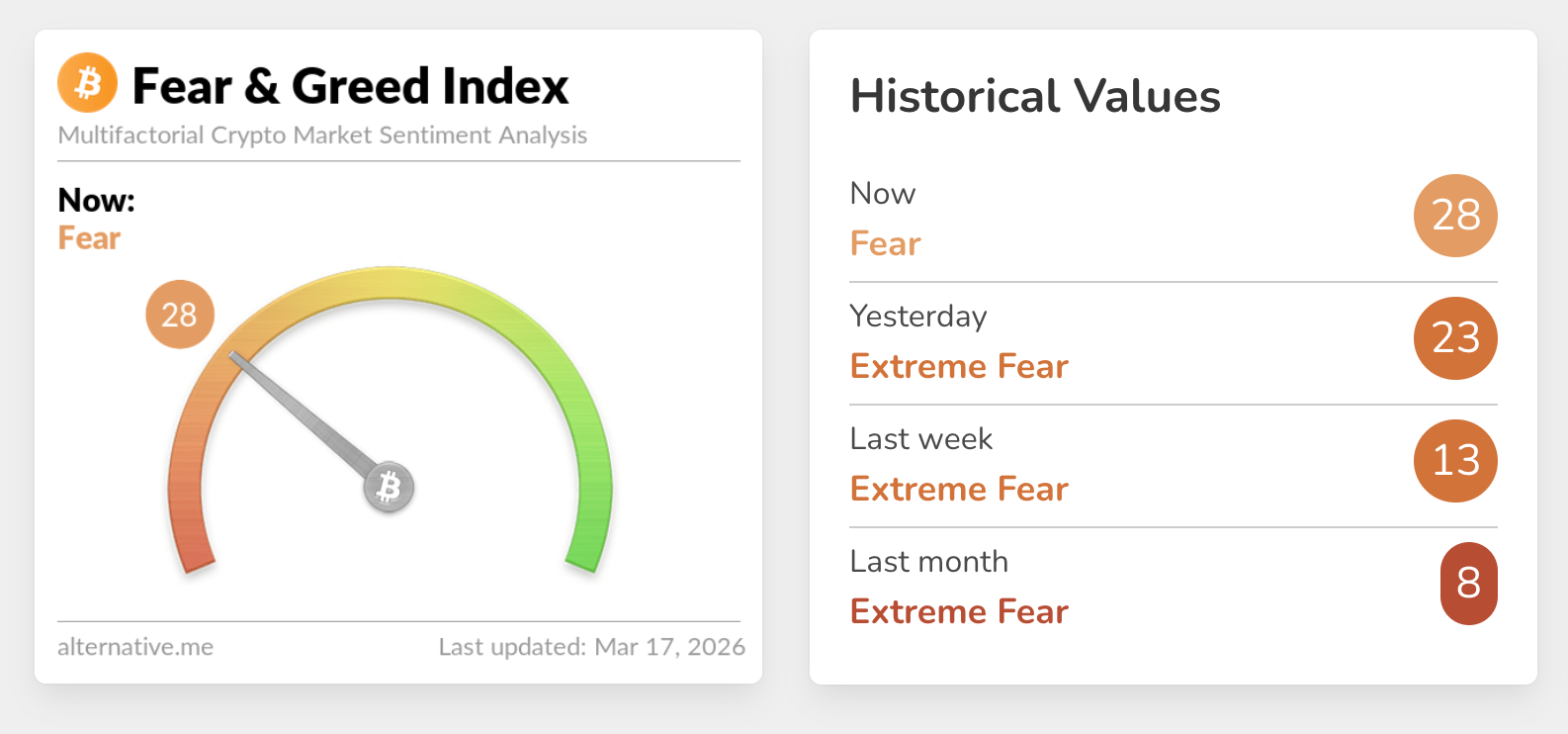

This expectation difference is directly reflected in market sentiment. According to Alternative.me data, today's cryptocurrency fear and greed index rose to 28, changing from "extreme fear" to "fear" recently—although still far from greed, the most pessimistic times may have passed.

However, the repair of macro expectations can only explain the starting point of the rebound and cannot support the price of $76,000. There is another force that truly pushes the price up.

Buying Coins Is No Longer News; How to Buy Is What Matters

In a market that has long felt "aesthetic fatigue" regarding DAT's increased holdings, the real discussion ignited is not "whether to buy," but "where the money comes from."

Strategy: Shifting from Diluting Common Stock to Issuing Preferred Shares

On the evening of March 16, Strategy issued another announcement: within a week, they spent $1.57 billion to buy 22,337 bitcoins.

The announcement indicated that of the $1.57 billion, only about $396 million came from the issuance of Class A common stock (MSTR), while a staggering $1.18 billion came from the issuance of "Stretch" perpetual preferred stock (STRC). This is the largest issuance by Strategy since it first went public with Stretch last July. Also, for the first time in weeks, Strategy relied mainly on Stretch for financing the purchase of Bitcoin. In other words, Strategy's "financing focus" is shifting from diluting common stock to issuing preferred stock.

This can be corroborated by recent dynamics. On March 1, Michael Saylor announced he would raise the annualized dividend rate (monthly adjusted) of STRC from 11.25% to 11.50%. Subsequently, according to BitcoinTreasuries.NET monitoring, the trading volume of STRC surpassed $200 million at the beginning of March, reaching a new high since 2026; coupled with the previously disclosed positive news of the U.S.'s first federally licensed digital asset bank, Anchorage Digital, holding STRC, other onlookers began to enter the market.

Last week, the stablecoin protocol Apyx announced an increase in its holdings of 200,000 shares of STRC (approximately $20 million), raising its total holdings to 255,000 shares. Meanwhile, Strive announced it would use $50 million to buy STRC, another noteworthy player.

As a Bitcoin treasury company, Strive is also engaging in similar practices—issuing preferred stock to raise funds, with part of the raised money used to buy Bitcoin and part kept as cash reserves to pay fixed dividends on the preferred stock. According to Strive's CEO Matt Cole, this cash reserve is typically held in low-yield money market funds, but this time, Strive took out $50 million and exchanged it for Stretch with an annual yield of 11.5%.

From "issuing stock to buy coins" to "issuing preferred stock to buy coins," Strategy is constructing an increasingly sophisticated financing machine. The popularity of Stretch reveals a deeper trend: when one DAT's preferred stock starts to be acquired by another DAT, and when stablecoin protocols and compliant banks also begin to hold them—a reality is quietly taking shape, where Bitcoin serves as the underlying asset, connected through preferred shares, with various institutions holding each other's stocks.

BitMine's "Alternative Strategy"

Aside from Strategy, other companies are also seeking their own ways.

In the first and second weeks of March, BitMine increased its holdings by 60,976 and 60,999 Ethereum respectively, significantly higher than the previous average weekly increase of about 40,000 to 50,000. As of March 15, its total Ethereum holdings had reached 4,595,562, approximately 3.81% of the total Ethereum supply.

Similar to Strategy, what truly attracted the market's attention is not the quantity of purchases, but the method of buying.

On March 15, the Ethereum Foundation announced it would sell 5,000 Ethereum through OTC, with the proceeds going towards the foundation's operations, including protocol development, ecosystem development, and community funding. The buyer is none other than BitMine. Typically, the Ethereum Foundation is viewed as a potential source of market sell pressure; once its held ETH is sold, it often raises concerns in the market. However, BitMine directly taking delivery from the foundation effectively transforms potential sell pressure into substantial buying.

Comments have jokingly referred to this as "official certification of the buyer." But from another perspective, this is precisely BitMine's strategy: seeking every possible source of chips outside the public market, even if it means buying directly from the foundation. This "targeted acquisition" provides liquidity to the foundation while avoiding the market impact of a public sell-off, making it a better solution for both parties.

Moreover, BitMine's holdings are not just sitting idle on the books. As of March 15, the total amount of Ethereum staked by the company reached 3,040,515, with an annualized staking yield of approximately $180 million.

For BitMine, since the implementation of its Ethereum treasury strategy, it currently faces an unrealized loss of over $6 billion. But Tom Lee remains calm. He believes that when the "mini crypto winter" truly ends, every single purchase made now will appear incredibly cheap.

Japanese Players Follow Suit

Besides Strategy and BitMine, across the ocean, a Japanese company is taking similarly aggressive actions.

On March 16, Metaplanet's CEO Simon Gerovich sent out two announcements:

- The first: by allocating new shares to global institutional investors, raising approximately $255 million; at the same time issuing warrants with fixed exercise prices, raising an additional approximately $276 million. In total, approximately $531 million will be used to increase Bitcoin holdings.

- The second: issuing the first movable warrants with "mNAV" terms, totaling 100 million shares. This warrant can only be exercised when the company's stock price reaches 1.01 times or more of the mNAV (net asset value per Bitcoin). Simon Gerovich stated that this design will enable the company to raise around $234 million in additional funds for acquiring Bitcoin.

The goals of the two announcements are aligned: raise funds to buy Bitcoin. However, unlike Strategy's combination of preferred shares and common stock, Metaplanet has introduced a new twist in the warrant structure.

mNAV is a metric invented by Metaplanet, calculated as follows: the total value of Bitcoin held by the company divided by the total number of issued shares. In simple terms, it indicates "the net asset value per share related to Bitcoin." The threshold of 1.01 times means that the warrant can only be exercised when the stock price is at least 1% higher than "the net asset value per share in Bitcoin." The brilliance of this design lies in that it binds the financing cost with the interests of shareholders. If the stock price is below the net value, the warrant cannot be exercised, preventing dilution of existing shareholders. If the stock price is above the net value, exercising the warrant to finance the purchase of Bitcoin keeps or even increases the amount of shares per Bitcoin, ensuring existing shareholders do not lose.

From Strategy to BitMine, and then to Metaplanet, these companies share a common logic: using public companies as financing platforms, swapping the raised funds for crypto assets, allowing stock prices to fluctuate with cryptocurrency prices. This model has its vulnerabilities. If Bitcoin prices fall for too long or too deeply, the financing premium will disappear, and the flywheel will reverse. But for now, the flywheel is still turning.

Conclusion

As of the time of writing, Bitcoin has fallen below $74,000, down about 2.95% from its intraday high. The test of $76,000 came quickly and left just as quickly, seemingly silently reminding everyone: the journey to regain lost ground has never been smooth.

However, aside from the superficial fluctuations, the underlying capital flows continue to signal bullish trends. According to the latest data from CoinShares, last week saw a net inflow of $1.06 billion into digital asset investment products, marking three consecutive weeks of strong inflows. Additionally, last week, the U.S. Bitcoin spot ETF had a net inflow of $767 million, while the Ethereum spot ETF had a net inflow of $161 million, maintaining positive inflows for three consecutive weeks. In other words, even amidst the market's turbulence, Wall Street's "smart money" continues to enter.

Looking through the fog of market trends, ordinary investors should recognize the two core main lines supporting this round of rising: one is the expectation difference in geopolitical situations: the market is no longer trading "the war itself," but "the war will not escalate indefinitely"; the other is the continuous cash generation from DAT companies: Strategy, BitMine, and Metaplanet are using real money and innovative financing levers to transform Bitcoin from a volatile speculative asset into a core reserve on global corporate balance sheets.

There will be a day when the gunfire ceases, and the expansions by Strategy feel more like a long-cycle narrative.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。