Author: Zuo Ye Web3

The Correct Approach to Tokens and Liquidity

Recently, I have been reflecting on token economics and the possible future of the cryptocurrency circle/Crypto/Web3, with a greater focus on exploring the paths of asset inflation driven by RWA. However, after some contemplation, I found that we should not directly conclude that there are no good players in the DeFi space.

There are no shortage of good tokens in the world, but there is a lack of discoverers.

Using Exchange Credit to Sell Your Own Tokens

“

USDS: Apple Distribution Network + Luxury Goods Allocation

To make it clear at the outset, I have always believed there are two reasons for the demise of token economics:

Under PoS, public chain tokens cannot have "actual use," with the residual Gas Fee becoming a financialized virtual use case. Even L1s like Tempo have essentially moved towards a Gasless model, where extremely cheap stablecoin Gas makes it so that sellers or companies can simply pay;

Most DeFi protocols do not need to issue tokens. Uniswap's token issuance was a desperate move in response to SushiSwap's traffic hijacking, and only Curve created a complex Ve(3,3) bribery model, making tokens barely have economic use beyond governance.

Unfortunately, the Curve system is not up to the challenge; from Convex to Resupply and Yield Basis, it is filled with the desire to make quick money, wasting the two quality assets of $CRV and $crvUSD.

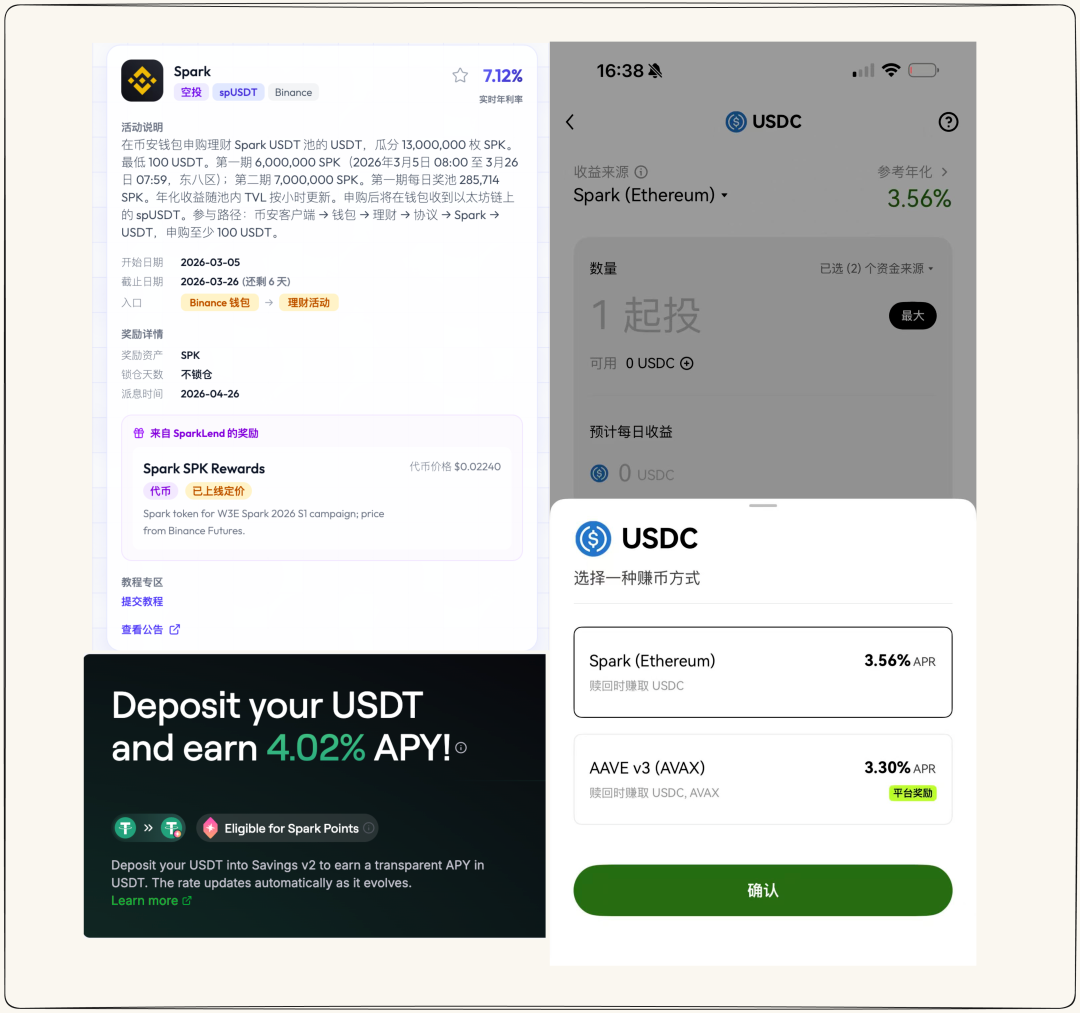

Seeing a glimmer of hope, during the development of Barker.money, I needed to research financial products from various exchanges, including Spark under Sky. In Binance's spUSDT reward promotion, the APY was approximately 7.12%, while OKX's USDC on-chain financial product, which is based on the same pool as Spark, had an APY of only 3.56%. Further tracing the other on-chain records of this pool revealed that many exchanges are contributors to liquidity: Bitget, HTX, Kraken, LBank, Bitso, Crypto.com, CoinEx…

Although the stablecoin deposits vary, behind it all is Spark managing liquidity. Whether it's a stablecoin or the $SPK token, Spark seems to deliberately distribute its financial pool through exchanges and even all participants in the crypto market, forming its own large liquidity distribution network.

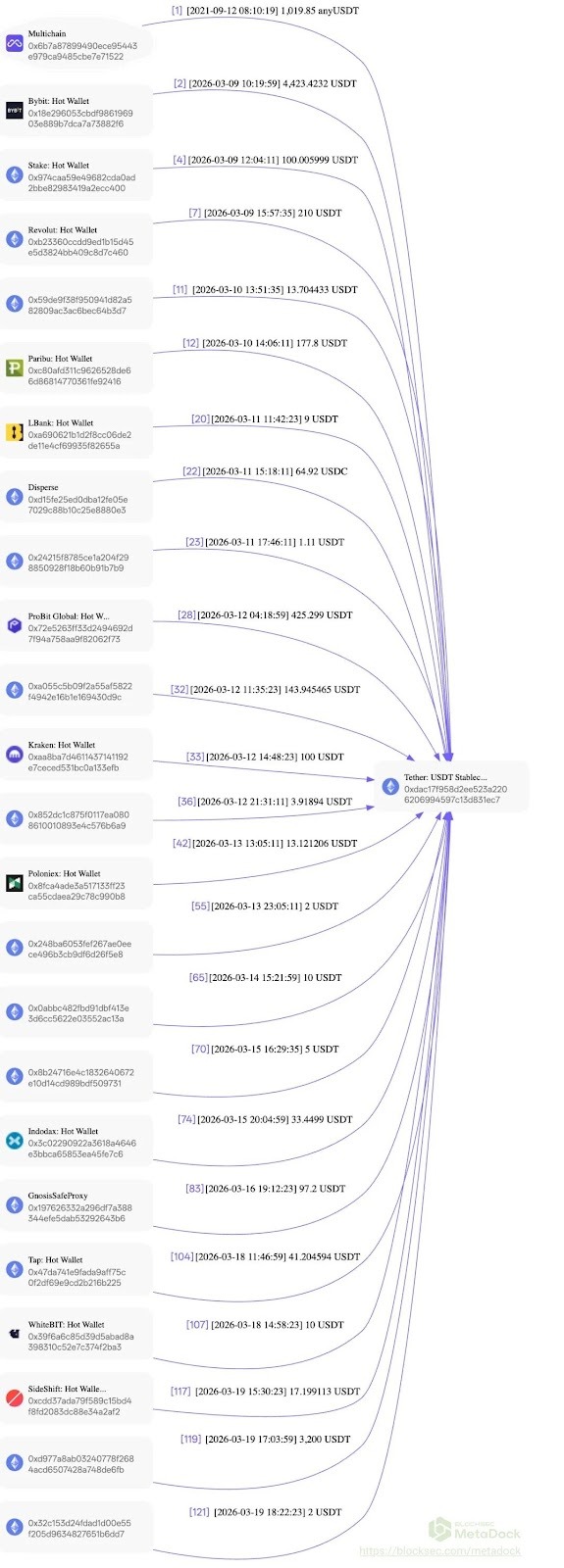

Image description: Addresses of multiple exchanges

Image source: @MetaSleuth

It looks no different from the conventional "selling tokens to attract deposits," but inadvertently, I discovered that tokens in PoS era DeFi protocols can have a second purpose: to control the quantity standards for distributors to acquire goods.

Sky/Spark stands out among various on-chain DeFi protocols; the price of USDS does not require the complex hedging mechanisms like Ethena's USDe, nor does sUSDS need to build liquidity pools like sUSDe everywhere. However, what you see with Curator and USDC may potentially be linked to Spark and $USDS.

Ultimately, USDe was constrained by Binance's operational level, becoming the largest passive victim of 10·11. The circular lending scheme initiated by Aave-Pendle abruptly stopped, ultimately degenerating into a white-label platform for interest-bearing stablecoins and a liquidity distributor for Hyperliquid—HyENA.

In comparison, USDS operates very simply, even so simply that it does not warrant documentation.

Promoting USDS requires just three steps: Step one, buy government bonds and USDC to support USDS's pegged price; step two, sell your liquidity management capabilities through first, second, and third-tier exchanges. Users can deposit using USDT/USDC; step three, control the airdrop pairing ratio of $SPK to classify and control the flow to distributors.

Image description: Comparison of Binance, OKX/Spark APY

Image source: @BarkerMoneyX @OKX @sparkdotfi

$USDS itself does not need to expand externally to avoid external shocks to the greatest extent. Even if the on-chain pool uses Spark to manage part of the liquidity, it cannot replace Sky/Spark's control over USDS.

Moreover, we can glimpse the correct usage of protocol tokens: do not view $SPK as a governance token, and it is not a forced intrusive economic module; $SPK is a measurement standard for managing the APY given to users by various protocols.

When the exchange credit level is high, for example, Binance, there is more supply of $SPK to raise the APY, but there can be an upper limit set to avoid liquidity rebalancing attacks like $UST. If Curator actively integrates or the exchange's credit level is low, then $SPK rewards should be reduced or even not provided, allowing for direct U in U out.

“Sky is essentially selling the liquidity of USDS, while Spark is essentially selling liquidity management.

It is important to understand that $USDS requires expenditure to transport government bonds onto the chain and has previously lamented its poverty, distributing all $500 million in government bond interest to sUSDS holders. However, do not forget that the issuance of $SPK has no cost at all.

Positioning itself as an asset for sale is always more profitable than selling someone else's assets; Spark is creating demand for $SPK using government bonds.

At Spark, $SPK becomes a tool for interest rate control, not fearing users mining, withdrawing, and selling. Even if the user's participation cost is low, it cannot reach zero.

The price of $SPK cannot be too high; otherwise, the maintenance cost will be too high. Again, a relatively low price combined with a large supply, along with $USDS liquidity essentially controlled by Sky/Spark, makes it nearly unprofitable for speculators to hoard $SPK.

USDS sits comfortably at home, remotely controlling on-chain Vault and exchange financial products.

Spark has reinvented the organization of liquidity, establishing a close distribution network of $USDS –> Spark –> CEX/Vault, outsourcing the token front end to USDC/USDT, outsourcing sales front end to exchanges, and they have to actively "distribute" the worthless $SPK.

Serving All On-Chain Liquidity

“RWA and bonds are better suited beyond government bonds and stablecoins.

The most remarkable aspect of Binance is that it has developed the BNB brand from the channels, which is also the fundamental reason it surpasses exchanges like OKX, allowing BNB Chain to retain funding even after years of "copying."

This is akin to Huawei's evolution from trafficking, assembly, OEM to operating its own 5G chips and phone brands, possessing bargaining power against dominant brands in a certain sense.

In terms of $SPK adjustments to APY rates, the amount of $SPK each exchange can receive is fixed for each activity cycle. For instance, if there are too many participants from Binance, the APY will decrease.

At this time, although small exchanges have fewer participants and $SPK, their APYs remain relatively stable; this allows for flexible adjustments in the competitive dynamics between large and small exchanges, avoiding strong dominance by a single channel.

Observing the exchange landscape through financial product competition tends to be clearer than through trading. Brand owners do not want to be eaten by a single channel and will have the incentive to maintain the existence of multi-tier distributors.

Apple, Huawei, luxury goods rely on different kinds of stores to delineate sales regions, reflecting the physical stratification of people. Stablecoins, on-chain Vault, exchanges rely on different levels of APY and sales volume to determine classes, which is behind the supply quotas of protocol tokens.

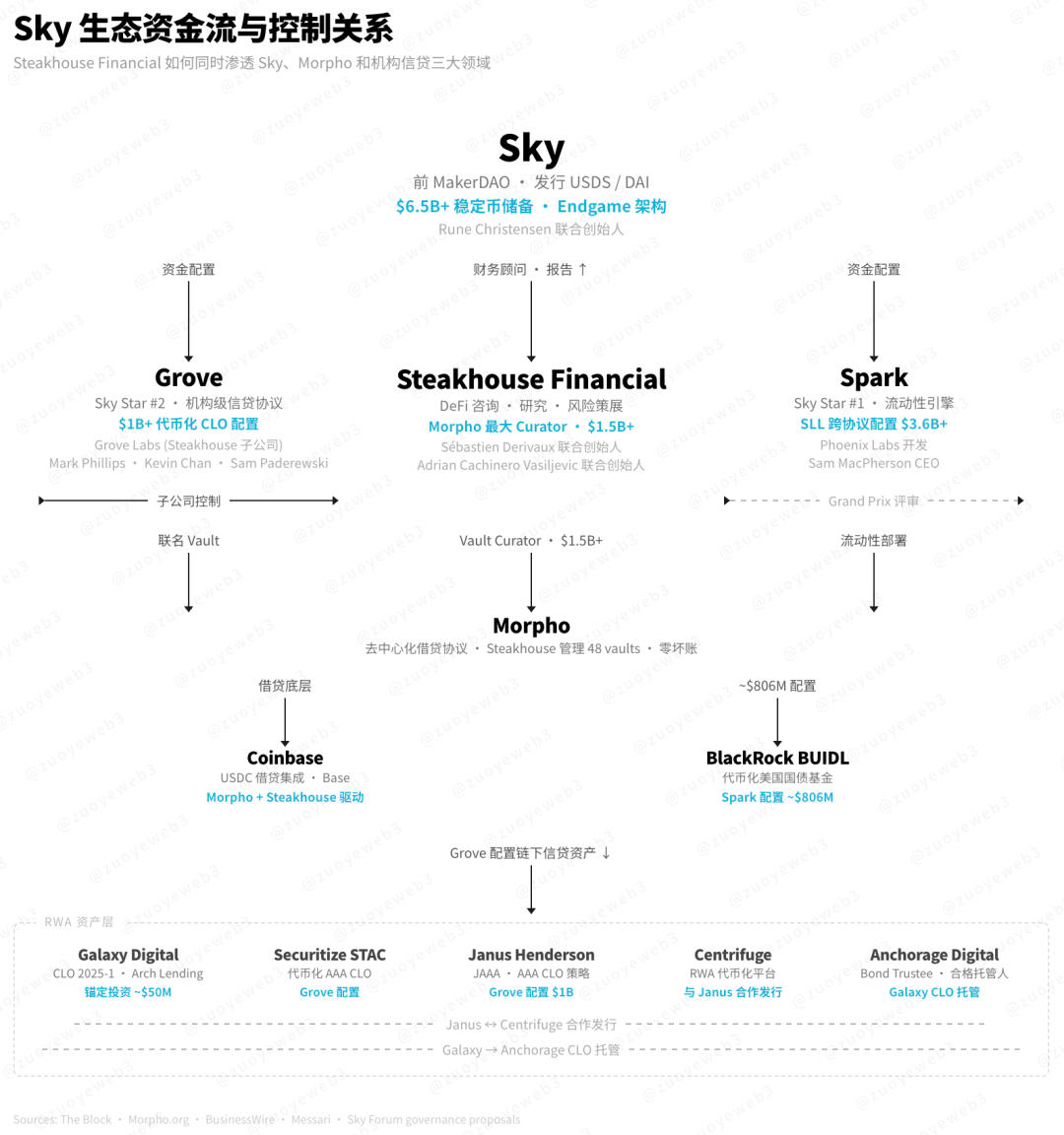

In contrast to Curve's clumsiness and Aave's internal wars, Sky is laying out entire on-chain liquidity. The stablecoin based on government bond arbitrage is just the current phase; RWA and various bonds have already been quietly positioning themselves.

Image description: Sky Ecosystem Layout

Image source: @SkyEcosystem

Since MakerDAO's rebranding, Sky has become the most successful Ethereum DeFi protocol. Compared to the centralized Aave, Sky embodies a more "decentralized" spirit; you may not even particularly sense its existence.

Under Sky, it is divided into multiple sub DAOs (also known as Stars).

Spark, also the first star of Sky, builds its core liquidity around USDS. After users deposit at the front end (USDT/USDC/ETH/PYUSD), Spark uniformly manages their yield strategies.

Grove, the second star, manages Sky's institutional and RWA business, but most importantly, it encompasses the products of Steakhouse Financial, with Steakhouse being the largest Curator of Morpho.

It can be further extended to the path of Morpho's CEX expansion, for example, Coinbase's USDC treasury is essentially operated daily by Steakhouse.

Grove itself is also an important maneuver for Sky's RWA bond layout, such as Sky funding $1 billion for Grove to acquire JAAA's CLO products (Collateralized Loan Obligation).

This differs significantly from the simple open institutional deposit business in DeFi protocols; Grove aims to become the source of liquidity for institutional DeFi, just as USDS holds a position in the stablecoin Vault.

Bringing RWA on-chain, whether it be tokenized stocks or tokenized bonds, poses a serious liquidity mismatch problem. The stock and bond markets do not face significant barriers in terms of on-chain technology and custody services.

The greatest deficit is the initial liquidity, or the mechanism that triggers asset price inflation. Please note, this doesn't imply a lack of trading volume for US stocks on chains; instead, it refers to the question of whether tokenized assets can issue assets again.

For instance, BTCFi's inability to establish roots in the lack of motivation for large holders to move BTC into DeFi; WBTC has already sufficiently met daily cross-chain participation needs. However, switching to Babylon for on-chain surfing requires extremely high yields to be feasible.

The most successful BTCFi model is MicroStrategy's approach of issuing interest-bearing bonds based on purchasing Bitcoin. However, it is clear that DAT does not possess such universality.

The RWA situation is similar; for instance, Galaxy's issuance of CLO products, after obtaining ratings and custody, can merely create a certain revenue product form, and users lack a strong demand for "proxy purchases." If high yields are incentivized, UST, xUSD, etc. are waiting for you. Grove needs to create a sense of "my bonds are as safe as US bonds," or based on US bonds, create tiered discounts to be incorporated into the existing DeFi operational system, for instance, acting as reserves or developing fixed-income products based on this.

Providing mere process services for RWA assets to go on-chain would approach a SaaS product, which is destined to fail at producing good prices.

Furthermore, if Sky shifts more assets to sub-US bond assets, its arbitrage potential will further increase, essentially leveraging the positions of holders for itself, and users maintain emotional stability due to their powerlessness.

“For a product aimed at liquidating exit scenarios, one must first inject enough liquidity, subsequently supporting the sale of its assets.

This methodology or approach embodies the most mature distribution ecology in the coin circle. Time shapes the true leverages of the Sky brand, using years of safety to ensure future security.

Referencing Sky's modus operandi also answers a long-standing question of mine.

Previously, I could not understand why Sun Ge wanted to create $USDD. Even if it aimed to participate in interest-bearing scenarios, wouldn't it be more direct to use $USDT instead? Or reframe the question: why is Sun Ge attempting to raise funds from small retail investors? If he has money, why not engage in asset management and insist on creating 2C products?

But now I speculate that the significance of $USDD lies in brand segmentation and liquidity barriers.

Even if $USDD is constrained by Sun Ge's reputation, the actual fundraising amount is limited. Compared to the high cost of fundraising from Yilihua, retail investors top out at 20%. Sun Ge can utilize it for wealth management, trading, and speculation, creating significant space for maneuvering;

Moreover, even if $USDD faces a crisis or liquidity issue, Sun Ge still has $TRX generated cash flow from $USDT Gas to support it. He can repay slowly or simply choose not to repay, as the cost for retail investors to pursue rights protection is extremely high;

It cannot use $USDT, not only because it is Tether's product, but also because people are willing to believe the narrative that "Sun Ge can keep making money from USDT."

It's all the same; we are willing to believe that Sky has the capacity to maintain business balance through the secure returns of US bonds. Therefore, the sub DAOs' participation in sub-bond businesses is inconsequential. Even hypothetically, if Grove's RWA business encounters a crisis, it will indirectly affect Sky, for example, with a cap of $1 billion, while Sky has a scale of $10 billion.

Conclusion

“

People most like to lend money to wealthy individuals who do not lack money.

Understanding today's DeFi, tokens, and DAOs has turned into an overly complex reasoning game, but its basic logic still revolves around tokens. Beyond governance, bribery, and air, Spark's APY control tool represents a new perspective.

Of course, perhaps there are even more sophisticated plays, but whatever changes, the core remains: "Sell yourself as an asset" rather than helping others sell their assets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。