Are American institutions' cash reserves gradually increasing, and will they drive the market up?

At the end of January this year, the risk market experienced a sharp decline without any warning, with Bitcoin's price falling from above $90,000 to $60,000. At that time, my view was that American institutions had run out of cash reserves. Although they were optimistic about the market, they no longer had the ability to continue to drive the market up, and their cash reserves had hit a historic low, which would inevitably lead to cash balance increases through reductions in holdings. This was also the main reason for the decline.

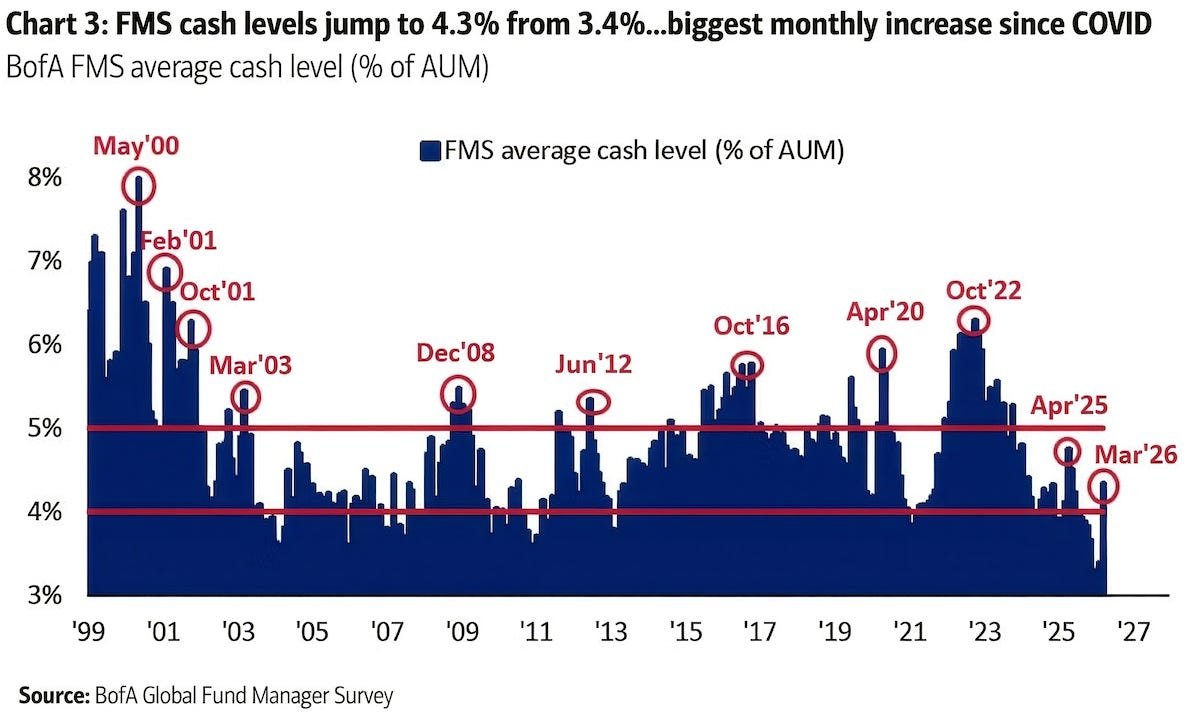

One and a half months later, looking at the latest institutional cash reserves, they increased from 3.4% to 4.3% over the course of a month from mid-February to mid-March. This represents the largest single-month increase since the pandemic, while the lowest point for institutional cash reserves in mid-January was 3.2%.

The source of institutional cash reserves does not need much explanation; it essentially comes from the aforementioned reduction of positions to lower risk exposure and converting some of the positions back into cash. So after two months, institutions' cash reserves have risen, but has this reduction reached its limit?

We need to return to the current institutional cash reserves. Although there was a significant increase in reserves over the past month, the current 4.3% is still at a relatively low level historically, still some distance from the average line of 5%. This is not a very abundant level of cash, nor does it imply a large amount of idle funds waiting to enter.

To put it more directly, institutions are not back to high cash levels from low cash levels; they have merely returned from having almost no ammunition to a point where they finally have some buffer. This is very important, as it determines what state the market is likely to be in next.

At the end of January, the market's issue was that institutions ran out of money. The result is that even with a bullish outlook for the future, they had no way to continue pushing up, and instead, they had to sell their risk assets to replenish cash. The decline in such a state often occurs rapidly, not due to emotional issues, but due to position structure problems; it is forced selling to exchange for liquidity.

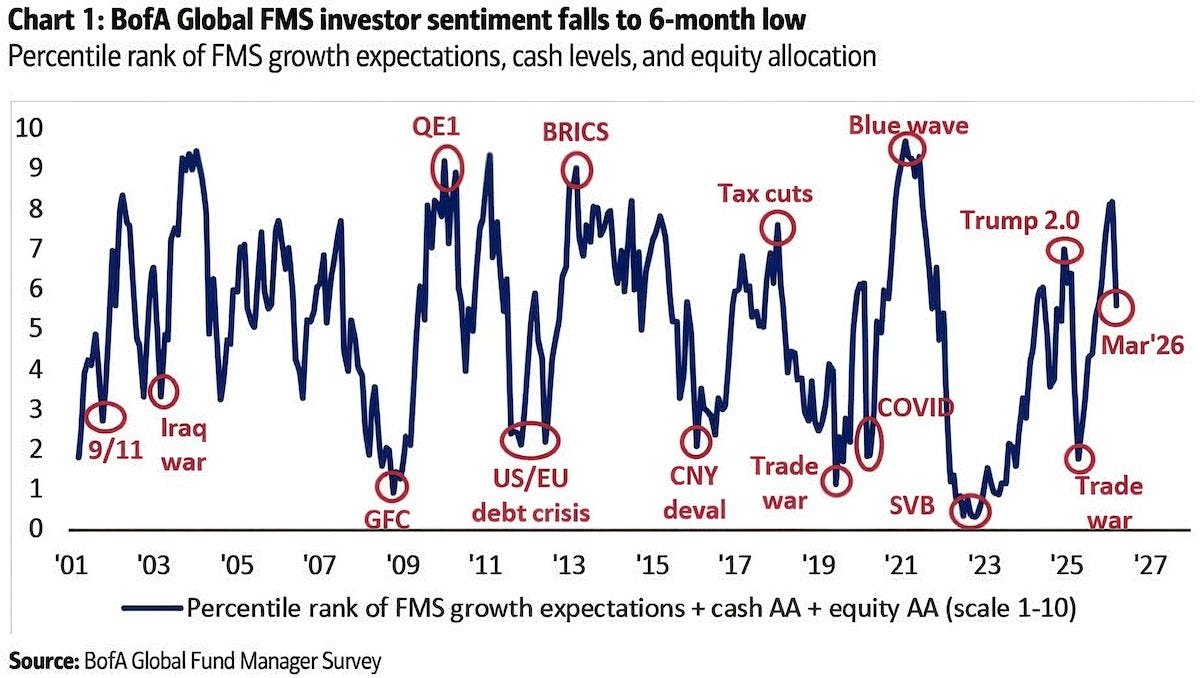

Now, by mid-March, while the issue has eased somewhat, it has not been completely resolved. Cash has returned somewhat, but it is still far from sufficient. Meanwhile, the overall sentiment of institutions, growth expectations, and allocation directions have not strengthened.

To put it simply, it is not that institutions are ready to drive the market up now; rather, they no longer have to forcibly sell to replenish cash.

Benefiting from the current cash rebound, it resembles a recovery from an extremely low level to a normal low level, representing more of a reduction in selling rather than an increase in active buying. Of course, for the risk market, the positive significance of this change is that institutions now have some buffer and do not need to sell while being bullish as before.

As for $BTC, to truly re-enter a trend upward, merely seeing cash increase is not enough. We also need to see institutional sentiment stabilize, growth expectations not continue to downgrade, and the market begin to re-accept higher risk exposures. Only then can the replenished cash shift from a "defensive mode" to an "offensive mode."

End

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。