Author: shtanga0x & securezer0

Translation: Wenser, Odaily Planet Daily

Editor's note: Recently, on the timeline of the X platform, posts related to Polymarket's LP incentive for NCAA "March Madness" have been flooding in. At the same time, official members of Polymarket revealed that a major announcement will be made next Monday, and the community speculates it may be related to financing or token issuance information.

After the SEC and CFTC cleared the obstacles for airdrops on crypto platforms through the five-pronged approach, POLY has become the "last hope for grabbing free tokens" for many people, and LP market-making may become one of the key indicators for airdrops.

In light of this, Odaily Planet Daily will provide a more comprehensive perspective for Polymarket users by borrowing the pros and cons of LP market-making incentives from two analysts. Below is the translated content, with some information edited.

Positive View: Four Major Categories Behind the Polymarket LP Incentive Program

Recently, Polymarket's incentive mechanism has undergone a low-key upgrade, shifting its focus to liquidity providers (LP). For the past few years, the platform has implemented a "zero trading fee" strategy, but since the beginning of this year, it has quietly introduced transaction fees for specific betting events, along with two major market maker incentive programs.

Superficially, the collection of transaction fees seems disadvantageous to trading users, but in reality, it is addressing the most core structural pain point of prediction markets—the liquidity issue.

The new fee structure aims to fund incentive projects, rewarding users who provide limit orders and maintain order depth. As a result, both Polymarket and its users benefit from: narrower spreads, a richer order book, and a better trading experience—especially in a high-frequency crypto market.

The path it promotes is also quite clear, showing a trend from singular to diverse:

- January 2026: 15-minute Crypto market

- February 2026: Expanded to 5-minute Crypto market + NCAAB College Basketball + Serie A

- March 6, 2026: Expanded to all Crypto markets (covering events like 1H, 4H, daily, weekly, etc.)

Based on the above information, this article will explain in detail how the new fee and reward systems operate—and why the fees paid + rewards earned may become potential anti-sybil indicators in POLY airdrops. This is not a simple monetization operation, but Polymarket is using actions to tell everyone: what it truly wants is liquidity, not bot volume.

Part I. A Comprehensive Analysis of the New Taker Fee Mechanism

The vast majority of Polymarket markets remain completely free. Deposits, withdrawals, and trades (for the majority of event markets) still have zero platform fees.

Trading fees currently only apply to taker orders, covering three types of markets:

- All Crypto up and down markets (15min, 5min, 1H, 4H, daily, weekly, etc.)

- NCAAB (U.S. College Basketball League)

- Serie A (Italian Football)

The key point is that taker fees only apply to markets created after the fee activation date, and previously existing betting events are unaffected.

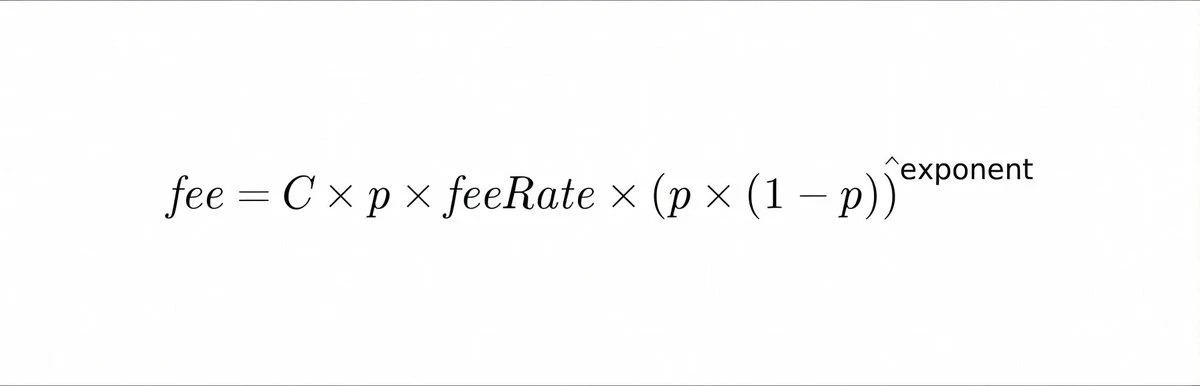

The fee formula is uniform (where C = number of trading chips, p = chip price/market probability, the fee is rounded to four decimal places, with a minimum fee of0.0001 USDC):

Effective fee rates follow a symmetric probability curve:

- When the probability is close to 50% (highest uncertainty about the outcome), the fee is highest;

- When the probability is close to 0 or 1 (higher certainty about the outcome), the fee approaches 0.

For example, in a $100 Crypto market transaction,

- p=0.50 → trading fee (fee) is approximately $0.44;

- p=0.10 or 0.90 → trading fee (fee) is approximately $0.02.

The probability curve for sports events is similar, but the midpoint (probability around 50%) incurs slightly higher fees, specifically detailed as follows:

- Buy: fee deducted from chip share;

- Sell: fee deducted from USDC funds;

- Market-making incentives are paid in USDC.

It is worth mentioning that the Polymarket platform does not retain the entire fee pool, as a fixed percentage of the transaction fees (20% for Crypto markets, 25% for sports betting events) is directly returned to LP. (Note: Polymarket's compliant platform in the U.S. uses a simple fixed fee of 0.01%. This analysis only discusses the global CLOB platform, which has introduced the new fee system in 2026.)

Part II. Market Maker Incentive Program (Limit Order Execution Rewards)

This portion of the incentives only covers markets that have charged taker fees. This means that only limit orders that are taken by traders can receive corresponding rewards; simply placing an order that does not get executed does not count.

The calculation of the reward amount matches the fees charged to takers. Each participant's reward is proportional to their trading volume, with the total prize pool comprising a portion of the collected fees (20% for Crypto markets, 25% for sports betting events).

Competition only occurs within specific betting events, and LP orders only compete against other LPs within the same liquidity pool.

Daily incentives are sent directly in USDC to the corresponding wallet addresses.

Part III. Liquidity Incentives (Idle Order Incentives)

The second set of incentive systems is provided by the Polymarket platform and applies to all betting events (including those that do not charge fees).

The core distinction is: there is no need for orders to execute, as long as liquidity is provided by placing orders on the order book.

Each betting event defines several parameters that determine eligibility:

- Maximum incentive price gap (e.g., ±4 cents)

- Minimum order quantity

- Daily total reward pool

The platform samples the order book every minute, recording 10,080 snapshots over the week.

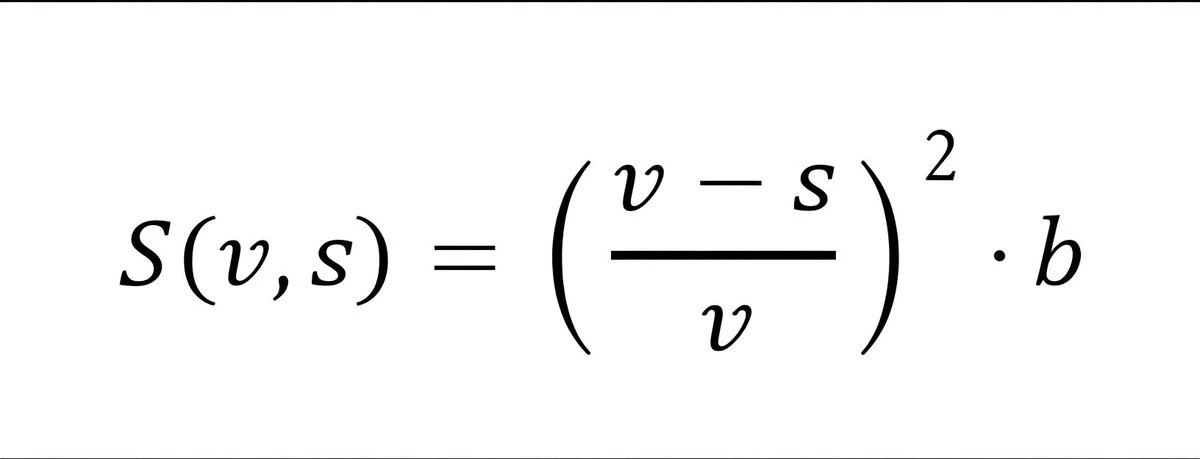

The reward calculation formula has super detailed aspects:

1. Distance score (quadratic equation)

Where,

V - maximum incentive price gap

s - distance from the midpoint

Orders close to the midpoint score exponentially higher.

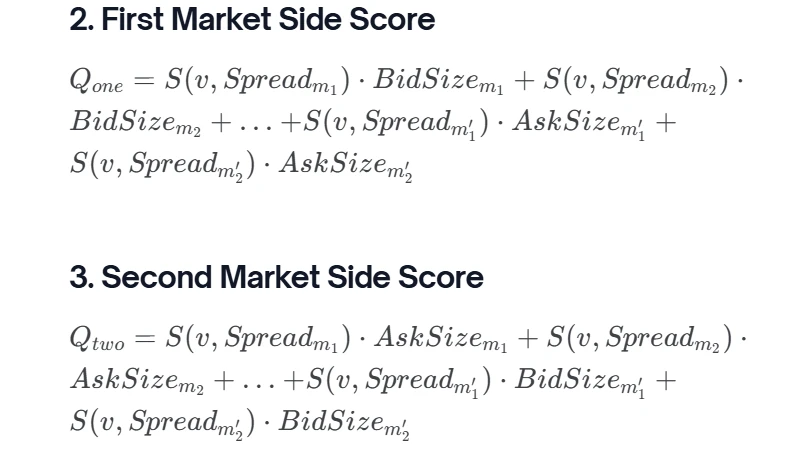

2. Bilateral score (YES/NO complementary structure)

Bids (bid) and asks (ask) calculate scores separately, considering the Yes/No market's complementary structure.

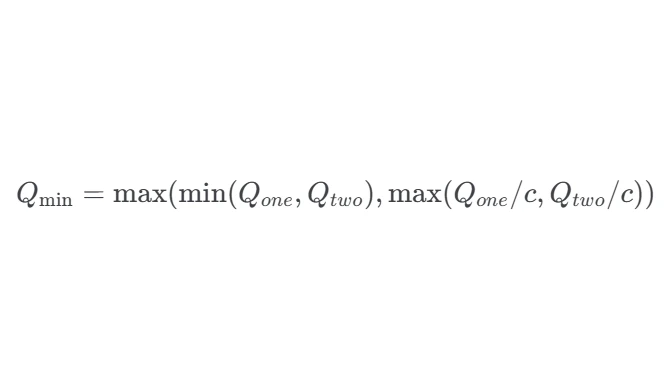

3. Q-value minimization adjustment

Providing liquidity at both ends of the order book scores higher in betting events.

Single-sided quotes are penalized unless the market probability is close to 0 or 1.

4. Final score

All LP scores will be normalized and aggregated over time to determine each participant's share of the market reward pool.

Rewards will be distributed at midnight UTC in USDC, starting from a minimum of $1.

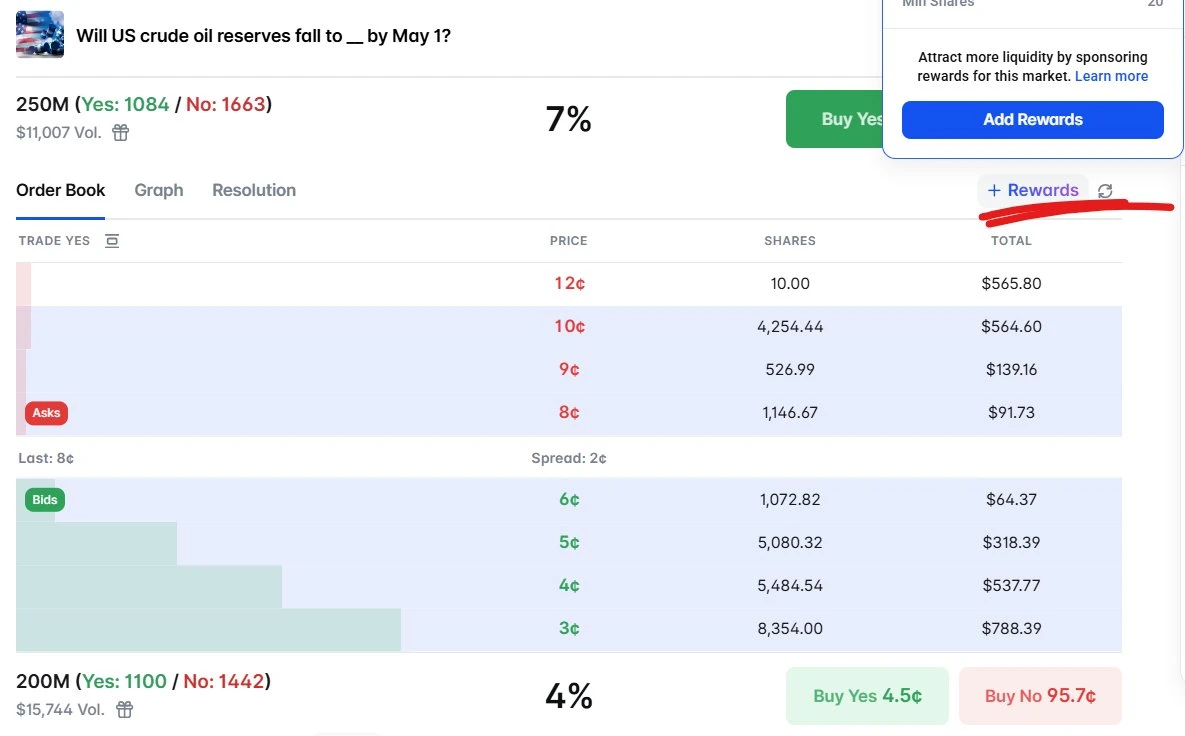

You can currently view active reward betting events and personal earnings in real-time at polymarket.com/rewards. The incentive price range is highlighted in blue on the order book interface, and users can also check the official Polymarket documentation.

Currently, single-sided orders can still earn points (but at a discount), while two-sided quotes receive priority for incentive points. Rewards will be calculated individually for each betting event. There is no cross-event calculation. In practice, this system rewards traders who maintain tight spreads and balanced liquidity near the market midpoint, enhancing the trading experience for all users.

Part IV. Sponsored LP Incentives

The third mechanism allows anyone to directly add LP incentives to specific markets using USDC, attracting LPs to market-making. Sponsors can invest or withdraw funds at any time, and unspent funds will be automatically refunded.

The rules for this mechanism are completely consistent with the liquidity incentive program—orders can be placed without the need for execution.

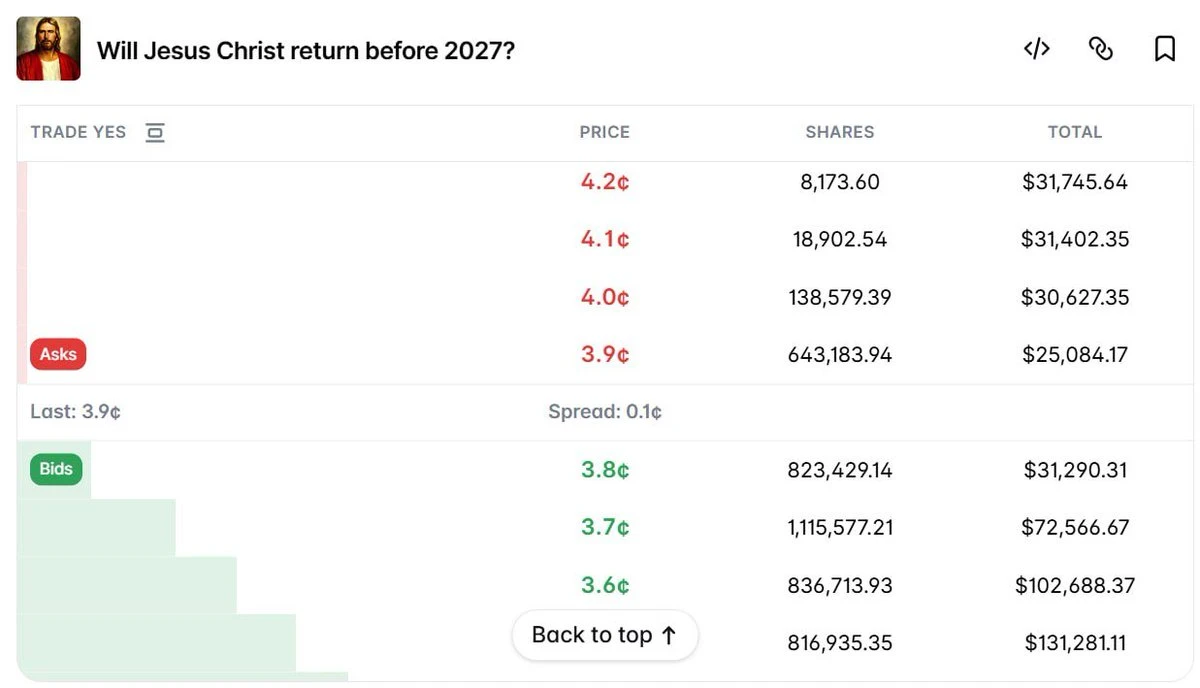

A typical case is the betting event "Will Jesus Christ return before 2027?" where a user on a certain platform dropped $70,000 as LP incentives in February and now receives about $57 a day in liquidity incentives, making this event one of the deepest betting events on the platform. This mechanism allows the community to significantly enhance the market liquidity of any betting event without waiting for Polymarket's official intervention.

Part V. The Most Powerful Anti-Sybil Indicator for POLY Airdrops

At first glance, Polymarket seems to only need more traders.

However, if most users only rely on market orders, the platform will soon face liquidity issues.

Polymarket does not depend on centralized market makers; thus, if there are not enough limit orders, the order book will become sparse.

In this scenario, it is hard to avoid excessive slippage when buying, selling, or executing large orders, and trading fees will surge.

Polymarket does not need volume-boosting bots; it needs true LPs that provide value.

In the past, everyone focused on boosting trading volume, thinking a large trading volume was the key to obtaining airdrops. However, the new fee structure and reward program imply a different incentive model—what matters is not just the trading volume, but the active involvement in betting events that generate fees and need liquidity. In other words, the platform rewards targeted LPs, not just passive limit orders.

The reward distribution formula effectively reveals the type of liquidity that Polymarket values most. The scoring system evaluates:

- The proximity of orders to the midpoint

- Order size

- The balance between buy and sell prices

Thus, rewards become a direct measure of how much a trader's liquidity contributes to the platform's value. If traders continuously earn rewards, it indicates that their orders are actively enhancing market liquidity and execution quality. Here are examples of market participants earning potential incentives:

- Will the Arctic sea ice extent reach its maximum this winter?——has existed for 3 months, trading volume under $20,000, liquidity reward only $9;

- Will Bitcoin reach $75,000 in March?——has been active for two weeks, trading volume reaches $3 million, liquidity reward is $142;

- Bitcoin Up/Down - 15 minutes —— covers hundreds of betting events, daily trading amount of millions, daily average fees about $10,000, liquidity reward of $2000.

Compared to specific betting events, the truths revealed by the data are more critical—compared to simple trading volume metrics, taker fees and received liquidity rewards are harder to manipulate artificially. Systematically earning market-making incentives requires capital, risk management, and ongoing presence, which significantly weakens the advantage of those looking to exploit the system and instead benefits genuine market participants.

Conclusion: Taker fees and LP incentives may become key indicators for POLY airdrops

The future allocation of POLY tokens will not only depend on trading volume but is more likely to depend on the paid taker fees and earned LP rewards. These indicators are transparent, measurable, and highly aligned with the platform's needs. In this model, rewards are not linked to trading volume boosts but are connected to contributions that truly optimize the platform's trading experience: liquidity, stability, and efficient price discovery.

In other words, those who are the best-performing LPs are also the most valuable users. The most hardcore Polymarket players are never the ones with the highest trading volume, but the LPs that deepen the liquidity of the order book the most.

Of course, there are always differing opinions in the market, and some believe that the LP incentive program launched by Polymarket seems like "spending money to swap for liquidity," but in fact, it is a trap set for LP users to make a profit. Let's hear this opposing viewpoint.

Opposing View: Is the Polymarket LP Incentive a platform scam? Is LP essentially a "spending money to lose" trap?

Regarding the recent LP incentive program launched by Polymarket, arbitrage traders and Polymarket/Kalshi bot players securezer0 directly labeled the "Polymarket Rewards Farming," which is touted by many influencers in the industry, as a massive psychological operation, explicitly stating that it is a collective hype created with the platform's direct financial input or heavily incentivized KOLs.

The truth about LP: Another form of "spending money to lose"?

Multiple LPs candidly stated: Currently, Polymarket's LP mechanism is essentially "spending money to lose."

Where does the problem lie? The leaderboard directly accounts LP rewards in profit-loss data display, but fails to mention a critical concept—LP wear.

When your position gets executed on a one-sided basis, it often cannot be sold at a reasonable price or may not sell at all before the betting event settles; this portion of capital loss is systematically concealed by the platform. The actual ROI data is far lower than the surface numbers, and for most LP participants, profitability is actually negative. They only believe that POLY airdrops can cover the losses—this is not an arbitrage incentive program but a platform faith transaction.

Why are professional market makers unwilling to participate?

Professional market makers generally approach Polymarket LP operations with avoidance; the core reason is straightforward: there is a real risk of insider trading.

Polymarket and Kalshi have to exchange equity for liquidity to get professional market makers to the table—this itself indicates the issue.

Effective LP operation is a set of extremely complex automated risk control systems. The myth of "low entry barrier, high return" for LP only holds true if Polymarket consistently pours heavy financial resources into subsidizing liquidity rewards—and this path is fundamentally unsustainable in the long term.

The platform's real dilemma: needing to "create" millions of dollars out of thin air daily

Inadequate liquidity is the primary driving force behind Polymarket gradually opening the fee switch.

To maintain liquidity rewards for various betting events and retain more USDC liquidity on the platform, Polymarket needs to expend millions of dollars daily to maintain trading depth. If a better solution cannot be found, the platform has no choice but to charge transaction fees on every buy and sell to sustain investors and market makers.

Once comprehensive fee collection is implemented, ordinary users will face a very awkward situation—because in that case, traditional sports betting platforms might turn out to be more cost-effective, for the following reasons:

- Composite rates yield equivalent odds;

- Traditional platforms also offer cashback and cash incentives;

- Clear rules, protected by regulation;

- Insider traders can get their accounts banned or even face jail time.

Three truly viable solutions: fixed transaction fees, POLY liquidity pools, expanded product fees

Rather than drinking poison to quench thirst, it is better to address the root problem: target the vampire rather than harvest from users. Charge fees to those arbitrage bots drawing USDC from genuine users. After all, these bots are the source of liquidity pollution. Specifically, there are the following methods:

Charge a fixed fee of 1% only on profits, that is, charge only on the net earnings portion after subtracting the principal from the sell price, without affecting the principal or harming users' trading experience.

Build a native liquidity pool with POLY tokens. Programmatically and at the protocol level, provide liquidity for each betting event, deeply tying tokenomics with liquidity supply.

Charge fees on expanded products rather than core products. Props, derivatives, leverage—these are natural charging scenarios, and attacking here won’t harm the foundational user experience.

Currently, the moat of Polymarket's business remains to be strengthened. Zero fees and better odds are the most critical value anchors that distinguish it from traditional betting platforms. Abandoning these two points for short-term revenue would be equivalent to self-sabotage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。