Author: Master Xiao Lu

This afternoon, I had some free time and couldn't sleep while lying on the hotel bed, so I went downstairs and asked the driver accompanying the team to take me out for a stroll. However, he just shook his head and said that there was no gas available here, and that it’s better not to move around. I was a bit taken aback and asked him where the nearest gas station was. After thinking for a moment, he gave me an address. I looked at it, and it wasn't too far, so I walked over. The scorching sun made me sweat heavily along the way, and when I thought about giving up, I spotted a long line of motorcycles queuing not far away, and I knew I had arrived.

As I walked closer, I noticed that the employees at the local gas station looked very serious, pouring gas from muddy plastic buckets into everyone’s containers, and the tool used for refueling was a mineral water bottle. Each person could fill just one bottle. Watching them carefully pour the pink liquid gasoline into the bottles made me truly realize that the place I was standing in was no longer China, but in the county of Mengxing in the province of Luang Namtha, Laos, a place of extreme poverty yet full of vitality, where the hard-earned industry is facing the most severe drought.

At this moment, I thought about the heated discussions in everyone’s mouths about the petrodollar, which does not exist only in the futures market, geopolitical discussions, and simple financial education books. For most resource-rich and impoverished countries, it first represents a development dilemma: they clearly stand on top of oil, natural gas, copper mines, iron ore, rubber, and timber, yet they can only sell them as raw materials without further processing, and then use the dollars they received to buy machines, fertilizers, steel, cars, medicines, power plants, and mobile phones made by others at high prices. Thus, the so-called petrodollar, on the surface, is the dollar pricing oil, but in essence, it reflects the long-standing inability of resource countries to retain their resources domestically and turn them into their industrial, energy, and consumer systems, being reduced to the role of the simplest supplier and the most compelled generous purchaser.

Because of this, the petrodollar has never been just a story about oil and dollars but rather a story about positioning. Since the latter part of the Cold War in the last century, with the United States achieving an absolute dominance in the world trade and financial system, it began to decide who is responsible for selling resources, who is responsible for manufacturing, who absorbs the surplus, and who provides the safest havens globally while reaping the most profits. Only by understanding this issue can we break free from existing narrative frameworks and see a more genuine world.

Looking back over the years, especially in recent days, whenever the topic of the petrodollar arises in the Chinese public opinion space, it often sparks two completely opposite yet overly simplistic narratives. The first narrative prefers to paint it as a conspiracy theory, as if all the world's problems can be traced back to the U.S. forcing everyone to use dollars to buy oil and goods; while the second narrative prefers to depict it as an old order that is on the verge of collapse, as if on any day when a certain Middle Eastern country decides to settle oil purchases in another currency, the dollar's hegemony would immediately shatter. Both views capture part of the petrodollar's essence but misjudge its real focus. If the petrodollar were merely about warehouse receipts, oil tankers, and incredibly powerful fleets, it wouldn’t have dominated the world for so long. What truly supports it has never been the number of barrels floating through the Strait of Hormuz, but rather the much larger resource-manufacturing-financial return system behind the strait.

This system is what underpins the world economic division of labor we are familiar with. This division consists of at least four layers: the first layer, resource-rich countries export oil, natural gas, minerals, and food to earn dollar income, but most of this income is converted into investments in the United States, which forms the outermost shell of the petrodollar; the second layer, manufacturing countries purchase these resources with dollars and produce steel, machinery, chemicals, electrical equipment, vehicles, construction materials, and various industrial products, continuing to settle trade in dollars and arrange reserves globally; the third layer, the surpluses and profits obtained by manufacturing countries do not universally convert into their national capital markets but largely settle as dollar reserves, sovereign wealth funds, offshore financial allocations, and secure assets like U.S. Treasury bonds; the fourth layer, the United States, leveraging the deepest treasury market, the most liquid capital markets, the strongest legal and financial intermediary networks, and a substantial domestic demand market, absorbs global savings, maintains current account deficits, exports debt, while continuing to attract global risk aversion demands.

Therefore, simplifying this system as petrodollars is less accurate than describing it as a dollar order formed by resource locations, manufacturing locations, consumption locations, and financial safe havens. Oil is indeed important here, but its importance does not stem from its mystique, but from the fact that in modern industrial civilization, energy has always been the most fundamental and indispensable input. Whoever controls the pricing of energy and the return pathways of energy surpluses will find it easier to control the positions of resource-rich and manufacturing nations in global division of labor.

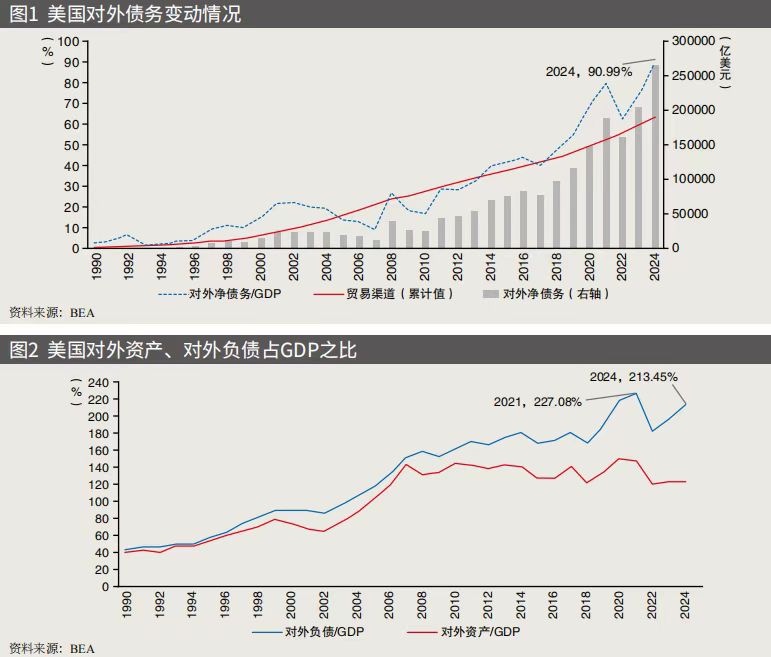

This is why, at the peak of the petrodollar, the U.S. often appeared to be in violation of common sense. By general economic intuition, a country with a long-term trade deficit, long-term fiscal deficit, and long-term dependence on external financing should eventually face capital flight, currency collapse, or debt crisis. Yet the U.S. has not. The reason lies not in its violation of this common law, but in its positioning at the other end of the rule: not as an ordinary debtor under capital judgment but as the issuer of the world’s primary reserve currency, the largest provider of global safe assets, and the ultimate haven for global liquidity. Data from the U.S. Bureau of Economic Analysis shows that by the end of 2024, the U.S. net international investment position expanded to negative $26.23 trillion, while external liabilities skyrocketed to $62.12 trillion. Normally, under such a scale of external debt, a country would have experienced severe turbulence long ago; yet the U.S.'s issue is precisely that it has not truly been crushed by this debt until today.

Why? Because the strongest aspect of the dollar system is that the U.S. can convert its debts into the most willingly held assets worldwide. This means that not only can the U.S. go into debt, but it can do so at a lower cost; not only can it incur low-cost debt, but it can take the money that the whole world is willing to lend it at low cost to engage in higher-yield global allocations. For a long time, the U.S. has not been merely a straightforward world debtor but more like a global banker, exporting dollars worldwide through trade deficits while earning investment income through financial channels, creating an almost abnormal golden debt structure.

However, once any system operates to this extent, cracks will simultaneously begin to emerge. This privilege is not inherent; it must rely on several prerequisites: resource-rich countries must continuously export raw materials, manufacturing countries must continuously need dollar settlements and reserves, U.S. capital markets must continue to be viewed as the safest haven, and the U.S. itself must possess sufficiently strong institutional credibility, R&D capabilities, fiscal resilience, and domestic consumption capacity. If any of these links begins to weaken, the cost of the entire system will rise rapidly.

Now, we can shift our perspective back to domestic issues, where the problems arising from this system will gradually reveal their own answers. For ordinary people standing here, oil and various raw materials have never merely been an item on Wall Street's balance sheet, but rather the most fundamental survival materials. Whoever can stably access all these, transform oil into electricity, chemicals, transportation capacity, and industrial raw materials, truly holds the capabilities facing the future.

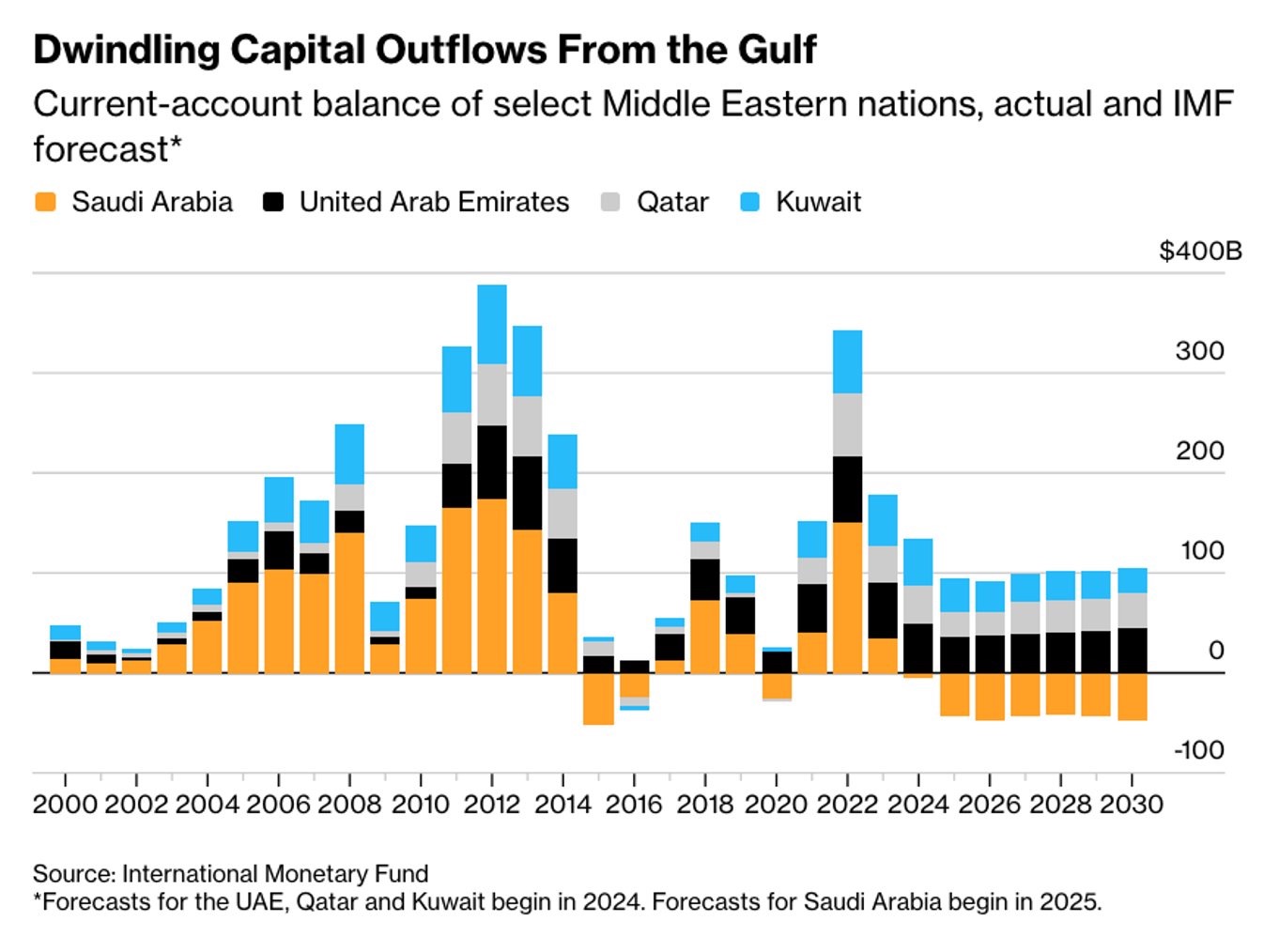

Such changes are not only occurring in China but are also appearing globally with the push of the Belt and Road Initiative, where the first changes are happening in the destination of resource surpluses. In the past, Gulf countries became a crucial link in the petrodollar system because they reinvested their massive surpluses from oil sales back into the dollar system. However, this is now changing. For instance, Saudi Arabia’s current account has shifted from a surplus of 2.9% of GDP in 2023 to a deficit of 0.5% of GDP in 2024, and this deficit increasingly relies on external borrowing and the reduction of overseas asset accumulation for financing. Behind this is a large-scale expansion of domestic capital expenditure, including projects for future cities, infrastructure, industrial zones, logistics, and tourism facilities. In other words, part of the oil surplus that would have previously flowed back to the U.S. financial market quite naturally is now staying more and more locally, supported in construction by China.

Examining the global picture, such changes are even more profound, as the center of manufacturing and capital supply is experiencing a structural shift. More and more resource-rich countries and emerging market nations are starting to try to keep resources local and extend their industrial chains with the help of equipment, financing, engineering, and digital infrastructure provided by China. Goldman Sachs research shows that by 2024, China's exports to developed economies have dropped to 42%, down from 58% in 2005, while the proportion to emerging markets has risen to 36% and to frontier markets has risen to 8%, with the share of Belt and Road-related economies in China's total trade further increasing to 47%. This means that China’s foreign trade focus is no longer merely selling consumer goods to developed countries but outputting industrial capabilities into a broader emerging world.

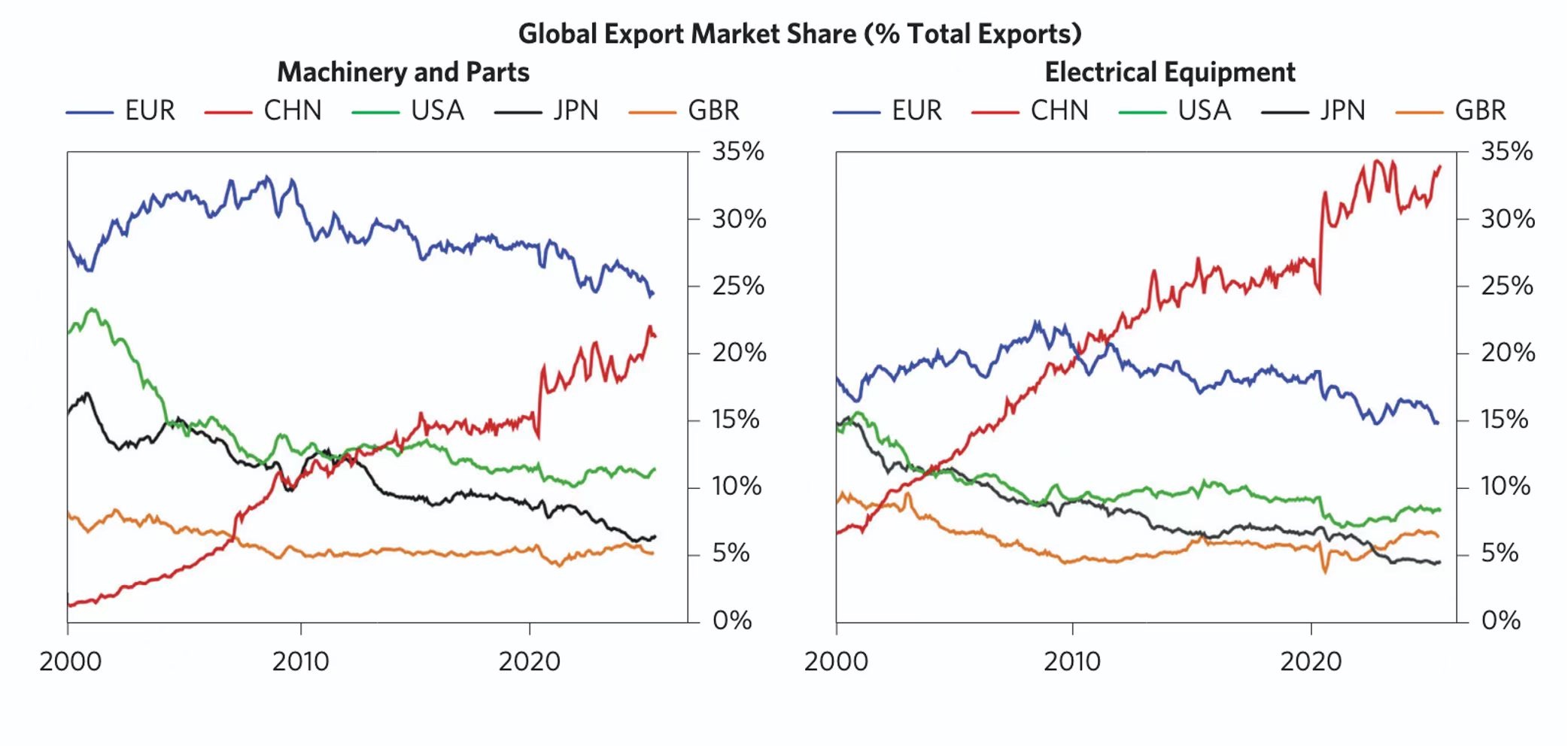

It is also noteworthy that China's global share in exports related to electrical equipment and machinery has become extremely high. Public trade and industrial research show that China's global export share in electrical equipment remains at around 30%, while it occupies one of the most important positions in machinery and component exports. In contrast, the U.S. share and supply capacity in these "machines that make machines" sectors are evidently weaker than those of China and some European and East Asian countries. This indicates that the U.S. has become significantly dependent on imports for many capital goods and intermediate equipment necessary for rebuilding its manufacturing sector. Therefore, the U.S. today no longer has the capability to stand at the zenith of research and manufacturing to complete the allocation of the industrial system as it once did.

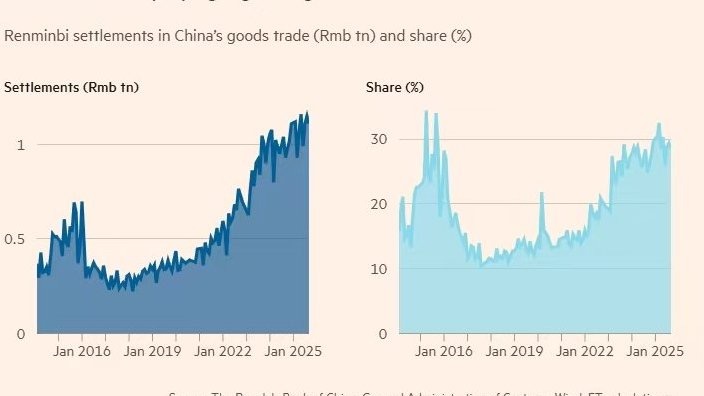

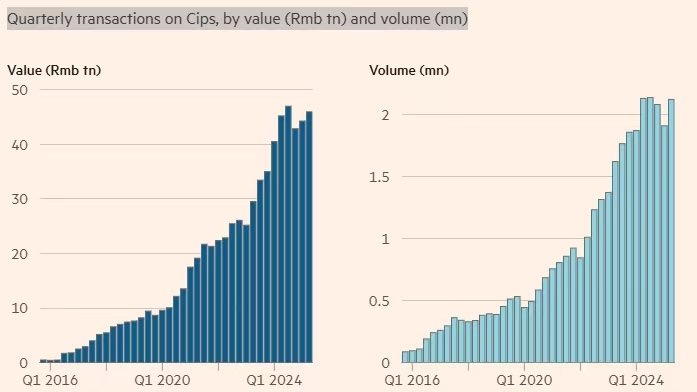

The forthcoming changes become inevitable, as the export of resources themselves is increasingly bypassing dollars as the transactional interface. Resource-rich countries, manufacturing nations, and emerging markets are gradually establishing new channels for themselves that do not necessitate passing everything first through dollars, then through New York, and finally back to the U.S. asset pool. What is most noteworthy here is China’s actual expansion in cross-border payments and renminbi settlements in recent years. The Financial Times cited data from the People’s Bank of China and CIPS indicating that in the past five years, the cross-border use of the renminbi has significantly increased, with the quarterly trading volume of CIPS, calculated by amount, rising from less than 1 trillion yuan at the beginning of 2016 to about 45 trillion yuan in 2024, and the number of transactions increasing from less than 100 million to nearly 2 billion. Meanwhile, the share of renminbi settlements in China’s goods trade has been steadily rising, closing in on 30% around 2024. This indicates that under the support of China’s trade network and industrial spillover, the renminbi is gradually gaining a larger settlement space.

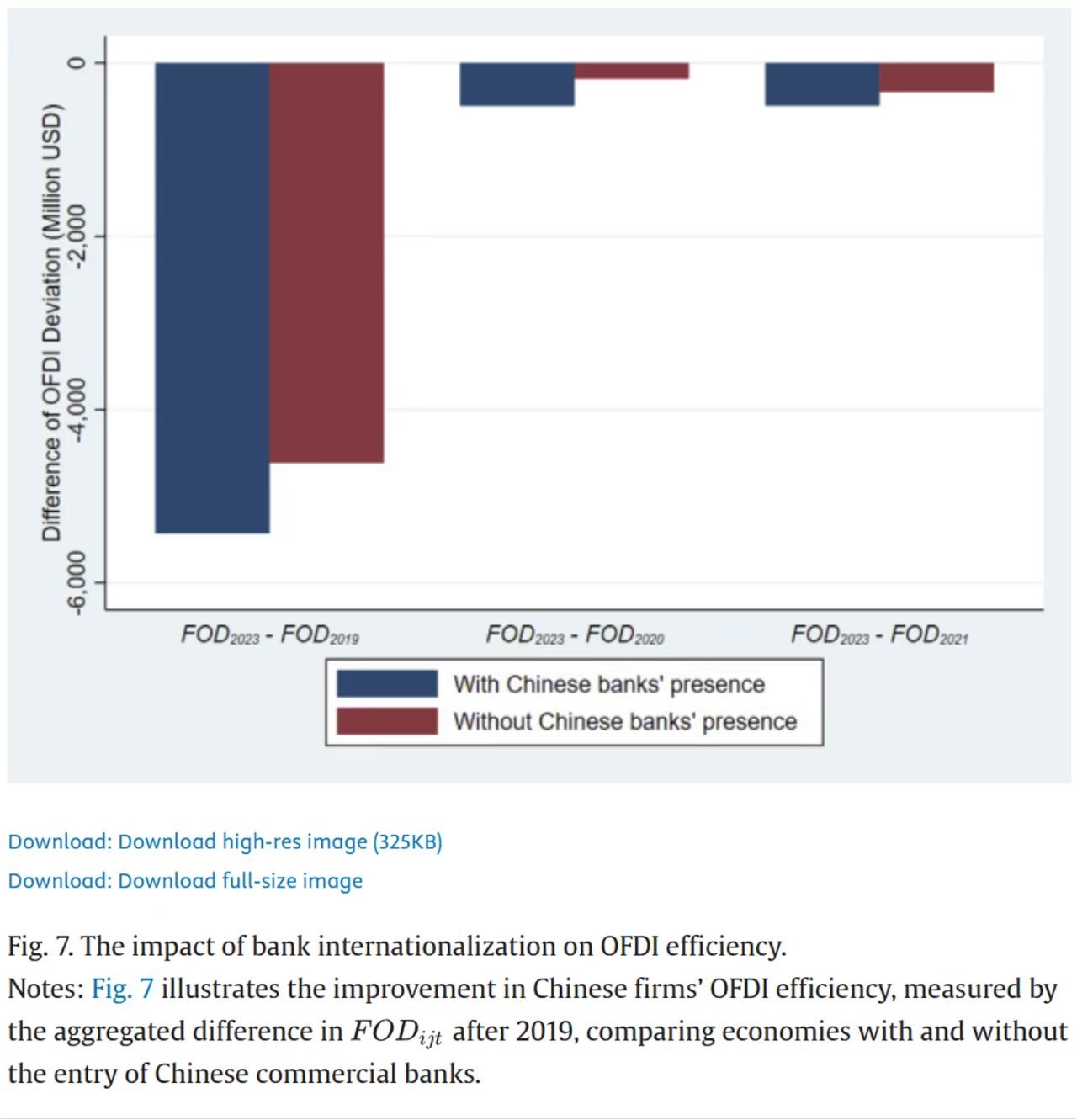

In the past, resource-rich nations had to first sell resources for dollars, then take those dollars to buy industrial goods because the dollar was not only the pricing currency but also the only highway for global trade and finance. Now, China is building new ramps, new service areas, and new toll stations right next to it little by little. As a result, you will see that increasingly more relationships between Belt and Road countries and China are no longer as simple as "exporting raw materials and importing finished products." Besides the goods trade itself, the expansion of China's banking sector's overseas branches is changing the financing and information structure between Chinese enterprises and host countries. Based on research covering 136 host countries and 1,035 Chinese enterprise samples from 2013 to 2023, the presence of Chinese banks' overseas branches can simultaneously enhance the efficiency of outward direct investment by Chinese enterprises through reduced credit friction and alleviated information asymmetries, especially impacting small and medium-sized enterprises and Belt and Road projects more significantly. In other words, many resource-rich nations, even if willing to engage in deeper industrial cooperation with China, often get stuck in barriers like financing, information, and institutional limitations; while financial infrastructures like banking, payments, clearing, and post-loan supervision, which may seem not grand enough, are transforming such cooperation from mere imagination into tangible reality. This implies that the integrated path of "transactions — financing — investments — returns" that the dollar once monopolized has now begun to show a somewhat asymmetric but increasingly complete alternative network.

Once such a network is formed, what it resets is not only the choice of currency but also the position of resource-rich countries themselves. For a country that has long been locked in the position of raw material exporter, the most crucial aspect is not whether the invoice states dollars or renminbi, but whether it can use the money earned from selling resources to build a railway, establish a power plant, initiate a smelting project, create a level of refining, or extend an industrial chain. If the answer remains negative, then even if it settles a few oil shipments in other currencies today, it’s merely a scratch on the shell of the petrodollar system; however, if the answer begins to turn positive, even if it hasn't completely escaped the dollar, it has already quietly developed a muscle within the dollar system that no longer fully obeys the old order.

Looking back at the U.S. itself, it is increasingly exposing its risks, which are appearing not just in its manufacturing sector but also in its capital markets. For a long time, the U.S. indeed possessed a capability that few other countries could match: it could continuously issue dollars to the world through trade deficits while simultaneously earning higher returns through financial channels. In other words, despite maintaining a constant trade deficit, due to its foreign asset returns historically being higher than the costs of its foreign debts, its net debt could continue to produce a positive return, forming what is termed as "golden debt."

If we break down this process, we can identify four stages. From 1977 to 1988, the U.S. remained a creditor nation overall, despite its merchandise trade deficit reaching $847.57 billion, financial channels provided investment income surplus of $788.51 billion leading to only a modest net increase of about $59.06 billion in net debt. From 1989 to 2002, the U.S. transitioned from a creditor to a debtor nation, yet financial revenues of $469.17 billion still offset a portion of its trade deficit of $2,901.01 billion. By 2003 to 2007, during the peak of the dollar's excessive privileges, the U.S. merchandise trade deficit soared to $3,508.17 billion, yet it secured a staggering $4,639.7 billion in foreign investment income, resulting in a net debt reduction. During this phase, the U.S. sold low-yield safe assets while allocating risk assets with higher returns globally. However, post-2008, the situation began to change: between 2008 and 2024, the U.S. net international investment position deteriorated to -$26,539.47 billion, while its net foreign debt surged by $25,260.64 billion, with trade and financial channels contributing equally to this decline. This means that the U.S. is no longer merely dragged down by trade deficits; financial returns themselves have also begun to fall short. This change is more visibly observed from the perspectives of yields and costs. From 1977 to 1988, the return on foreign assets was 14.1%, and the cost of foreign liabilities was 9.4%; from 1989 to 2002, asset yield was 6.1%, still surpassing the 4.7% liability cost; between 2003 and 2007, the yield on foreign assets peaked at 15.7%, far exceeding the 6.6% liability cost, and the net debt cost even expanded to -42.9%, meaning every dollar of net debt could yield nearly $0.43 of profit for the U.S., the most extreme form of "golden debt." However, post-2008, this structure flipped: the cost of foreign liabilities rose to 5.9%, while the return on foreign assets dropped to just 4.9%, turning net debt costs positive at 8.7%. In simpler terms, the U.S. began entering a genuine interest payment phase.

This development is extremely important. It signifies that the calmness with which the U.S. once operated—saying, "I owe the world money but can still make money from the world"—is gradually fading. The excessive privileges brought about by the petrodollar have not collapsed overnight, but their income structure has begun to decline. The U.S. can still issue bonds, still absorb global savings, and still hold the strongest supply capability of safe assets, but the costs of maintaining this system are evidently higher than before. Consequently, an interesting phenomenon has emerged: the U.S. today increasingly resorts to military means, tariffs, sanctions, and financial coercion, because it can no longer maintain order easily relying merely on financial attractiveness, institutional credibility, and market depth.

Adding to the trouble, all this compounds on the increasingly heavy double deficits that the U.S. is facing. Market research generally predicts that by 2026, the sum of the U.S. fiscal deficit and current account deficit will amount to around 11% to 12% of GDP. This means that today, the U.S. must maintain the deepest global capital markets, the strongest supply of safe assets, and the largest domestic demand market, while also pushing for re-industrialization, coping with rising interest expenses, sustaining security commitments to allies, and exerting influence simultaneously in the Middle East, Europe, and the Indo-Pacific. Under circumstances where "golden debt" has begun to fade, these burdens will not automatically lighten; instead, they will increasingly require external funds, external trust, and continued cooperation from surplus countries. The problem lies here: as Gulf capital ceases to flow back as naturally to U.S. Treasuries, as resource-rich nations and emerging markets start to develop new industrial and financial interfaces, and as China continuously enhances its capabilities in capital goods, equipment, engineering, and payment settlements, the U.S. will find it increasingly challenging to maintain the old order using previous methods.

The dollar was at its strongest when the world depended on it; it began to recoil when it realized it could not continue to depend unconditionally on the world. Today, the U.S. chooses brazen measures, coercing Venezuela, demanding sovereignty over Greenland, and now attacking Iran.

Many people, when interpreting this war, remain focused on the most intuitive energy security layer: the Strait of Hormuz is important, Middle Eastern oil is important, and Iran is a key variable. If the U.S. can control Iran, it can continue to control the lifeblood of global energy, and thus the petrodollar would naturally be secure. However, the issue is that the importance of the Strait only highlights the fact that the petrodollar cannot rely solely on the Strait of Hormuz for survival.

For the strait can ensure energy flow but cannot guarantee capital returns; navy vessels can protect shipping security but cannot automatically create long-term trust; bombings can temporarily deter opponents but cannot persuade the world to continue willingly parking its savings in American capital markets as before. For a truly stable order, the ideal state is never "I must frequently fire to remind others to obey," but rather "I do not need to fire, as others still believe staying here is the safest." The real advantage of the U.S. over the past decades has been precisely in the latter. It has not relied on incessant warfare to ensure the world holds dollars, but rather on capital market depth, institutional predictability, asset liquidity, industrial and technological advantages, along with the capacity to absorb global surpluses, making dollar assets a natural haven for the entire world.

Today, however, this once-trusted system is increasingly deferring issues that ought to reside in finance, trade, and reserve arrangements to the military-industrial complex to resolve.

What does this mean for resource-rich countries? It means you must think more seriously about where your wealth will continue to be settled and whether your energy exports should remain locked in a single pricing, clearing, and financing chain.

What does this mean for manufacturing countries? It means you must contemplate whether your industrial chain should continue to heavily depend on an order that could tie logistics routes, payment networks, and geopolitical conflicts together at any moment.

What does this mean for emerging markets? It means you must seriously consider if your development financing, equipment sources, technological interfaces, and digital infrastructure should be diversified, rather than placed entirely in the goodwill of the old order.

In other words, if the U.S. persists in tightly binding the petrodollar with military deterrence, it seems to be reinforcing the system while actually forcing more countries to consider how to weaken it. Gulf countries are more likely to keep capital locally, Russia will strive to reduce dependence on old financial channels, and nations like Iran, Turkey, Central Asian countries, Africa, and Latin America will be more inclined to accept support from China in terms of equipment, engineering, banking, and payment systems. Similarly, China will more naturally extend its trade networks, industrial capital goods, and renminbi settlement space.

Therefore, the true twilight of the petrodollar is not the sunset reflecting in the shimmering waters of the Strait of Hormuz but rather at the windows of every silent entrepreneur, politician, and citizen. The forces that truly shape the future do not reside in Washington's war rooms, nor in the shadows of fleets in the Persian Gulf, but in those silent construction sites. Among the solidifying steel frames in Saudi's future city, at the seams of Indonesia’s high-speed railway tracks, next to newly built reactors in Iran’s petrochemical parks, and in every Southeast Asian village lit up by high-voltage grids. There, there are no explosive rumbles—only the silence of solidified concrete, the soft clicks of gears meshing, and the hiss of electricity piercing light bulbs for the first time. Even if these sounds are too faint, easily drowned out by the roar of jet fighters, they are substantial enough to bend the brilliance of an old era.

The twilight of empires is always long and magnificent, filled with glowback military actions and financial coercion, but once the dawn of a new industry begins, it becomes irreversible. When resource-rich nations first truly touch the threshold of industrialization, when they realize they no longer need to use water bottles to contain their pink destiny, and when they learn to settle today’s transactions with local currency, resources, and future productive capacity rather than past debts, that last era—dominated by aircraft carrier battle groups and quantitative easing—will have ended with ease, without leaving a single echo as it sinks into the sea.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。