Authors: Alex Immerman & Santiago Rodriguez

Translated by: Deep Tide TechFlow

Deep Tide Insight: a16z used Revolut's 2025 annual report to analyze how a company achieving 76% CAGR in mature financial markets accomplished this. The numbers themselves are remarkable, but the growth logic behind them is even more worth reading: generating profit not reliant on interest margins, ROE is 3-4 times that of traditional banks, and user NPS is over double the industry average. Together, these elements tell a story that transcends that of a challenger bank.

The full text is as follows:

As growth stage investors, we often say that excellent companies speak through their numbers. Revolut, as a British company, is required to disclose its annual financial data, and its numbers are outliers—this is a conservative assessment:

Revenue grew by 46% to £4.5 billion

Pre-tax profit grew by 57% to £1.7 billion, with a profit margin of 38%

Retail customers grew by 30%, adding 16 million in 2025

Revolut penetrates all of Europe, with no single country accounting for more than 25% of fee income

Revenue is distributed across six business segments, with no single category accounting for more than 22%

11 product lines generate over £100 million each

Return on equity (ROE) reached 35%, a record level among peers (despite excess capital)

Revolut continues to maintain rapid and efficient growth—its "Rule of 75%" (revenue growth + net profit margin) places it at the top tier among modern and mature financial institutions.

Importantly, we believe that Revolut still has ample room for growth in both customer acquisition and monetization in existing markets. Not to mention the new markets that may yet be untapped—Revolut has just applied for a banking license in the United States, showcasing genuine global ambition.

This is not your grandma's new bank. Revolut has the potential to become one of the largest banks in the world. There is much to be done to reach that point, but we believe the foundation has already been laid.

Enough chit-chat, let’s get to the point.

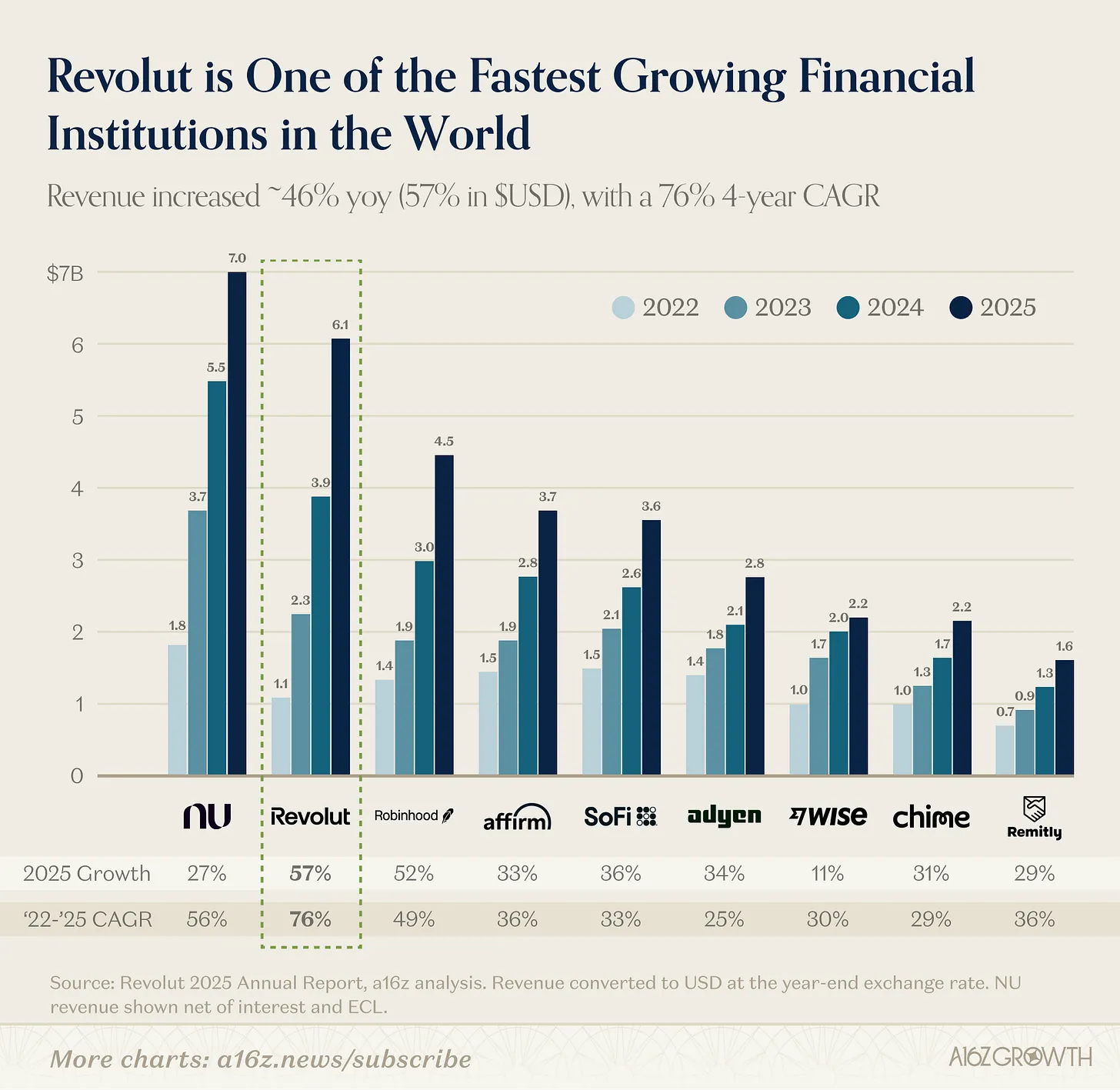

1. One of the Fastest Growing Financial Institutions Globally

Let’s start with revenue. Revolut's revenue growth is astonishing.

Alongside NU (Nubank), they stand in a distinct league compared to others in the consumer fintech industry (see the chart below). Since surpassing $1 billion in revenue in 2022, Revolut has achieved an astonishing compounded annual growth rate (CAGR) of 76% (70% in GBP terms) over the subsequent four years, making it one of the fastest-growing companies post the billion-dollar revenue mark. Given the extreme maturity of the consumer banking sector in Europe (as opposed to the developing markets where NU operates), this growth rate is particularly impressive.

Chart: Revenue converted to USD at year-end exchange rates; NU revenue is net after deducting interest and expected credit losses (ECL)

Source: Revolut 2025 Annual Report

For perspective: in 2022, Revolut's revenue was on par with or slightly less than any of Robinhood, Affirm, Sofi, Adyen, Wise, or Chime. Now, its revenue surpasses any of those well-known consumer fintech companies by 33% to nearly three times.

2. Breaking Down Revolut's Growth Algorithm: Six Horses in Sync

A key differentiator for Revolut is that it is no longer just a horse with one trick. It has multiple revenue drivers working simultaneously.

Revolut started by addressing a real pain point for Europeans: foreign exchange fees. With Revolut, Europeans traveling within and outside the Eurozone no longer face payment delays or the 5% fees charged by banks.

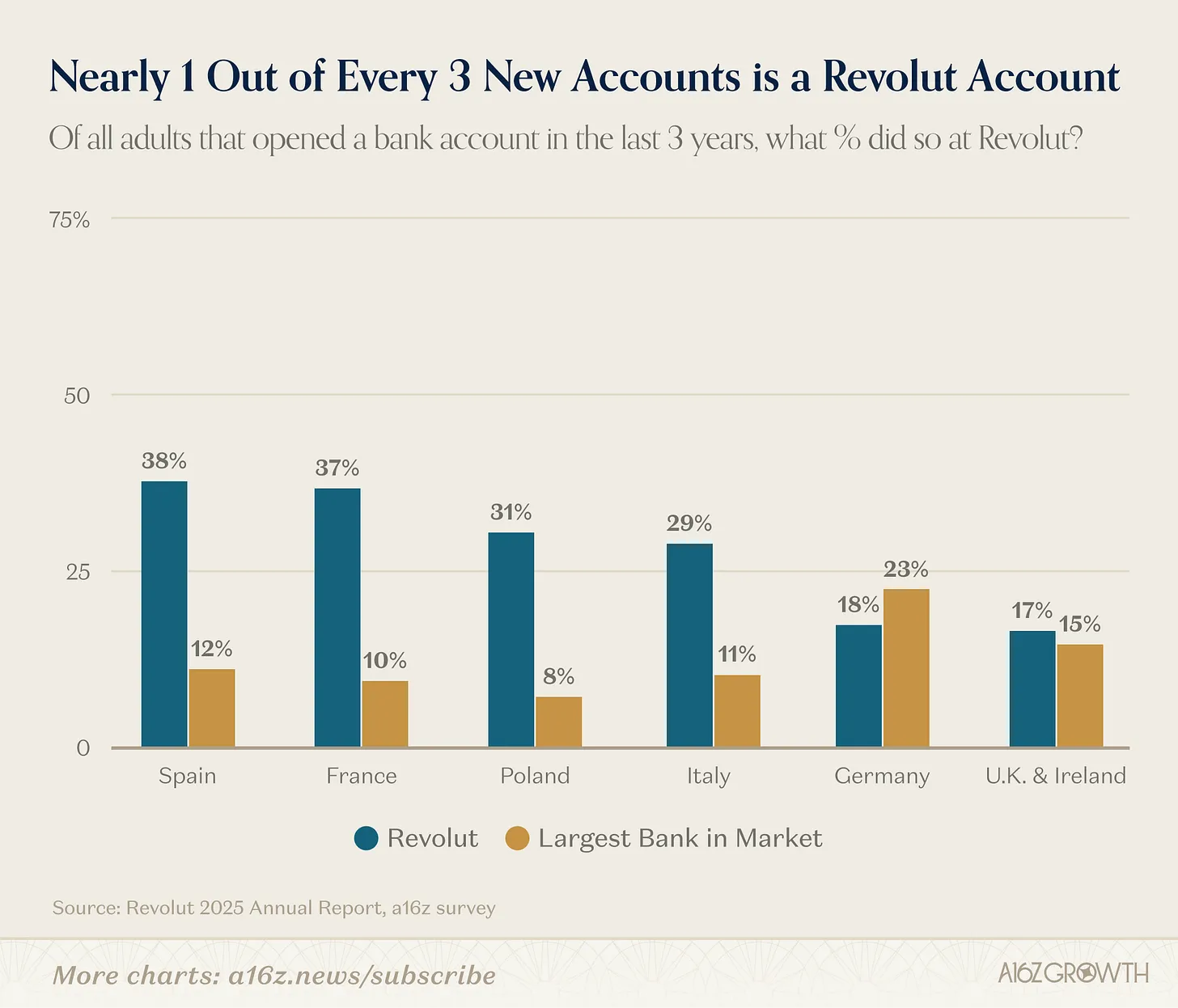

From a once-single product, geographically concentrated pain point solution, Revolut has grown into a fully functional personal and business bank. Now in Europe (Revolut's main operational area), approximately one in three new accounts opened chooses Revolut:

Chart: Survey conducted in key markets, using a sample of the general adult population; respondents indicated where they opened accounts and the time each account was opened

Source: a16z European Banking Survey, July 2025 (N = 3500)

One in five working-age individuals in Europe uses Revolut. Revolut's appeal across the Eurozone reflects the company's speed of product iteration and execution, which is truly remarkable.

Revolut has launched a complete suite of personal and business banking functionalities, driving growth in diverse European markets. Importantly, Revolut's product suite increasingly attracts users in the Eurozone who do not initially care about the foreign exchange value proposition. We could say Revolut's platform is "fully functional," but since Revolut continues to roll out new features, this description might underestimate it.

It's not just about the quantity of features and products, but also the quality of execution. Users love it. The company reported in 2024 that 65% of new users came through organic acquisition or referrals from existing users. Our research also shows that Revolut's user NPS exceeds twice the industry average.

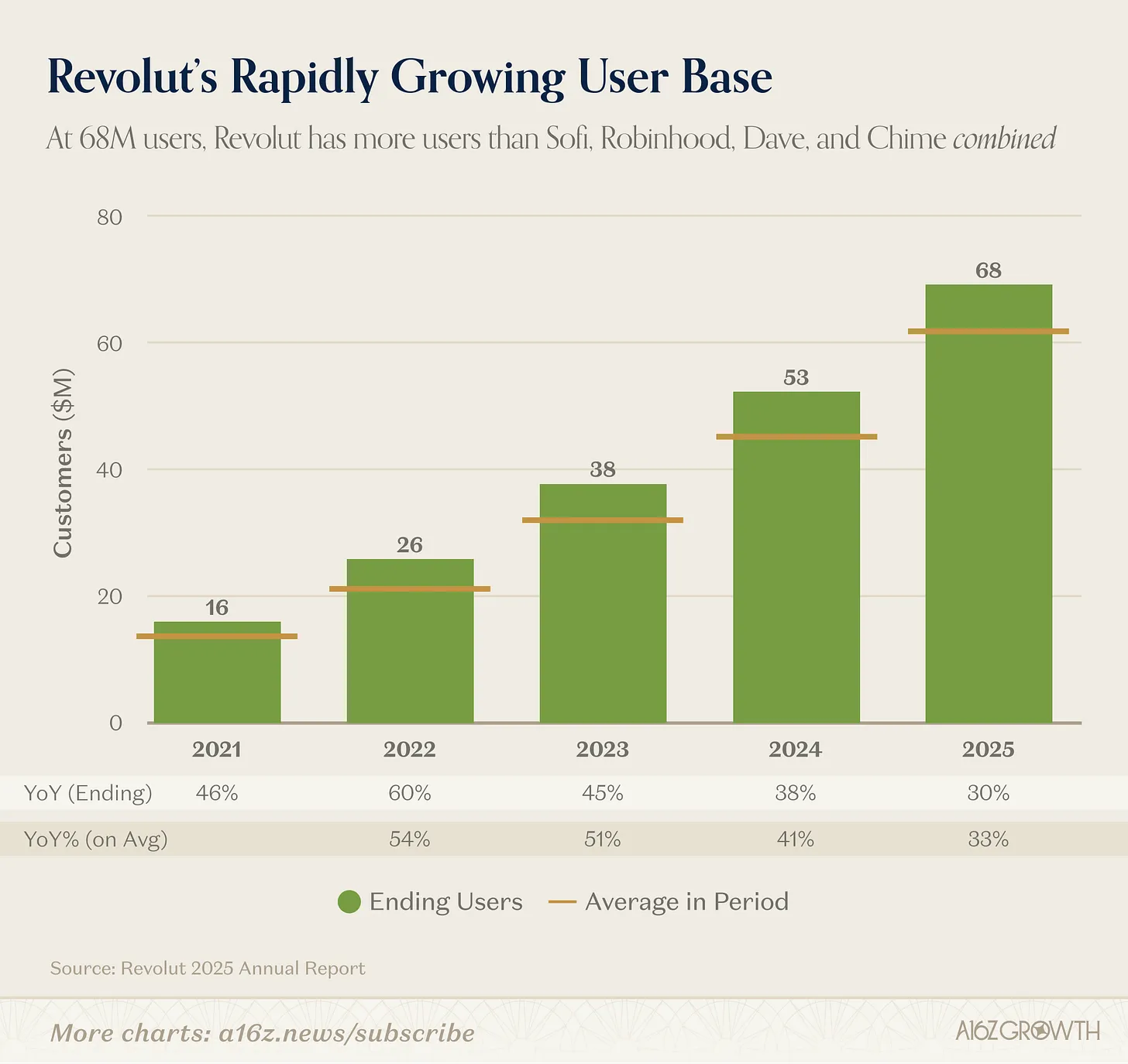

Overall, the user base continues to grow at a 30% compounded rate, reaching 68 million by the end of 2025.

Source: Revolut Annual Report

To understand the 68 million users in context: JPMorgan— the largest bank globally outside of China— has about 85 million consumer clients (over 70 million of whom are deemed "digitally active" users).

Indeed, while JPMorgan's total AUM places its scale far beyond Revolut's, from a purely user coverage perspective, Revolut is no longer just a "challenger"; it is a real competitor. Revolut's user count exceeds the combined total of Sofi, Robinhood, Dave, and Chime.

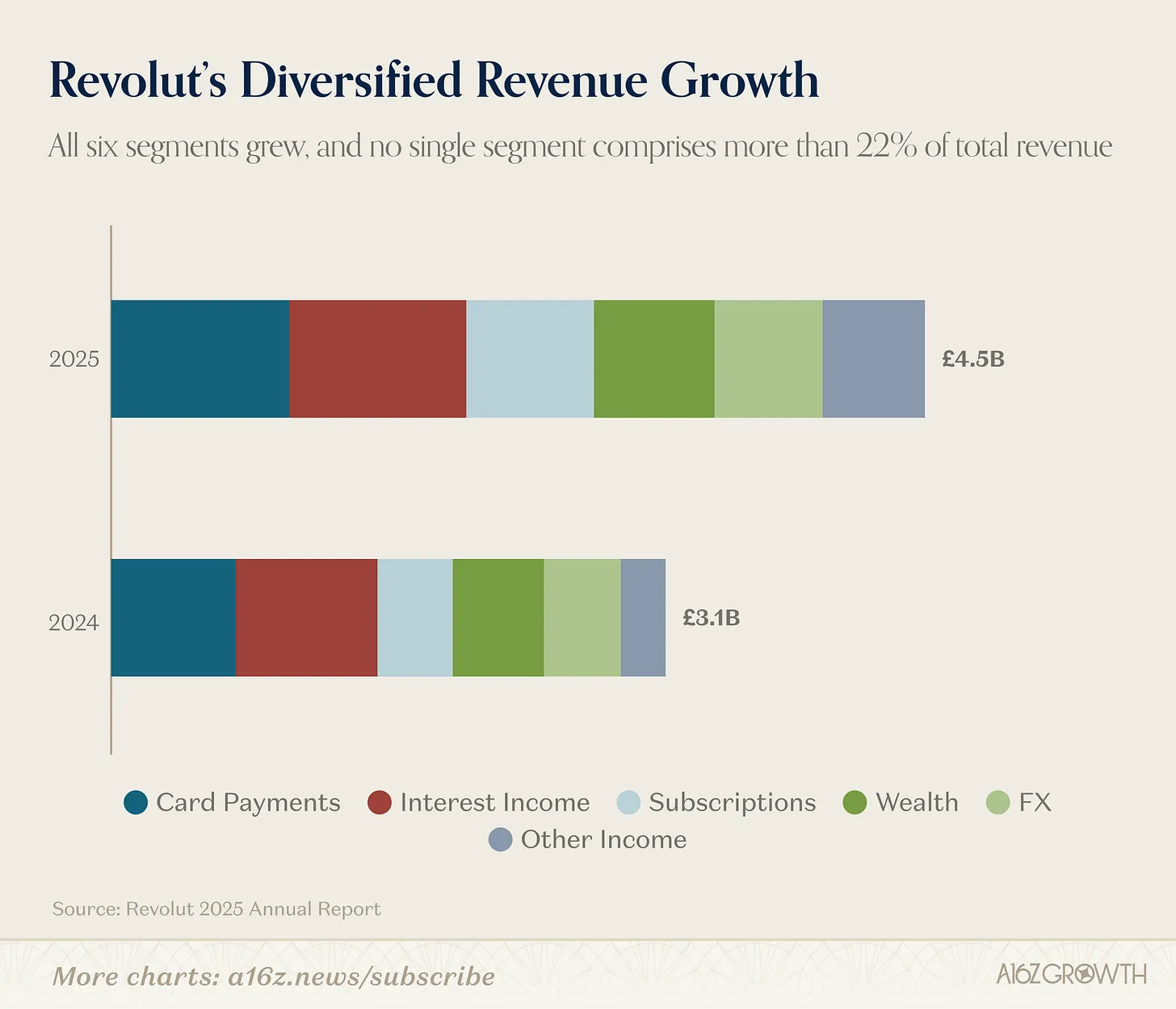

A complete product suite not only continually attracts more customers but also creates an increasingly diversified revenue structure:

Source: Revolut Annual Report

The company openly discloses six main sources of revenue:

Interest income

Card payments

Subscriptions

Other income

All six segments have grown year-on-year, with no single segment accounting for more than 22%.

The level of diversification of the business is even greater than what's reflected in this disclosure, as there may be multiple sub-products under each revenue stream (e.g., the wealth segment simultaneously includes public stocks and crypto assets). By 2025, revenue from 11 product lines each exceeded £100 million.

Importantly, 76% of revenue comes from fees, which is over 4 percentage points higher than in 2024, while interest income accounts for just under 22%. This stands in stark contrast to traditional banks that derive over 70% of their income from interest, and is also one reason why Revolut can achieve high ROE (discussed further below).

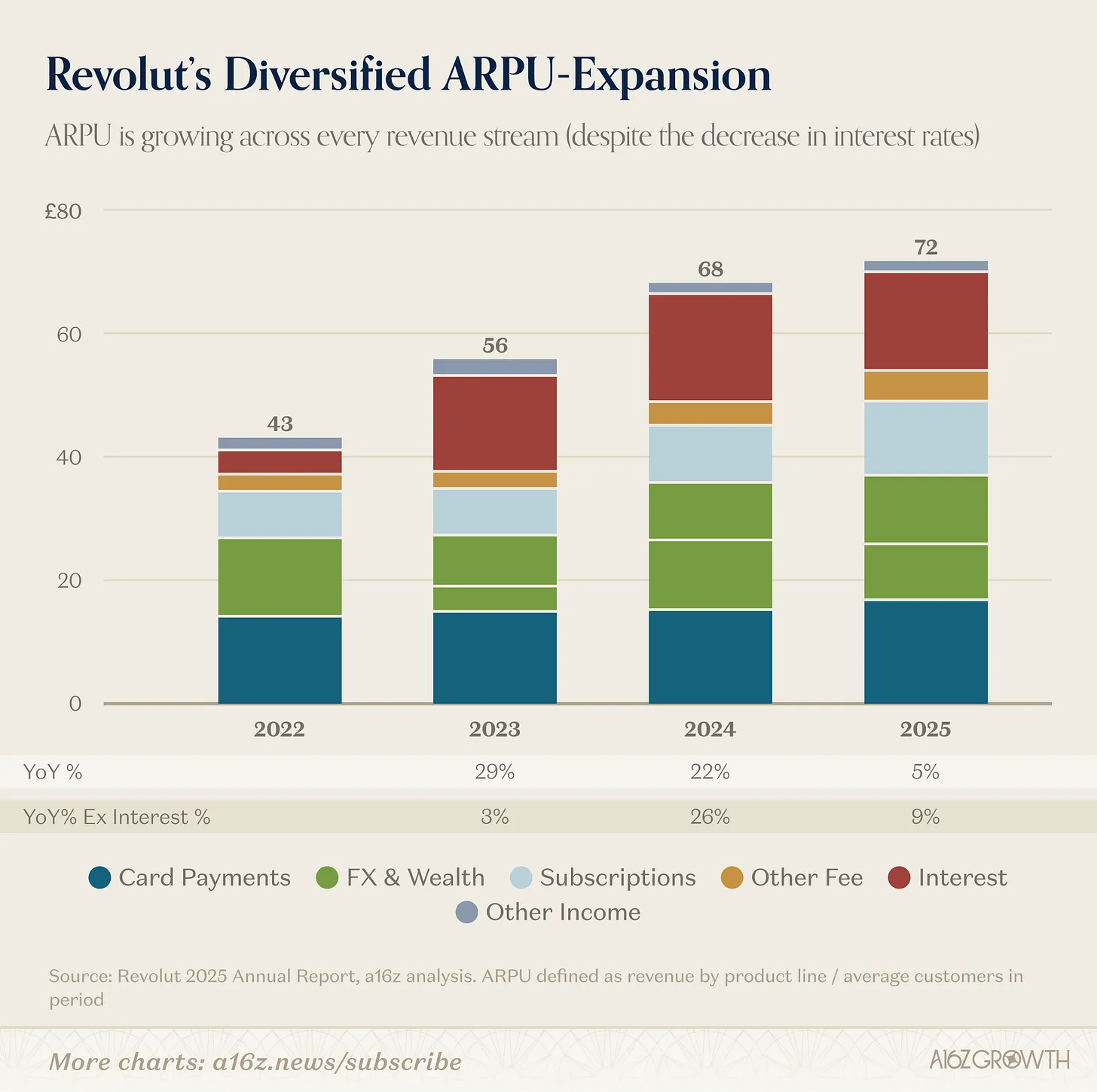

Not surprisingly, the diversified revenue structure has also brought diversified ARPU growth.

Chart: ARPU is defined as product line revenue/average number of customers during the period

Source: Revolut Annual Report

Since 2022, each disclosed revenue stream has achieved growth, with overall ARPU rising by approximately 65%, equating to an 18% annualized compounded growth rate.

The importance of diversification lies in its support for ongoing compounding and building risk resilience. In any given year, certain product lines may surge, while others may face headwinds (like last year's interest rate drops). But overall, continually acquiring wallet share through new product add-ons and core business can still drive strong ARPU growth.

3. Top-tier Efficiency

Revolut demonstrates rapid user growth, strong product iteration speed, and diversified revenue, and we have also delivered on efficiency as promised.

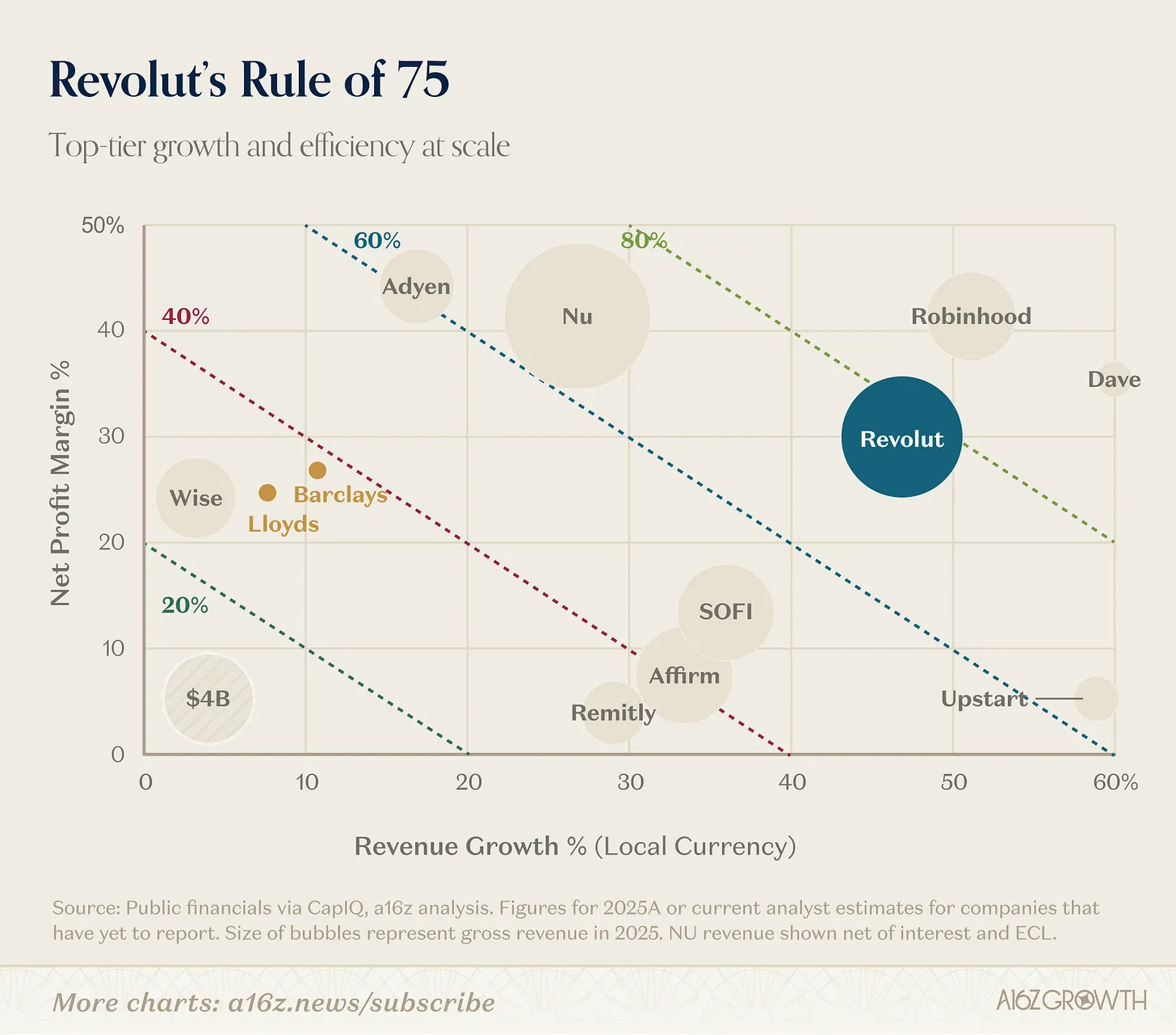

In 2025, Revolut achieved revenue growth of 46% and a net profit margin of 29%, with the "Rule of X" (growth rate + profit margin) reaching 75%. The "Rule of 40" is no longer sufficient!

Chart: 2025A data or current analyst forecasts for companies yet to release financial reports; bubble size represents total revenue for 2025; NU revenue is net after deducting interest and expected credit losses (ECL)

Source: Public financial data obtained through CapIQ, a16z analysis

This combination of growth and efficiency places Revolut in an extremely rare position—companies that achieve a Rule of 75% with revenues exceeding $1 billion are few and far between in history.

In fact, considering that both Robinhood and Dave's expected growth rates for next year are below 30%, Revolut may soon find itself standing alone at the top of the podium.

Efficiency is ingrained in Revolut's DNA. The combination of autonomously developed banking infrastructure, highly organic growth, and strict cost control has achieved a 29% net profit margin. With minimal physical branches, Revolut now has a meaningful cost advantage over traditional banks, which will continue to compound as scale expands.

AI is also further enhancing operational leverage. For instance, in customer service:

In 2024, Revolut's intelligent assistant chatbot reduced problem resolution time by 80%. In 2025, this improvement persists—retail resolution times dropped by over 40% and enterprise resolution times by over 50%, while user NPS increased by nearly 12 percentage points year-on-year. Revolut's intelligent assistant can now resolve over 75% of customer inquiries.

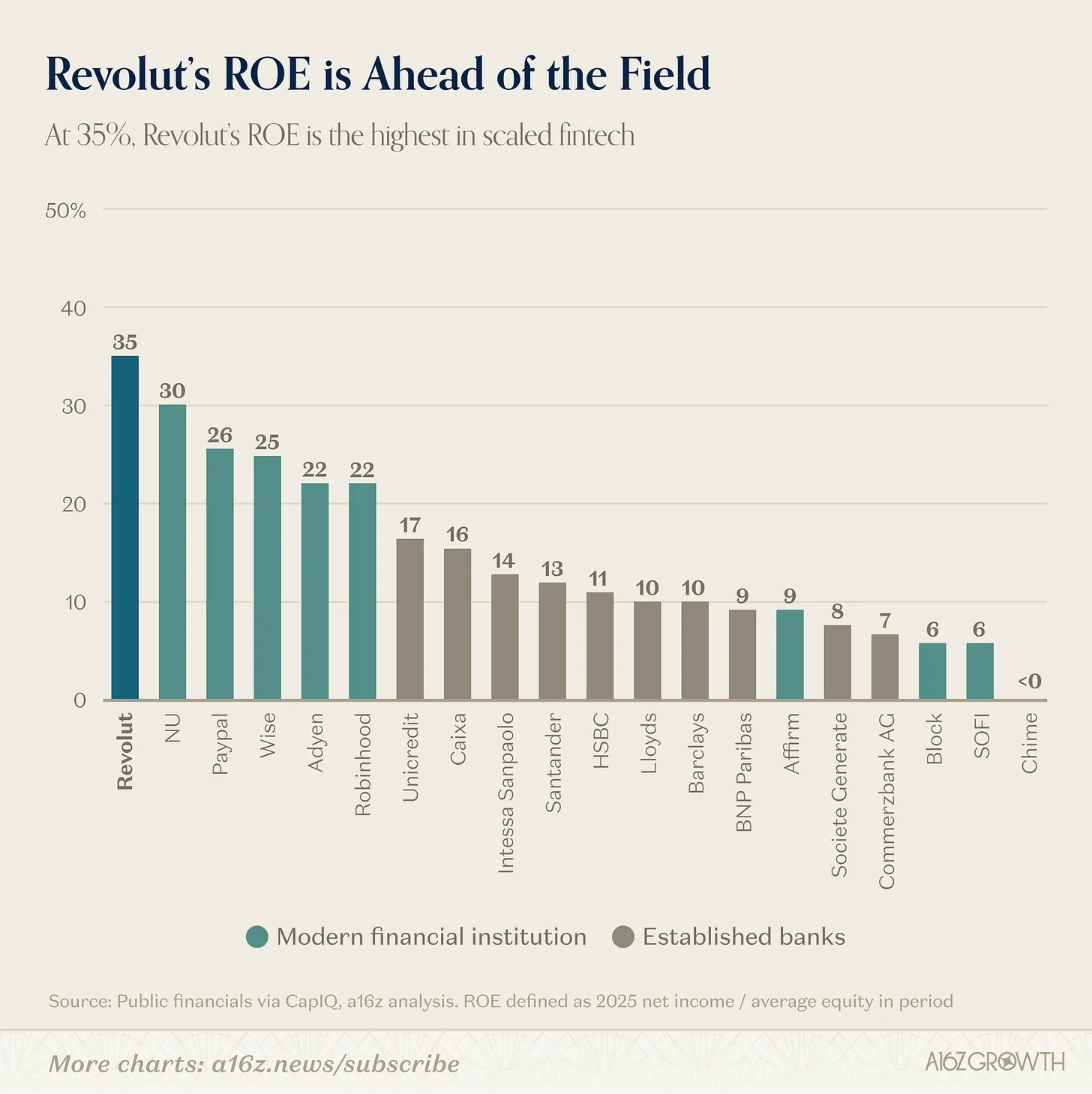

This efficiency has enabled Revolut to achieve the highest ROE we have seen in financial technology-scale enterprises (and it's continuing to improve). We have previously written about the importance of ROE for bank valuations, and Revolut exemplifies scale efficiency.

Chart: ROE is defined as net income for 2025/average equity during the period

Source: Public financial data obtained through CapIQ

Revolut's 35% ROE significantly surpasses other leading consumer fintech companies and is approximately 3-4 times that of mature banks. It's noteworthy that Revolut is in a "capital surplus" state (meaning reported equity exceeds what is required for bank capital), suggesting its "true" ROE may be even higher.

It is now rare to find growth that can achieve such capital efficiency.

4. Ample Growth Space: ARPU × User Count

Although Revolut's 2025 performance is impressive, we believe there is still a huge runway ahead. Returning to the company's core revenue growth formula (user count × ARPU), both variables have significant room to drive growth.

More Users to Acquire

The company reports a user count of 68 million by the end of 2025. As mentioned above, this number is substantial, but it accounts for less than 15% of Europe's (excluding Russia) approximately 450 to 500 million adult population. This doesn't even include Australia and Singapore (current markets), Mexico and Brazil (newly entered markets), the United States (just applied for a banking license), and more regions yet to be explored.

Revolut has many potential users to acquire.

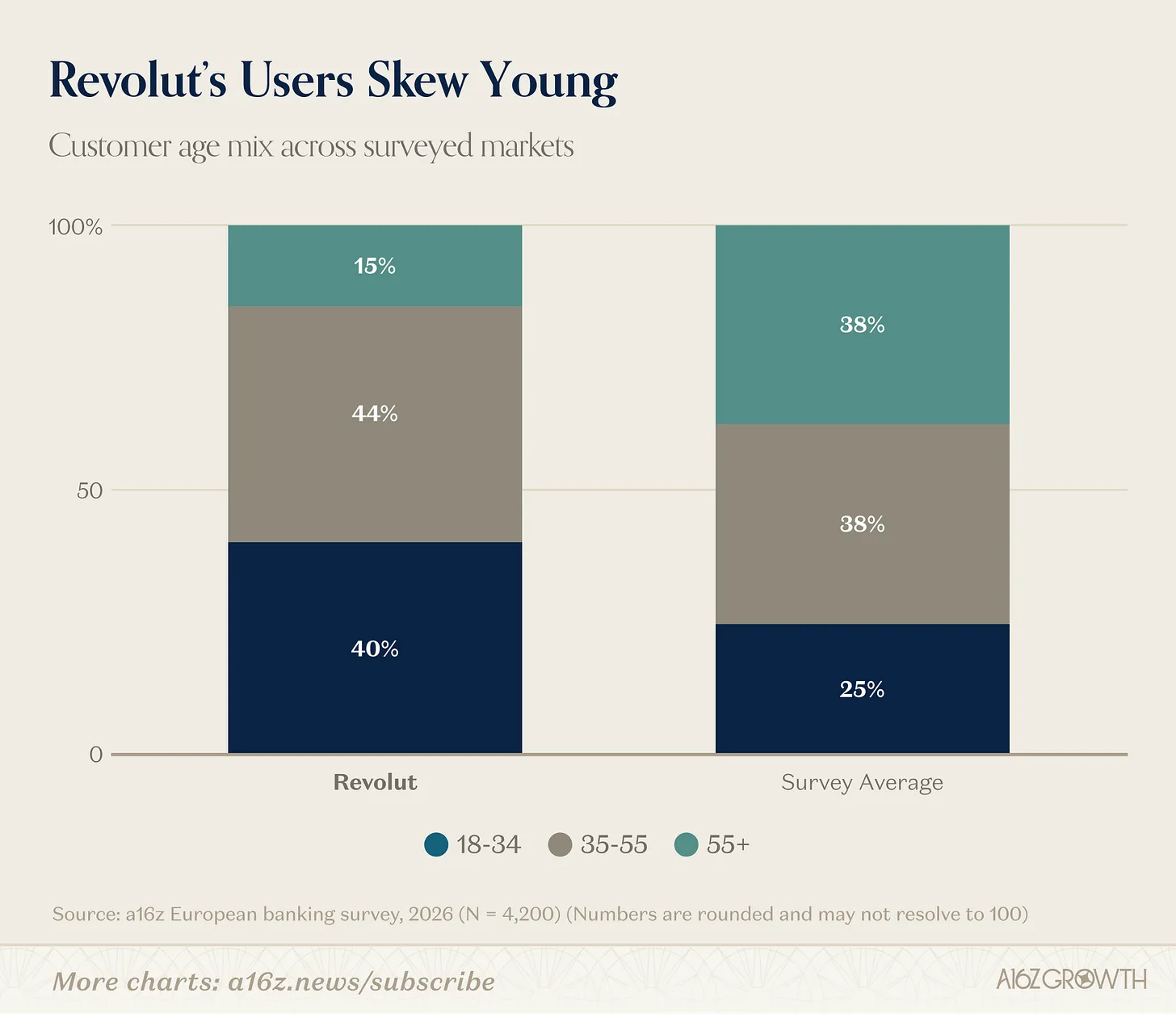

Moreover, the current user composition already indicates that the future will differ from the present. Unsurprisingly, Revolut users tend to be younger and more digitally savvy—we believe this demographic represents the eventual aspirations of the majority of the population.

Chart: Surveyed markets include the UK, Ireland, France, Spain, Italy, Germany, and Poland

Source: a16z European Banking Survey, February 2026 (N = 4200)

As Revolut continues to capture a significant proportion of first-time account holders (and persuades older demographics that the banking experience can be pleasant), market share should continue to grow.

Importantly, our research shows that approximately 25% of Revolut users under 35 consider Revolut as their primary account. Just this aspect alone, as these users age, will have a profound impact on the future market share in European banking.

ARPU Has More Expansion Potential

The other growth dimension, ARPU, has even greater potential.

Wallet share shifts in financial services typically occur over decades, rather than annually. Revolut continues to win user confidence: primary account users (according to company metrics) grew by 45%, exceeding the overall user growth rate of 30%.

The rapid growth of primary account users is crucial because, in terms of ARPU, "primary account" users are the prize:

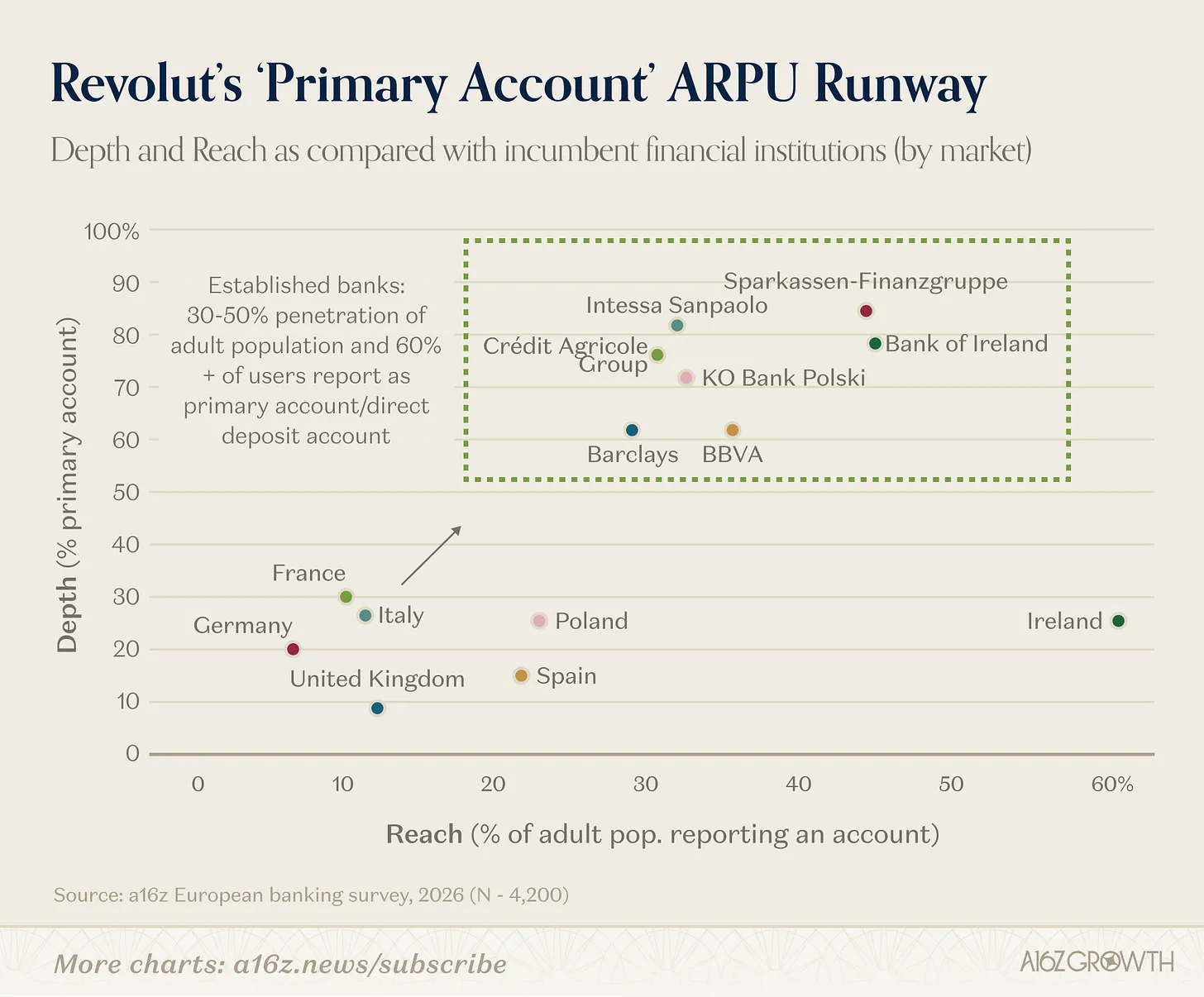

Our research indicates that traditional banking institutions with mature customer relationships can push their "primary account" share to over 60%.

Revolut primary account users report that their spending and savings on their primary account are about twice that of any other active account—and spending amounts tend to increase with age.

In short, more (and increasingly mature) primary account users can translate into higher ARPU, and if the traditional bank experience serves as a reference, Revolut's continually rising "primary account share" ceiling is quite high.

Another facet of growth in primary account relationships is the loan income opportunities that Revolut has yet to fully tap:

As mentioned earlier, Revolut currently derives 76% of its income from fees, while the typical proportion for mature banks is around 30%;

By the end of 2025, Revolut's loan-to-deposit ratio (LDR) was only about 6%, whereas mature banks typically operate at over 70-90% (about 4% if calculated on total customer balances). Loan balances are expected to grow about 2 times in 2025 and can continue to compound for many years.

Of course, stable loan growth takes time. However, if the ceilings of traditional banks can serve as a reference, Revolut has ample opportunities to significantly expand ARPU by leveraging its balance sheet to offer better loan products to customers. For comparison, a rough estimate for Barclays' UK consumer and commercial banking line's ARPU is around £435, approximately 6 times that of Revolut today.

Here is where Revolut stands in terms of coverage breadth (penetration) and depth (primary account share):

Source: a16z European Banking Survey, February 2026 (N = 4200))

Revolut has a substantial runway to continue advancing upward and to the right (particularly in Ireland) both by expanding its user base and deepening more relationships into "primary accounts." The latter should organically occur as the younger user base matures.

5. Conclusion: No Longer Just a Challenger

The importance of Revolut's 2025 numbers lies not only in their impressiveness but also in the complete picture they paint of a financial institution, rather than just a "challenger" bank.

User growth remains exceptional, monetization capability continues to expand, the adoption rate of primary accounts is rising, and even as the company continues to invest and expand rapidly, profitability is strengthening. This combination is exceedingly rare in financial services (and indeed any industry).

Execution challenges remain ahead—particularly in loans, regulation, and entering new markets—but after reading this annual report, we feel that the focus of the question has shifted from "Can Revolut become a scaled banking platform?" to "How big can this platform become?"

The company's publicly stated long-term goal is to "have 100 million daily active users in 100 countries." This journey is already underway.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。