Helium may become a key factor impacting the performance of companies like Nvidia, Samsung, and SK Hynix! 🧐

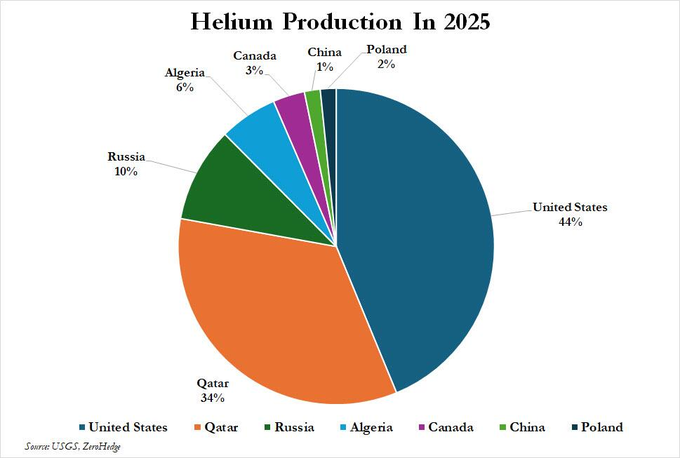

Helium is one of the "invisible oils" of the AI era, with semiconductors accounting for over 20% of global helium demand. According to helium supply data from 2025, supply is highly concentrated, with the United States accounting for 44%, Qatar for 34%, and China only 1%.

Many people feel that AI is abstract, such as code and computing power. However, in reality, the more advanced AI becomes, the stronger its connection and demand for the physical world.

Recently, the situation in the Middle East has escalated, and everyone is watching oil prices. In fact, the true grip on global technology is held by that colorless, odorless element, helium, which seems so far removed from us.

1️⃣ Helium: The "refrigerant" of semiconductors

Why would a helium shortage possibly lead to supply chain issues for Nvidia?

Cooling for 3nm: Advanced chip processes like 3nm use EUV lithography machines, which operate at extremely high temperatures, and only helium can provide an absolutely stable cooling environment.

Etching and cleaning: To etch circuits on wafers smaller than viruses, high-purity helium is required to drive the plasma.

Irreplaceability: Industrial-grade helium must achieve a purity of 99.9999%. Currently, over 30% of global helium comes from Qatar's Ras Laffan facility. Following two recent attacks, Qatar Energy announced "force majeure," with production halting directly and the repair period expected to take 3-5 years.

We are currently facing a deadlock; global AI demand is surging at an annual rate of 6%-8%, but 30% of the raw material supply has suddenly "physically dropped offline."

2️⃣ The East Asian trio: Who is "swimming naked"?

In this storm, Japan, South Korea, and Taiwan, the "three brothers of East Asia," are the most directly and severely impacted.

South Korea is particularly affected as a "storage giant," being the world leader in high-bandwidth memory (HBM), with SK Hynix and Samsung supplying the majority of storage chips for Nvidia.

However, South Korea currently relies on Qatar for 64.7% of its helium imports, with only six months of inventory on hand. Although the recovery rate has reached 80%-90%, the remaining 10% loss is essential. Once the inventory runs out, the production capacity for HBM4 will be halved. For South Korea, this is a critical issue; the total market value of the South Korean stock market is only $4.4 trillion, of which Samsung and Hynix together account for 40%, or $1.5 trillion. If these two heavyweights underperform, the South Korean stock market will face a severe shock!

Taiwan, known as the "king of chip foundries," is also precarious; while TSMC currently claims "minimal impact," this is merely a short-term illusion.

TSMC holds 90% of the world's advanced processes. Although they claim a recovery rate of up to 95% and are touted as "the most resilient," it's important to remember that Taiwan's energy is almost entirely dependent on imports.

Another potential crisis is that while the helium supplies from Taiwanese chip manufacturers can continue to be sustained through recycling for a while, if liquefied natural gas for power generation cannot be imported due to a blockade of the Strait of Hormuz, Taiwan's energy supply could be compromised, leading to real disaster. From current estimates, price increases for chips are a foregone conclusion.

Japan is an economy "gripped by the throat"; if Korea and Taiwan are "lacking materials," Japan is "deprived of resources."

Japan currently has a 100% dependence on foreign oil, with virtually no domestic production. The core supply relies on the Middle East, with 95% of crude oil and 80% of natural gas sourced from there.

Compounded by recent dual blows to the exchange rate, the yen has fallen to a 30-year low of 159 yen to 1 dollar. A quick calculation shows that for every $10 increase in oil prices, Japan must pay an additional 1.3 trillion yen annually. If oil prices surge to $150, Japan's GDP would directly face negative growth, even worse than the 2008 financial crisis.

In summary, this crisis reveals a harsh truth for investors: the more digitized the economy, the more fragile the dependency on physical resources.

In the past, we thought of energy as separate from technology. But in the year 2026, these two have merged into one; natural gas is converted into electricity to power server operations, and helium drives wafer fabrication to create chips.

Semiconductor recycling technology will become the core competitive advantage in the next two years.

Diversifying the helium supply chain (such as seeking alternative sources from Russia and the United States) will become a new battleground for major power competition.

The exchange rate pressures on the yen and won will long suppress the valuations of East Asian technology stocks.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。