The market demand for Pre-IPO assets is real, and the scale is enormous, but all existing supply-side solutions—whether closed-end funds, SPV tokens, or synthetic perpetual contracts—exhibit non-negligible structural flaws.

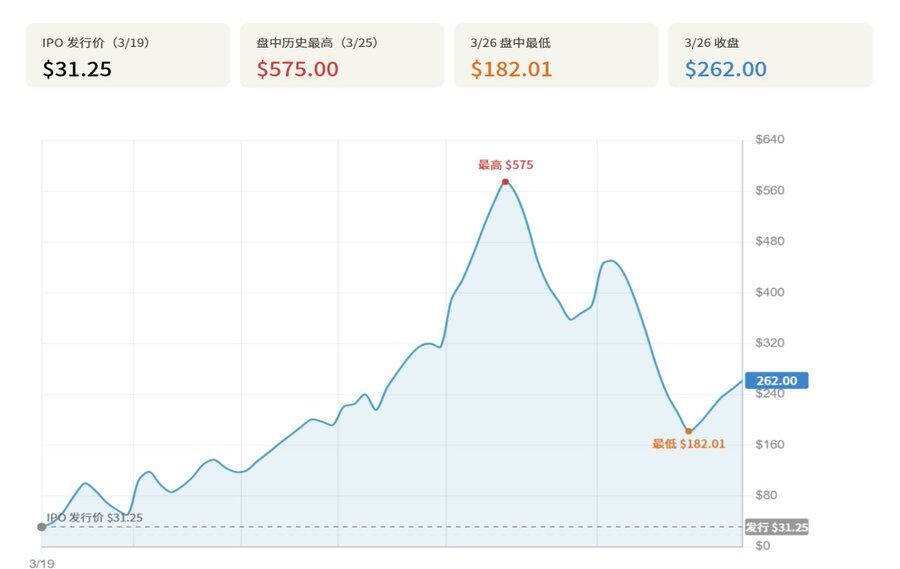

On March 19, 2026, the @fundrise Innovation Fund (NYSE: VCX) debuted on the New York Stock Exchange with an issue price of $31.25, reaching a peak price of $575 within seven trading days, an increase of 1,740% from the issue price, while its net asset value (NAV) per share maintained around $19, creating a peak premium close to 30 times. On March 26, short-selling firm Citron Research issued a short report and sent a letter to the SEC, causing the stock price to plummet by about 40% that day.

This article takes the $VCX incident as a core case study, analyzing six dimensions: holding structure, comparison with similar products, causes of premium, product nature, rights structure risk, and parallel paths in the crypto market.

The study suggests that the extreme premium of VCX does not arise from expectations of excess returns on the underlying assets but rather from the superposition of three structural factors: extreme scarcity of circulating chips (with non-locked shares just over 10%), high-intensity endorsement of the AI narrative, and institutional channels providing unequal access for retail investors. From the product nature perspective, VCX is essentially a financial instrument that sells access qualifications through a compliant shell, and its premium logic fundamentally differs from the @MicroStrategy flywheel mechanism, facing rapid pressure to bring the access premium to zero after the underlying company completes its IPO.

1. Event Overview: Soaring and Plummeting in Seven Days

On March 19, 2026, Fundrise Innovation Fund (NYSE: VCX) officially debuted on the NYSE, with an issue price of $31.25. The core selling point of this closed-end fund is simple and straightforward: it packages shares of top Silicon Valley private tech companies like Anthropic, OpenAI, and SpaceX into a financial product that ordinary investors can freely trade in the secondary market.

However, what transpired after the listing was likely unforeseen even by the issuer itself. On the first day, the closing price increased by 63%, and it continued to rise over the next four trading days, hitting an intraday historical high of $575 on March 25, a 1,739% increase from the issue price of $31.25. Bloomberg reported that by the close on March 24, VCX was priced at $314.99, while its underlying assets had an NAV of only about $18.97, resulting in a premium multiple of around 16.6 times between the two. By the time it peaked at $575, the market had granted a premium nearing 30 times the underlying assets.

VCX price chart within 7 days of listing (March 19 - March 26)

On March 26, renowned short-selling firm Citron Research announced its short position on VCX and published an article indicating that the fund's share price was still trading above $400 while its asset value was approximately $19, representing significant detachment. Citron also sent a letter to the SEC, requesting an investigation into whether Fundrise had continued to employ social media influencers, YouTube bloggers, and content publishers to pay for traffic to VCX—based on their previous penalty by the SEC for failing to disclose compliance after paying about $8 million to over 200 influencers in 2023. That day, the VCX stock price fell sharply, plunging about 40% from a previous closing price of $380 to around $226, with an intraday low of $182.01.

Key price points since VCX listing (data sources: Bloomberg, CNBC, investing.com, data as of March 26, 2026, compiled by Go2Mars)

2. Holding Structure: What Exactly Was Purchased

VCX disclosed its top ten holdings as of February 15, 2026, in its prospectus and on the fund's official website. The narrative logic of the whole portfolio is very clear: with Anthropic (20.7%) as the largest holding, supplemented by Databricks (17.7%) and OpenAI (9.9%), alongside high-recognition star projects like Anduril, SpaceX, and Epic Games.

However, the problems inherent to the holding structure are precisely the most direct irony of this premium. With VCX's NAV at about $19 as the baseline, if calculated based on the peak market price of $575 on March 25, the market was willing to pay about 30 times the premium for this batch of Pre-IPO equity. In other words, the price investors paid to buy VCX that day, when translated to Anthropic, implied a valuation premium that far exceeded its valuation in private financing, all occurring under a closed-end fund structure with extremely low liquidity and no direct redemption of holdings.

Top ten holdings of VCX (as of February 15, 2026)

3. Comparison with Similar Products: Similar Logic, Different Fates

VCX is not an isolated case. In fact, between 2024 and 2026, at least three closed-end funds or similar products that primarily held private tech company equities were successively listed in the U.S., and their market responses exhibited great variance.

DXYZ (Destiny Tech100) is the most comparable reference point to VCX. This fund was listed on the NYSE in March 2024 and initially faced excessive speculation from retail investors, rising above $100 at one point, while its NAV was only about $5, resulting in a premium near 2,000%. However, its subsequent trajectory has proven that such premiums cannot be maintained for the long term: as of March 26, 2026, DXYZ closed at about $29.8, with its latest disclosed NAV at $19.97 (as of December 31, 2025), a premium of about 50%, significantly narrowed from its peak. Its 52-week high was $50.50, still down about 33% compared to its initial peak.

Overview of Pre-IPO closed-end fund comparison (as of March 26, 2026)

RVI (Robinhood Ventures Fund I) represents another fate. In March 2026, Robinhood launched its closed-end fund product, priced at $25, with a scale of about $658 million. However, RVI immediately broke below its offering price on its first trading day, closing at $21, down 16%, marking a stark contrast to the frenzy surrounding VCX. By March 26, 2026, RVI was approximately trading at $32, with a premium of about 28%, but compared to VCX, the premium level is negligible.

The significance of this comparison lies in the fact that both are closed-end funds holding Pre-IPO equity, with the intensity of the AI narrative endorsement directly influencing the degree of market speculation.

- In VCX's portfolio, AI-related targets (Anthropic, OpenAI, Databricks) account for nearly 50%, which is the core reason it is highly sought after amid the current AI boom.

- In contrast, RVI's portfolio leans towards fintech and platform-based targets like Revolut and Databricks, with relatively thin AI concepts, naturally missing out on retail enthusiasm.

Citron Research provided a concise estimation framework for this: if VCX's premium ultimately compresses to DXYZ's current premium level of about 35%, the corresponding reasonable price for VCX would be about $26, representing a decline of over 93% from the peak of $575. This prediction does not represent a guaranteed outcome, but it accurately describes the risk of a closed-end fund's premium reverting from an extreme high back toward the average NAV.

4. Causes of Premium: Chips, Narrative, and Institutional Inequality

The extreme premium exhibited by VCX after its listing cannot be explained by a single emotional factor; rather, it results from the combination of three structural reasons.

The first layer is the extreme scarcity of chips. According to official information from Fundrise, by the time of VCX's listing, approximately 100,000 existing investors had accumulated, with shares held under a lock-up period of six months from the listing date and cannot be sold. According to a fund spokesperson's public statement, the shares in a non-locked state account for just over 10% of the total. This means that in the face of extremely active buying, the truly tradable circulating chips available in the market are very limited, and any marginal buying will have a magnifying effect on prices, pushing the stock price far above the NAV. This is a natural amplifier under special supply and demand conditions within the structure of closed-end funds.

The second layer is the high-intensity endorsement of the AI narrative. At the beginning of 2026, competition in the large model track intensified, with Anthropic launching the Claude smart body that can control users' computers, and OpenAI's valuation continued to rise, with the entire AI industry's high attention constituting the backdrop for sustained emotional output. VCX completed its listing precisely at this juncture, with Anthropic as its largest holding and OpenAI as its third-largest holding, effectively becoming a rare channel for retail investors to directly participate in top-level AI private assets. The scarcity was priced by the market at an extreme premium.

The third layer, and the most fundamental, is an issue of institutional inequality: those entitled to access the private equity market are selling to those who cannot enter at a premium. The underlying assets of VCX were obtained by Fundrise through institutional channels in the primary market or private secondary market, a domain only accessible to top VCs or qualified institutional investors; however, after these assets were packaged and listed by the fund, retail investors were not purchasing at primary market prices but were instead paying over 16 to 30 times the NAV premium on a already significantly inflated secondary market price. This is a perfectly legal structural inequality in terms of information and channels—institutions that hold the rights to acquire original assets convert them into a product that can be traded in the public market, selling it at the highest price the market is willing to pay to retail investors lacking pricing power.

5. Product Nature: Selling Access Qualifications Through a Compliant Shell

The analysis above reveals a core conclusion: VCX has achieved premium not because of outstanding asset selection or higher expected returns, but rather because it is selling access rights themselves. To this end, a question must be answered: what kind of product is VCX?

From a legal perspective, it is a closed-end fund registered with the SEC, with transparent holdings and compliant structures, essentially indistinguishable from any ordinary stock ETF on the market. However, from a functional standpoint, what it sells is not "expected investment returns" in the traditional sense, but rather an access qualification to the asset side—something only top VC institutions and qualified investors could previously touch—packaged into units that can be bought and sold on the NYSE.

Therefore, the market is willing to pay 16 to 30 times the NAV premium, essentially pricing this access right rather than assessing the future benefits of the underlying assets.

From this perspective, the comparison between VCX and MicroStrategy (MSTR) can illustrate the point well. On the surface, both are doing similar things: packaging hard-to-access scarce assets (Bitcoin/top Pre-IPO equity) into tradable securities for the secondary market, presenting a premium that far exceeds the underlying asset value. However, there are fundamental differences in their capital operation logic:

- MSTR funds itself by continuously issuing convertible bonds and preferred shares, then using that capital to increase its Bitcoin buying, giving it dynamic expansion capacity and the ability to maintain stock price premiums to a certain extent.

- VCX, on the other hand, is constrained by the structural limitations of closed-end funds: asset size is largely locked in after issuance, unable to continuously purchase new assets through refinancing, and the liquidity of holdings highly depends on the IPO or exit through acquisition of the underlying company. Once retail enthusiasm wanes, or after the six-month lock-up period, increasing circulating chips will put far more pressure on the decline of its premium than it will for MSTR.

Comparison between VCX and MSTR (Strategy) models

In other words, the premium of MSTR has a continuing capital mechanism to support it, while the premium of VCX primarily arises from chip scarcity and emotion-driven hype. This product logic itself has no inherent right or wrong, but the risks embedded in it are harder for the market to price correctly than those of ordinary closed-end funds:

Once retail investors buy in at prices far exceeding NAV, they are not actually paying for the value of the assets themselves, but rather a premium for access qualifications—which pressure to return to zero will be faced once the underlying company completes its IPO and a direct trading channel is established in the public market.

6. Beyond Premium: Access Barriers and Structured Exits

The structural issues here extend beyond the premium itself, with deeper risks resting on two points.

- First, the appeal of Pre-IPO assets relies heavily on their "not yet listed" status, rather than the intrinsic value of the assets themselves. Once underlying companies like Anthropic, OpenAI complete formal IPOs and enter the public market, the scarcity premium associated with existing closed-end funds will be rapidly erased—by then, prices for products like VCX will converge toward public market prices, and investors currently holding positions at a tenfold NAV premium will be exposed to significant risks of retracement, reflecting the historical trajectory of DXYZ.

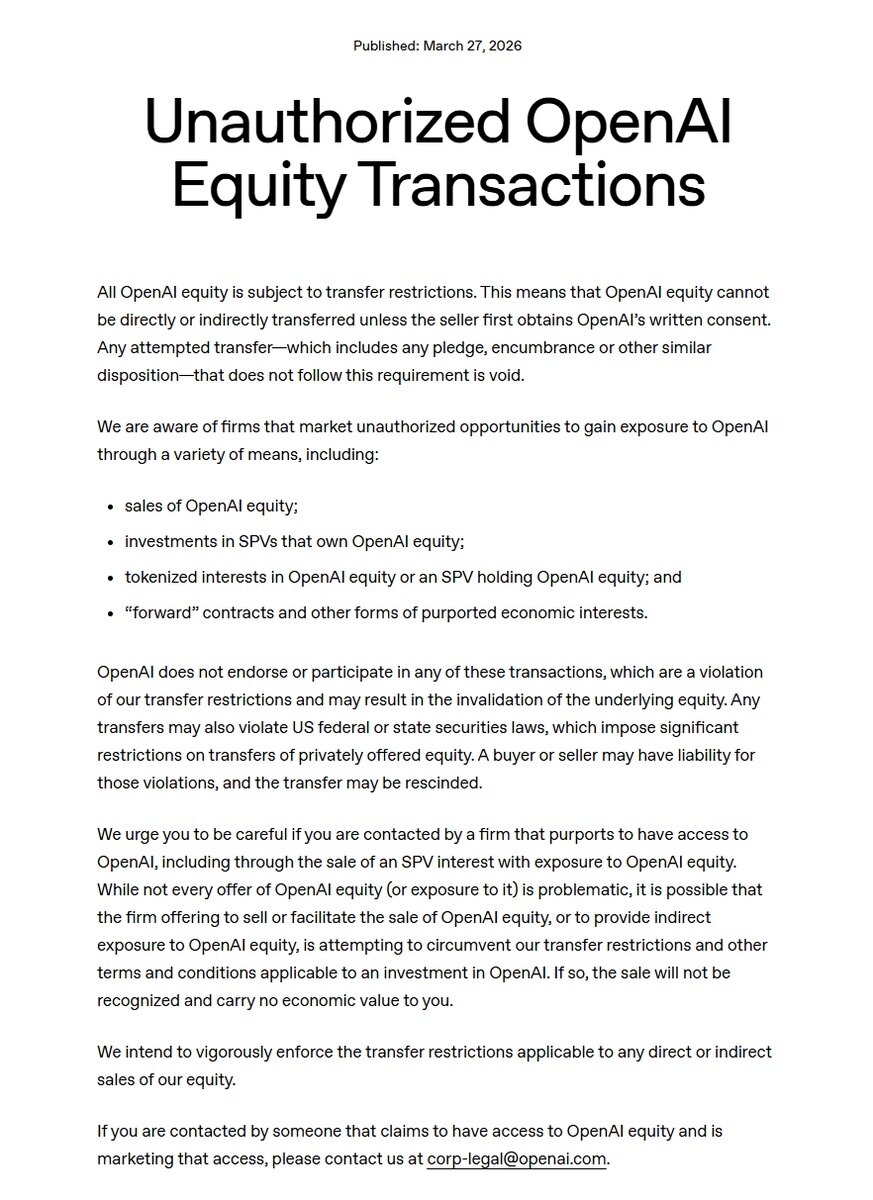

- Second, there is a more severe issue regarding the uncertainty of underlying rights. As shown in the image below: companies like OpenAI and Stripe have issued stark warnings, clearly stating that holding their equity through SPV structures violates transfer restrictions in shareholder agreements, and corresponding token or certificate holders are not recognized as shareholders on the company register. If the underlying company refuses to convert shares for relevant SPVs during future formal IPOs or denies recognizing their shareholder status, secondary market investors entering at high premiums will ultimately only hold contractual rights to an offshore SPV, not any meaningful company equity. This fragility in the rights chain is a structural risk that the current market sentiment severely underestimates.

OpenAI's official statement prohibiting equity transfers (https://openai.com/policies/unauthorized-openai-equity-transactions/)

From the phenomena discussed above, two key industry perspectives can be drawn:

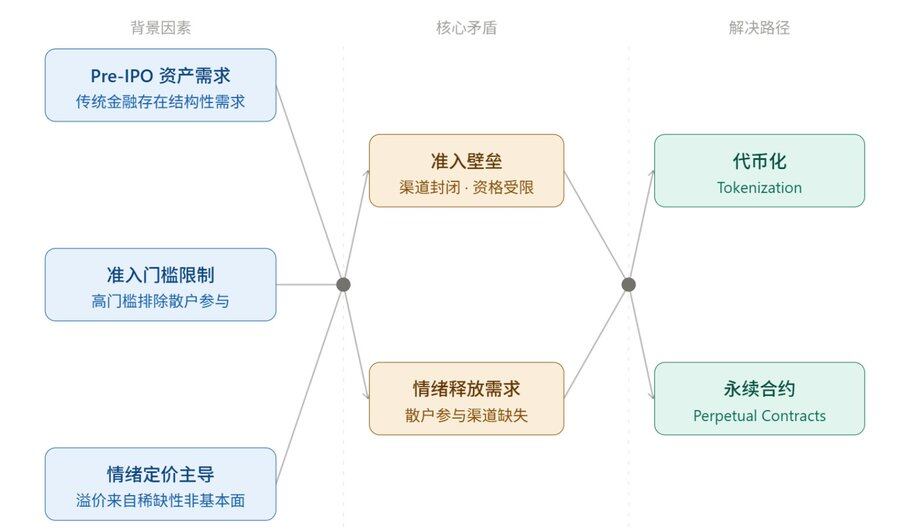

- First, there is indeed a massive real demand for early-stage high-growth assets within the traditional financial system, but constrained by existing compliance frameworks and structural dilemmas, this demand cannot be met efficiently and fairly.

- At the same time, the market's enthusiastic pricing of Pre-IPO assets is more of a payment for the entry barriers and liquidity premium before their listing, rather than purely based on the financial fundamentals of the assets.

Structural contradictions in the Pre-IPO market and potential crypto mechanisms for resolution

Against the backdrop where traditional financial channels struggle to resolve this supply-demand contradiction and regulatory friction, the tokenization mechanisms in the crypto asset space demonstrate significant potential for release: through tokenization and perpetual contracts, it is possible to bypass access barriers and structural dilemmas, facilitating the release of retail enthusiasm.

Return to Crypto Perspective: From Perpetual Contracts to SPV Tokenization

The VCX case illustrates the structural limitations of traditional financial channels in resolving the supply-demand contradictions and compliance friction of Pre-IPO assets, while the tokenization and perpetual contract mechanisms in the crypto asset space show the possibility of bypassing access barriers and releasing retail sentiment.

Ventuals: Perpetual Contracts for Valuation Exposure

@ventuals was built on the HIP-3 standard of Hyperliquid, allowing users to long and short the valuations of private companies like OpenAI (vOAI), SpaceX (vSPACE), and Anthropic (vANTHRPC), supports leverage of up to 20 times, and settles in USDH, which is pegged to the U.S. dollar. Its pricing mechanism directly maps valuations to contract prices, measured in units of company valuation divided by one billion. For example, if OpenAI's current valuation is $350 billion, then 1 vOAI would be approximately $350. What users hold is not any form of equity—the platform explicitly states that Ventuals contract holders do not own any form of economic rights to the target company, being purely speculative exposure to valuation changes.

In terms of scale, Ventuals has grown rapidly since its launch in October 2025. According to LorisTools, as of February 12, 2026, the platform's cumulative trading volume has exceeded $215 million, with 5,342 individual traders and over $70,000 in cumulative fees generated. Its cumulative trading volume surpassed $100 million on January 24, 2026, and further broke through $200 million within the next 17 days, nearing $400 million by March 26, 2026.

In terms of product nature, what Ventuals sells is not access qualification but a lighter and more hollow item—a contract bet on the direction of private company valuations. Holding a vOAI position does not grant users any legal rights over OpenAI, will not enter its shareholder register, and will not automatically convert into public market shares upon IPO. This is fundamentally different from VCX: VCX buyers at least hold real equity exposure registered with the SEC, while Ventuals holders have no claims on the target companies.

SPV Tokenization Platforms: Layered Dilution of Rights Chains

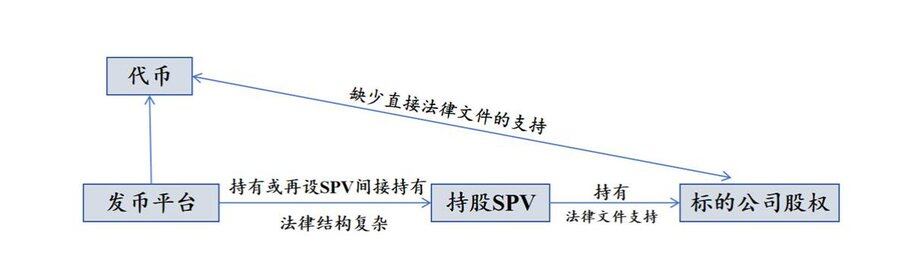

Beyond compliant paths like VCX and DXYZ, there are crypto market platforms operating Pre-IPO tokenization through SPV (Special Purpose Vehicle) indirect holding models, including Jarsy, PreStocks, and Paimon Finance. The architectural logic of these platforms is generally the same: they first acquire shares of target companies in the private secondary market, package them into an offshore SPV, and then tokenize the SPV's benefit certificates for sale to users, constructing tokenized exposure to companies like OpenAI, SpaceX, and Anthropic on-chain.

Structure diagram of SPV indirect holding tokenized Pre-IPO issuance (data source: Pharos Research)

The issues with this structure are concentrated in the nature of the assets held by users:

- The tokens held by users correspond to the benefit certificates of the SPV, not the equity of the target company itself;

- The SPV may hold fund shares rather than direct shares of the target company;

- The target company is often unaware of, or explicitly opposes, the existence of the SPV and its tokenization actions.

Thus, this constitutes a layered structural risk: on-chain tokens are a mapping of SPV benefit certificates, SPV certificates are a mapping of indirect equity, and the entire structure may not be compliant from the target company's perspective.

OpenAI and Stripe have both issued public warnings in 2025, clearly stating that such SPV equity holding practices violate transfer restriction clauses in their shareholder agreements, and token holders will not be recognized as legitimate shareholders. Robinhood faced an investigation by Lithuanian regulators after setting up an entity in Lithuania and launching OpenAI tokens in June 2025 following OpenAI's warning.

Horizontal comparison of main Pre-IPO exposure acquisition methods

The opacity of this layer of structure marks a clear distinction from VCX. As a closed-end fund registered with the SEC, VCX's holdings are disclosed regularly on its official website, with clear legal status; in contrast, SPV token platforms typically only show users proof of asset-side holdings (that SPVs do own equity), while the operational financial situation of the platform itself and the liabilities of SPVs remain largely opaque.

Horizontal Comparison: Different Pricing Logics for the Same Asset

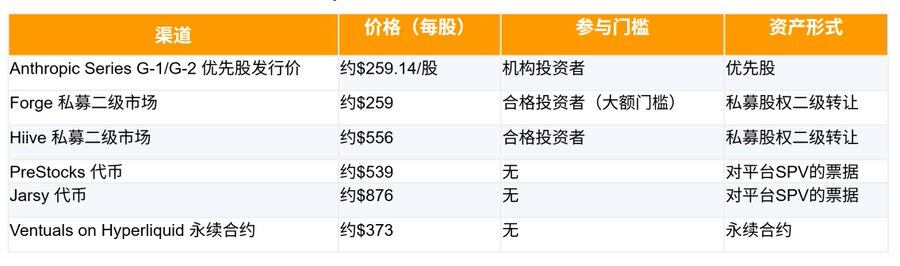

Using @AnthropicAI as an anchor, the pricing differences among the various channels mentioned above can be directly quantified. The reference price in the institutional primary market is about $259 per share, corresponding to the preferred stock issuance price of Anthropic's Series G round; Forge's private secondary market is roughly at parity, around $259, but with qualified investor thresholds and relatively high minimum subscription requirements; Hiive, on the other hand, has risen to around $556, existing over a double price difference with the institutional price, showing a clear stratification even in the private secondary market due to information channel differences.

Comparison of different channel prices for Anthropic (as of March 26, 2026) (Note: Ventuals' official price at this time was $547, but converted through the Ventuals mechanism was $373/share)

After entering the crypto market, the pricing logic further diverges from the underlying assets. Concerning equity in Anthropic, PreStocks tokens are about $539, Jarsy tokens are about $876, while perpetual contracts on Ventuals are approximately $373 (after conversion). These six price points correspond not to the same asset but to six different depths of access rights—from real preferred shares to SPV benefit certificates, to pure synthetic derivatives, with the rights chain progressively thinning, yet pricing does not diminish, and in some cases, even increases.

This phenomenon reveals a key structure: under the premise of high opacity in private market pricing, on-chain platforms are not simply marking up from a clear benchmark price; they are searching for arbitrage space within a fuzzy zone that already exists with a huge range. The over double price difference between Hiive and Forge illustrates that the so-called "private market price" has never been a single anchor; rather, the token pricing on crypto platforms is simply layering additional liquidity premiums and information asymmetries within this range.

From a trend perspective, there are a few noteworthy points.

- First, the ceiling on the access premium is determined by the scarcity of supply, rather than the quality of the assets. VCX's extreme premium largely arises from the product uniqueness on the NYSE. As RVI, DXYZ, and more similar closed-end funds enter the market, the monopoly advantage on the supply side will be continuously diluted; simultaneously, if key targets like Anthropic and OpenAI complete their IPOs, direct channels to the public market will become available, and the central premium will forcefully converge toward the asset NAV. The trajectory of DXYZ from nearly 2,000% down to around 50% confirms this logic.

- Second, the pricing discrepancies in institutional-level private secondary markets are the prerequisite for all premiums in this product category. The same asset class of the same company shows price differences of over double between Forge ($259) and Hiive ($556)—indicating that the so-called "private market pricing" has never been a single anchor but is a highly dependent interval based on information channels and access qualifications. On-chain token platforms are precisely looking for arbitrage within this interval, rather than applying a markup to a transparent price base.

- Third, the target companies' attitudes toward SPV structures will become the largest exogenous variable in this market. As the IPO expectations for Anthropic and OpenAI become increasingly clear, both companies have strong motives to clean their shareholder registers before going public and refuse to acknowledge the legality of SPV transfers. In such a scenario, whether SPV token holders can realize equity redemption at the IPO moment will shift from vague legal risks to concrete barriers to payment.

- Fourth, the regulatory arbitrage window for on-chain synthetic derivatives like Ventuals is narrowing. Currently, the operation of such products relies on major jurisdictions not having clear regulatory standards for private company valuation contracts. Once mainstream regulatory frameworks include them into the domain of derivative management, the structural advantages of the agreements will face direct compression.

- Fifth, the true sustainable evolution of the market depends on whether the target companies are willing to shift from passive response to active participation. Currently, all supply-side solutions are unidirectionally constructed under the premise of the target companies not participating or even opposing. If the target companies can actively participate in compliance token issuance or on-chain equity registration, access barriers may shift from arbitrage objects to cooperative restructuring institutional variables.

Conclusion: A Structural Dilemma Regarding Access Rights and Pricing Rights

The VCX incident unveils a collective pursuit of top AI assets by retail investors on the surface; however, at a deeper level, it reveals a long-standing structural contradiction within the traditional financial system: a barrier to entry jointly built by compliance frameworks and channel thresholds exists between private equity market high-growth assets and retail investors in the public market, and this barrier is being commercialized by various financial products in different ways.

From compliant closed-end funds like VCX and DXYZ to on-chain synthetic derivative protocols like Ventuals, and to SPV token platforms like Jarsy and PreStocks, the supply side is doing the same thing: repackaging scarce assets that institutional channels can access and selling them to investors lacking original access qualifications in some form. And this "some form" precisely determines the real value of the assets held by users at critical redemption nodes.

Three types of products, three different qualities of access rights, and three entirely different redemption expectations—yet these three differences have been almost completely overlooked by the market in the face of VCX's fervent $375 premium. This is likely the structural legacy that the VCX incident leaves for the next phase of this market to confront.

For the Pre-IPO market to reach true maturity, there is an inescapable structural premise: the target companies must actively participate in the design of issuance and circulation, rather than passively becoming the underneath narrative of various products. Only when companies like Anthropic and OpenAI are willing to clearly design and recognize some form of pre-listing participation mechanisms for different types of investors outside their IPO paths can this market transition from one-sided channel arbitrage to effective pricing through bilateral cooperation. This remains a critical point that all existing solutions have yet to achieve, and the true starting point for this market's eventual move toward regulation.

Original author: @xizhe_chan

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。