Written by: Donovan

Compiled by: AididiaoJP, Foresight News

Hyperliquid is a product of world-class quality. The team consists of only 12 people, generating $600 to $800 million in revenue per year, with customer acquisition costs close to zero, and has returned over $1 billion to token holders through a buyback mechanism.

However, based on a circulating market capitalization of $9 billion, does HYPE still have valuation attractiveness? What are the expectations represented by this price level for token holders?

To address these questions, I used a reverse discounted cash flow model to clarify the current market's implied growth expectations for HYPE, and then cross-validated the potential scale that the perpetual contract market might realistically achieve using a bottom-up valuation approach.

Reverse Discounted Cash Flow Model

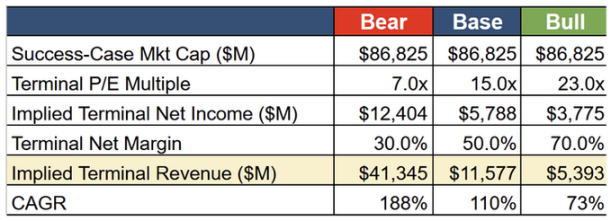

Under the assumption of a 30% terminal growth rate over four years, the current $9 billion market capitalization of HYPE implies the following information.

First, in the base case scenario (assuming a terminal price-to-earnings ratio of 15 times and a net profit margin of 50%), Hyperliquid's revenue needs to grow to approximately $11.5 billion by 2030. This means that with the current annualized revenue of $601 million as a base, the average annual compound growth rate over the next four years must reach 110%, a growth rate significantly beyond the normal range.

Such growth rates have no precedent in the development history of traditional financial exchanges. The Chicago Mercantile Exchange, Nasdaq, Intercontinental Exchange, and the Chicago Board Options Exchange have not achieved such organic high-speed growth within four years, even during their most rapid expansion phases. Fairly speaking, traditional financial exchanges are limited by regulatory and regional attributes, so their comparability to Hyperliquid may be somewhat limited, and this viewpoint holds some reasonableness. Taking Binance as the closest example, it achieved an average annual compound growth rate of over 200% from 2018 to 2021, enjoying the same advantages of no regulatory constraints and global market access that Hyperliquid currently possesses. However, Hyperliquid would still need exceptionally unique market conditions to replicate such growth.

Second, the model requires the overall potential market size for perpetual contracts to expand at a rate exceeding any comparable market. Currently, the global annual trading volume of perpetual contracts is approximately $95 trillion, with decentralized exchanges accounting for about 10% (around $7 trillion to $9 trillion). As of March 2026, Hyperliquid's market share in the decentralized exchange perpetual contract market is about 30%, corresponding to an annual trading volume of approximately $20 trillion. For the base case scenario's valuation to hold, Hyperliquid's trading volume needs to increase to $51 trillion per year (calculated as $11.5 billion in revenue divided by 2.25 basis points), which is about 25 times the current level.

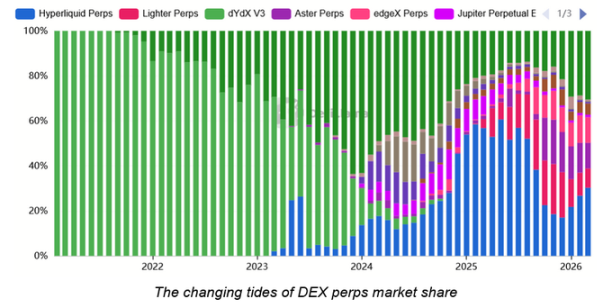

Lastly, such growth also requires Hyperliquid to maintain its dominant market share during this expansion process. Given the intense competition in the perpetual contract market, achieving this assumption is quite challenging. From past market patterns, different stages have exhibited different leaders—GMX and Synthetix in 2021, dYdX in 2023, and currently Hyperliquid, with frequent changes in market leadership.

Dynamic Changes in Decentralized Exchange Perpetual Contract Market Share

Hyperliquid's current profit margin exceeds 85%, and the team size is only a dozen people, reflecting a very high capital operation efficiency. However, such high profit margins also bring new competitive pressures, such as the emergence of projects like Aster and Lighter. Recently, Binance, Coinbase, and Kraken have successively launched equity and commodity perpetual contract products, directly entering the RWA perpetual contract market that previously drove Hyperliquid's growth. The distribution capabilities of centralized exchanges cannot be underestimated, as these platforms have hundreds of millions of verified users, a well-established institutional sales system, and asset-liability capabilities sufficient to sustain competitive rates over the long term. Hyperliquid has the corresponding coping mechanisms through HIP-3 and builder code mechanisms, but even in an optimistic scenario, as the cost of maintaining market share rises, its profit margin will face structural downward pressure.

Overall, the conclusion drawn from the reverse discounted cash flow model indicates that at a $9 billion market capitalization, HYPE's valuation level is high. The market environment implied by the current pricing requires sustaining a revenue growth rate that no historical exchange has achieved while relying on a market that has not yet reached the corresponding scale, and must depend on a moat that is already facing competitive erosion to maintain its position. While this scenario does not rule out the possibility of realization, for fundamentally oriented investors, it at least should be considered as the base case rather than the tail scenario, to form a reasonable basis for current buying.

Bottom-Up Valuation Model

To assess HYPE's reasonable value more prudently, we adopted a bottom-up valuation approach to explore the following question: What share of the global derivatives market can perpetual contracts occupy, and what proportion can Hyperliquid capture within this market?

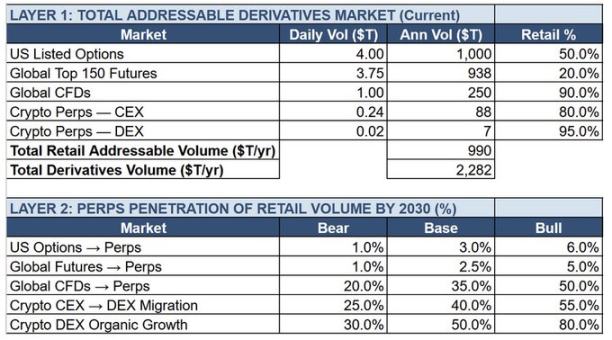

The core advantage of perpetual contracts lies in providing a simpler and more capital-efficient tool for investors pursuing directional leverage, with no expiration date, no need for physical delivery, and no reliance on brokers. By 2030, perpetual contracts are expected to absorb considerable trading volume from the following markets. According to the "Great Perpetualization" theoretical framework proposed by Syncracy Capital, the current size of major global derivatives markets is as follows:

- U.S. Options: approximately $1,000 trillion per year

- Global Futures: approximately $938 trillion

- Contracts for Difference: approximately $250 trillion

- Crypto Asset Perpetual Contracts: approximately $95 trillion (including centralized and decentralized exchanges)

The assumed penetration rates for these markets differ. We believe that contracts for difference are the easiest market to be replaced, as they also cater to retail speculative demand, whereas perpetual contracts structurally have advantages that can avoid the opacity and counterparty risks of over-the-counter brokers. The substitution difficulty for the options and futures markets is higher because institutional hedging users require expiration mechanisms and physical delivery, functions that perpetual contracts are difficult to provide; meanwhile, regulated futures exchanges have customer relationships and compliance infrastructure that decentralized exchanges find difficult to replicate.

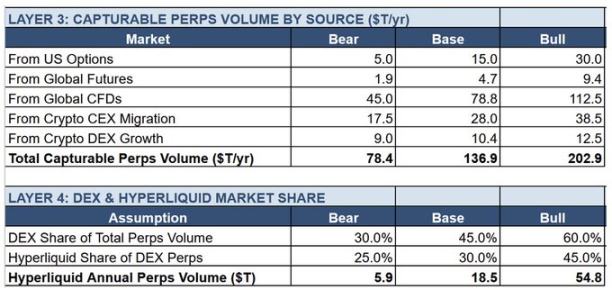

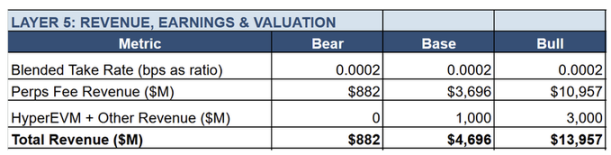

In summary, the base case assumes that by 2030, decentralized exchanges will account for 45% of the total trading volume of perpetual contracts (reflecting the ongoing trend of moving trading execution from centralized to on-chain), with Hyperliquid holding about 30% of that decentralized market share.

Under the assumption of a 2 basis point fee rate, Hyperliquid's revenue range in 2030 is expected to be between $4.7 billion (base case) and $14 billion (optimistic case).

The realization of the base case is somewhat feasible but requires meeting multiple conditions: the overall potential market size for perpetual contracts expands as expected; Hyperliquid maintains its market share; profit margins remain stable; and HyperEVM's annual revenue grows from the current $800 million to $3 billion (implying growth driven by HIP-4 predicted markets). If any of these conditions fall short of expectations, it will result in a pessimistic scenario that cannot support the current valuation.

Conclusion

In summary, the analyses from both models show that HYPE’s current market price has basically reflected most of the positive factors, with limited margin of safety.

In the base case scenario, there is about a 2.5 times gap between the $11.5 billion revenue required by the reverse discounted cash flow model and the $4.7 billion derived from the bottom-up model.

The current price can only be supported in an optimistic scenario, where the $14 billion revenue derived from the bottom-up model is significantly above the $5.4 billion revenue threshold of the reverse discounted cash flow model. However, this optimistic scenario requires the simultaneous realization of the following conditions: decentralized exchanges capture a 60% share in the rapidly expanding perpetual contract market; Hyperliquid maintains a 45% share in that market; HyperEVM revenue grows from the current $800 million to $3 billion.

It should be noted that the reverse discounted cash flow model is quite sensitive to the 30% return assumption. If investors are willing to accept lower return requirements, the valuation conclusions will change significantly, as shown in the table below.

Under the 30% return assumption, the base case indicates that the current price has accounted for most of the expected value. What investors obtain at the current price level is mainly the potential gains from the right-side tail scenario, and they have paid a fairly reasonable price for this.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。