1. Market Focus Interpretation

Last week, the core driving factor for the market was the severe escalation of the US-Iran conflict, with the Strait of Hormuz facing substantial threats, causing WTI crude oil prices to surge nearly 17% during the week, reclaiming the $100 mark. This also triggered strong inflation expectations, leading to rising US bond yields, which heavily impacted high-valuation technology stocks. The US dollar index broke through the 100 threshold, suppressing gold's gains. Cryptocurrencies, as high-risk assets, faced significant sell-offs, with weekly declines exceeding 6%. As the US-Iran conflict entered its fifth week with no signs of resolution, the selling tide continued. Last week's volatility and uncertainty indicators reflected the current macroeconomic tone. The VIX index closed at 31.05, reaching the highest level since the outbreak of war; meanwhile, CNN’s Fear and Greed Index fell to the "extreme fear" level, the lowest since November of last year. The bond market further adjusted pricing, with the 10-year US bond yield rising to 4.44%, and the 30-year US bond yield briefly exceeding 5%, before retreating to just below that level. This trend reflects the market's deeply entrenched expectation that "high interest rates will persist for a longer time," with the current market generally believing that the likelihood of the Federal Reserve lowering rates before autumn is minimal, while the chances of a 25 basis point rate increase this year are about 25%.

2. Liquidity Analysis

2.1 Net Fund Flows of Crypto ETFs

In the past week, crypto ETF fund flows showed a clear "outflow followed by recovery" structure: midway through the week, funding sentiment weakened rapidly, with spot ETFs seeing a total net outflow of approximately $500 million, including around $296 million outflow in BTC and about $207 million in ETH, with selling pressure mainly concentrated on March 26-27, indicating a clear phase of risk reduction by institutions. Over the weekend, there was marginal inflow back into gold, ending the trend of continuous outflows. Overall, institutional funds are still mainly cautiously allocated under macro uncertainty.

2.2 TradFi Liquidity

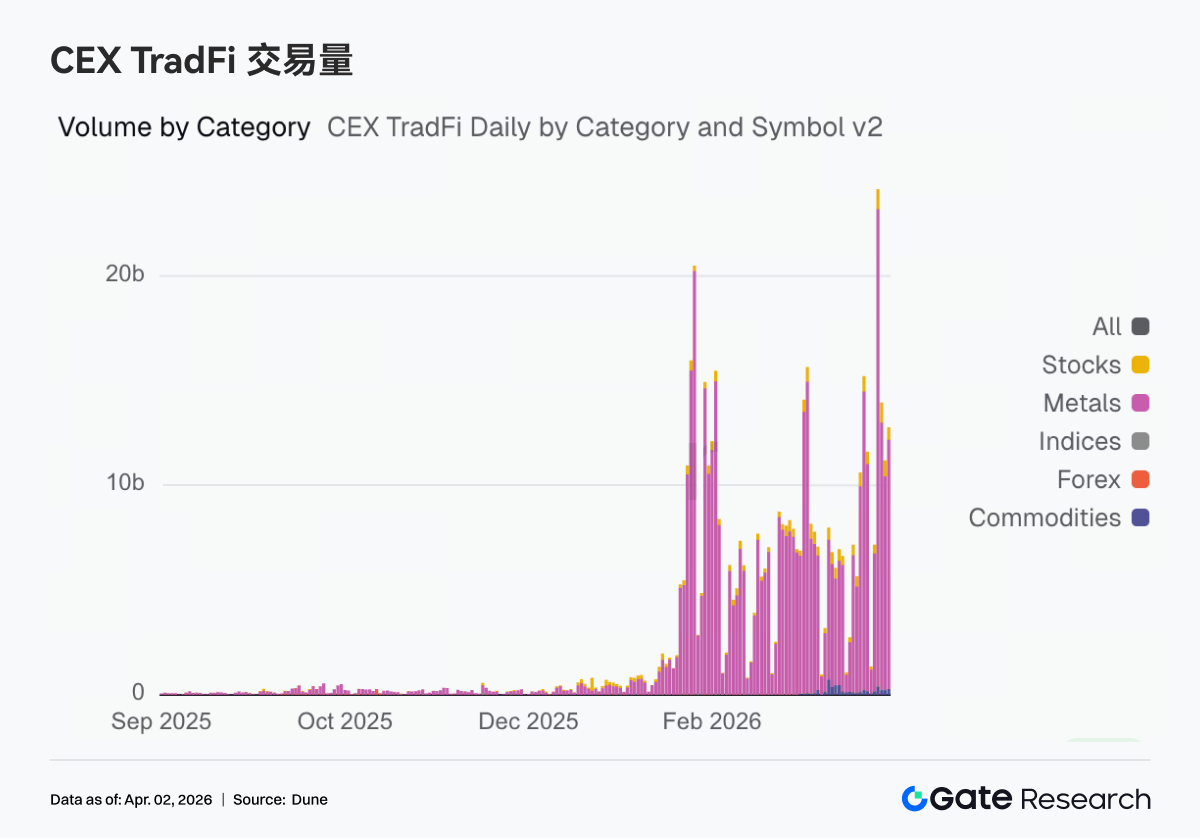

In the past week, on-chain trading remained focused on macro asset volatility. The Perp DEX TradFi trading volume increased to $17 billion, with crude oil trading still holding the highest weight but continuously decreasing month-on-month, while gold's share rose again. On CEX, TradFi perpetual trading volume soared, with March 23 trading volume hitting an all-time high. Each sub-category showed significant growth, with commodities and metals showing the highest month-on-month increase.

In the past week, the market depth change of PAXG exhibited a structural characteristic of "weak to strong, with tail volume expanding." At the beginning of the week, Delta was mainly negative, compounded by prices retreating from high levels, indicating that the market was predominantly net sellers, with liquidity inclined to withdraw; then around March 23, a round of concentrated selling pressure emerged, causing prices to plunge quickly, forming a temporary liquidity vacuum. By the weekend, the depth structure significantly improved, with Delta turning to a consistently positive value and expanding significantly, indicating that funds began actively participating and driving prices higher.

In the past week, the number of TradFi asset categories further expanded, with the total number in three major CEXs within TradFi asset categories (only counting TradFi and CFD sectors, excluding perpetual contracts) increasing from 598 to 619, a month-on-month growth of 3.5%. Among them, the growth in metal categories was most significant, rising from 22 to 31, a 40% month-on-month increase; overall, only Gate showed growth in TradFi asset categories last week.

3. On-Chain Data Insights

3.1 DEX Trading Cooling, Meteora Maintains High Levels

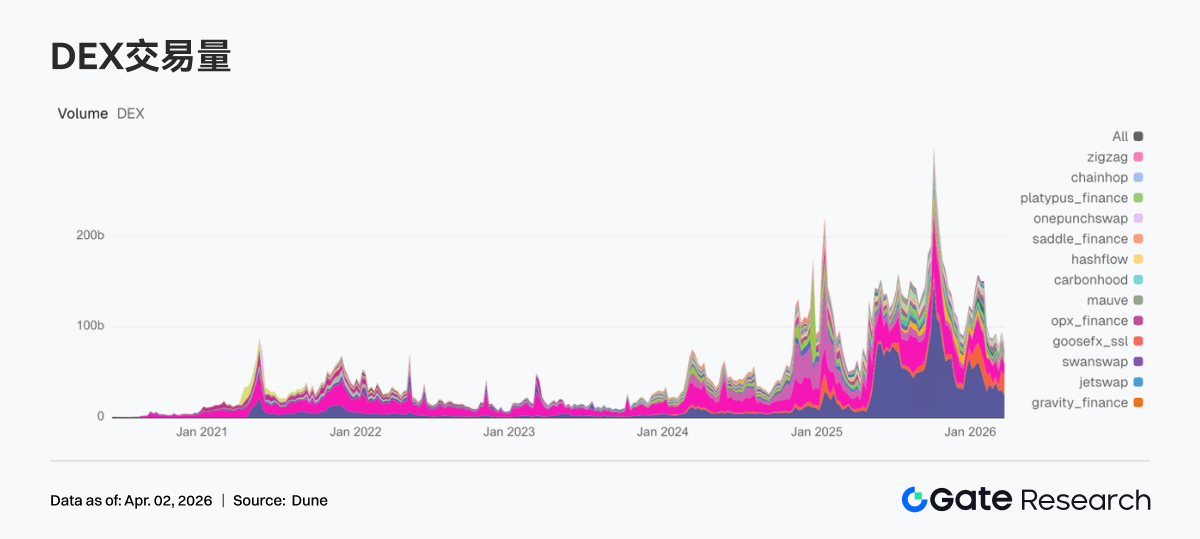

Trading heat cooled off from last week's high, with leading protocols generally declining. PancakeSwap and Uniswap showed a decrease in weekly trading volume compared to last week, with overall spot trading demand on mainstream chains converging. On the Solana side, differentiation was evident as Meteora maintained a trading volume slightly above $20 billion, but marginal increments have slowed; Raydium's weekly trading volume fell by 50%, marking the largest decline among leading DEXs. Aerodrome, Humidifi, and Bisonfi also experienced varying degrees of decline. Considering the protocol side situation, PancakeSwap's Infinity structure and Meteora's DLMM still represent the strongest efficiency tags, but this week the market placed greater importance on deterministic liquidity.

3.2 Total Supply of Stablecoins Consolidates at High Levels, DAI Shows Resilience

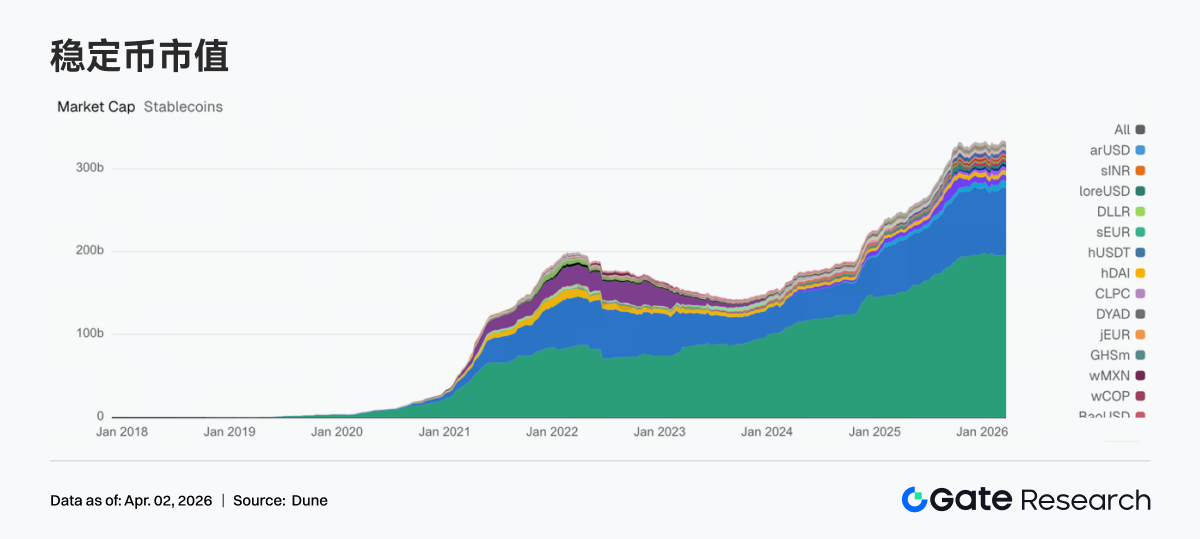

This week, there have been no new external increments in the stablecoin sector, with overall high-level consolidation. USDT remained almost flat compared to the previous week. USDC fell by about $1.4 billion, and PYUSD also declined by nearly $200 million, indicating a slight decrease in demand for payment and settlement-oriented stablecoins this week. Relatively more stable are protocol-based stablecoins, with DAI experiencing slight growth and USDS maintained at high levels. USD1, USDe, and GHO showed slight fluctuations, leaning towards structural reallocation. Circle is still advancing the multi-chain expansion of USDC + CCTP, but this week's data reflects that stablecoins are internally shifting from payment settlement to DeFi scenario resilience.

3.3 LST Protocols Withdraw Concurrently, ETH and SOL Both Begin to Slow

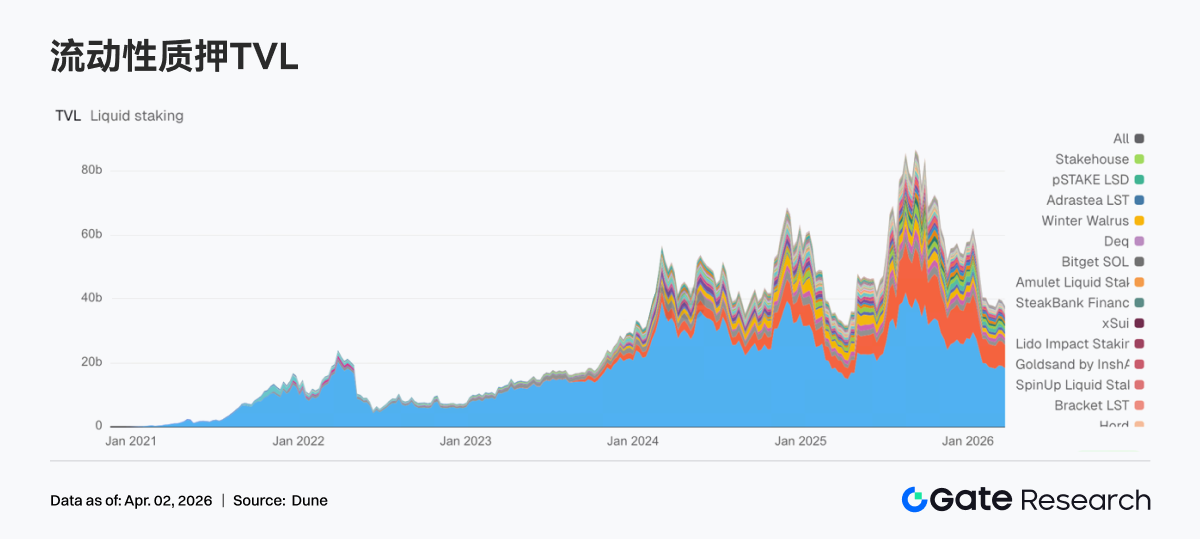

This week, liquidity staking sectors saw ETH and SOL both slowing down concurrently. Influenced by poor ETH performance, ETH LST funds began to reduce positions temporarily, with Lido and Rocket Pool's TVL both showing declines. Lido’s V3 and EarnETH / EarnUSD vault expansions have widened product boundaries, but short-term TVL is more affected by market risk preference and staking asset price fluctuations. SOL faced similar pressure, with Jito and Sanctum Validator LSTs also seeing retreats. Overall, this week reflected a downward shift in risk preference across the sector.

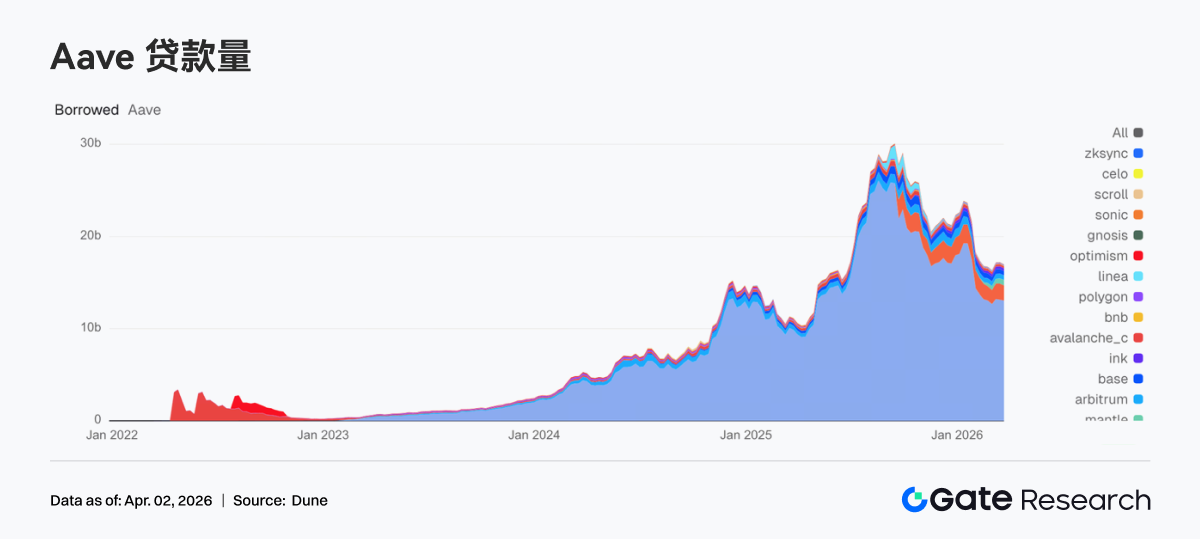

3.4 Aave Loan Volume Retreats, Mantle Becomes One of the Few Markets Absorbing Increment

This week, Aave's total loan balance slightly retreated compared to the previous week. The main Ethereum market and Plasma saw a decline of about $100 million, indicating de-leveraging signs in mainstream markets. Multi-chain expansion also temporarily slowed this week, with Base and Arbitrum retreating together. Mantle was one of the few markets that grew against the trend, with loan volumes rising from $555 million to $574 million, becoming a structural highlight of the week. Ink also saw a slight increase from $289 million to $292 million, but the growth was limited. Aave is currently pushing the V4 Hub-and-Spoke framework, and the market is pricing for future cross-market liquidity efficiency, but current funds prioritized shrinking total leverage before allocating a small amount of increment to sub-markets with new narratives.

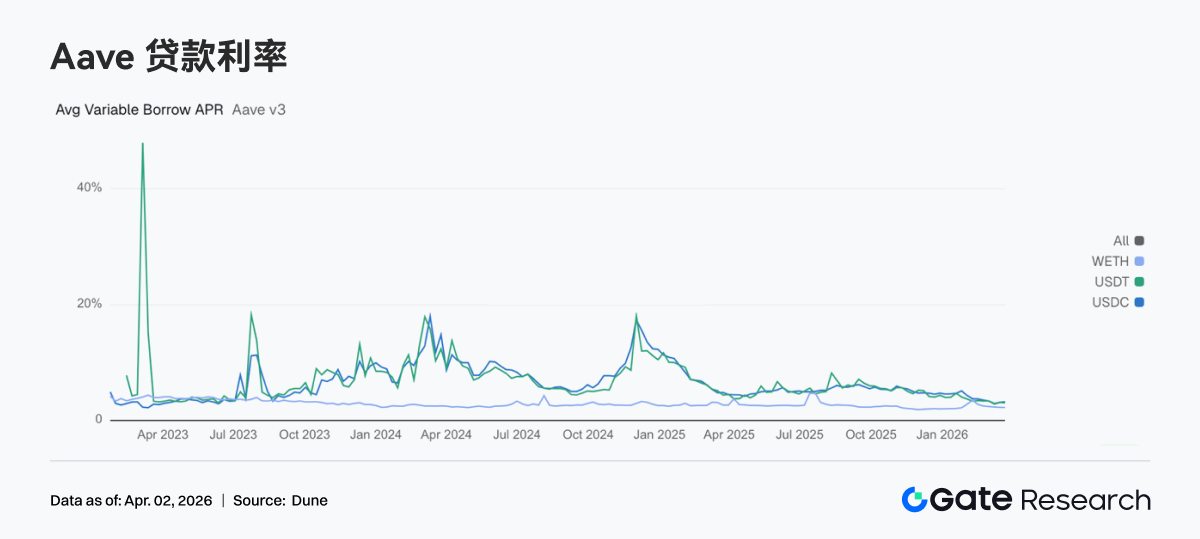

3.5 Aave's Three Core Assets' Loan Rates Continue to Diverge

The average floating borrowing APR for USDC rose from 3.10% to 3.23%, indicating that demand for dollar stablecoins did not weaken alongside the total loan balance decline. In contrast, USDT fell from 3.10% to 3.02%, and WETH also slightly decreased from 2.25% to 2.23%. This week, on-chain funds, while compressing broad risk exposure, concentrated borrowing demand more on USDC. From a strategic perspective, this typically corresponds to institutions preferring to use USDC for liquidity scheduling, collateral management, and neutral strategy rotations. Combined with Aave's recent governance progress, the risk isolation and liquidity routing framework of V4 is gradually becoming clearer, which is likely to lead to more frequent interest rate divergence between different assets in the future, as well as better reflecting true funding preferences.

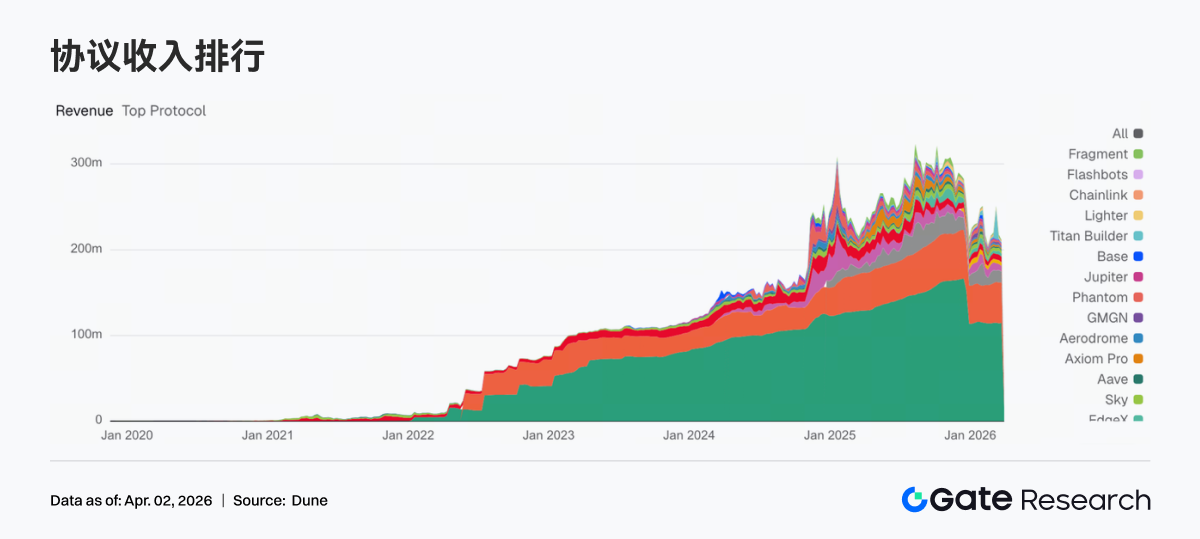

3.6 Protocol Revenue Shifts from Transaction-Driven to Stock-Driven

Revenue from transaction-based protocols has generally cooled, while stablecoin issuers remain the most stable profit centers. Tether and Circle’s revenues remained in a high stable range during the week. In contrast, Hyperliquid fell from $14.3025 million to $12.6277 million, Pump decreased from $7.1452 million to $6.6905 million, and EdgeX also dropped from $4.5534 million to $3.7969 million; the cooling trading activity has already transmitted to the revenue side. Overall, the main line of protocol revenue this week is whose revenue relies less on short-term trading fluctuations.

4. Derivatives Tracking

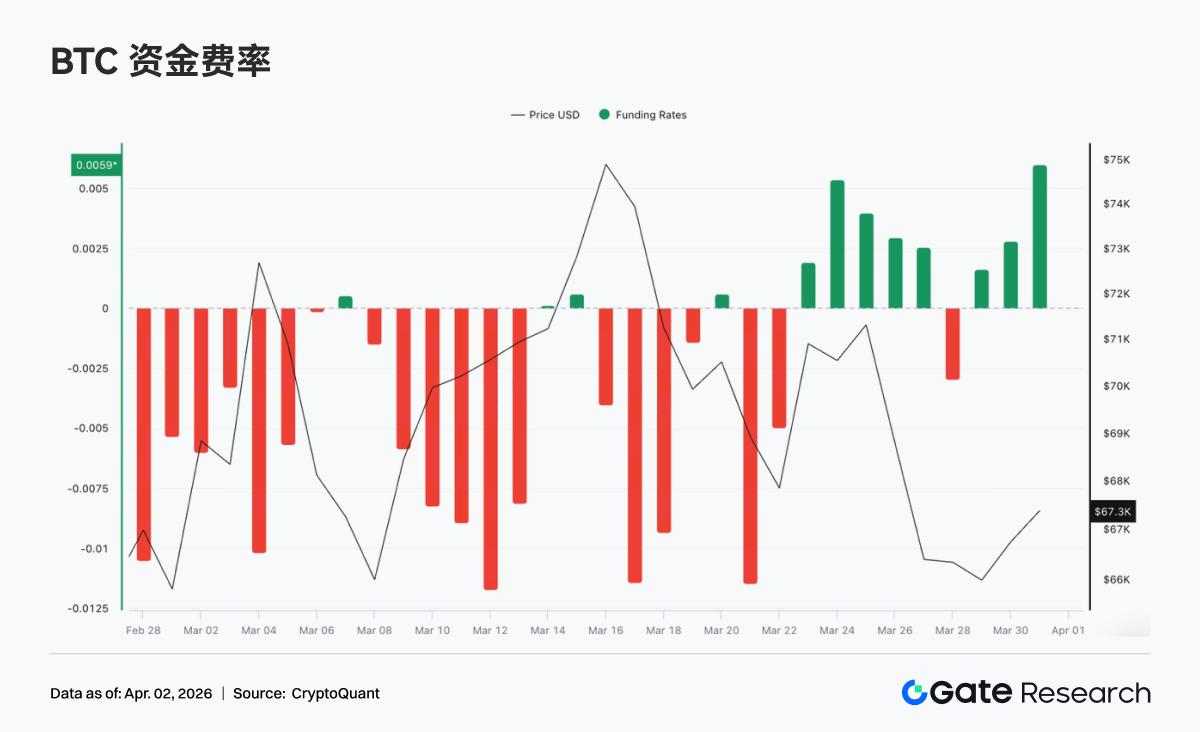

4.1 Funding Rates Turn Short-Term Bullish, Sentiment Shifts to Tentative Longs

BTC funding rates showed an overall structure shifting from repair to a brief positive phase, then fluctuating again. The previously dominant short position pattern in deep negative values has eased significantly, with funding rates turning positive for a few days mid-week (peaking near +0.005), leading the market to adopt a proactive long strategy, and short-term risk preference showed signs of recovery, resonating with the price's temporary rebound. However, the duration of this positive rate phase was short-lived and limited in intensity, lacking a trend towards a sustained positive premium structure.

4.2 Open Interest Peaks and Then Retracts, Leverage Funds Shift to Wait-and-See

In the past week, BTC open interest first expanded to a temporary high with prices rising, but then quickly decreased to around $21 billion as prices retreated, indicating significant de-leveraging in the market; subsequently, open interest did not return to previous highs but oscillated and repaired within the $21 billion to $22.5 billion range, gradually shifting the overall central point downward, with insufficient new capital inflow and leverage contracting. Overall, the current open interest structure primarily relies on existing stock games, lacking sustained volume cooperation, with the market still in the oscillatory reconstruction phase after de-leveraging.

4.3 Options Open Interest Concentrated in Mid to Long-Term and High Strike Prices, Bullish Structure Dominates

BTC options open interest is primarily concentrated in mid to long-term contracts such as those for April and June, with the market mainly focused on mid-term positions; structurally, Calls are significantly higher than Puts, leaning towards a bullish sentiment. From the perspective of strike prices, Calls are mainly concentrated in the $80,000 to $120,000 range, while Puts are distributed in the $60,000 to $80,000 range, creating a typical structure of bullishness above and hedging below. It is noteworthy that there's a considerable amount of Puts around $60K to $70K, indicating that while the market maintains mid-term bullish expectations, short-term defensive sentiment is also strengthening.

4.4 Skew Remains in Negative Range, Short-Term Defensive Sentiment Still Dominates

In the past week, BTC 25D Skew maintained an overall negative range (approximately -6 to -10), with Puts still holding a premium over Calls and the market's pricing for downside risk remaining high. Short cycle (7D, 30D) volatility was more pronounced, fast dropping before briefly recovering, reflecting that short-term sentiment was switching back and forth; while medium to long-term (60D and above) remained relatively stable, overall staying in the -5 to -7 range, showing that medium-term risk expectations had not changed significantly. Overall, the Skew has not steadily risen towards neutral or positive territory, meaning that while the market has made attempts at recovery, defensive allocations still dominate.

4.5 Implied Volatility Stabilizes, Market Has Limited Expectations for Short-Term Volatility

In the past week, the BTC DVol index generally oscillated in the 52%–55% range, retreating slightly before rising again, without showing a trend-driven uptick, signaling the market's restrained pricing for future volatility. During this time, prices experienced noticeable declines, but implied volatility only rose moderately without panic-driven spikes, indicating that the market did not view the current adjustment as a high-risk event. Overall, IV and prices displayed certain desensitization characteristics, reflecting that traders prefer to expect range-bound volatility rather than one-sided trend movements.

5. This Week’s Outlook

6. Gate Institutional Dynamic Update

Refined Operations

1. Advance data-driven and refined management, accurately identify customer needs, and enrich customized solutions.

2. Significant results in reactivating dormant users.

Capital Business

1. Continuing growth in mortgage lending scale, approaching bull market levels.

2. Reduction in BTC rates, driving new demand growth.

Products and Technology

1. Websocket contract BBO real-time push fully opened in April.

2. AI gradually implemented, institutional services enter AI-assisted operation phase.

Events and Markets

1. CrossEx Advanced Trading Incentive Program launched, enjoy a maximum contract rebate order fee rate of -0.01% starting April 9.

2. The April Hong Kong Web3 Festival Side Event is about to start.

Data Source:

•Investing, https://investing.com/currencies/xau-usd-historical-data

•Gate, https://www.gate.com/trade/BTC_USDT

•CMC, https://coinmarketcap.com/real-world-assets/?type=all-tokens

•Coinglass, https://www.coinglass.com/pro/depth-delta

•Dune, https://dune.com/gateresearch/gate-institutional-weekly-report

•CryptoQuant, https://cryptoquant.com/asset/btc/chart/derivatives

•Amberdata, https://pro.amberdata.io/options/deribit/btc/current/

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform, providing readers with in-depth content including technical analysis, hot insights, market reviews, industry research, trend forecasts, and macroeconomic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks, and users are advised to conduct independent research and fully understand the nature of the assets and products purchased before making any investment decisions. Gate shall not be responsible for any losses or damages arising from such investment decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。