Written by: Benji Siem @IOSG

Introduction

Stripe acquired Bridge for $1.1 billion. Mastercard acquired Zerohash for about $2 billion. Robinhood launched its own L2. These are not isolated bets but signals of a structural shift — the largest fintech giants are directly embedding blockchain infrastructure, stablecoins, and decentralized finance rails into their core products. Over the past decade, fintech companies have transformed payments, banking, and investing through software-native platforms and massive digital distribution. The next phase has begun: crypto is becoming the backend.

This report analyzes the strategies of ten leading fintech companies in the digital finance space, focusing on their business models, revenue drivers, and strategies for integrating crypto payments with DeFi infrastructure. A consistent pattern emerges: the most successful companies do not view crypto as a speculative asset but as backend infrastructure that can enhance settlement speed, reduce costs, and expand global financial connectivity. Stablecoins are particularly becoming the bridge between traditional financial systems and on-chain markets.

Insights into the Fintech Industry

Consensus on Digital Finance: How Different Players View This Opportunity

The digital finance foundations of these ten companies can be summarized as:

“Financial services should be borderless, real-time, software-defined, and composable — compliance should be invisible to the end user.”

Different types of players’ understanding of the opportunity:

Infrastructure Players (Visa, Mastercard, Stripe, Adyen)

Core Perspective: Transforming the underlying pipelines of capital flow without holding customer relationships

Opportunity: Each new payment rail (stablecoins, A2A, instant payments) is expanding the addressable market

Crypto Entry Point: Stablecoins reduce settlement friction, enabling 7×24 hour capital management

Consumer Platform Players (Nu, Revolut, PayPal, Cash App)

Core Perspective: Owning primary financial entry points for users and cross-selling a suite of services

Opportunity: Merging banking + payments + investing + crypto into a single app to enhance LTV

Crypto Entry Point: Treating crypto as a layer to enhance engagement and monetization (transaction fees, interest products, cross-border)

Hybrid Players (Robinhood, Block, SoFi)

Aggregators bid their capacity across various markets:

Core Perspective: Vertical integration at both the consumer product and infrastructure ends

Opportunity: Capturing profits through multi-layered approaches (consumer engagement, B2B infrastructure, asset custody)

Crypto Entry Point: Bilateral crypto strategy (consumer distribution + infrastructure ownership)

Main Trends in Fintech

Based on the analysis of these ten top companies, several clear patterns emerge. They are the core arguments of this report, and subsequent company cases and integration playbooks serve as corroboration.

Infrastructure First, Not Speculation

Almost all companies treat crypto as backend infrastructure rather than front-end speculative assets. Visa, Mastercard, Stripe, and Adyen are upgrading their settlement layers with stablecoins while keeping the consumer experience unchanged. Crypto will only succeed when it is “invisible.” This is the most consistent pattern among the ten companies and runs through subsequent integration strategies.

#

Stablecoins as the "Bridge Asset"

Every company that touches crypto is betting on stablecoins as the transitional layer between TradFi and crypto:

Visa: USDC settlements on Solana, 130+ stablecoin card programs

Mastercard: Four stablecoins (USDC, PYUSD, USDG, FIUSD) covering multiple chains

Robinhood: Partnering with USDG and sharing revenue

PayPal: Spontaneously issuing PYUSD and internalizing settlement

Stripe: USDC for cross-border merchant payouts

Stablecoins can compress settlement times, reduce FX friction, and enable programmable capital management without exposure to volatility.

Moat of "Regulated Distribution"

Companies with a large user base (PayPal 400 million, Revolut 50 million+, Nu 122 million, Cash App 58 million) position themselves as compliant entry points for inflows and outflows rather than protocol builders. Their competitive advantage lies not in technology, but in trust, compliance, and scalable distribution.

DeFi is Wholesale, Not Retail

No company directly exposes native DeFi protocols to end consumers. Instead, DeFi exists as a wholesale backend: yield sources (tokenized government bonds, money markets), liquidity optimization (faster settlements, cheaper cross-border), and product packaging (compliant savings accounts backed by DeFi yields). DeFi has become the infrastructure supporting regulated products rather than a user-facing experience. This foundation also dictates the subsequent integration opportunities and investment themes in this report.

Multi-Rail Strategy

Companies are building infrastructures that are agnostic to payment methods:

Stripe: “No matter which rail we take, I want to own that layer of programmable currency”

Mastercard: “Multi-rail company” covering cards, A2A, real-time payments, and blockchain

Adyen: “Global operating system for business payments”

As payment methods become increasingly fragmented (cards, A2A, stablecoins, BNPL), the winners will be companies that can intelligently route between all the rails.

Convergence Points

Winning strategies can be distilled down to: building the compliant shell for programmable currencies, capturing value through distribution, trust, and compliance rather than relying on holding protocols or exposing speculative positions.

The most advantaged companies possess at least one of the following: large-scale distribution (Nu, PayPal, Revolut, Cash App), control over infrastructure (Visa, Stripe, Mastercard), or vertical integration (Robinhood, Block, SoFi).

Good Models vs. Bad Models

Scalable and Robust Business Models

Tollbooth Model of Payment Networks (Visa, Mastercard)

Marginal cost per transaction is nearly zero; huge fixed cost leverage; network effects are almost unbreakable.

Essentially infinitely scalable: each new transaction adds revenue, but incremental costs are nearly zero.

Crypto integration risks: Theoretically, stablecoins and A2A payments could bypass card organizations, but Visa and Mastercard's response is to position themselves as "networks of networks," sitting atop all rails including crypto.

Infrastructure-as-a-Service (Stripe, Adyen)

Once embedded in the merchant tech stack, the switching costs are extremely high; revenue compounds as merchants grow; value-added services (anti-fraud, tax, billing) continually raise ARPU.

Stripe processed $1.4 trillion in 2024 (approximately 1.3% of global GDP).

Stripe's Bridge/Tempo bet is currently the most aggressive infrastructure play. If stablecoin payments scale, Stripe may capture the developer layer of crypto-native business.

Recurring Revenue + Float (Coinbase Subscription and Services, Revolut Premium)

Interest from stablecoin reserves (Coinbase alone is expected to earn $332.5 million from USDC in Q4 2025), staking rewards, and subscription fees are much more stable than transaction commissions.

Revenue expands with AUM/AUC rather than just transaction volume, making it more predictable.

Low-Cost Digital Banking for Underserved Markets (Nubank)

Monthly service cost is only $0.80, whereas traditional banks are $5–10+; monthly active rate exceeds 83%; net interest margin is 17.7%.

In underbanked markets, customer acquisition is almost viral; 122.7 million customers with huge cross-selling potential.

High-Risk / Poor Scalability Models

Pure Dependency on Transaction Fees

Companies with over 90% of revenue from transaction fees are completely at the mercy of market cycles. In a crypto bear market, transaction volumes can fall by 70–90%.

PFOF (Payment for Order Flow) Dependency

PFOF has been banned in the EU and is continuously scrutinized in the US. Companies relying on PFOF face life-and-death regulatory risks for their core revenue models.

Better paths: Transition to subscriptions (Robinhood Gold), interest income, and institutional clients (acquisition of Bitstamp).

Crypto Businesses Without Recurring / Sticky Revenues

Crypto exchanges relying solely on spot trading fees, without staking, stablecoin interest, custody, DeFi protocol revenue, or subscriptions — this is an extremely cyclic business.

Good crypto business models will layer multiple revenue lines (trading + staking + interest + protocol fees + subscriptions).

Loss-Making "Bitcoin Revenue Lines"

Block reported $1.97 billion in Bitcoin revenue in Q3 2025, but the cost of Bitcoin revenue was $1.89 billion, with a gross margin of only about 4% on BTC channel revenue. It drove up revenue but contributed marginally to gross profit.

Its strategic value lies in ecosystem lock-in (users who buy BTC on Cash App are stickier), rather than directly profiting from BTC.

Framework: What Makes a "Good" Crypto Fintech Business Model?

Fintech Crypto Integration Playbook

The following playbook outlines how ten companies execute the above foundations. To understand why these strategies work, please refer back to the earlier section on “Main Trends.”

Stablecoin Integration (Most Common and Fastest Growing)

Visa: USDC settlements within the network

Mastercard: Card partnerships with OKX; acquisition of Zerohash

PayPal: Spontaneous issuance of PYUSD ($3.6 billion circulation); supporting DeFi usage

Stripe: $1.1 billion acquisition of Bridge for stablecoin orchestration; building Tempo L1

Coinbase: Co-issuer/collaborator of USDC; expected stablecoin revenue of $1.4 billion in 2025

Making Crypto Trading a Feature

Robinhood: Native integration of crypto trading with stocks/options

Revolut: Over 200 tokens available for trading within the app

Nubank: NuCripto

Block/Cash App: Buy, sell, transfer Bitcoin

Low addition cost; captures retail demand in bull markets; enhances user stickiness.

Building Blockchain Infrastructure in-house

Coinbase → Base Chain (L2 based on OP Stack)

Stripe → Tempo (L1, in collaboration with Paradigm)

Robinhood → Robinhood Chain (L2 based on Arbitrum)

Owning the chain = owning the economics (Sequencer fees, MEV, ecosystem network effects). The analogy is Visa building VisaNet itself, rather than relying on third-party networks.

Full-Stack Bitcoin Play (Block's Approach)

Consumer wallet (Cash App) → Merchant acceptance (Square Bitcoin/Lightning) → Self-custody (Bitkey) → Mining (Proto) → Open-source development (Spiral).

This is a high-confidence vertical bet: If Bitcoin truly becomes a daily payment rail, Block will own every layer; if not, this is a major resource investment with uncertain results.

Custody and Institutional Services

Coinbase Prime: Custodian for most Bitcoin/Ethereum spot ETFs in the U.S.

Mastercard and Visa: Providing compliance/KYC/AML layers for institutional crypto adoption

Institutional funds require trusted, regulated custody — this is a high-barrier, high-margin business.

DeFi In/Out and Protocol Participation

PayPal: PYUSD supports DeFi lending/trading on Ethereum

Coinbase: Base Chain supports DeFi protocols; USDC is the dominant stablecoin in DeFi

Revolut & Robinhood: Staking services (ETH, SOL)

Integration Opportunities for Crypto Payments and DeFi

Upstream (Wholesale / Infrastructure Layer)

Stablecoin Settlement Networks

Using stablecoins for interbank settlements, capital management, and merchant withdrawals. Settlement times are compressed from T+2 to near real-time, reducing correspondent bank costs.

Beneficiaries: Visa, Mastercard, Stripe, Adyen

Example: Visa settles VisaNet obligations using USDC on Solana

Tokenized money markets as liquidity

Using tokenized government bonds (like Ondo OUSG, Franklin OnChain) as interest-bearing reserves, achieving liquidity without taking on credit risk.

Beneficiaries: PayPal, Nu, Revolut, SoFi

Example: Mastercard MTN supports tokenized government bond assets

Cross-Border Remittance Rails

Using stablecoin rails to replace SWIFT / correspondent banks for B2B and consumer remittances. Instant settlement, lower fees, better FX rates.

Beneficiaries: Stripe, PayPal (Xoom), Revolut, Nu

Example: Stripe enabled USDC withdrawals for global merchants

Programmable Compliance Layer

AML/KYC, transaction monitoring, and sanctions screening based on smart contracts. Automated compliance, reducing manual tasks, achieving real-time risk scoring.

Beneficiaries: All regulated players (especially value-added service providers like Visa, Mastercard)

Example: Visa Protect for A2A payments, Mastercard Crypto Secure

Downstream (C-end / Merchant Layer)

Stablecoin-linked Cards

Cards that allow spending directly from stablecoin balances, converting to fiat at the POS.

Beneficiaries: Visa, Mastercard (infrastructure), Revolut, Cash App (distribution)

Example: Visa's 130+ stablecoin card programs, Mastercard OKX Card

Crypto Collateralized Lending

Using crypto assets as collateral for fiat loans without triggering taxable events.

Beneficiaries: Robinhood, SoFi, Block, Revolut

Example: Bitcoin-backed loans offered through Cash App or SoFi

High-Yield Savings Accounts

High-yield savings products supported by tokenized government bonds or DeFi lending protocols, delivered with a compliant shell.

Beneficiaries: Nu, Revolut, PayPal, SoFi

Example: "Crypto earn" type products offered by Revolut, with returns close to staking yields

Merchant Stablecoin Settlements

Allowing merchants to settle in stablecoins rather than fiat, reducing FX risk and speeding up withdrawals.

Beneficiaries: Stripe, Adyen, Square, PayPal

Example: Mastercard allows merchants to settle in USDC, PYUSD, or USDG through Nuvei/Circle

Instant Cross-Border P2P

Stablecoin-driven remittances, arriving in seconds, with rates under 1%. Competing with Western Union/MoneyGram in LatAm and Asia.

Beneficiaries: PayPal (Xoom), Revolut, Cash App, Nu

Example: Nu enabling BRL → USDC → local currency transfers in Latin America

Differentiated / High-Margin Niche Opportunities

Self-Custody Wallet-as-a-Service

White-label self-custody solutions aimed at institutions and high-net-worth users. Enables charging custody fees while meeting self-custody compliance requirements.

Beneficiaries: Robinhood (Bitkey), Block, Stripe (via Bridge)

Example: Block's Bitkey hardware wallet

Blockchain-Based Loyalty Programs

Issuing points in token form, enabling cross-ecosystem redemption. Enhances stickiness and creates new revenues through tokenized rewards.

Beneficiaries: Mastercard, Visa, PayPal

Institutional DeFi Protocol Integrations (Great Potential)

Providing regulated DeFi lending, staking, and liquidity mining access through compliant middleware for institutions.

Beneficiaries: SoFi (Galileo), Stripe (Bridge), Mastercard (MTN)

Example: SoFi Galileo providing white-label crypto staking for banks

Privacy-Preserving Payments

Using zero-knowledge proofs to achieve “both private and compliant” stablecoin transfers. Supports confidential corporate payments while meeting AML compliance requirements.

Beneficiaries: All companies (especially B2B players like Visa/Mastercard)

Unbundling-Rebundling: A Structural Perspective

Connecting to insights from another report: The Architecture of Value: Structural Evolution of Financial Innovation and Deep Dive Report on Venture Capital Strategies

(https://claude.ai/30284df5d6ec8003aa52f792bb549832?pvs=25)

The winners of rebundling will be infrastructure providers, not consumer platforms

The most enduring and scalable fintech businesses are those that allow others to do the bundling rather than bundling themselves:

Infrastructure Players (Visa, Mastercard, Stripe, Adyen)

90–98% gross margins, 50–62% operating margins

Customer acquisition costs are nearly zero (developers/banks bring users)

Network effects or developer lock-in serve as a moat

Revenue grows as the ecosystem expands, not through direct customer acquisition

Consumer Platforms (Robinhood, Nu, Revolut, PayPal):

30–50% gross margins, 10–25% operating margins

Customer acquisition costs between $200–450

Must achieve 3+ product engagement to be profitable

More vulnerable to regulatory changes and market cycles

Visa captures 97.8% gross profit on $170 trillion in payment volume, while Robinhood’s crypto trading revenue is cyclic — this comparison highlights the fundamental gap between the two.

Three Key Dependencies Determining the Success or Failure of Rebundling

Dependency 1: Source of Funds (Banking License = Compounding Moat)

Winners: Nu ($19 billion in deposits, 3-4% cost of funds, 17.7% net interest margin), SoFi (banking license can absorb deposits)

Losers: PayPal (unlicensed, cannot absorb deposits), Revolut (UK license delays prevent competitive lending)

Consumer fintechs without banking licenses are either hostage to BaaS partners (like Synapse crashing in 2024) or cannot internalize the spread between “deposits - loans” — which is key to making rebundling profitable.

Dependency 2: Cross-Selling Economy (Threshold of 3+ Products)

Single-product users (annual income of $50, LTV of $150) lose money at CAC between $200–450. Users with three products (annual income of $180, LTV of $540) start to become profitable.

Successful Cases: Robinhood (11 products, ARPU $191, year-on-year +82%), Revolut (wealth business revenue +298%), Nu (cross-product monthly active rate 83%)

Failure Cases: PayPal (400 million users, most only use checkout, unable to cross-sell Venmo/crypto/savings)

Dependency 3: Developer / Enterprise Lock-In (Integration Depth)

Stripe's moat: Once integrated with Billing + Tax + Connect + Radar, it takes over 6 months of engineering investment to decouple. Each additional product compounds switching costs.

Visa’s genius of “mixed order”: 20,000 banks compete for customers (decentralized), but all use Visa’s protocol (centralized). Banks cannot leave because the network itself is the product. Zero CAC, 97.8% gross profit, revenues collected from $170 trillion in transaction volume as "toll fees".

For C-end crypto, structural challenges include: custody responsibilities, profit margins being pressured (Uniswap 0.3% vs. Coinbase 1-2%), no lock-in (users can self-custody to withdraw), and strong cyclicity (Coinbase revenue drops -75% in 2022–2023).

Foundation for Crypto Success: Be the "Stripe / Visa of Stablecoins"

The common pattern of successful fintech case studies is clear: building compliant middleware that abstracts the complexity of blockchain for enterprise and fintech customers.

Investment Theme 1: Stablecoin Orchestration Layer

Stripe's $1.1 billion acquisition of Bridge proves one thing: Enterprises want stablecoin settlements but do not want to run nodes, manage wallets, or deal with regulations across 50 states.

Winning Product: An API that simultaneously handles multi-chain routing, liquidity optimization, compliance checks, and tax reporting. Enterprises only need to call POST /transfer, and the infrastructure handles the rest.

Economic Model: Charging a 0.5–1% take rate on massive transactions, with zero incremental costs per transaction, and very high switching costs once integrated. Again, over 90%+ gross profit, but applied to a stablecoin settlement market of over $20 trillion.

Investment Theme 2: Vault-as-a-Service ("Fireblocks" Approach)

PayPal, Robinhood, Nu all hold billions of dollars in crypto assets. Custody requires OCC compliance, MPC/HSM security, $100 million+ insurance, and disaster recovery.

The opportunity lies in providing "AWS of Crypto Custody" — enterprises access via API, responsible for key management, policy engine (e.g., "withdrawals over $100,000 require 3 approvals"), compliance reporting, OFAC screening.

Every fintech that has added crypto needs this

Zero CAC (B2B sales cycle)

High retention (switching custody = 12+ months of security audits)

Winners: Fireblocks ($8 billion valuation), Anchorage Digital (holds OCC license), Copper.co

Investment Theme 3: DeFi Middleware / "Vault Curator" Layer

What is currently missing: A "Stripe for DeFi Yields." It can aggregate yields across Aave, Compound, Morpho, and tokenized government bonds (Ondo OUSG), while abstracting Gas fees, generating tax reports (IRS-compliant 1099), providing insurance shells, and compliance layers.

Vault curator opportunities:

Ondo Finance: Tokenized government bonds, 5% yield

Backed Finance: Tokenized corporate bonds

Maple/Goldfinch: Institutional-grade DeFi lending with underwriters

Specific Example: SoFi holds billions of dollars in deposits, while traditional accounts give only 0-1%. If its B2B platform Galileo could provide a "DeFi Yield API" connecting to 5% tokenized government bonds, SoFi could offer customers 4% APY, keep 1% spread, and not bear the assets on the balance sheet. This middleware approach, positioned between protocols and regulated fintech, responsible for compliance shells and tax reports, is the current white space.

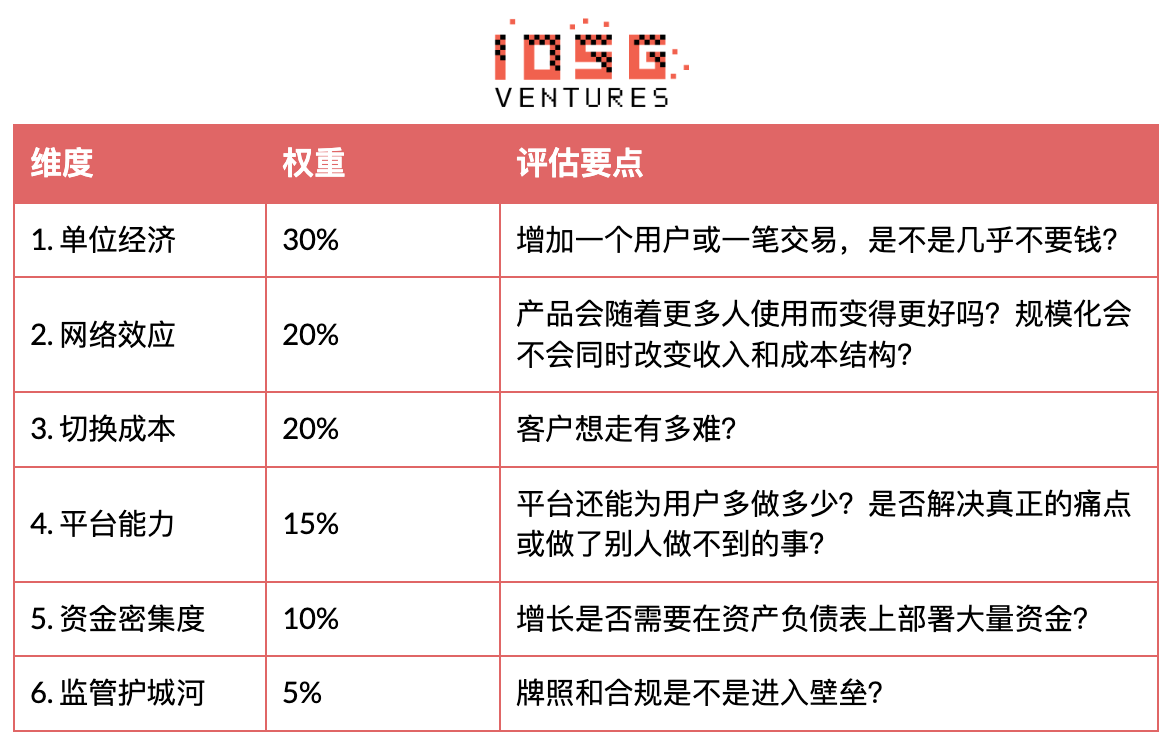

Framework: Assessing Fintech Business Models

Overview Table

Crypto Integration and Foundation Alignment of Each Company

Conclusion

The future of fintech lies in the integration of traditional financial platforms with programmable financial infrastructure. Blockchain technology is not replacing existing systems but is increasingly being integrated as a layer operating behind the scenes for settlement and liquidity. Stablecoins, tokenized assets, and on-chain markets are delivering faster settlements, cheaper cross-border payments, and new financial products that are essentially invisible to end-users.

Ultimately, the companies that can capture value in digital finance are those that possess large-scale distribution, regulatory trust, and control over infrastructure. Whether through payment networks, developer platforms, or consumer financial ecosystems, the winners will be those that abstract financial complexity while orchestrating across multiple payment rails. As programmable currencies are more widely adopted, fintech companies that successfully integrate traditional finance with blockchain infrastructure will shape the next generation of global financial services.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。