As the war situation in Iran becomes increasingly enigmatic, the crude oil market has endured significant fluctuations.

Meanwhile, a rare phenomenon occurred in the perpetual contracts for crude oil on Trade.xyz, specifically WTIOIL-USDC: the annualized funding rate stabilized between -300% and -400%. This means that any trader willing to go long at this moment can receive a profit equivalent to 1% of their principal from the shorts' pockets each day.

The market doesn't just give away money for no reason. Understanding this abnormal negative funding rate requires starting from the fundamentals of futures trading.

Rolling Over

Crude oil futures are a series of contracts lined up by delivery month. May delivery, June delivery, July delivery, each has its own price. When the front month is about to expire, the market needs to roll over from the old contract to the new contract; this action is called rolling over.

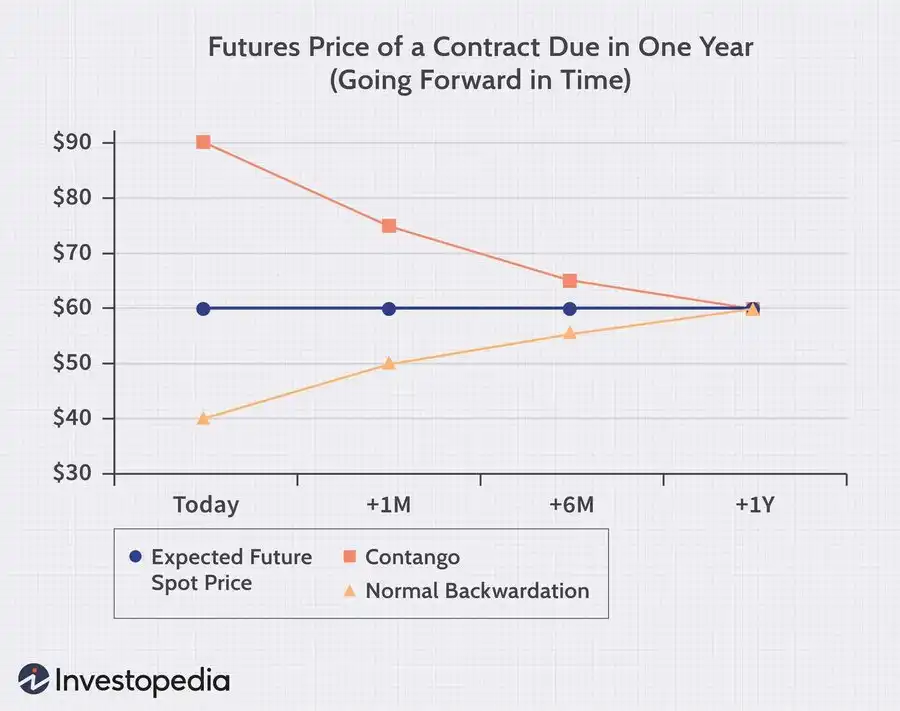

Under normal circumstances, long-dated contracts imply that oil traders will hold onto the oil for several more months, incurring additional storage costs, so the delivery price should be higher. The phenomenon of future contracts being more expensive than near-month contracts is called Contango, while the opposite situation, where near-month contracts are more expensive than long-month contracts, is called backwardation. This typically occurs when there is a current shortage and everyone wants to obtain oil right away.

In this instance, during the rolling over of crude oil on Trade.xyz, the crude oil futures market exhibited this near high and far low structure.

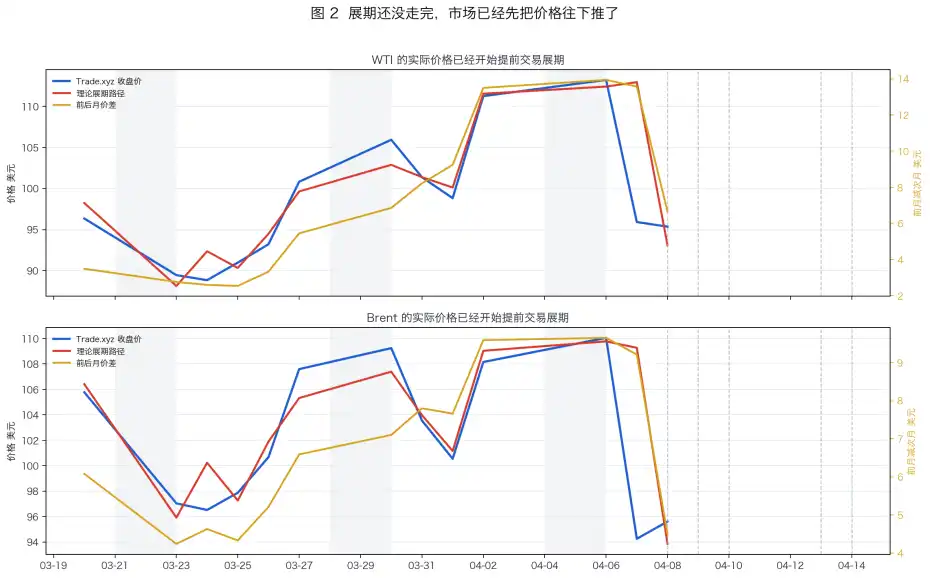

From late March to early April 2026, the WTI crude oil curve was in an extreme backwardation. As shown in the picture above, the price of the May contract (near month) consistently remained above that of the June contract (far month), with the price spread widening to over $14 at one point.

And on Trade.xyz, the WTIOIL-USDC perpetual contract is anchored to this May near-month contract.

However, we won't be trading this May contract for long. It must be rolled over to the next June contract. So how does rolling over occur?

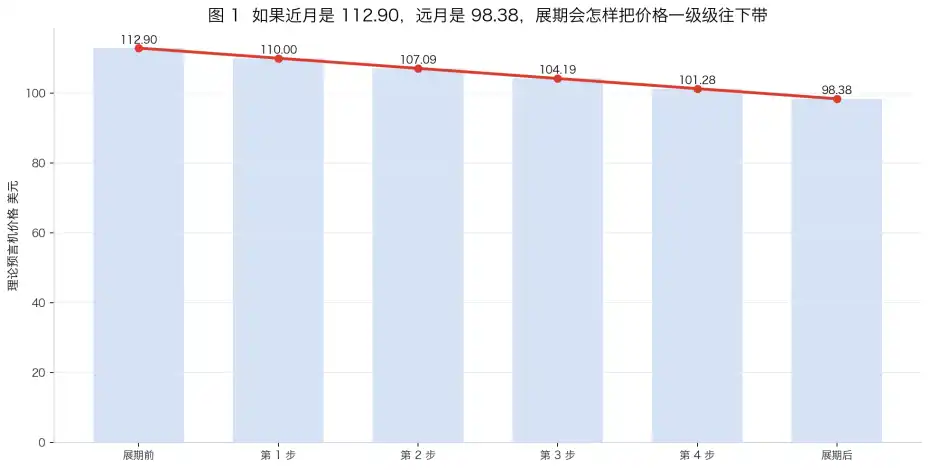

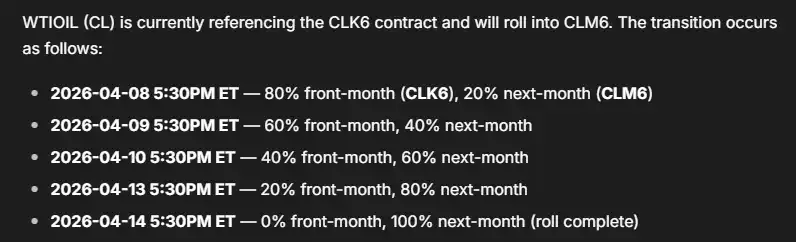

According to the documentation from Tradexyz, the oracle will take 5 trading days to gradually switch the price weighting from 100% near-month contract to 100% far-month contract.

In the context of "backwardation," this means that the oracle price on Tradexyz will drop from the near-month price to the far-month price over 5 trading days.

Market participants familiar with this mechanism have a clear expectation of the contract price after the roll-over. Everyone knows it will drop, and thus they rush to short. As shorts accumulate, the funding rate turns negative, and shorts begin to pay longs.

From the perspective of the no-arbitrage principle, this is normal. The price spread between near and far months gives short sellers a profit. The funding fee will offset this profit. The larger the spread, the higher the negative funding rate charged by the market.

Once the negative funding fee reaches a certain level, this seemingly obvious arbitrage opportunity will be flattened out. The costs for shorts will fully cover the profits.

Strategies

How to make money in such a market context? Below are three common strategies.

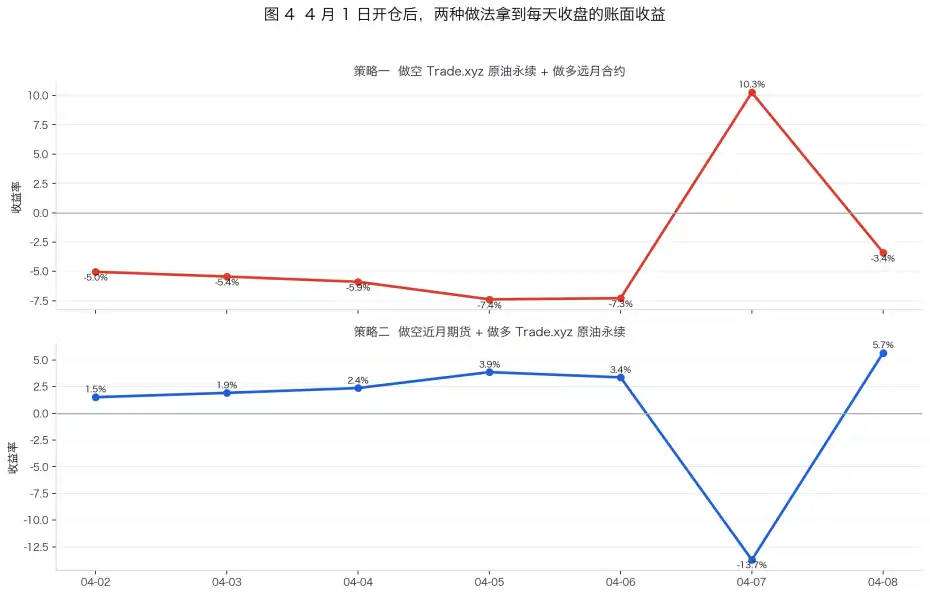

1. Short the crude oil contract on Tradexyz at the current price while going long on the far-month contract on CME.

This seems like a risk-neutral strategy that can earn stable spreads, but several factors have not been considered.

Assuming you short the WTI contract on Trade.xyz at $95.352 on April 8, simultaneously going long on the June futures contract at $87.75, each with a notional capital of $10,000. If both sides eventually converge, theoretically, you could achieve a spread of $7.60, which is approximately $797 in profit. However, on April 8, the daily funding rate for shorts had already reached 1.42%. Based on the remaining 6 days to complete the roll-over, funding fees would need to be paid off at $851. By this point, the net profit has already dropped to -$53. This does not even consider transaction fees and slippage.

Abraxas Capital began implementing this strategy on March 19, right after the last roll-over. They held a position in Brent crude oil on Tradexyz that accounted for 20% of the market's open contracts and reaped huge profits when early funding rates remained relatively neutral, but as more arbitrageurs entered, the funding fees consumed 80% of their arbitrage profits.

A large position also means they may find it difficult to exit, leaving them to passively pay.

2. Short the far-month futures contract, long the near-month contract on xyz, and close the position before the roll-over begins.

This trade is almost the opposite of strategy 1, betting on the market being over-arbitraged. After April 1, this strategy can indeed yield profits.

3. Short the funding rate contract on xyz on Boros before the roll-over starts.

Boros is a market developed by the Pendle team specifically for trading rates. In Boros's crude oil contract market, traders engage in the funding fee expectations for Trade.xyz's crude oil contract during the forthcoming period. If users believe the negative funding fee will continue to deepen, they can short the market funding rate contracts.

However, limited by slippage costs, position caps, transaction fees, and extremely low capital efficiency (supporting only 0.2x leverage), this trade also faces challenges in achieving the ideal high returns.

Conclusion

The rise of trading platforms like Trade.xyz, which deal with real-world assets, is pushing a group of "crypto traders" to become "futures traders." DeFi players are also starting to learn the CME roll-over calendar, calculating the price spreads between months, and watching the rate curves on Boros to make decisions.

Trading platforms are continuously iterating, and market participants are adapting to the new infrastructure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。