TL;DR

Background: Aave launched V4, Morpho advanced V2, and DeFi lending is entering a new round of architectural upgrade cycle.

Evolution history: Shared fund pool model was born → Aave V2/V3 promoted multi-chain expansion and risk layering → Morpho "curation revolution"

Three paradigms: Multi-asset fund pool | Isolated market + curation mechanism | RWA lending

Aave V4 VS Morpho V2: Aave is more like a "big bank" on the chain, while Morpho is more like an "asset management platform" on the chain.

Risks: Oracle and parameter configuration risks | Governance and organizational risks | Vault/Curator risks | Smart contract and runtime risks

Opportunities: Lending markets are becoming "modular financial building blocks" | Institutionalization becomes a product path | RWA and credit layering broaden asset boundaries

Conclusion: DeFi lending in the V4/V2 era is moving toward a professionalized, modular, and institution-friendly financial operating system.

DeFi lending is entering a new round of architectural upgrade cycle. Recently, the two major DeFi lending protocols, Aave and Morpho, announced significant version upgrades: Aave V4 went live at the end of March, and Morpho V2 officially launched in February. Aave V4's hub-and-spoke architecture aims to unify liquidity and expand into the RWA field. However, the sudden announcement from Chaos Labs to exit today, along with previous departures of core contributors like ACI, governance disputes, and liquidation anomalies, has raised widespread doubts. Although Morpho V2's non-custodial Vaults V2 greatly increased asset efficiency by 20-30% through the Curator curation mechanism, discussions about Curator management risks and safety are equally intense. The simultaneous upgrades of the two protocols signify that lending protocols are evolving from "on-chain deposit and lending tools" to more complex capital management and credit layering infrastructures. Furthermore, this also serves as a wake-up call for ordinary crypto investors: opportunities and risks coexist, and behind the upgrades are profound tests of capital efficiency, security, and governance dynamics.

I. Understanding DeFi Lending Protocols

1. The underlying logic of DeFi lending

The underlying logic of DeFi lending can essentially be summarized in one sentence: moving the deposit and loan business of traditional banks onto the chain and rewriting it with code.

In this system, lenders deposit assets into the protocol to earn interest, while borrowers obtain funds by providing excessive collateral. The biggest difference from traditional finance is that this process does not rely on manual review, credit assessment, or centralized institutional backing, but is entirely executed by smart contracts automatically. Fund circulation, interest rate calculation, and liquidation mechanisms are all driven by preset rules, ensuring high transparency and verifiability.

Because of this, the threshold for DeFi lending has been significantly lowered—any wallet address holding crypto assets can participate without permission.

2. Use cases of lending protocols

From an investor's perspective, the use cases of lending protocols mainly focus on two typical demands.

Collateral without selling coins: Users can use assets such as BTC and ETH as collateral to borrow stablecoins, gaining liquidity without giving up potential appreciation, thus avoiding missing out on market opportunities due to premature selling.

On-chain interest accrual: Users deposit idle assets into the lending protocol to receive stable interest rate returns, treating it as an on-chain "savings account" or "cash fund alternative." In the context of a lack of low-risk yield tools in the crypto market, this function has long served as a fundamental yield anchor.

Funding market infrastructure: Almost every complex strategy implementation relies on the liquidity support it provides. For example: liquidators need immediate funds to participate in liquidations to earn liquidation rewards; arbitrageurs need short-term liquidity to complete cross-market price arbitrage trades; other protocols (such as derivatives, stablecoins, yield aggregators) require composable collateral and borrowing interfaces to construct their product structures.

It is evident that lending protocols do not merely serve end-users but are also providing "blood circulation" for the entire on-chain financial system.

3. Two core capabilities: pricing and risk isolation

From a mechanism design perspective, the complexity of lending protocols can ultimately be reduced to two core capabilities.

Pricing capability: This includes interest rate models, collateralization rates, liquidation thresholds, and incentive mechanisms. These parameters collectively determine the supply and demand relationship of funds and capital efficiency, and they directly reflect the competitiveness of the protocol.

Risk isolation capability: In an environment with multiple assets and markets, how to prevent the fluctuations or risk events of a single asset from spreading to the entire system is a key proposition for the long-term evolution of lending protocols. Isolation pool design, risk layering, and independent market structures all revolve around this goal.

II. Evolution history of lending protocols

The evolution of lending protocols is not simply adding new functions; instead, it seeks a new balance between several key contradictions: between efficiency and safety, between decentralization and specialization, between open access and controllable risk management. In a sense, the development history of DeFi lending is a process of continuously reconstructing mechanisms around this triangular relationship, as well as the history of Aave and Morpho's rise and expansion.

1. Origin phase (2018-2020): Birth of the shared fund pool model

In June 2018, Compound officially launched the cToken mechanism, which is regarded as the true starting point of DeFi lending. Users deposit assets such as USDC and ETH into a shared large liquidity pool, and the system automatically adjusts the interest rates based on supply and demand; borrowers can borrow funds by depositing 150%-200% collateral. This is the classic "peer-to-pool" model: everyone's funds are mixed together, offering high liquidity, and anyone can deposit or withdraw at any time, proving for the first time to the world the feasibility of "permissionless lending" on the blockchain.

Aave's predecessor, ETHLend, attempted pure P2P point-to-point matching in 2017, but due to low matching efficiency and severe fragmentation of liquidity, it was hardly utilized in 2019. Aave V1 launched in January 2020, introducing a fund pool structure and bringing flash loans as a key innovation into DeFi, establishing its later dominant position.

2. Explosion and iteration phase (2020-2023): Aave V2/V3 promoting multi-chain expansion and risk layering

After the "DeFi summer" of 2020, liquidity fragmentation and multiple hacking events revealed the shortcomings of the single pool model. Aave V2 (launched in December 2020) expanded batch flash loans, debt tokenization, collateral swaps, and one-click operations for direct repayments with collateral, reducing gas consumption by 15-20%. These upgrades significantly enhanced V2's capital efficiency, user experience, and developer friendliness.

Aave V3 (launched in March 2022) introduced three killer innovations: isolated markets (e-mode, allowing similar assets such as ETH and stETH to serve as collateral for each other), cross-chain portals (supporting multi-chain liquidity transfers), and smarter liquidation parameters (LTV, liquidation threshold, liquidation bonus can be dynamically adjusted based on market conditions). Aave's cumulative lending volume exceeded $1 trillion by the end of 2023.

3. Optimization and modularization phase (2023 to present): Morpho "curation revolution"

In 2023, Morpho emerged as the "interest rate optimization layer" of Aave and Compound, prioritizing the matching of P2P borrowing parties, with residual funds being returned to the original pool, often yielding rates higher by 0.5-2%. Morpho V1 created a market consisting of "one collateral asset + one borrowed asset": market parameters are unchangeable, risks are isolated within a single market, and creation requires no permission. The V2, launched in 2026, fully externalized risk management and pricing: Curators (professional curators like Gauntlet, Steakhouse, Bitwise) are responsible for setting parameters such as interest rates, terms, and LTV, while the protocol only provides timelock delay changes, flash loan-style redemption, and Sentinel protection mechanisms to ensure complete non-custodial status. The goal of V2 is to allow "the market rather than the protocol" to determine interest rates and support fixed rates/fixed terms, smoother cross-chain operations, and more structured contracts closer to traditional credit.

III. Three mainstream paradigms of DeFi lending

The mechanisms of lending protocols can be divided into three dimensions: how assets are aggregated, how risks are isolated, and how interest rates are formed. Along these three dimensions, current DeFi lending can be roughly summarized into three mainstream paradigms.

1. Multi-asset fund pool: Liquidity-first "standard model"

The first type is the most classic and also the most familiar mode for users—multi-asset fund pools (Pooled Money Market), represented by Aave and Compound.

The core of this model lies in: funds are aggregated by asset, with interest rates algorithmically adjusted based on supply and demand. All users' deposits are pooled together into the same pot, and borrowers withdraw funds from the pool, with interest rates dynamically changing with utilization. This design brings extremely high liquidity and availability: deposits and withdrawals are instant, the liquidation mechanism is mature, and it supports advanced features such as flash loans.

However, the high efficiency comes with "partial risk sharing." Although Aave V3 has achieved risk layering for different assets through isolation mode and e-mode, significant fluctuations of a single asset under extreme market conditions may still impact overall liquidity.

2. Isolated market + curation mechanism: Rebalancing efficiency and safety

The second type is the rapidly rising paradigm of recent years—isolated markets + curation (Isolated Markets + Vault Curation), represented by Morpho.

The core idea is: first, isolate risks, and then make up for efficiency through structural design. In Morpho Markets, each market is usually "single collateral + single borrow," with fixed parameters that are independent of each other, inherently avoiding risk transmission between different assets. This design is superior in safety compared to traditional fund pools.

The problem lies in the fact that complete isolation can lead to liquidity fragmentation and a decrease in user experience. To address this, Morpho introduced Vaults and Curator mechanisms: Curators are responsible for selecting underlying markets and configuring parameters; Vaults repack multiple isolated markets to present users with a near "fund pool" one-click experience; while dynamically reallocating assets between different markets to enhance yield and utilization.

As a result, this model achieves a compromise: yields are typically 0.5%-2% higher than Aave; risks are more granularly isolated; but it also introduces new variables—the management capability and moral hazard of the Curator.

In other words, Morpho has externalized part of the risk management responsibilities originally borne by the protocol to "professional roles," which is essentially a step from "complete decentralization" toward "professional governance."

3. RWA lending: Connecting the "new boundary" of on-chain and real world

The third type is the fastest-growing and most structurally significant direction—RWA (real-world assets) lending. The key change in this model is that collateral or cash flow sources are no longer limited to on-chain assets but come from the real world, such as accounts receivable, bonds, real estate, or corporate financing demands. Typical projects include Maple, Goldfinch, Centrifuge, etc.

Structurally, RWA lending can be roughly divided into two categories:

Over-collateralized: Tokenizing real assets as collateral (e.g., invoice financing);

Credit-based/low-collateralized: Relying on off-chain due diligence, on-chain reputation, or partial KYC (e.g., Goldfinch’s layered fund pool structure).

These protocols are much closer to traditional finance in terms of risk management logic:

Returns primarily come from fixed-rate loans, usually between 4%-8% or even higher;

Lower correlation with crypto market fluctuations, possessing a certain level of "counter-cyclicality";

But they are also more reliant on oracles, legal structures, and compliance frameworks.

From an industry trend perspective, RWA is becoming an important incremental source in the lending track: its TVL has accounted for over 10% of lending protocols, with Aave V4 explicitly identifying RWA as a key expansion direction; Morpho is also collaborating with institutions like Ondo and Apollo to introduce off-chain assets. It can be anticipated that the development of RWA will drive DeFi lending from "internal crypto circulation" to "on-chain-off-chain integration" in a new stage.

IV. Aave V4 and Morpho V2: Two upgrade paths, two futures for lending

If the main line of DeFi lending in recent years has been to continuously seek a balance between "efficiency, safety, and scalability," then Aave V4 and Morpho V2 represent two completely different answers. The former chooses "unified liquidity + modular expansion," attempting to make itself the central hub for on-chain lending; the latter moves towards "non-custodial curation + customized markets," returning more pricing power and risk management authority to the market and professional managers.

1. On-chain data performance

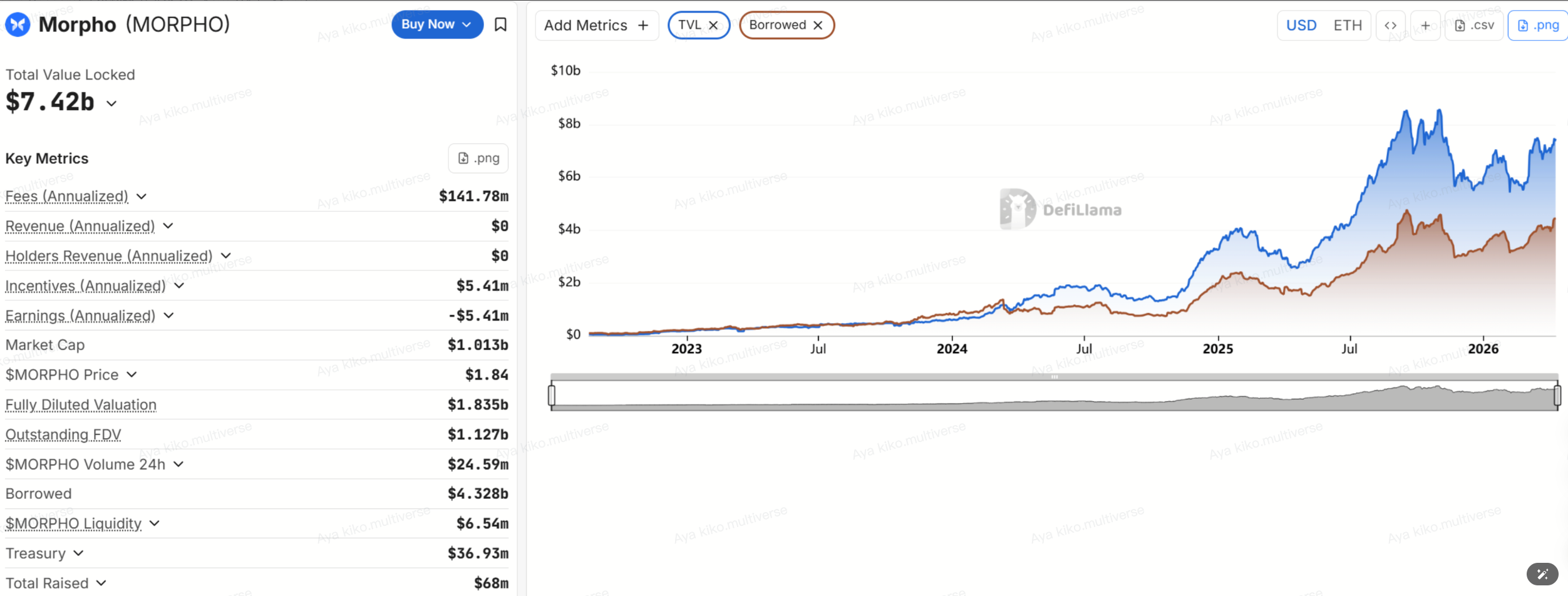

If we take "lending track TVL" as the denominator, Aave accounts for about half, while Morpho is at the 10%+ level; if we take "total lending across the network" as the denominator, the share of Aave lending is even higher, exceeding 50%, indicating that it remains the core layer for on-chain leverage and credit demand.

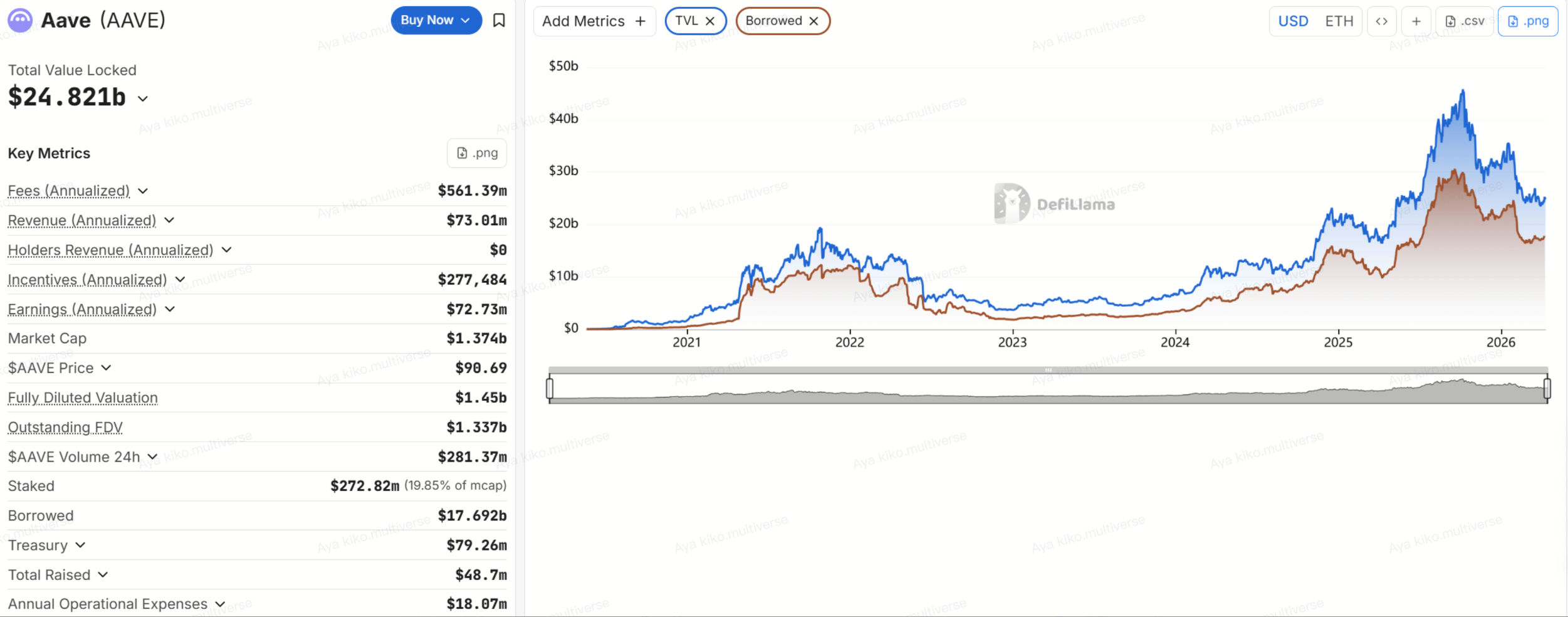

According to DefiLlama data, as of April 9, 2026, the TVL for the DeFi lending track is approximately $51B, and total lending across the network is about $34.4B.

Aave's TVL is approximately $24.8B, with lending around $17.6B, of which Ethereum accounts for about $20B in TVL, while the remainder is distributed across Plasma, Arbitrum, Base, Mantle, Avalanche, and other multi-chains.

Source: https://defillama.com/protocol/aave

Morpho's TVL is approximately $7.4B, with lending around $4.3B, mainly distributed in Ethereum (about $3.9B) and Base (about $2.3B), with some distribution in Hyperliquid L1, Arbitrum, etc.

Source: https://defillama.com/protocol/morpho

2. Aave V4: Restructuring liquidity with Hub-and-Spoke

The core change in Aave V4 aims to solve a long-standing problem from the V3 era: the liquidity fragmentation caused by multi-market and multi-chain expansion. Under the V3 model, users deposit assets into a market on a specific chain, and the liquidity can generally only serve that market. To launch a new market, funds often have to be redirected, which is inefficient. Aave V4's solution is "Liquidity Hub + Spokes": A unified liquidity center is set for each network, with users entering the protocol through different Spokes, while the Hub is responsible for unified accounting, quota control, and core risk control constraints, thus sharing liquidity while placing different strategies and asset types into different risk zones.

The key points of Aave V4 can be summarized in three:

Unified liquidity: Reduce capital fragmentation between different markets on the same chain, enhancing overall utilization.

Modular risk isolation: Different Spokes can be configured with different parameters, avoiding "all assets sharing one risk pot."

Reserving space for institutions and RWA: RWA Spoke can impose stricter access, custody, and redemption rules to prepare infrastructure for on-chain real assets.

The challenges of Aave V4 stem precisely from its ambition. A more robust architecture means that governance, risk control, and operational complexity will simultaneously increase. The initial configuration of V4 will include 3 Hubs and 10 Spokes, and V4 and V3 are expected to run in parallel for 24 to 36 months.

It is at this stage that the governance controversies surrounding Aave have erupted. Core contributors like BGD, ACI, and Chaos Labs have successively announced their departure or the end of cooperation, with Chaos Labs publicly stating that the fundamental disagreement lies in "how risks should be managed."

3. Morpho V2: Making "asset management" a protocol capability

In contrast, the upgrade logic of Morpho V2 is more restrained and "modular." It is not a complete reconstruction but rather a step-by-step rollout of Vaults V2 and subsequent Markets V2. The official statement clarifies that Vaults V2 will launch first, initially continuing to allocate funds to the old version of the Morpho market; once Markets V2 is fully launched, it will then provide initial depth liquidity for fixed-rate, fixed-term markets.

The focus of Morpho V2 is not to create a larger total pool but to transform "asset management" itself into a protocol-level capability. Key changes include:

More granular role separation: Owner, Curator, Allocator, Sentinel each have their designated roles, facilitating responsibilities separation and institutional compliance.

Curator becoming the core role: Responsible for configuring risk parameters, setting liquidity allocation boundaries, and appointing Allocators for execution.

Enhanced non-custodial safeguards: Through timelock, flash loan-driven in-kind redemption, and Sentinel's emergency interventions, it strives to minimize worst-case scenarios.

The most crucial point is: the Morpho protocol no longer makes a "unified risk judgment" for all users but allows users to choose their Curators. Essentially, users are not selecting a unified market but are choosing an "on-chain fund manager." This is also the biggest difference between Morpho and Aave.

The appeal of Morpho V2 is very evident:

Users can one-click invest in professional strategies via Vault;

Strategy parameters are transparent and auditable;

Yields are often higher than traditional shared pool models;

The non-custodial exit mechanism is stronger, theoretically "can leave at any time."

However, the price for this is also clear: protocol risks are partially replaced by manager risks. This means that if the Curator's risk preferences are too high, their capabilities are insufficient, or governance defenses are too weak, localized risk events may still occur.

It is worth noting that lending protocols are being redefined by "institutional entrances." Since 2026, Morpho has seen multiple institutional collaborations and integrations: a partnership agreement with Apollo Global Management allows it to access the MORPHO on-chain lending market within certain limits and restrictions; meanwhile, custodians/providers like Anchorage Digital and Taurus offer pathways for "accessing Morpho Vaults within compliance workflows." Bitwise has also entered the Morpho ecosystem as a Curator, further enhancing the narrative that "Vault = on-chain product shell available to institutions."

4. Two paths, fundamentally a trade-off

Ultimately, Aave V4 and Morpho V2 do not replace each other but represent two possible futures for DeFi lending:

Aave V4 chooses "unification + expansion": The goal is to become the largest liquidity network, embracing institutions and RWA;

Morpho V2 chooses "modular + customized": The goal is to hand over pricing power and asset management authority to the market to the greatest extent.

For ordinary investors, a more realistic way to understand is not "who is more advanced," but "who is more suitable for your capital usage": funds that value underlying assets, low volatility, and prioritize protocol scale are more suitable for Aave; those willing to research Curators, seeking higher yields and more refined strategies, are more suited to Morpho.

V. Risks, Opportunities, and Future

If the past market understanding of lending protocols was still at the level of "deposit money to earn interest" or "collateral to borrow money," then entering the era of Aave V4 and Morpho V2, what truly needs to be re-recognized is the risk structure itself. At the same time, lending protocols are also welcoming a clear new opportunity: product modularization, institutional access, and credit expansion driven by RWA.

1. Risks and Issues

1) Oracle and parameter configuration risks: The wstETH incident at Aave in March 2026 illustrates that even if the protocol itself does not have bad debts, any slight deviation in oracle or exchange rate parameters can still trigger large-scale liquidations. More importantly, liquidation gains are often taken by external liquidators first, and whether and how to compensate afterwards ultimately depends on the DAO's governance willingness and execution efficiency. For users, this means that "the protocol has no bad debts" does not equal "users have no losses."

2) Governance and organization risks: Many past investors took for granted that top protocols have mature governance and stable teams, but several core service providers of Aave have recently departed, revealing another side: as protocols grow larger, risk management is no longer just a technical issue but can become a matter of budgeting, voting rights, accountability mechanisms, and organizational structures. For ordinary users, this kind of risk will eventually manifest in three areas: whether the parameters are still being well-maintained, whether rapid coordination can occur during a crisis, and whether budget resources are actually being spent on safety or on growth.

3) Vault/Curator risks: This is particularly important in the Morpho system. Vaults V2 utilizes mechanisms like Owner, Curator, Allocator, Sentinel, timelock, veto, etc., to transfer traditional asset management industry's "permission isolation, delayed operations, investor protection" onto the blockchain. However, just because mechanisms exist does not mean risks automatically disappear. It requires users to be willing and capable of reviewing the management structure behind the Vault—who the Owner is, who the multi-sig members are, how long the timelock is, whether there is a Guardian veto, and whether there have been instances of aggressive parameter settings in history. If this is not achievable, then "non-custodial" does not mean "no risks," but just shifts risks from the protocol layer to the manager layer.

4) Smart contract and runtime risks: This includes code vulnerabilities, logical flaws, boundary condition triggers, abnormal cross-contract interactions, and congestion and delays in on-chain execution during extreme market conditions. Protocols like Morpho have indeed adopted multi-layered security practices such as formal verification, fuzzing, code audits, and bug bounties, but no team can prove that "risks have been completely eliminated." In on-chain finance, the more realistic situation is that risks can only be diversified, mitigated, or delayed, but it is very difficult to completely eradicate them.

2. Opportunities and Space

Alongside the increased risks, new spaces are opening up for lending protocols.

1) The lending market is transitioning from "unified products" to "modular financial building blocks." Aave V4's hub-and-spoke architecture essentially creates a public foundational layer for liquidity, allowing different assets, risk levels, and business goals to share the same liquidity framework; while Morpho V2 further hands over pricing power to the market and Curators, introducing structures like fixed terms and fixed rates, bringing on-chain lending closer to the product forms of traditional credit markets. Future lending protocols may no longer be a single product but a suite of underlying financial engines.

2) Institutionalization is no longer just a narrative but is becoming a clear product path. Whether it’s partnerships with institutions like Apollo, or the entry of Bitwise, Steakhouse, and Gauntlet as Curators, it all indicates that on-chain lending is gradually embedding itself into more familiar institutional workflows and compliance frameworks. In the past, DeFi resembled markets among crypto-native users; today, it begins to attempt to accommodate larger-scale, more professional funds that have higher requirements for processes and permissions.

3) RWA and credit layering are broadening the asset boundaries of lending protocols. Although under current accounts, the TVL of RWA Lending is still notably smaller than traditional crypto-collateralized lending, its significance extends far beyond mere scale. What is truly important is that products closer to real credit structures have begun to appear on-chain: layered fund pools, delegated management, off-chain cash flows, and off-chain recovery mechanisms. The subjects served by lending protocols will gradually expand from "pure crypto-collateralized assets" to a broader range of revenue rights and cash flow assets.

Conclusion

DeFi lending in the V4/V2 era is no longer a simple "on-chain deposit and loan machine," but is becoming the core engine for the migration of traditional financial infrastructure onto the chain. It marks the transition of the crypto world from "the barbaric growth of high-yield experiments" to "a professionalized, modular, and institution-friendly financial operating system."

The two upgrade paths of Aave and Morpho jointly address the same macro proposition: should on-chain lending resemble a super bank or an open asset management platform? The answer may lie in integration—RWA will inject real-world credit, cross-chain unification will break liquidity islands, and institution-level non-custodial mechanisms will lower entry barriers. This evolution ultimately points to a broader future: DeFi is no longer an exclusive playground for crypto natives, but rather a structural reconstruction of global capital aiming to achieve "borderless, permissionless, and highly efficient" financial services.

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is committed to transforming professional analysis into your practical tools. Through our "Weekly Insights" and "In-depth Research Reports," we analyze market trends for you; leveraging our exclusive segment "Hotcoin Selection" (AI + expert dual screening), we identify potential assets and reduce trial and error costs. Every week, our researchers also engage with you face-to-face through live broadcasts, interpreting hotspots and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and seize value opportunities in Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investments carry risks. We strongly recommend that investors make investments based on a complete understanding of these risks and within a strict risk management framework to ensure the safety of their funds.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。