Original Title: "Stanford's 423-Page AI Report Released, US-China Gap Only 2.7%, Tsinghua's DeepSeek Enters Global Top Ten"

Original Authors: Hao Kun, Peach, New Intelligence Yuan

Introduction: Stanford's "2026 AI Index Report" has been grandly released! This 432-page long document is highly valuable: the peak confrontation between US and China in AI has nearly closed the gap, reducing it to merely 2.7%. The world's top AI production annually is 95, mostly concentrated in large companies. The harshest reality is that employment for developers aged 22-25 has been cut by 20%.

On April 13, Stanford HAI officially announced the "2026 AI Index Report"!

This annual report, spanning 423 pages, comprehensively reveals the latest power map of the global AI industry.

It presents a core conclusion: AI's capabilities are increasing rapidly; however, humanity's ability to measure and manage them has not kept pace.

Among these, the most shocking conclusion is —

The performance gap of AI models between the US and China has essentially vanished, with frequent role reversals in peak confrontations, and currently, Anthropic's lead advantage is only 2.7%.

The US spends more on AI than anyone else, but attracting top talent has become increasingly difficult.

The report also notes that the evolution of AI has not encountered so-called "bottlenecks," but is instead skyrocketing at an unprecedented rate.

In the past year, over 90% of the world's top models have matched or even surpassed human performance in doctoral-level scientific questions, multimodal reasoning, and competitive mathematics.

Notably, in coding capabilities, SWE-bench scores have surged from 60% to nearly 100% in just one year.

However, the phenomenon of "specialization" in AI is extremely severe, presenting a distorted status quo:

LLM can achieve IMO gold medals, yet fails to read a simulation clock with an accuracy of only 50.1%.

Meanwhile, the job-stealing phenomenon of AI has shifted from prediction to reality, and the first to suffer are contemporary young "workers."

Next, let's directly present the key points, the 12 hardcore trends worth noting in the "2026 AI Index Report."

Other Highlights at a Glance:

· Global AI computing power has increased 30-fold in 3 years, with NVIDIA holding 60%, and nearly all chips coming from TSMC

· Global corporate AI investment is projected to reach $581.7 billion by 2025, doubling year-on-year, with the US accounting for nearly half

· The number of AI researchers entering the US has dropped 89% in 7 years, with an 80% reduction in just the past year

· Employment for software developers aged 22-25 has declined by 20% since 2024, with entry-level positions being precisely cut

· China has established 85 public AI supercomputers, more than double that of North America, ranking first globally

· AI usage rate in Chinese workplaces exceeds 80%, far surpassing the global average of 58%

· The strongest models are increasingly opaque, with 80 out of 95 representative models lacking publicly disclosed training codes

US and China Face-to-Face, Gap Reduced to 2.7%

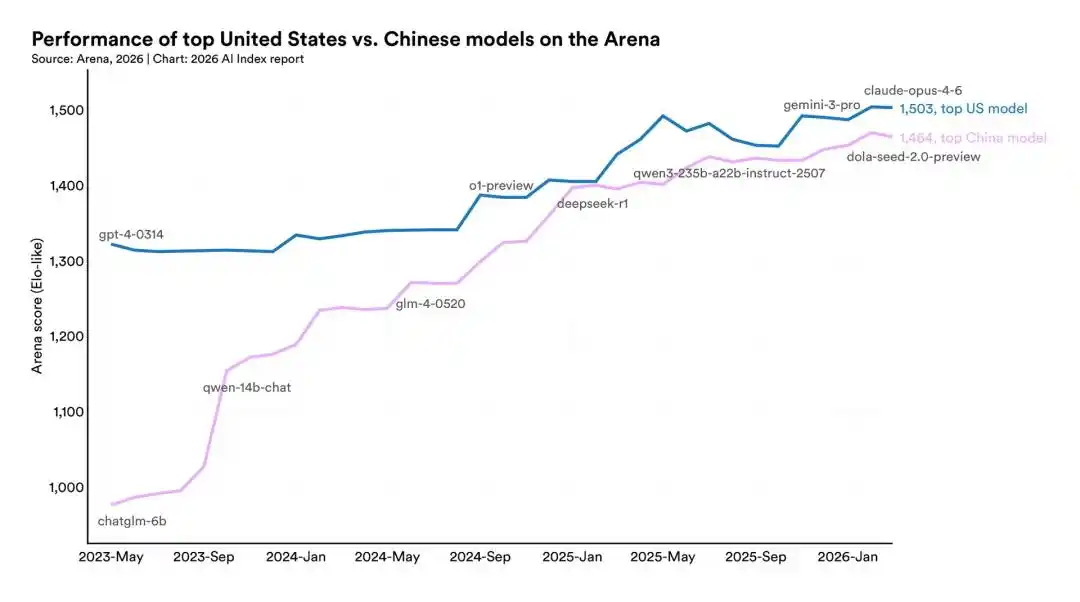

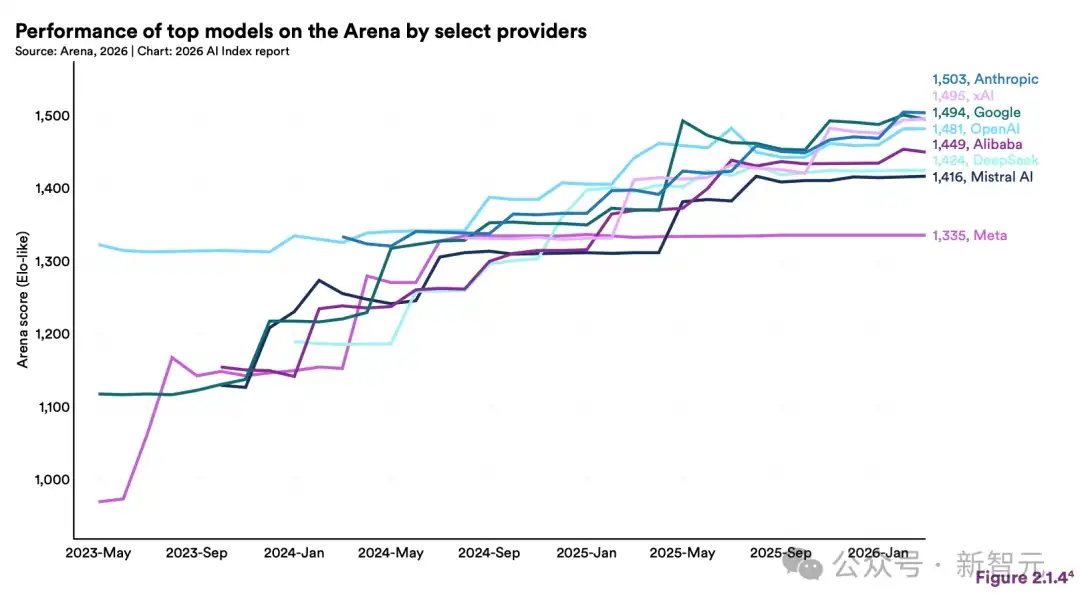

Stanford has plotted the top-ranking models from the US and China on the same coordinate system since May 2023.

In May 2023, gpt-4-0314 scored 1320 points in the lead, while China's top was still chatglm-6b, with a gap of over 300 points.

In February 2025, DeepSeek-R1 briefly matched the leading US models.

In March 2026, the US's Claude Opus 4.6 scored 1503 points, while China's dola-seed-2.0-preview scored 1464 points.

Now, the gap between US and China AI is only 39 points. Converted to a percentage, that's 2.7%.

More noteworthy is the frequency of role changes in the past year. Starting from early 2025, top models from both countries have exchanged positions multiple times on Arena.

In quantity, they are also nearly equal.

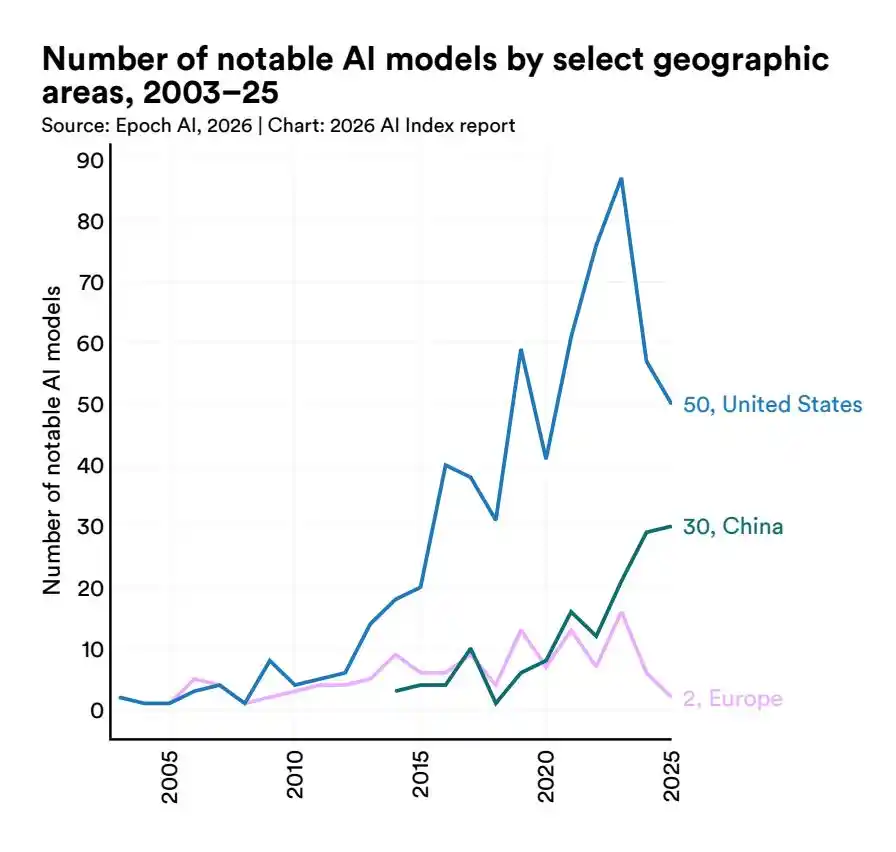

In 2025, the US launched 50 "notable models," and China followed closely with 30 top models.

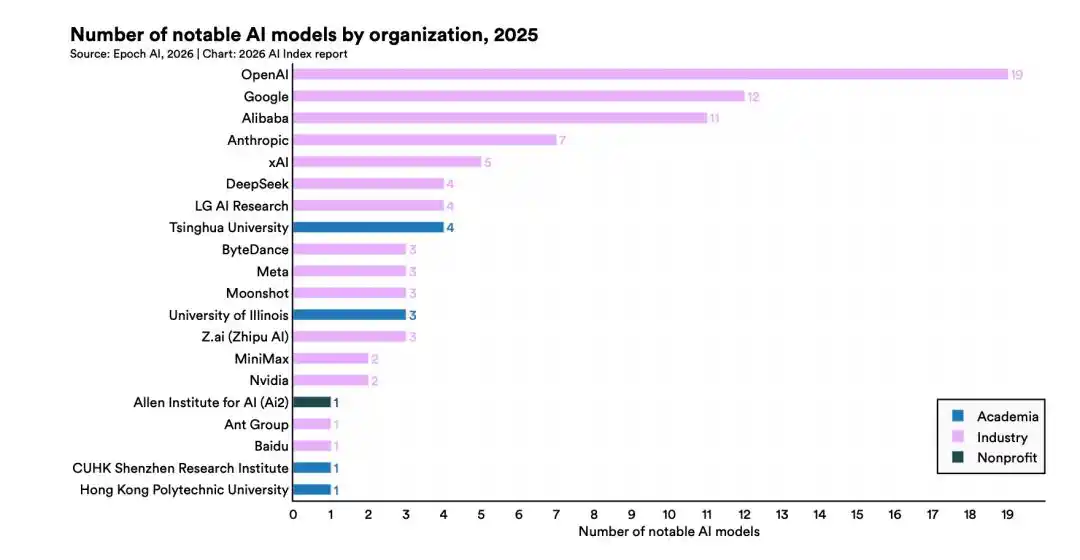

Among the first tier are OpenAI, Google, Alibaba, Anthropic, and xAI, sharing evenly the global TOP 5.

Further down to TOP 10, Chinese institutions and enterprises occupy four spots: Alibaba, DeepSeek, Tsinghua, and ByteDance.

This year, the focus of the open-source ecosystem has clearly shifted eastward.

DeepSeek, Qwen, GLM, MiniMax, Kimi have pushed the capability curve of open-source weights forward.

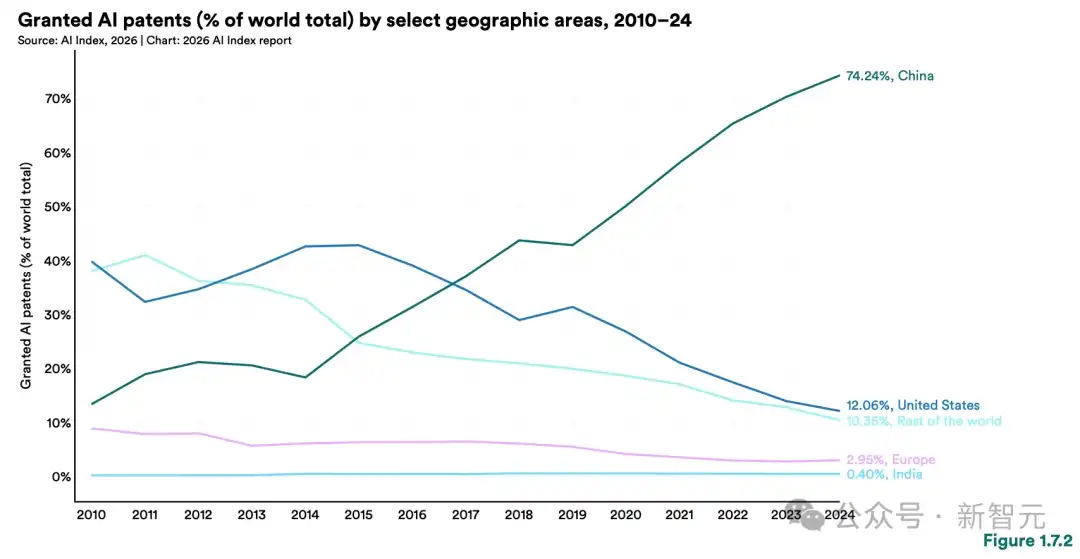

Including paper publication volume, citation counts, patent output, and industrial robot installations, China leads globally.

The price aspect presents another front.

Overseas developers have calculated a figure, estimating that the output price of Seed 2.0 Pro is about one-tenth of that of Claude Opus 4.6.

Performance is closely matched, yet the price is only one-tenth. The chain reaction of this will just begin.

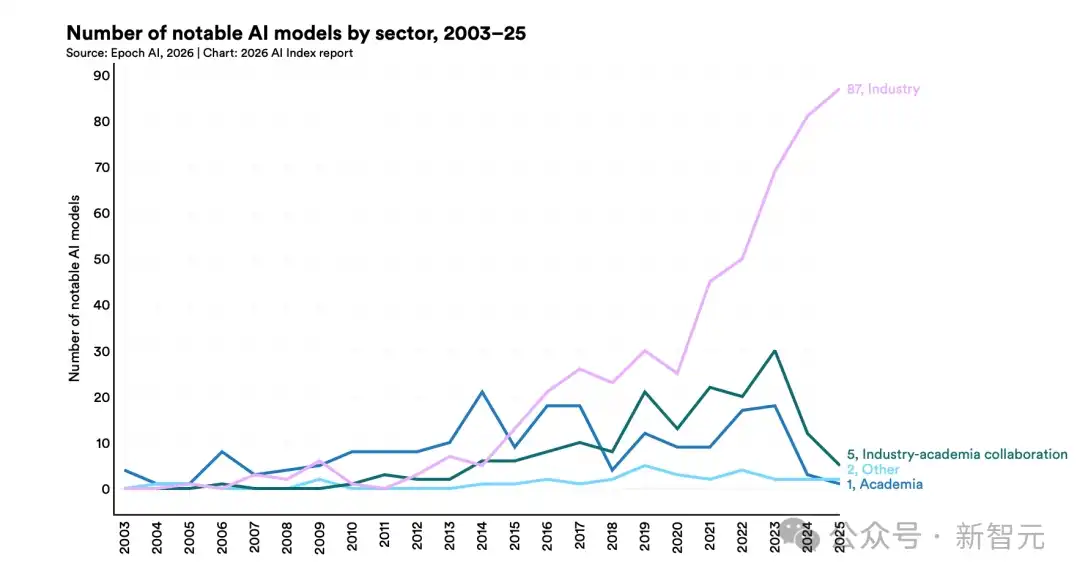

90% of Cutting-Edge Models Come from Industry, Speed of Commercialization Unprecedented

Among the 95 most representative models released last year, over 90% came from the industry, not academic institutions or government labs.

The academic community has fallen behind the cutting edge.

The release speed is also accelerating alarmingly.

In February 2026 alone, there were eight to nine flagship models released simultaneously, including Gemini 3.1 Pro, Claude Opus 4.6, GPT-5.3 Codex, Grok 4.20, Qwen 3.5, Seed 2.0 Pro, MiniMax M2.5, and GLM-5.

The timeline for achieving greatness has shifted from "years" to "months."

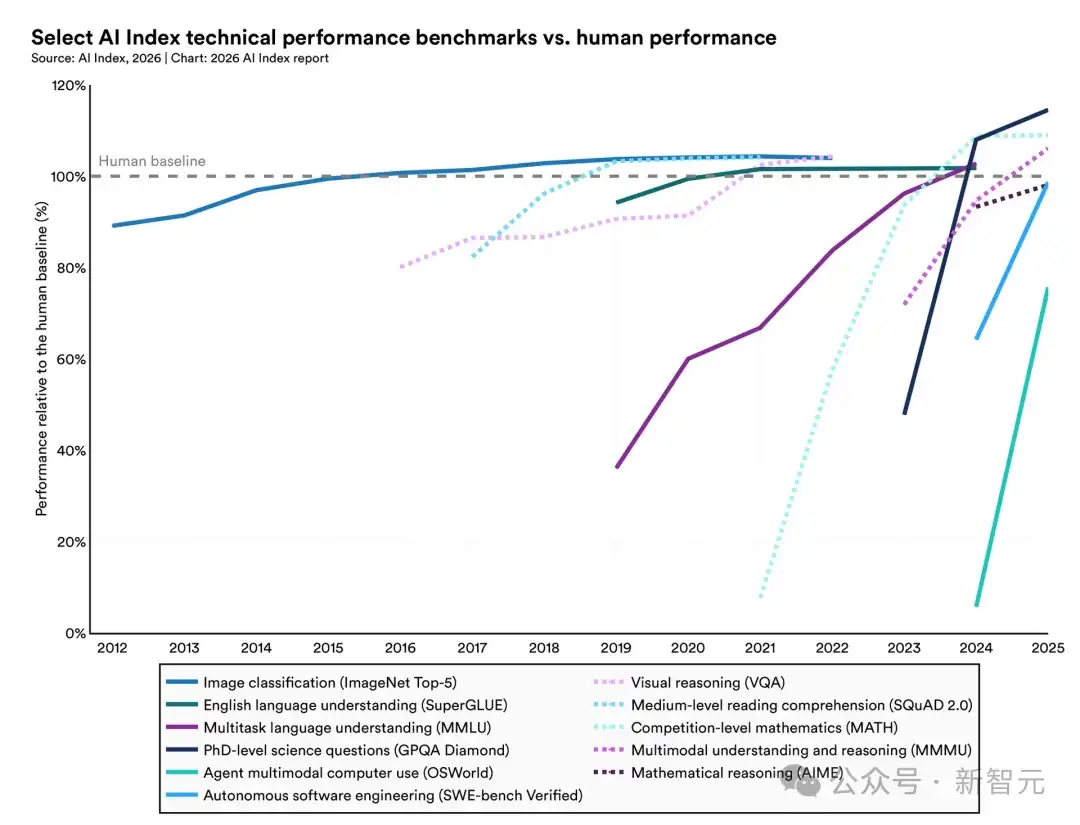

Benchmark Peak Reached in One Year, AI Has No Bottlenecks

The most striking curve is programming.

SWE-bench Verified, a benchmark for real bug-fixing, has risen from 60% to nearly 100% in just one year.

This is not just a few percentage points; it has essentially reached a ceiling.

Terminal-Bench testing the Agent's ability to handle real terminal tasks has increased from 20% last year to 77.3%.

The success rate of network security Agents solving problems has increased from 15% to 93%.

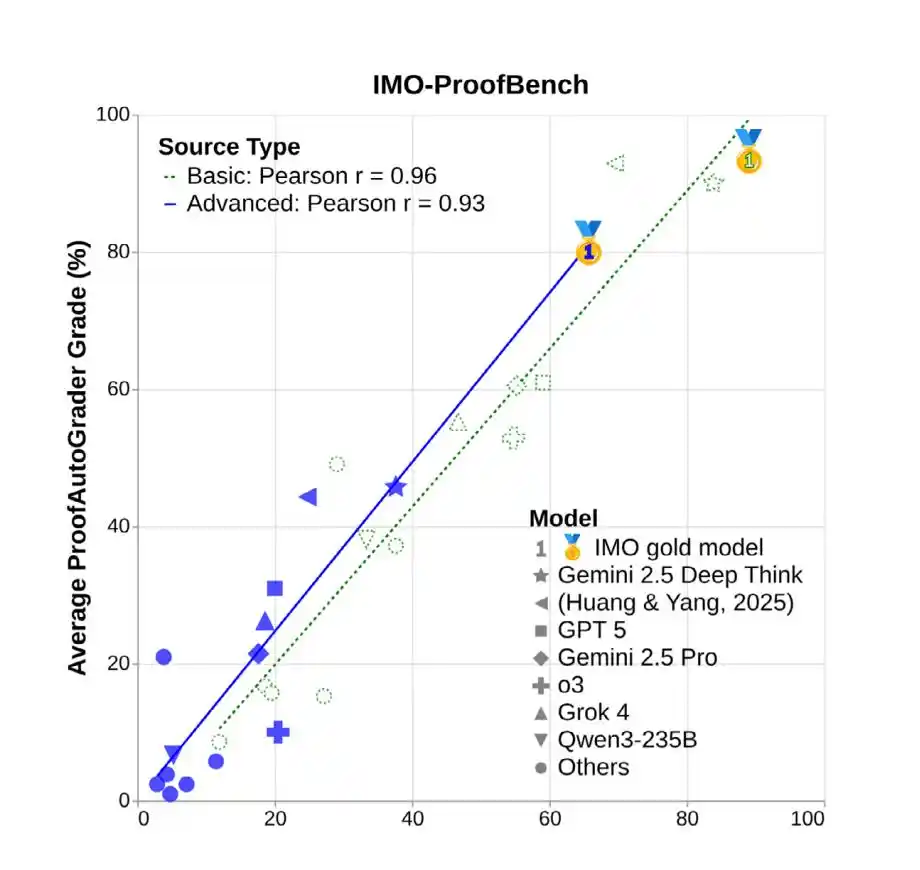

Gemini Deep Think has won a gold medal in the International Mathematical Olympiad.

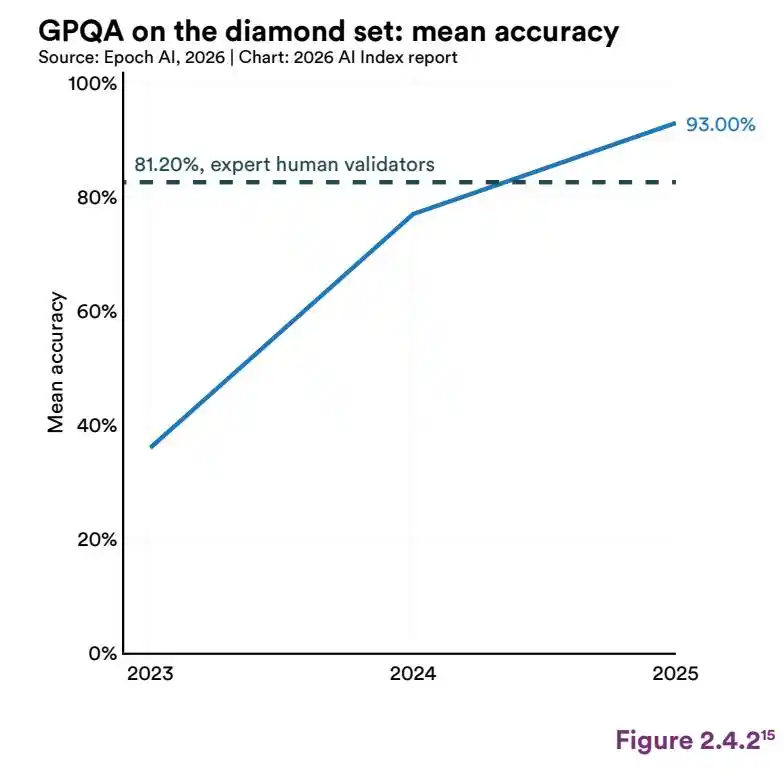

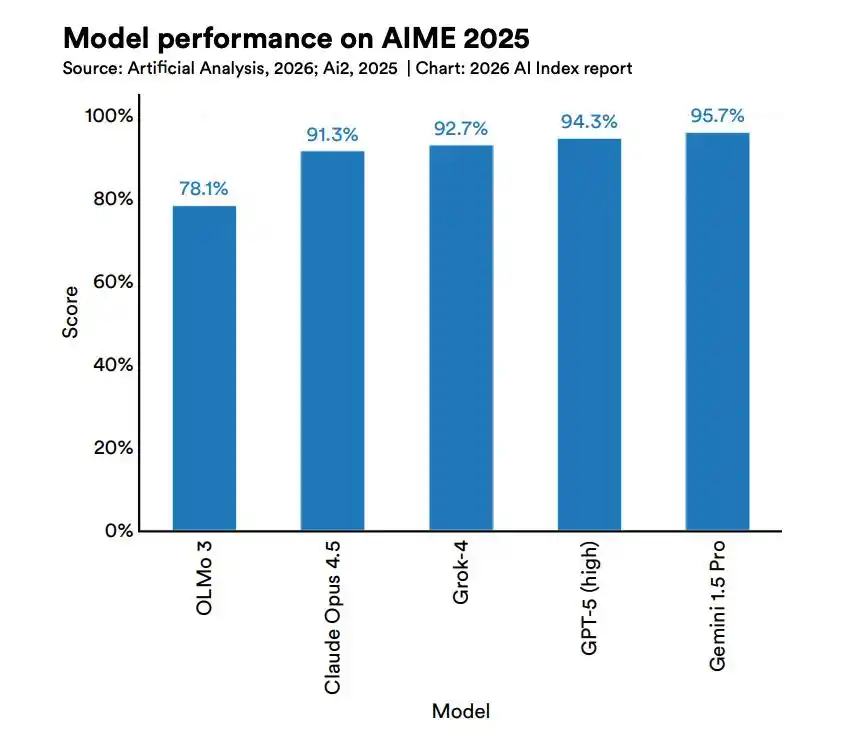

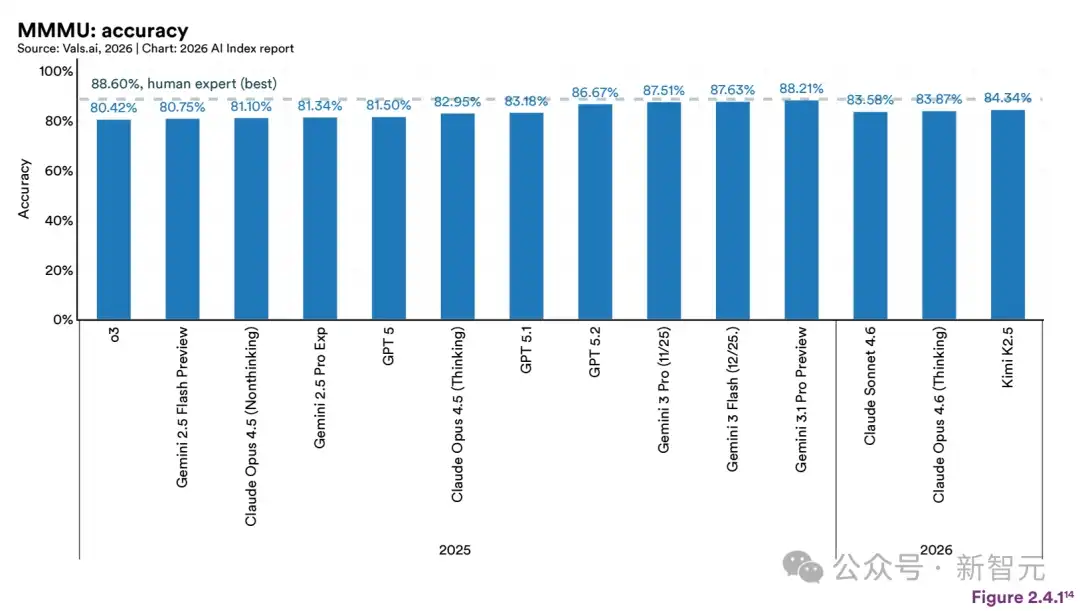

PhD-level scientific questions (GPQA Diamond), competitive mathematics (AIME), and multimodal reasoning (MMMU) — once deemed "unattainable by humans" — have all been tackled by cutting-edge models.

The most illustrative case is Humanity's Last Exam.

This test was specifically designed to "stump AI and favor human experts," with questions provided by top experts from various fields.

Last year, OpenAI's o1 scored 8.8%, while cutting-edge models have pushed that score up by 30 percentage points in a year, with Claude Opus 4.6 and Gemini 3.1 Pro now both exceeding 50%.

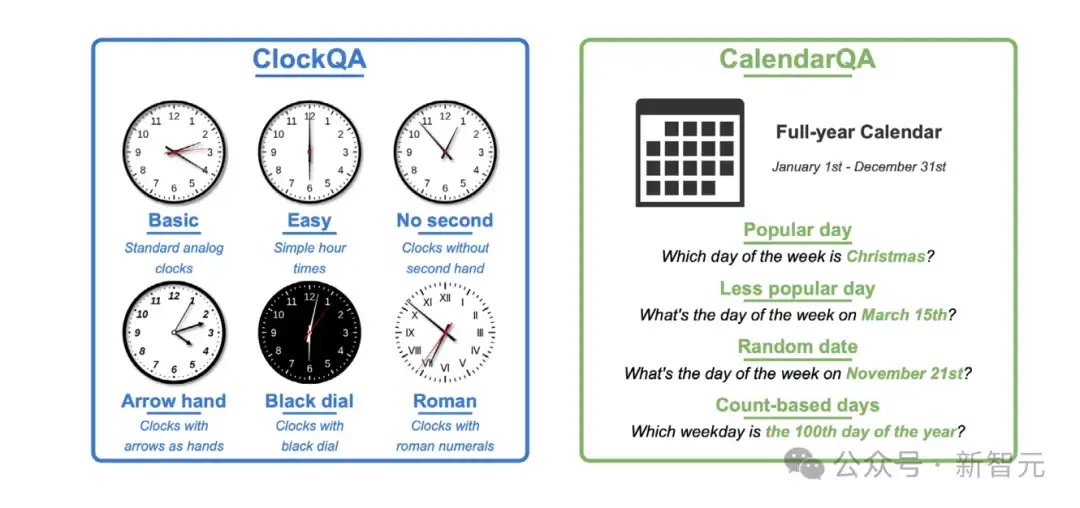

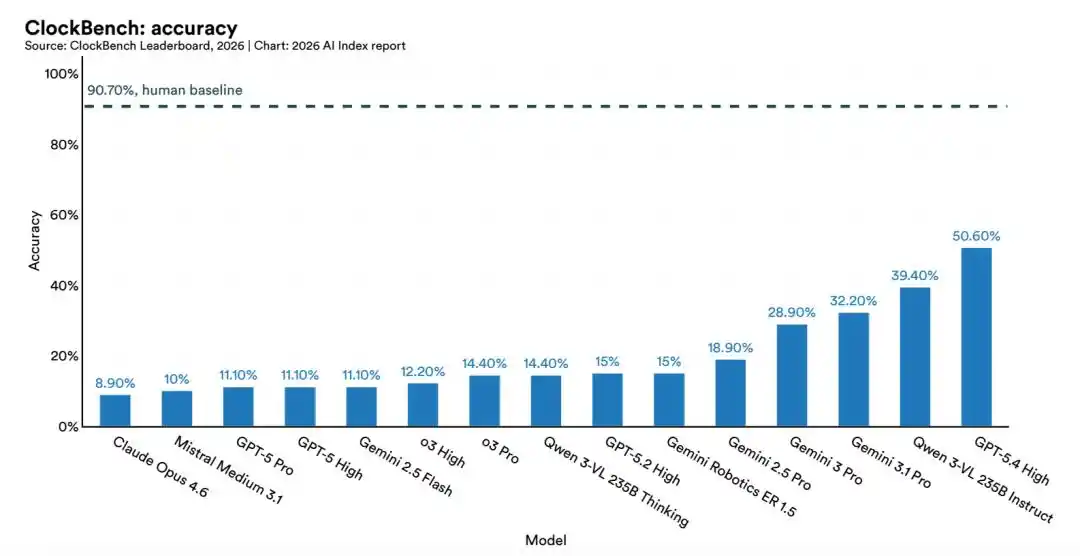

Sawtooth Frontier: Can Win IMO Gold but Can't Read a Clock

Yet the same index has revealed another set of figures.

The strongest models achieved only 50.1% accuracy on the "reading a simulation clock" task.

In laboratory simulation environments (RLBench), robots have achieved an operation success rate of 89.4%. However, when moved to real household scenarios to complete tasks like washing dishes or folding clothes, the success rate immediately drops to 12%.

The gap between the laboratory and the kitchen is 77 percentage points.

Researchers have named this phenomenon the "jagged frontier." The distribution of AI capabilities is uneven, capable of winning math Olympic gold medals but unable to reliably tell the current time.

AI can win math Olympiad gold medals but has only a 50% chance of reading a simulation clock. AI is accelerating, but not in the same direction.

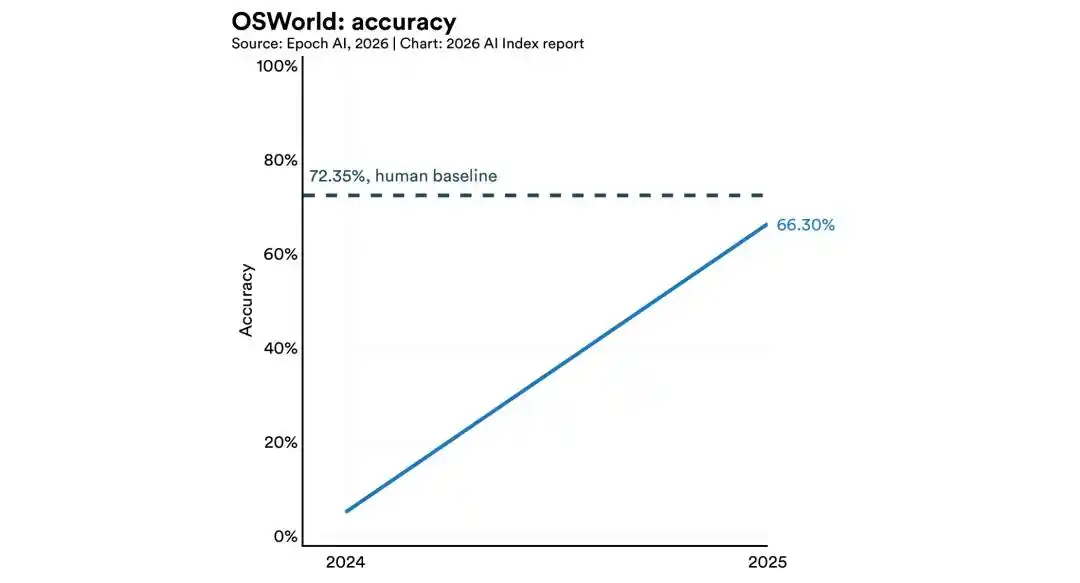

Additionally, in agent tasks, the OSWorld test shows that cutting-edge AI strength (66.3%) is approaching the human baseline.

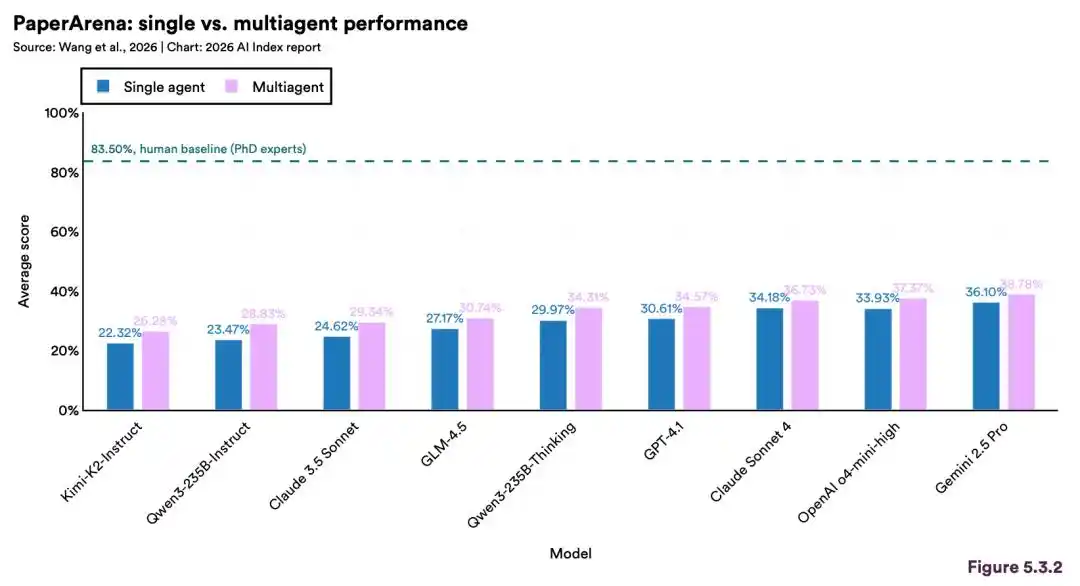

However, in the PaperArena test, specifically assessing scientific logic, the strongest AI-powered agent scored only 39%, which is only half the ability of a PhD student.

This unevenness does not deter businesses from integrating AI into production lines.

The AI Index provides another figure showing that the global enterprise AI adoption rate has reached 88%. 90% of companies have integrated AI into some workflow.

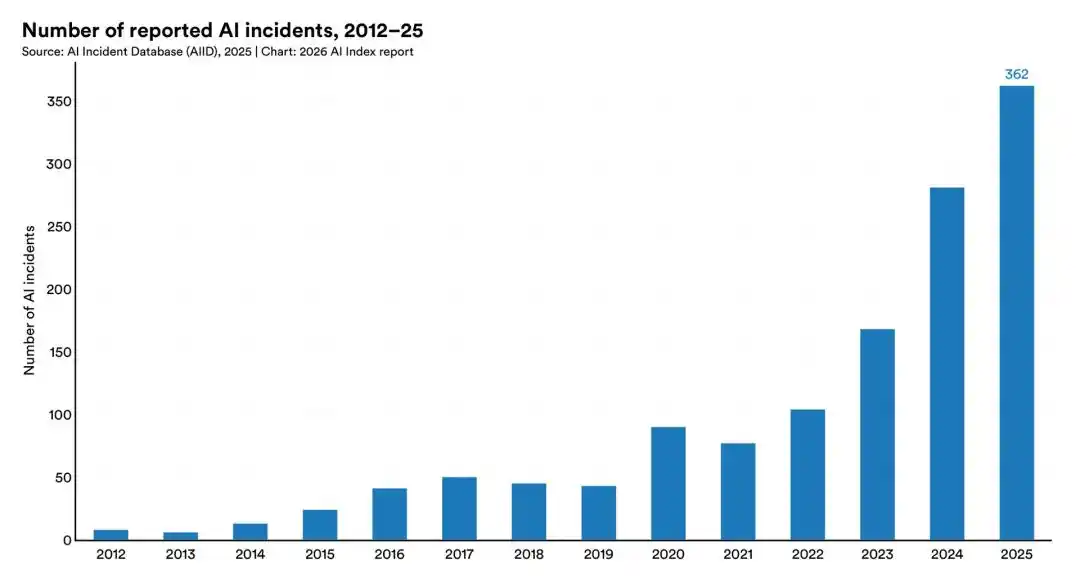

The cost is also rising. Records of AI-related incidents jumped from 233 in 2024 to 362.

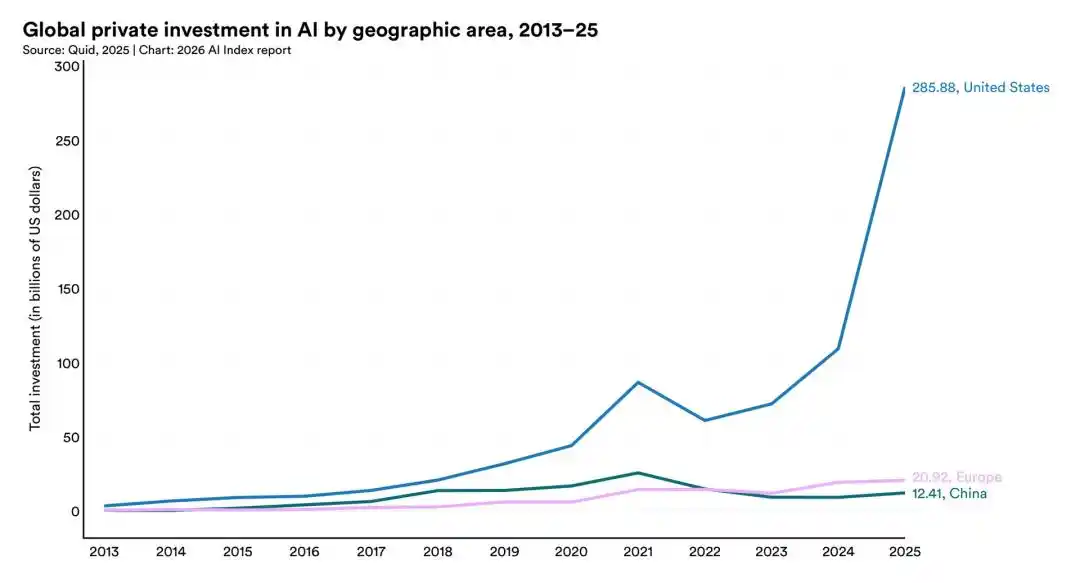

Money is Accelerating, $581.7 Billion Invested in AI

By 2025, global corporate AI investment is expected to reach $581.7 billion, an increase of 130% year-on-year. Private investment accounted for $344.7 billion, up 127.5% year-on-year.

Both curves are nearly doubling.

In terms of countries, the US is far ahead. In 2025, the US private AI investment reached $285.9 billion, with 1,953 new AI startups launched in a year, over ten times the second-ranked country.

Money is rapidly flowing into the US. However, another core resource in the US is moving in the opposite direction.

People are Leaving, AI Researchers Entering the US Down 89%

There is a set of numbers that left people stunned.

From 2017 to now, the number of AI researchers and developers entering the US has decreased by 89%.

More critically, this decline is accelerating. In just the past year, the rate of decline reached 80%.

The US remains the country with the highest density of AI researchers, but the influx is tightening.

The two curves of money and people are beginning to reverse. This situation has not been seen in the last decade.

Computing Power Has Increased 30-Fold in Three Years, Core Reliant on One Company

The curve of AI capability is accelerating, but the curve of computing power is running even faster.

From 2021 to now, global AI computing power has increased 30-fold. In the past three years, it has been tripling each year.

This curve is supported by a few companies.

NVIDIA alone occupies over 60% of the world's AI computing power. Amazon and Google rank second and third with their self-developed chips, but combined they still fall far short of NVIDIA.

Almost all these chips come from one foundry, TSMC. The steeper the computing power curve, the narrower the core reliance.

Meanwhile, the cost is also increasing.

The total power of global AI data centers has reached 29.6 GW, equivalent to New York state's total electricity demand during peak hours. The estimated carbon emissions from training xAI Grok 4 amount to 72,816 tons of CO2 equivalent, equivalent to the annual emissions of 17,000 cars.

Where data centers are built, where electricity comes from, and where chips are produced — these three issues have become the biggest headaches for CEOs of all AI companies this year.

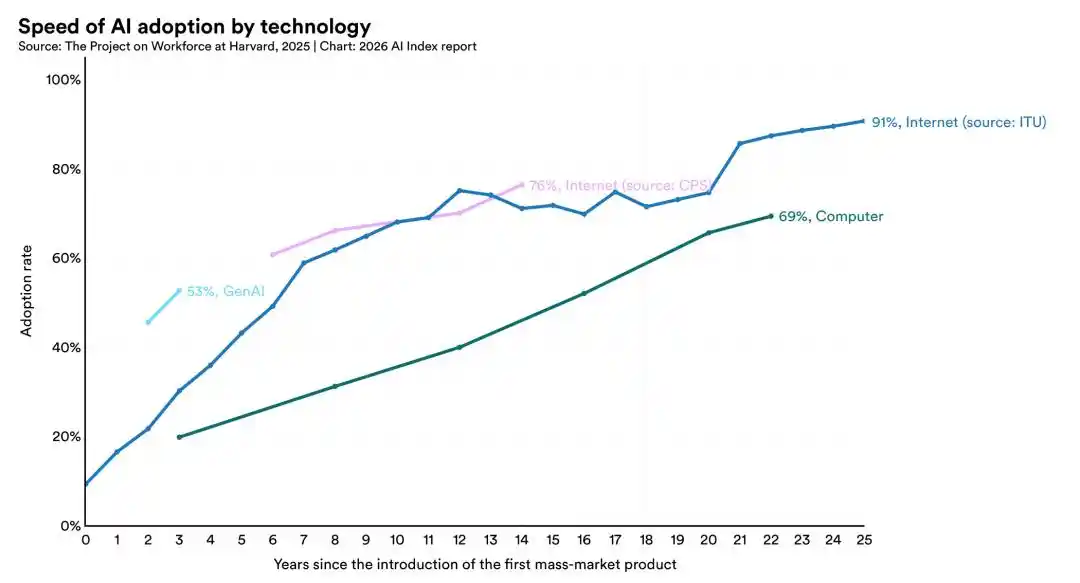

Generative AI 53% Penetration in Three Years, China's Workplace Usage Rate Over 80%

Generative AI has achieved a 53% penetration rate in the global population within three years.

This speed is faster than that of personal computers, and faster than the internet.

However, the penetration rate is strongly correlated with nationality. Singapore 61%, UAE 54%, both ahead of the US. The US ranks 24th among surveyed countries, with a penetration rate of 28.3%.

When changing the dimension from consumers to workplaces, the contrast becomes even starker.

Another set of data from the report shows that by 2025, 58% of employees globally have begun to use AI regularly at work. But in five countries — China, India, Nigeria, UAE, and Saudi Arabia — this proportion exceeds 80%.

China's workplace AI penetration rate is already over 20 percentage points higher than the global average.

More interestingly, concerning consumer value,

AI Index estimates that by early 2026, generative AI tools will create $172 billion in value for US consumers annually. From 2025 to 2026, the median value for each user has tripled.

The vast majority of users are still using the free version.

The money ordinary people are willing to pay for AI is far less than the value AI brings them. This gap is what all AI companies are attempting to bridge now.

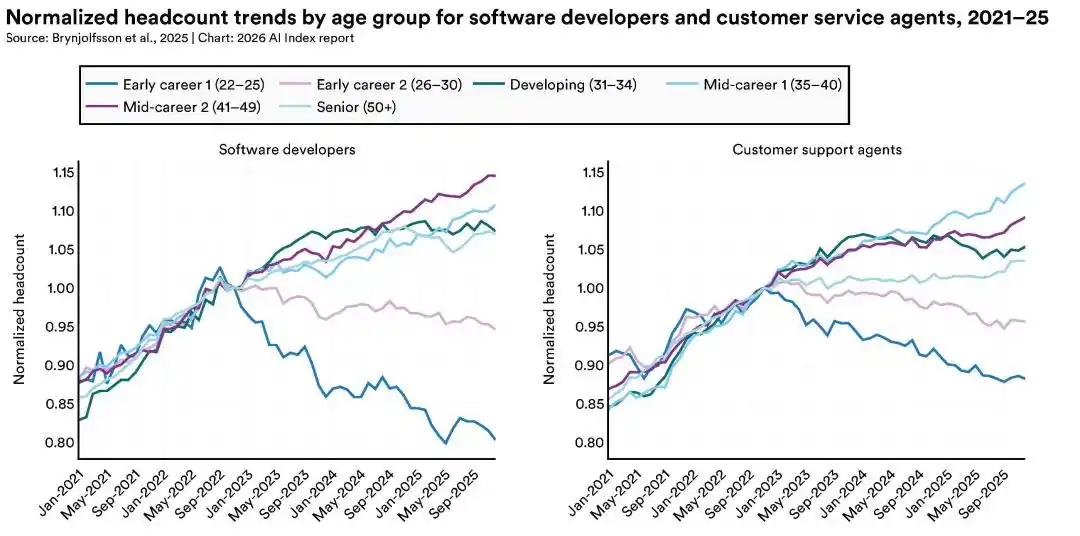

Entry-Level Positions Sharply Declined, 22-25 Age Developer Jobs Cut by 20%

The part of the AI Index that may leave Chinese readers silent is about young employment.

For software developers aged 22 to 25, the number of jobs has declined by about 20% since 2024.

During the same period, the older cohort has actually seen growth.

It's not just developer roles. Customer service and other high AI-exposure industries are also seeing the same pattern.

What’s more concerning is the results of executive surveys. Respondents generally anticipate that future layoffs will be larger than those in the past few months.

This is not merely about macro unemployment rates; it is about the precise cutting of entry-level positions.

With the first job gone, the entire career ladder is disrupted. The long-term impacts of this are currently unquantifiable.

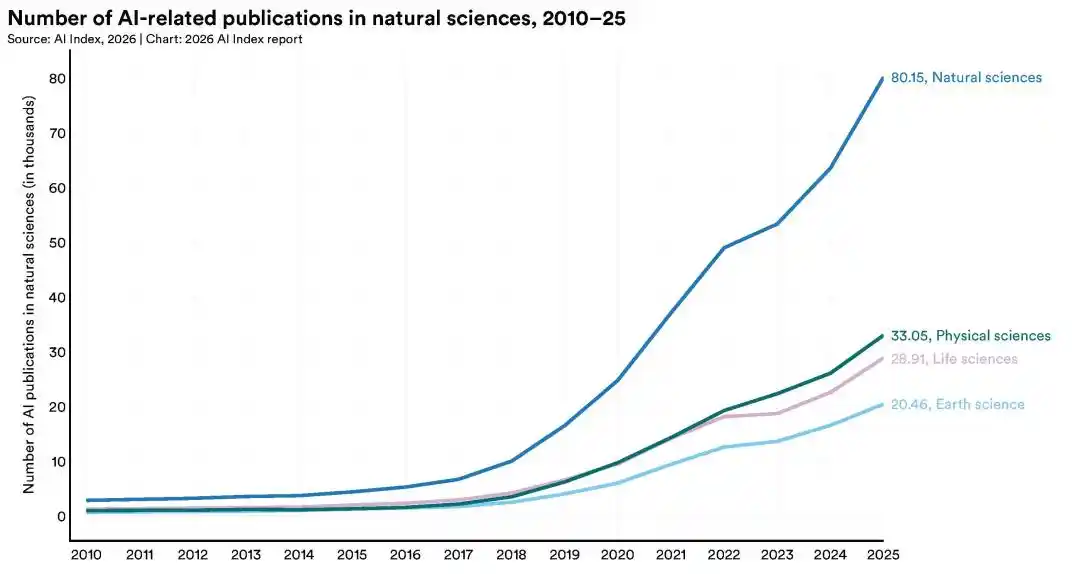

AI is Redefining the Way Scientific Discoveries are Made

If the employment section is cold, the one on science is hot.

AI-related papers in the fields of natural science, physical science, and life science grew by 26% to 28% year-on-year in 2025.

Specifically in applications, this year for the first time AI has successfully run the end-to-end weather forecasting process, directly outputting temperature, wind speed, and humidity from raw meteorological observation data without any involvement of traditional numerical models.

AI is shifting from "helping you write papers" and "helping you calculate numbers" to "making discoveries itself."

The same applies in hospitals. In 2025, numerous hospitals began deploying AI tools capable of automatically generating clinical records from patient consultations. Feedback from multiple hospital systems' doctors indicates that the time spent on writing medical records has decreased by up to 83%, and work fatigue has significantly decreased.

However, the same index doused cold water on medical AI. A review of over 500 clinical AI studies found that nearly half of the studies relied on exam-style datasets, with only 5% using real clinical data.

While AI can reduce the time doctors spend typing, its clinical value on real patients still raises numerous questions.

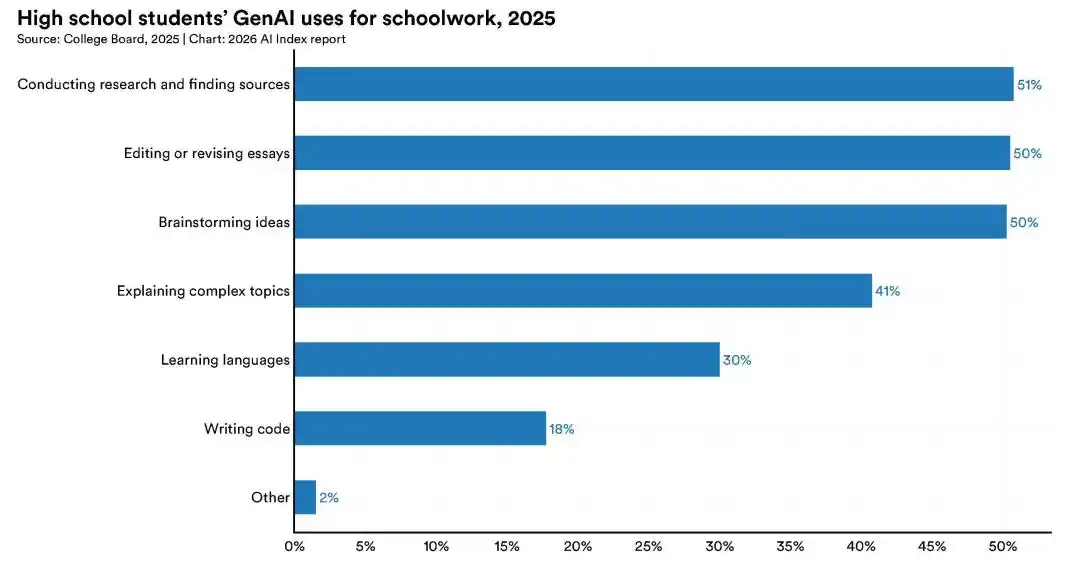

The Self-Learning Wave is Exploding Globally, Formal Education has Fallen Behind

Formal education cannot keep up with AI.

Currently, 4/5 of high school and college students in the US use AI to complete school assignments. However, only half of secondary schools have AI usage policies, and merely 6% of teachers believe these policies are clearly written.

Students are outpacing teachers, who are still in place, and rules have not yet emerged.

While formal education struggles, a wave of self-learning is explosively emerging globally. The report states that the top three countries showing the fastest growth in AI engineering skills are the UAE, Chile, and South Africa.

Not the US, not Europe.

The steepest part of the skills curve is developing where no one is watching.

The Strongest Models Become the Least Transparent, Experts and Public Split

The strongest models are becoming the least transparent models.

The average score of the Foundation Model Transparency Index has dropped from 58 to 40 this year. The AI Index specifically names that Google, Anthropic, and OpenAI have abandoned disclosing the latest model training data scale and training duration.

Of the 95 most representative models released last year, 80 did not disclose their training codes.

The sentiments of the public have also become more complex.

World-wide, the proportion of those who believe AI's benefits outweigh its drawbacks has increased from 52% to 59%. However, during the same period, the proportion of those feeling anxious about AI rose from 50% to 52%.

Both directions are increasing simultaneously.

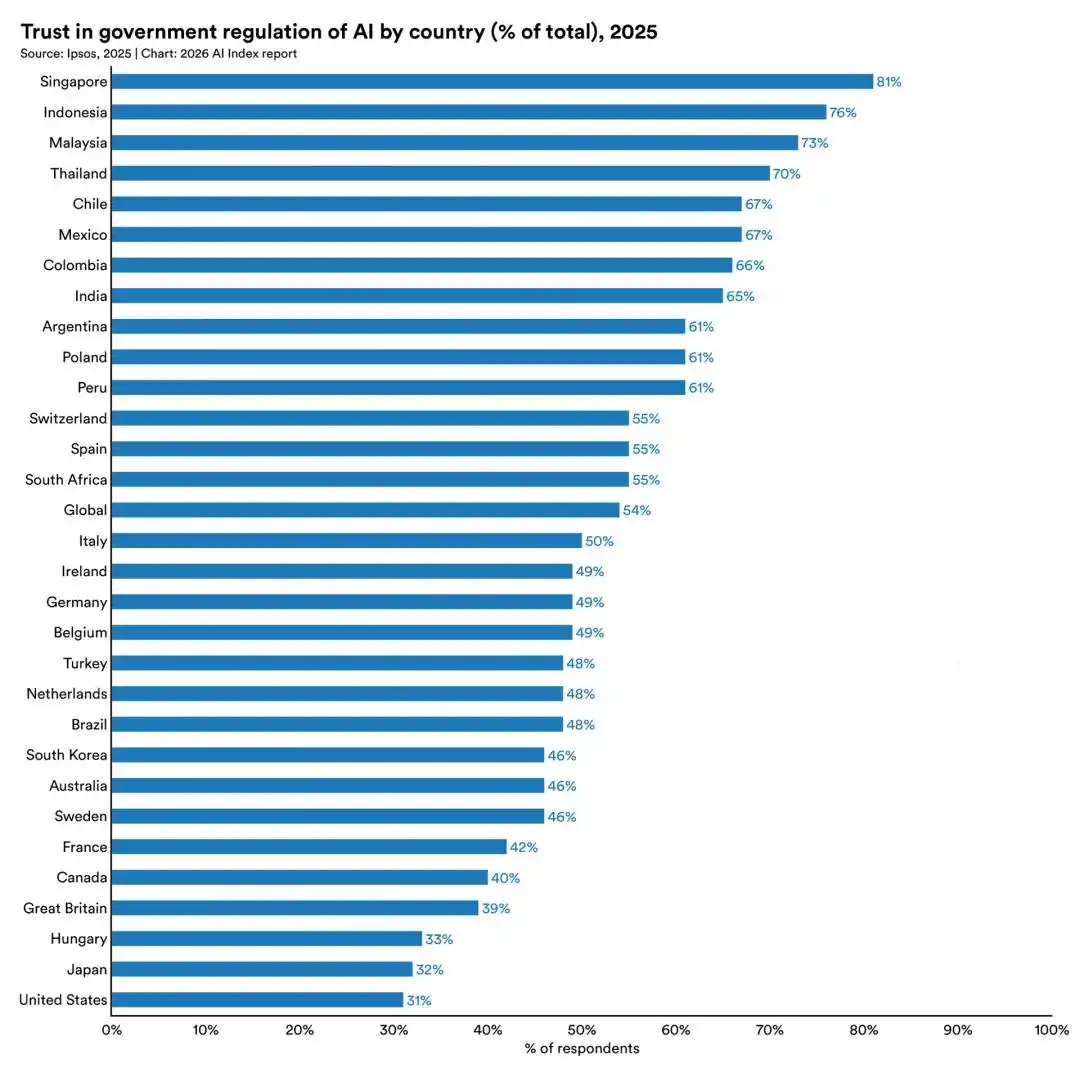

Most divided is the US. Only 33% of Americans believe AI will make their jobs better, while the global average is 40%. Americans have the lowest trust in their government's regulation of AI among surveyed countries, at 31%.

Singaporeans have an 81% trust in their government's regulation of AI.

Following a recent attack on Sam Altman's home, people in Silicon Valley were "surprised to find" that ordinary people in Instagram comments did not express sympathy, and some even felt "it should be more intense."

They are unaware that things have deteriorated to this level.

The research report cites data from Pew and Ipsos showing that the gap in perception between experts and the public regarding AI's impact on employment, healthcare, and the economy generally exceeds 30 percentage points, with the largest gap reaching 50 percentage points.

On one hand, curves in the lab are skyrocketing; on the other, ordinary people's anxiety is accumulating.

There is no bridge between them.

Final Note

Within the 423-page report are hundreds of charts, but essentially, it draws just one chart.

The horizontal axis represents time, and the vertical axis represents capability.

The curves of model capabilities are soaring, computing power curves are soaring, investment curves are soaring, and adoption rate curves are soaring. Everything else is stagnating or declining.

This encapsulates the entirety of the 2026 AI Index.

AI is accelerating. Everything else is disconnecting.

If you are someone in this industry, the question to ask now is not "what will the future hold," but "which curve do you stand on."

Reference:

https://hai.stanford.edu/ai-index/2026-ai-index-report

https://hai.stanford.edu/news/inside-the-ai-index-12-takeaways-from-the-2026-report

https://www.nature.com/articles/d41586-026-01199-z

https://hai.stanford.edu/assets/files/ai_index_report_2026.pdf

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。