Original Title: No Trade Zone

Original Author: Arthur Hayes

Translation: Peggy, BlockBeats

Editor’s Note: The current market is not "directionless," but has entered a "no trade zone" created by the combined effects of AI deflation shocks + geopolitical shocks. The true market status of Bitcoin depends on when the monetary supply will be passively expanded again.

On one hand, AI is reshaping the labor structure, eroding the incomes and credit abilities of knowledge workers, transmitting deflationary shocks to the financial system; on the other hand, energy conflicts and geopolitical games are forcing countries to increase fiscal spending, hoard resources, and maintain operations through money printing. Rising interest rates coexist with monetary supply expansion, causing severe differentiation in risk assets.

The deeper change lies in the monetary system itself. The restructuring around energy channels and settlement paths has loosened the "dollar-asset" loop, with gold and the renminbi passively entering trade settlements at the margins. This structural change has not yet achieved consensus, but its marginal acceleration is enough to influence market expectations.

In such an environment, Bitcoin is no longer an asset under a single logic. It bears the pressure of deleveraging and liquidity contraction while benefiting from expectations of monetary expansion and credit reconstruction. Therefore, price performance appears contradictory, yet it actually reflects the tug-of-war between two systems.

Rather than rushing to bet on direction, the author Arthur Hayes prefers to wait for a signal—when volatility truly spirals out of control and liquidity is forced to be released, the market will re-enter a "tradable" phase. Until then, this area feels more like a place where action should be restrained.

This is precisely the starting point of this article: in a world experiencing both deflation and money printing, the market may be undergoing a rare "no trade zone."

The following is the original text:

Since Maelstrom had almost no trading activity in the first quarter, some of our brokers would occasionally ask me for my views on the market and whether they could do something for us. My usual response is: "Now is a no trade zone."

Other than gradually increasing our position in Hyperliquid, we practically did no trading throughout the entire first quarter.

Two factors combined to create a trading "dead zone," at least for our long-only positions.

First, the rapid spread of agentic AI (what I call "claws"), which has the ability to act autonomously. This technology will destroy the career prospects of ordinary knowledge workers under the "flexible labor" structure in developed Western economies (primarily under the American order, i.e., the Pax Americana system). Accompanying this will be a deflationary financial collapse, which I have discussed in detail in my previous article "This Is Fine."

Second, after that article was published, U.S. President Donald J. Trump, the "emperor/ lead performer," actively initiated a war against Iran to turn it into the latest "trash country (Trashcanistan)," and received support from his somewhat clumsy, belligerent "backup singer," Israeli Prime Minister Benjamin Netanyahu ("the Bedouin butcher").

The war has lasted nearly seven weeks, and the only truly important question now is: how will the circulation of commodities and goods around the Strait of Hormuz be rearranged?

When discussing war or geopolitics, I always like to state upfront: I am just a skiing enthusiast, a crypto participant who dances two steps to house music. I know nothing about war and have no insider information regarding what global leaders will or will not do.

But what I can do is: interpret the mainstream propaganda narrative and use my AI tools to perform some basic calculations with publicly available data. I try to block out the noise and focus only on the variables that truly affect my investment portfolio. Fortunately, I do not live in the Levant or the Middle East, so my life and freedom are not directly at risk.

In my relatively simplistic worldview, three scenarios are worth considering at the moment—strictly speaking, four, but the fourth one, "nuclear Armageddon," has no investability and hence does not require elaboration.

Next, I will introduce these scenarios one by one and analyze how they might affect Bitcoin's price from a more macro perspective.

I don't know the probability of each of these scenarios occurring. But what I really want to clarify is: is there a way to construct a portfolio that, in the best case, can outperform hydrocarbons and their first-order derivatives (like food and fuel prices) in absolute returns; and, in the worst case, cannot outperform energy prices themselves, yet can at least achieve better relative performance against all major asset classes?

Scenario One: Return to Normal

In this scenario, the war ends swiftly, and the pre-war state is largely restored. However, a longer-term trend will not change: the process of replacing high-cost knowledge workers who "operate digital symbols" with cheaper and more efficient AI agents continues to accelerate.

The U.S. economy is most vulnerable in this process, as about 70% of its GDP comes from consumer spending. Consumers pay for their consumerism through bank credit, and these loans constitute assets on the bank's balance sheet. Once the repayment ability of ordinary knowledge workers disappears, these banks will functionally become insolvent, relying solely on the central bank's massive "money printing" to survive.

Scenario Two: Tehran Toll Booth

In this scenario, the U.S. military is either unwilling or unable to prevent Iran from restricting shipping traffic through the Strait of Hormuz.

Iran fulfills its promise: allowing "friendly nations" to pass, but requiring a "toll" of $2 million, payable in renminbi, cryptocurrency, sanctioned dollars, or other diplomatic arrangements.

In the most unfavorable conditions for the "American order" (Pax Americana) financial hegemony, countries must find ways to acquire renminbi. However, since most countries have a trade deficit with China, the only realistic path to obtain a large enough quantity of renminbi is: sell dollar assets (like U.S. Treasury securities or U.S. tech stocks) → buy physical gold → then exchange gold for renminbi in the Shanghai or Hong Kong gold markets.

Among the top ten economies in global GDP rankings, only Brazil and Russia maintain a trade surplus with China, and they only rank ninth and tenth respectively. In contrast, the "American order" itself is the largest economy with a global trade deficit, and its functioning relies on an equally significant capital account surplus to sustain it.

However, when countries begin to sell dollar assets to acquire renminbi or fill commodity gaps at extremely high prices in the spot market, this capital surplus will mathematically contract. The highly financialized economic system of the U.S. relies on foreign capital to finance government spending; once foreign capital decreases, this system can no longer sustain itself.

Ultimately, whether through falling bond prices (rising yields) or declining stock markets, the government will be forced to fill funding gaps through "money printing."

Scenario Two Point Five: Star-Spangled Blockade

A dramatic twist is that after the U.S.-Iran negotiations fail to reach a permanent ceasefire, on April 12 (Sunday), Donald J. Trump announced that the U.S. Navy will block all vessels entering and exiting the Strait.

This blockade could develop into a form of "pirate toll": vessels would be forced to pay fees to both sides, as if simultaneously "contributing" to Iran and the U.S., and even having to "shout Allāhu Akbar and Hallelujah" to express loyalty. It is also possible that later a plethora of exemptions would be granted to different countries, making this blockade a "leaky Swiss cheese."

But the core logic remains unchanged: if holding dollars no longer guarantees your assets won't be devastated by "pirate-like behavior," then why hold dollars?

Scenario Three: Empire Strikes Back

In this scenario, the U.S. Air Force and Navy fulfill their "proper duties": through a punitive long-range strike operation, they destroy the capabilities of Iran's Islamic Revolutionary Guard Corps (IRGC) to interfere with shipping in the Strait of Hormuz.

The Strait reopens, and all vessels can pass safely without paying extra fees. As the "imperial order" is re-established, countries will no longer need to use currencies other than the dollar in the short term, nor will they need to scramble to purchase commodities at high prices in the spot market.

But the problem is: to end Iran's control over the Strait could likely mean the complete destruction of Iran itself. In Donald J. Trump’s words, "sending them back to the Stone Age."

Many Americans who have grown up with the narrative, "Iran is the world's most evil country," will cheer for this tough stance. However, if Iran is destroyed in this way, it could very well carry out its threat in its "last gasp"—dragging the entire Gulf region's energy and commodity production into the abyss.

At that point, "spices will no longer flow" (i.e., a global supply chain disruption), and central banks worldwide will have no choice but to print money frantically amidst a comprehensive spike in commodity prices to keep the financial system running.

If you are in some "fragile countries," your local currency may experience hyperinflation against the dollar or the ruble. The U.S. and Russia will be the only major energy producers capable of adjusting supply to fill the gap left by a burning Middle East.

What may follow are: famine and widespread social unrest.

Therefore, even if your Bitcoin appears to be worth "infinitely many" of some worthless fiat currency on paper, if you cannot leave a high-risk area in time, your own survival will still face serious threats.

Scenario Chart

Before specifically analyzing Bitcoin's performance in different scenarios, let's quickly go through some "chart materials" to support the narrative above with more intuitive data.

Return to Normal

Given that I have discussed this scenario in detail in "This Is Fine," I will directly re-cite some charts and data provided at that time.

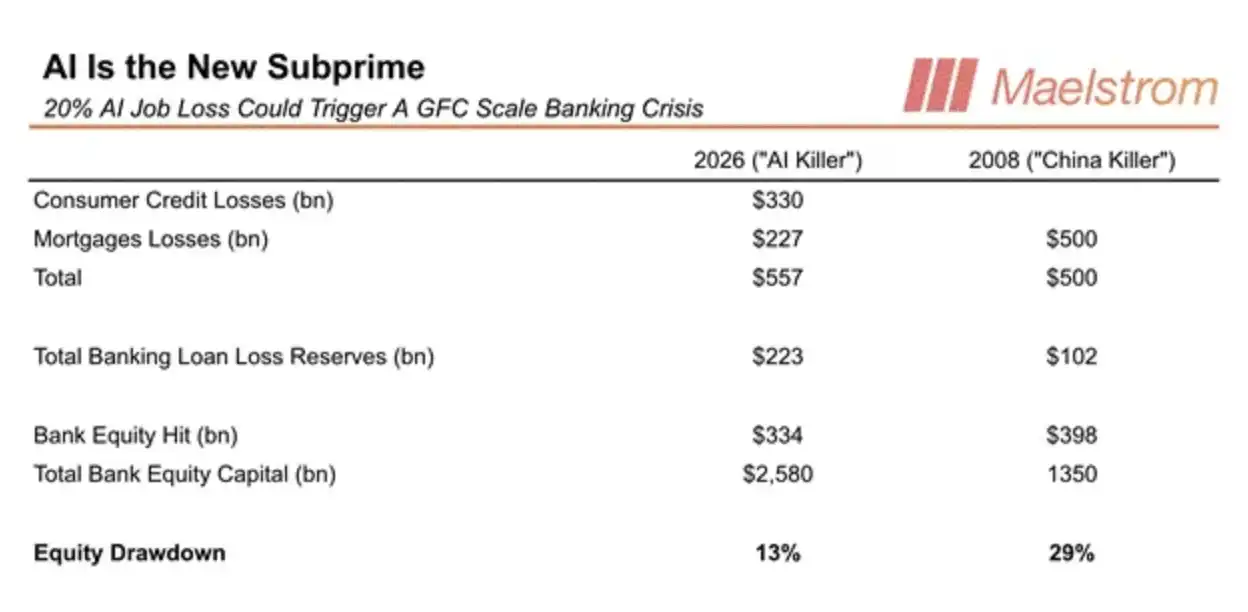

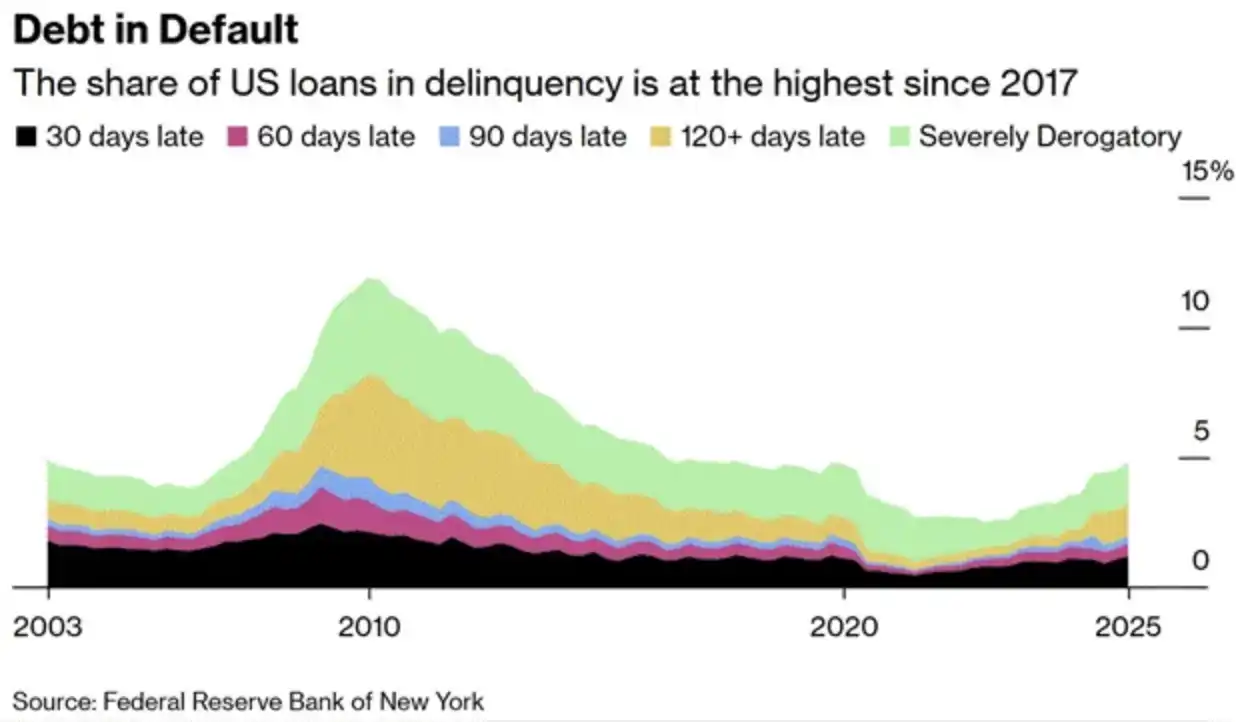

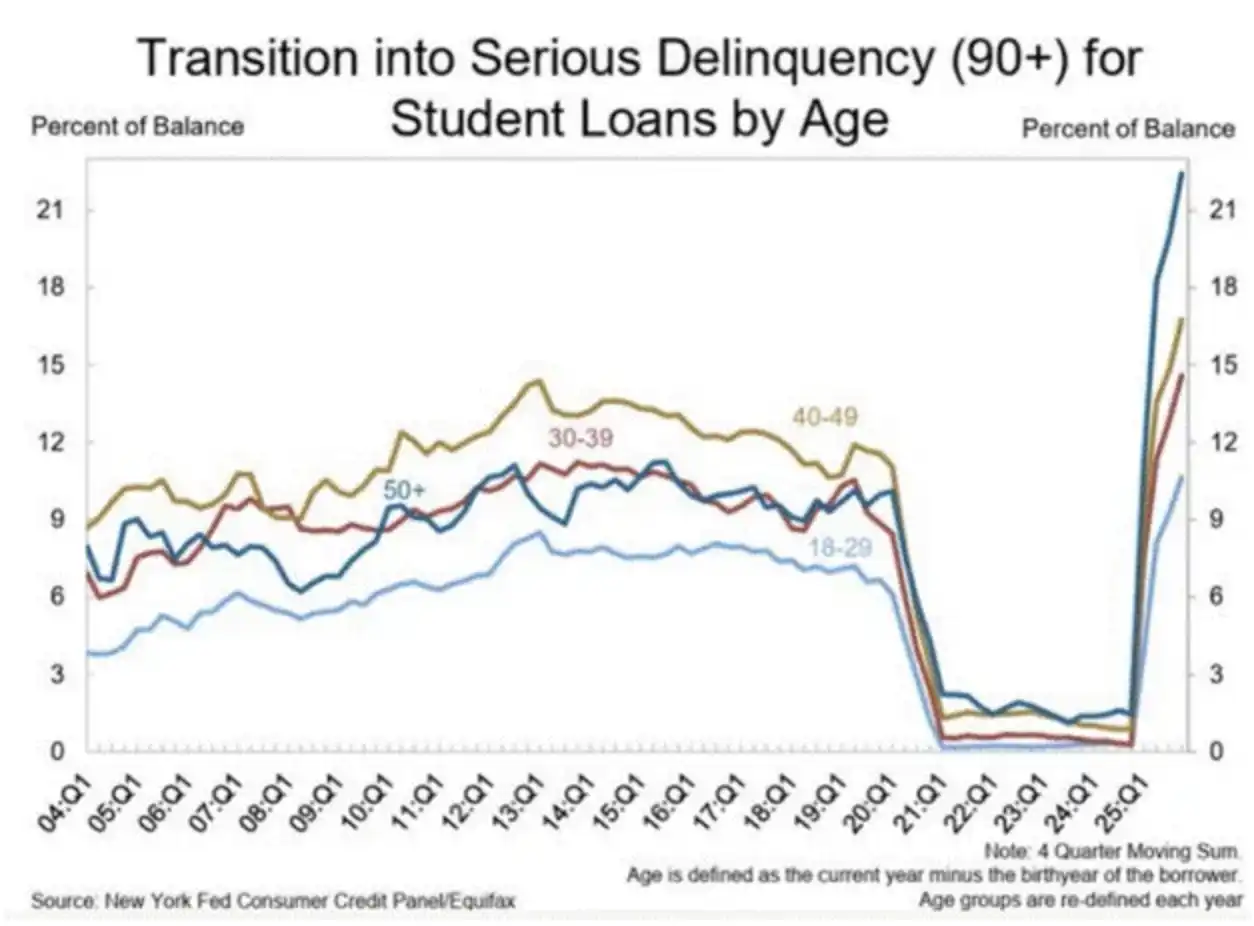

Overall, the severity of the deflationary collapse induced by agentic AI is no less than that of the 2008 U.S. subprime mortgage crisis (2008 Global Financial Crisis).

Currently, the default rate on consumer credit has started to rise, and the real large-scale wave of layoffs has not even officially begun.

Tehran Toll Booth

Essentially, if this scenario holds, it signifies the end of the "petrodollar system" and the rise of a new global reserve currency (or a basket of currencies).

Currently, the IRGC maintains a significant amount of flexibility regarding payment methods. But if its control over the Strait of Hormuz is truly consolidated, then, against the backdrop of continuous U.S. restrictions on its ability to use dollars, why would it still accept payment of tolls in dollars?

Ultimately, I believe it will no longer accept dollar settlements. The renminbi and gold are very likely to become the two core settlement assets in sovereign trade.

If a country must first exchange gold for renminbi, and then pay the toll with renminbi to complete commodity transport, what reason is there for it to continue holding dollars as reserves?

Given that most major economies have a trade deficit with China, the viable path to obtain renminbi is: sell dollar assets → buy gold → then exchange gold for renminbi.

In such a system, the future reserves that countries need to hold will be gold, rather than dollar assets like U.S. Treasuries or U.S. stocks.

To illustrate the expanding use of renminbi in trade settlements, I would like to quote some charts shared by Luke Gromen. These charts demonstrate the process by which a "quasi-renminbi-gold standard system" is quietly forming.

Step One: Sell Dollar Assets (such as U.S. Treasuries) and Buy Gold

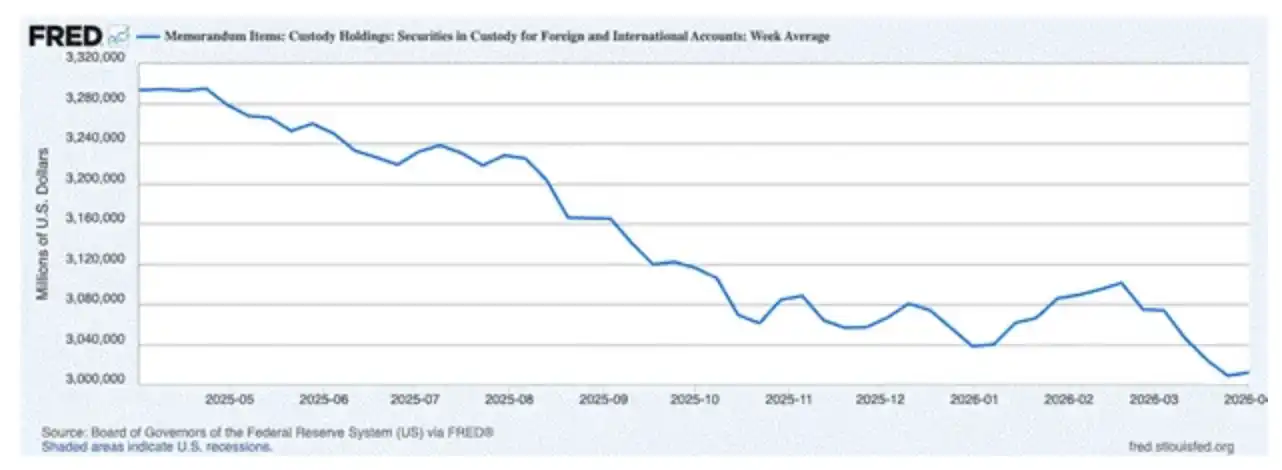

Since the war broke out, foreign holdings of securities under the custody of the Fed have decreased by $63 billion, on a net basis. I take this data as a "directional indicator" to assess the overall changes in foreign investor positions in U.S. Treasuries and other dollar assets (like stocks).

So, where did the money from those who sold dollar assets end up?

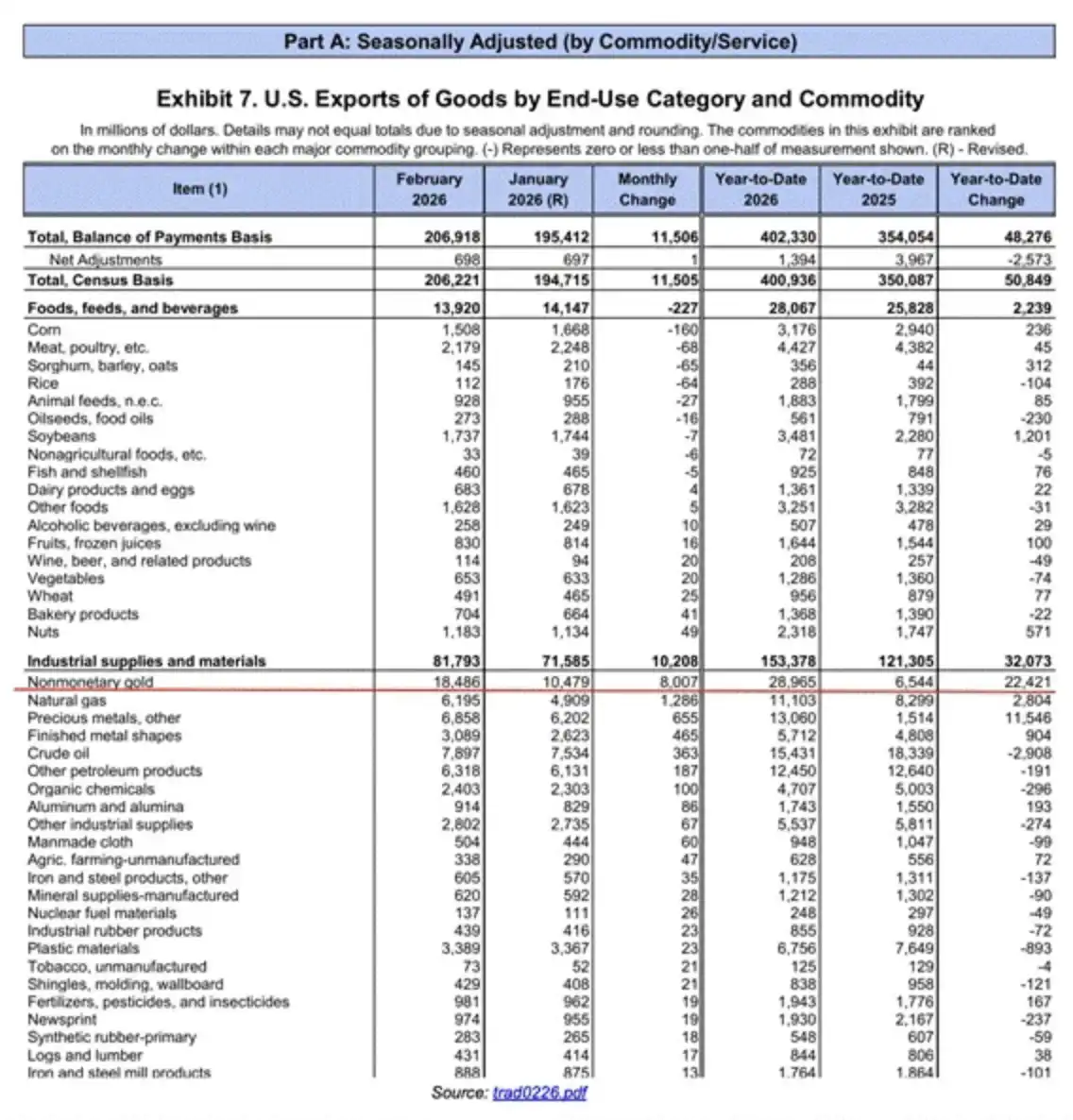

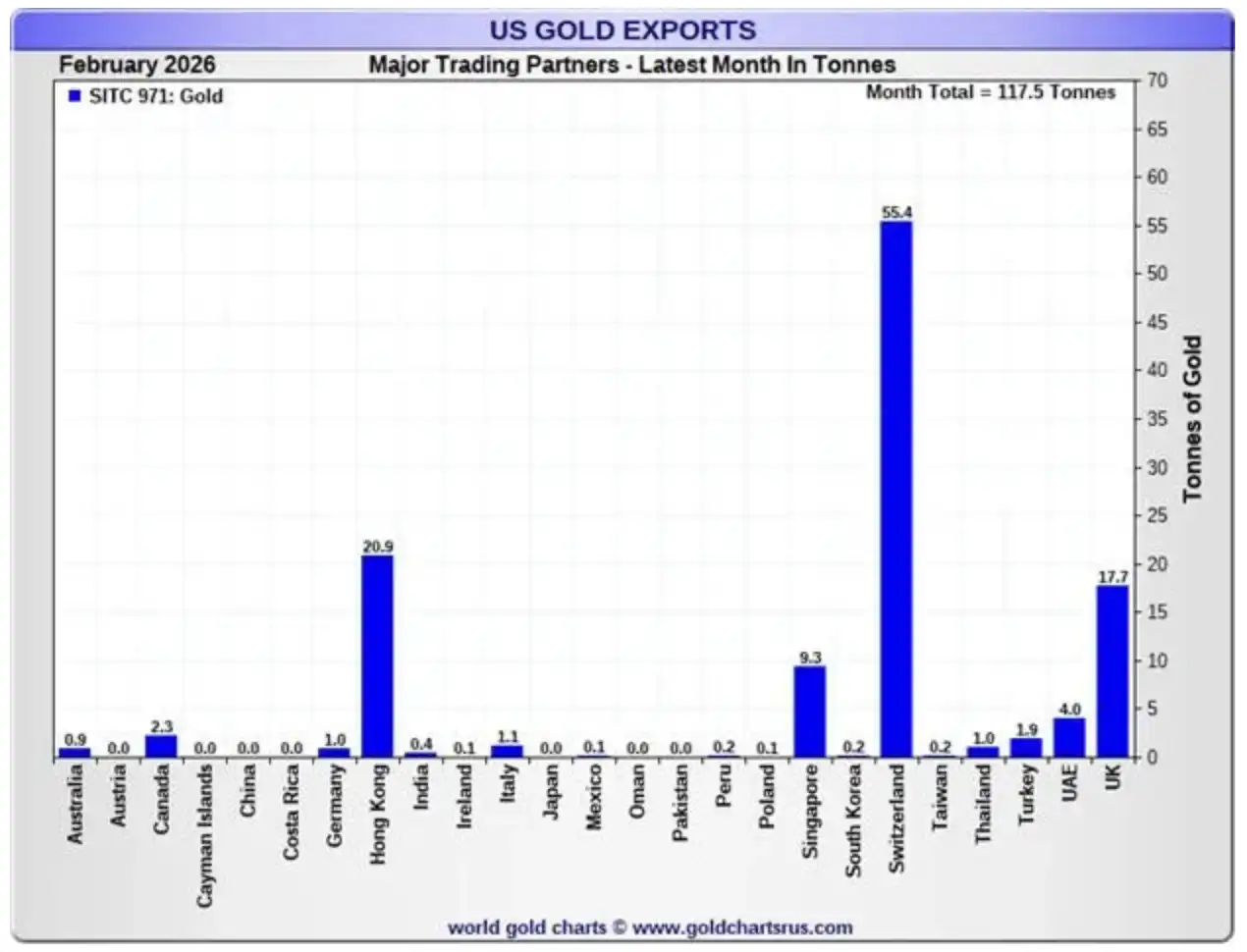

Non-monetary gold has become the biggest export product of the U.S. for four out of the past five months, with a year-on-year increase of 342%.

In other words, this money did not stay in the U.S., but was used to purchase gold and then exported from the U.S. The narrative of "re-shoring American manufacturing" seems quite ironic in reality—what is truly leaving America is a form of "barbaric heritage" (gold). For those supporters anticipating high-paying manufacturing jobs to return, this is undoubtedly an unmet expectation. Another presidential cycle has passed, and the working class still has not genuinely benefited.

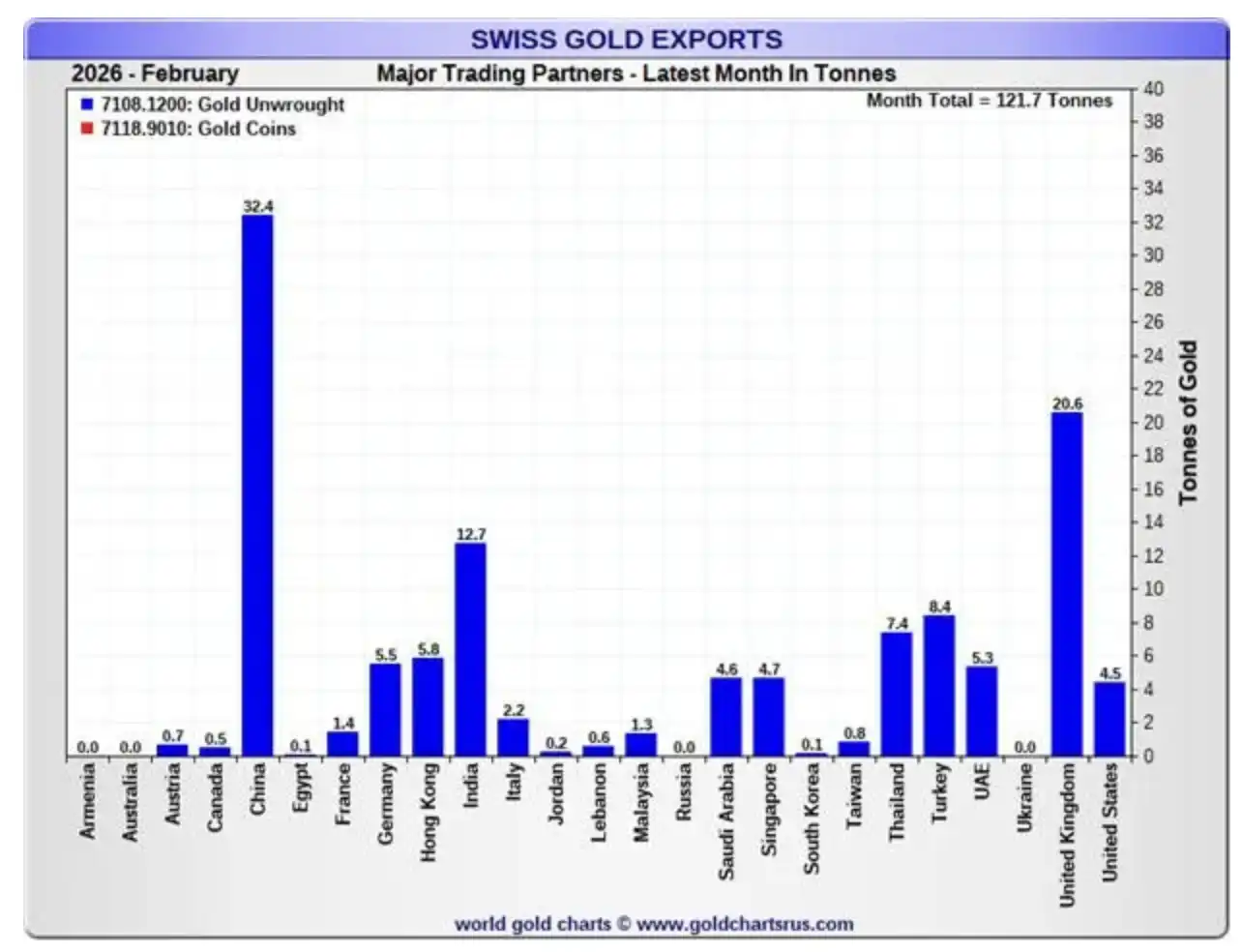

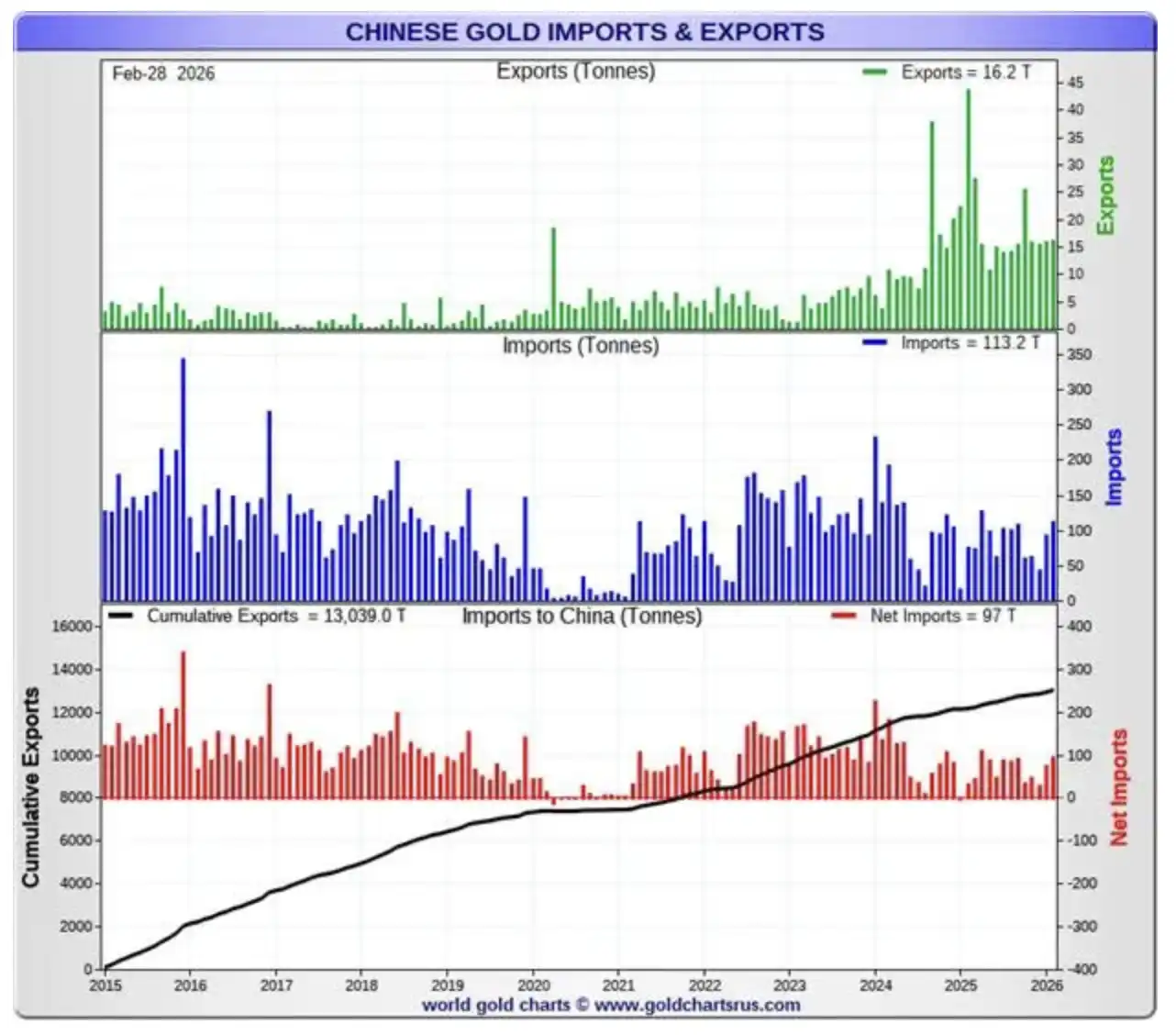

Step Two: Exchange Gold for Renminbi (Sell Gold for Yuan)

Swiss refineries receive gold from the U.S. and re-mint it into gold bars that meet Chinese delivery standards.

The key at this step is: Switzerland serves as the core hub for global gold refining, capable of processing gold bars of different specifications into high-purity standardized products that meet the needs of the Asian market (especially China). In other words, the gold flowing out of the U.S. will not directly enter China but will be converted through Switzerland as a "transit and standard conversion center."

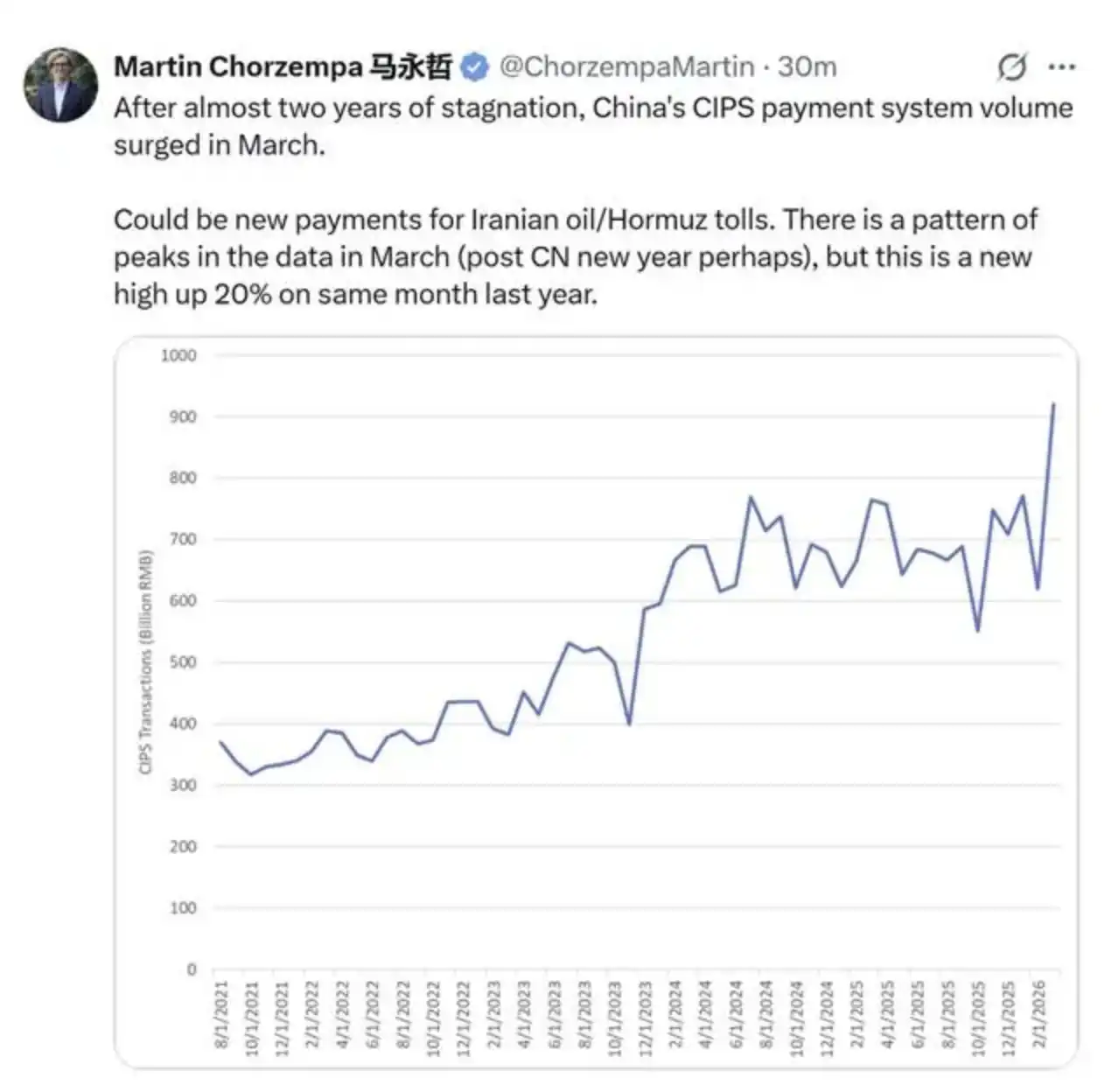

Step Three: Pay the "Tehran Toll"

The usage of the Cross-Border Interbank Payment System (CIPS) for renminbi is clearly increasing, and there has been a recent "anomalous acceleration."

"Buffalo Bill" Bassett was dead serious when he said that: "You either put dollars on your body, or you face another round of sanctions."

Due to the sanctions imposed by the U.S. nearly fifteen years ago, Iran cannot use the SWIFT payment messaging system. To deliver renminbi to the IRGC, it must rely on China's currency settlement system, China International Payment System. As you can see, since the war broke out, the transaction volume of this system has clearly increased.

This series of charts illustrates a chain of capital movement: dollar assets are sold, gold is purchased, and finally gold is exchanged for renminbi to pay Tehran or other suppliers. The key is not that dollars remain the dominant currency in trade today, but rather—that the market is forward-looking. Compared to the current fact that the scale of renminbi usage is still lower than that of the dollar, it is more important that its use in global trade is accelerating. For investors, avoiding dollar assets in advance before the market reaches a consensus is a way to protect their portfolio.

Historically, the pound was nominally still the global reserve currency before the 1944 Bretton Woods Agreement, but in reality, as the U.S. economy became the most productive economy in the world in the early 20th century, the dollar had long replaced the pound as the de facto reserve currency.

By 2026, the U.S. will generally have trade deficits with the world's most productive economies (China, Japan, South Korea, Germany, Taiwan, etc.), while most countries will also have trade deficits with China.

I want to emphasize this logic again: if you have to pay those "Stone Age" Middle Eastern forces with renminbi to get your goods, then what significance is there in keeping your assets in dollars?

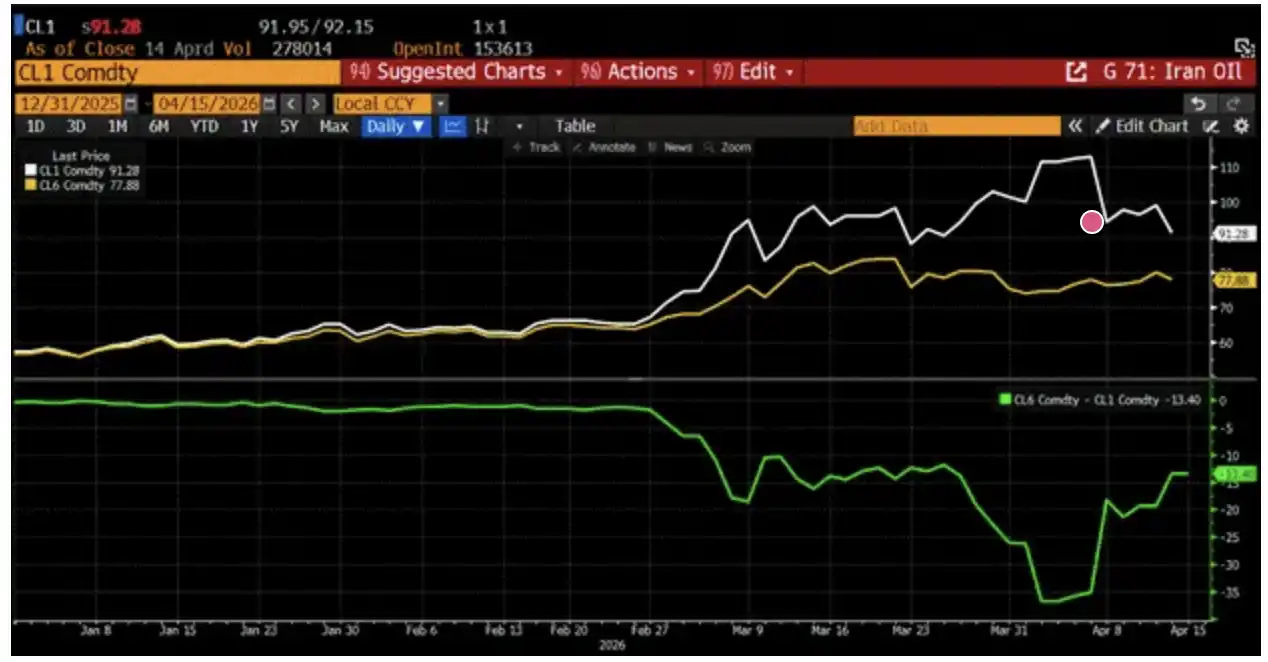

To determine whether the Strait is "open" or "blocked," look at the chart above, or create a similar one using any charting tool you prefer.

The upper chart shows a comparison of WTI crude oil futures prices for May 2026 (CL1, white line) and October 2026 (CL6, gold line). I chose WTI because this benchmark is closer to the gasoline prices faced by U.S. consumers. For Donald J. Trump, only when oil prices exert clear pressure on voters before the midterm elections in November does he have the motivation to significantly cool down the situation.

The lower chart depicts the price difference between these two contracts (longer months minus shorter months); the current curve is in "backwardation." Since the rise in long-term oil prices is less than that of the near-term, the market is essentially betting that the flow of oil through the Strait will significantly increase.

If this judgment holds, then as near-term prices fall, the price difference will expand. Conversely—if long-term prices rise and the price difference narrows—it would indicate severe shocks are facing the global economy.

So rather than focusing on the verbal duels between Trump and the IRGC, it's more prudent to keep an eye on this chart.

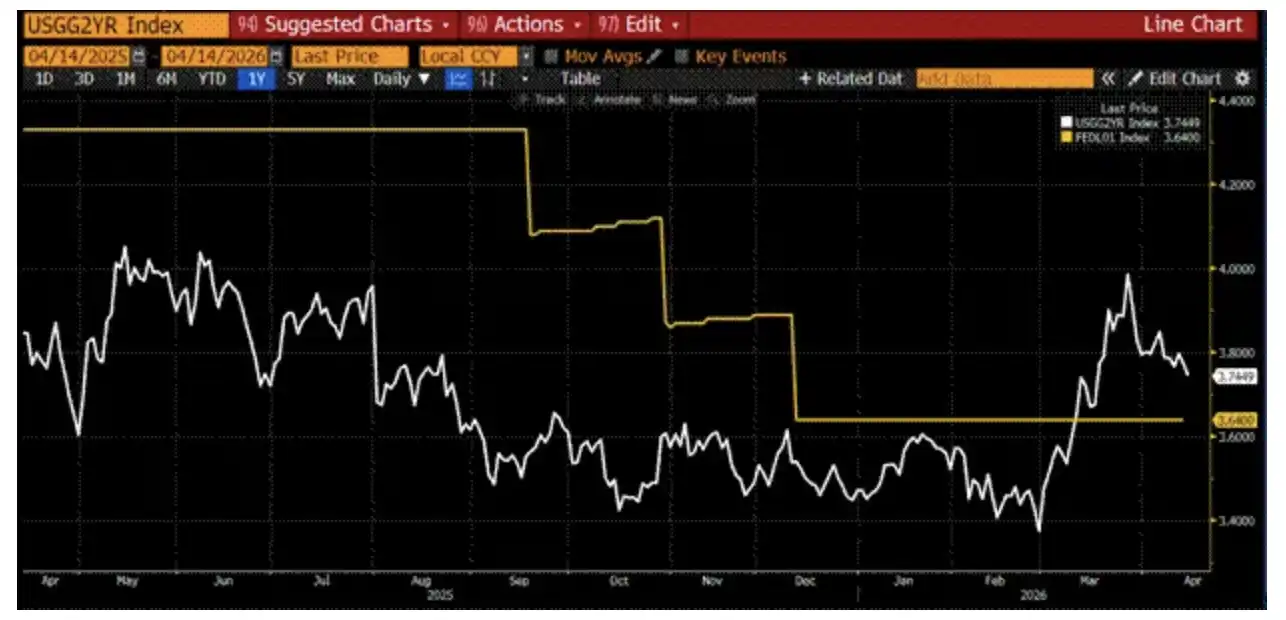

"Quantity" versus "Price" of Money

The yield on two-year U.S. Treasury bonds (white line) soared shortly after the war began, significantly above the effective federal funds rate (yellow line). This indicates that the market anticipated that the Fed would use interest rate hikes to offset rising energy inflation.

Now it’s time to pick a side: when pricing Bitcoin, do you think the "quantity of money" or the "price of money" is more important? I believe that what determines Bitcoin's price is the quantity of money, not the price of money. Bitcoin does not have cash flows, so the discount rate derived from central bank policy interest rates is not applicable to the valuation of this "internet magic currency." However, since Bitcoin's supply is fixed, its value denominated in fiat currency depends on the total fiat currency supply.

It is important to form this judgment because we may be entering a new macro state: major central banks, including the Fed, may be raising interest rates while simultaneously printing money (whether through direct money printing or indirectly expanding credit through the commercial banking system). As the war drives up food and energy prices, capable governments often subsidize key input costs in the economy, or it may lead to social unrest and even famine. To prevent inflation from spilling over into every good and service, central banks must also raise interest rates to suppress demand, especially to cool down those economic activities sensitive to credit. Any entity that relies on borrowing for consumption will reduce expenditure as credit costs rise.

If central banks only manage this much, then my judgment on Bitcoin is actually quite simple: in an environment where people generally cut spending except on food and energy, Bitcoin's price will drop. But the reality is that whether allies or adversaries of the "American order," countries must increase defense spending and stockpile key commodities. Would you want your country to be like Australia, which relies almost 100% on China for refined energy imports? Once the war started, China suspended exports, and Australia's stock would last less than a month. They had to seek help from Singapore and buy aviation fuel at exorbitant prices, or the entire country would come to a standstill.

To avoid becoming a "trash country," nations need to manufacture weapons (especially nuclear weapons) and hoard commodities, which will lead to a significant increase in government borrowing. If domestic private investors cannot or will not buy these "bad" government bonds, then the central bank or commercial banking system will print money to take over, thereby expanding the fiat currency supply.

This combination of "rising rates (increased price of money) + money supply expansion (increased quantity of money)" will lead to differentiation among different risk assets: assets priced based on discounted cash flows will decline, while assets with fixed or near-fixed supply (like Bitcoin and gold) will rise, as the banking system needs to expand credit to support government war and resource hoarding expenditures.

Before continuing to read my judgments on Bitcoin's movement in different scenarios, please keep this in mind: you must judge which is more important between the "quantity of money" and the "price of money," otherwise you will be unable to understand the seemingly contradictory price movements among different risk assets.

Return to Normal

Once the situation returns to pre-war conditions, Bitcoin may experience some rebound. However, the deflation shock caused by AI agents continues to accumulate. Until the Fed provides sufficient liquidity to the banking system to fill the balance sheet gaps caused by consumer credit defaults, Bitcoin is unlikely to see significant increases. This does not mean that it won't spike to $80,000 to $90,000 in the short term, but for me, without a clear signal of liquidity being released by the Fed, putting new fiat currency into the market is too risky. Given that I am already in a pure long position, seeing my net worth increase is certainly pleasant, but the current risk-reward ratio does not allow me to push my position to the extreme.

I cannot determine how long it will take for the banking system to really collapse. But I see similar news almost every week: certain companies are laying off a large number of knowledge workers due to AI improving efficiency, and the default rate on consumer credit continues to rise.

For example, I recently spoke with an entrepreneur running a crypto gaming company, who is an old player in the industry. We discussed the impact of AI on business. He, being a computer engineer, attempted to develop a project using the latest Claude model during Christmas 2025 and was quickly shocked by its efficiency—capable of producing deployable code in a very short time. Months later, he gathered the team for offline discussions, asking them to build a 24/7 AI programming workflow, even automating code reviews. The result was that every morning there was tested code ready to use. One employee, with the help of AI, completed a six-month development plan in four days.

After this, he decided to immediately adjust the company's processes, with about 50% of the employees being laid off in the coming weeks.

In the AI agent era, ordinary engineers will become redundant, while the productivity of top engineers will increase by 10 to 100 times. As models continually enhance their capabilities across various sub-sectors, many mid-level knowledge workers will face unemployment risks.

The issue is that even though unemployment insurance exists, the highest annual subsidy in various U.S. states is about $28,000, while, according to the U.S. Bureau of Labor Statistics (BLS) and the St. Louis Fed, the median annual salary for knowledge workers is about $85,000 to $90,000. The gap is enormous, and the result can only be a large number of individuals starting to default on bank consumer credit.

This is a fatal blow to the current "fictional" fiat partial reserve banking system.

In summary, after the ceasefire, the U.S. SaaS software stocks re-enter a unilateral downward trend, while Bitcoin remains stable and even rebounds. This temporary decoupling of correlations is encouraging, but in my opinion, it is still premature to assert that Bitcoin has "seen through" the deflation affecting knowledge workers triggered by AI and is poised for a massive increase.

Tehran Toll Booth

As countries sell dollar assets to acquire renminbi and pay the "toll," the prices of U.S. Treasuries and stocks will face downward pressure. This process might be gradual, as there are still other payment methods outside of renminbi. But considering the high-leverage structure embedded in the entire system, even a slight shock could trigger a chain reaction—selling leads to more selling, volatility rises, and market liquidity freezes. At this point, monetary authorities will have to step in and stabilize the situation through "money printing."

A key indicator to watch is the MOVE Index (U.S. Bond Market Volatility Index). Once this index rises above 130, it often indicates that some form of monetary easing is imminent.

As volatility rises, the prices of major U.S. tech stocks drop, and Bitcoin is unlikely to see a strong rise. When investors de-risk due to increasing market volatility and falling asset prices, they often sell Bitcoin to meet margin requirements. Only when the situation deteriorates to a certain extent and the market widely expects a bailout can Bitcoin truly rise.

Wait until Bassett, or any Fed chair at that time, presses the "money printer" (Brrrr button) before talking. Before that, attempting to position early does not offer a favorable risk-reward ratio. I hope Bitcoin can hold the $60,000 level when systemic financial shocks occur in traditional markets. If it can test and stabilize this level a second time, I would tend to gradually increase my risk exposure.

Star-Spangled Blockade & Empire Strikes Back

If long-term crude oil futures prices rise sharply and catch up to spot or near-term prices, the global economy will take a hit. At some point, demand contraction will strike U.S. Treasuries and the stock market. Similar to the previous scenario, the initial reaction will still be a drop in Bitcoin. And when the highly leveraged Western financial system begins to collapse, the money printing machine will start again.

Should the final situation evolve to: unblock the Strait through punitive bombings against Iran, while Iran retaliates by destroying the entire Persian Gulf energy production capacity, this could even lead to the national-level collapse of Iran. In such a scenario, Bitcoin driven by "money printing" could see a temporary increase, as this would significantly raise the risk of a Third World War.

Portfolio Construction

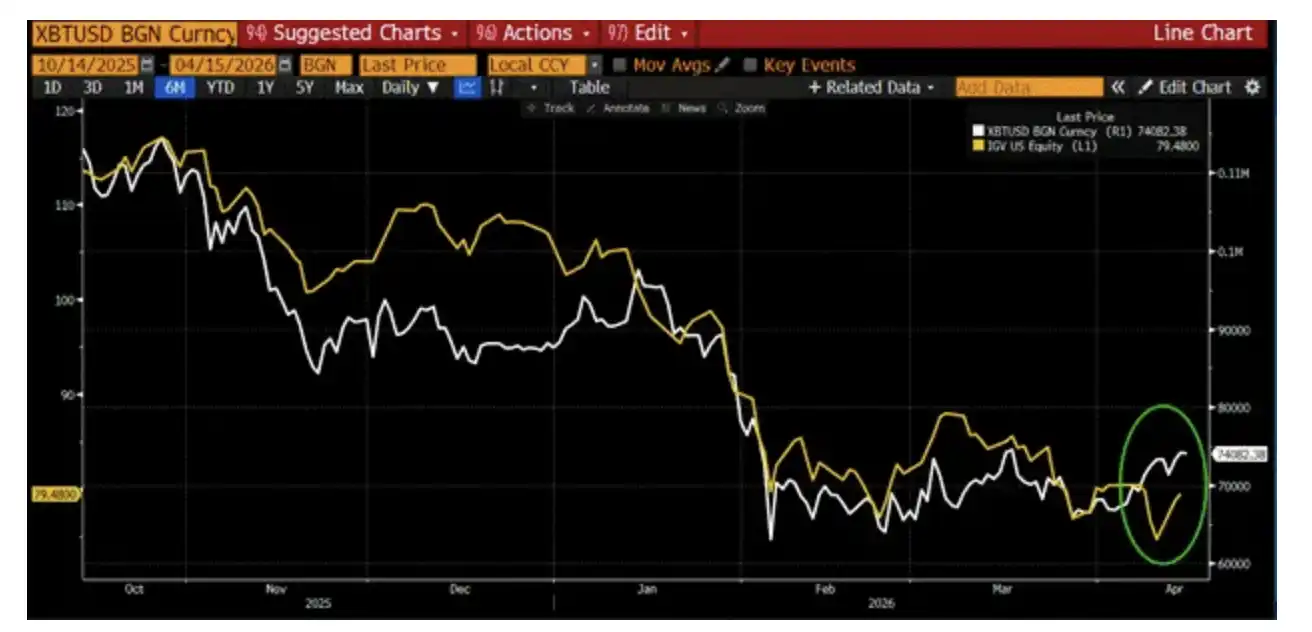

As a non-leveraged, pure long investor, Maelstrom can rely on time and compounding to naturally take effect. In the past few days, Bitcoin’s slight outperformance relative to IGV (U.S. Software SaaS ETF) is a positive signal, prompting me to reassess the previously formed bearish judgment based on "AI-induced knowledge worker deflation."

At this current stage, the only asset I am willing to increase risk exposure for is gold and $HYPE (the governance token for Hyperliquid). HIP-4 will launch in the coming weeks, and I expect it to capture a significant share of the market from Polymarket and Kalshi in the prediction market track.

Aside from this, all I can do daily is pray that Satoshi can "influence" the thinking of global political elites, urging them to choose to take drugs (acid) instead of dropping bombs.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。