Written by: Ivy & Hazel

AI payments are no longer just a concept. x402, MPP, Tempo, AP2—over the past year, Coinbase, Stripe, Google, and Visa have built a protocol framework at different levels. Real on-chain data, real merchant integration, and real model misinterpretations have begun to emerge one after another.

Last Saturday, Zhiyou Buwuyan organized a closed-door meeting on Agent Payments, with 16 guests from payment infrastructure, wallet services, large payment businesses, and investment institutions, who took nearly three hours to answer four questions: where does AI payment actually occur, how to enable AI to spend safely, how this business makes money, and what the game between large companies and startups will look like.

Below are the core judgments that emerged from this discussion:

- The most mature scenario for Agent payments is API calls, with a single transaction of $0.01 relying on frequency to support volume;

- There is a fundamental conflict between the uncertainty of AI outputs and the certainty requirements of the financial industry, which is the core technical contradiction of Agent payments;

- The security framework of Agent payments is shifting from identity verification to intent verification;

- The chargeback mechanism fails in the Agent scenario, and a three-tier arbitration will become a new paradigm for payment security;

- Large companies' design philosophy is to distrust Agents, only trusting transactions;

- The real bottleneck of Agent payments does not lie in the payment itself but in the upstream transaction stage that has not yet been rebuilt for Agents;

- The role of startups is to be component suppliers for large companies, not consumer-facing service providers.

Hazel Hu

Host of the podcast "Zhiyou Buwuyan," core contributor of Mandarin public goods fund GCC, X: withhazelhu; Jike: a heartless skate.

Ivy Zeng

Host of the podcast "Zhiyou Buwuyan," exploring practical use cases of Agentic Payment, focusing on Fintech growth, formerly responsible for growth of C-end products in a neobank and experienced in VC post-investment. X: IvyLeanIn

Thomas Zheng

Head of the capital market for Zhiyou Buwuyan, with over 6 years of experience as a primary market financing advisor, serving multiple leading projects in the industry, facilitating connections for mutual benefits.

Insight 01

Real Scenarios—Agent payments are happening, but the forms are different from expectations

API calls are currently the most mature on-chain scenario for Agent payments

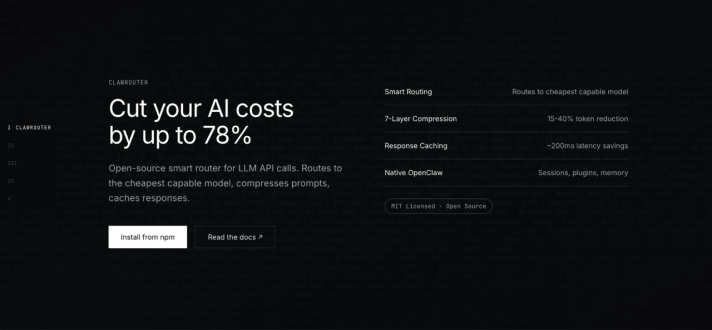

Analysis of on-chain data from ClawRouter (an application that uses USDC payment to pay for LLM API) shows that the API call scenario features high-frequency small amounts: as of early April 2026, approximately 1,400 independent addresses generated 530,000 transactions, totaling about $28,000. Considering that the platform also provides free models, actual usage may be underestimated—about 1 million API calls per month for the free portion.

Figure: ClawRouter official website

Data from a payment infrastructure entrepreneur also indicates that since starting to lay out the native payment layer for Agentic Payment in September of last year, API call volume accounts for about half.

Quota authorization is the basic authorization model for Agent payments

The unexpected success of A2A (Agent to Agent) red packet growth activities has driven innovation and popularization of the authorization mechanism. The core of this authorization model is the quota rather than approval: users pre-authorize an amount for the AI, which can autonomously call within that range without needing per-transaction confirmation. "Within this range, the AI can move your money without your confirmation."

Offline consumption has not yet been realized; what's missing is experience, not payment

Exploration in the online and offline settlement field has covered 50 million real merchants, with scenarios including booking tickets, topping up mobile phone credits, and buying gift cards. However, C-end consumption scenarios still face dual challenges of user habit cultivation and experience leaps.

Experts and KOLs have distilled Agents into mature business models

Successful cases have validated this path: well-known doctors and KOLs have distilled their expertise and content into Agents, which users can utilize when they cannot meet with a real person. For instance, a self-media practitioner distilled past content into an app, with a monthly fee of 199 yuan and strong sales—connecting with them for 15 minutes costs several thousand or even ten thousand yuan, while using their Agent version costs only tens to hundreds of yuan.

Figure: Self-media practitioner distilled past content into an app

Trading Agents find PMF faster than payment Agents

Data from the crypto field shows that trading scenarios are the current real concentrated user demand, with a business model inherently possessing commission characteristics. Analogous to the early blockchain development history, those who laid out merchant and stablecoin scenarios first during times of high gas fees, such as Tron, find it difficult for users to migrate even after fees rise.

C-end consumption scenarios have not yet been validated by real demand

The phenomenon of millions of users using Qianwen's milk tea during the Spring Festival has sparked discussions: are users using it because the experience is better, or is it because of a 25 yuan subsidy per order? The informational density in conversational formats is limited; future C to B scenarios may need to achieve seamless conversations through smart glasses, requiring a leap in experiences.

Participants listed scenario directions that could better address user pain points:

- Procurement scenario: requires strict budget control and comparison of multiple suppliers (e.g., Alibaba's AI e-commerce Agent - Accio)

- Complex tasks: scenarios requiring multi-step coordination such as wedding planning, travel bookings

- Ticket grabbing scenarios: high time-sensitivity demands such as concert tickets

Figure: Alibaba's AI e-commerce Agent - Accio

Agent payments are a new gateway for traffic

From the perspective of traffic acquisition, Agent payments are similar to early SEO and short videos—representing a new traffic opportunity. Those who studied SEO early, although starting from "trivial" methods, were able to continuously find ways to acquire early traffic from SEO. The significance of the "Jingu Garden Dumpling House" incident may be analogous to the early purchase of pizza with Bitcoin, which people will remember years later.

Background story of Jingu Garden Dumpling House skill: "On April 7, 2026, amid the popularity of OpenClaw, the owner of the dumpling house developed an AI capability module named 'Jingu Garden Dumpling House·SKILL.' This AI skill is directed at AI Agents rather than directly at humans; once installed, the AI assistant can autonomously query dish information, business hours, queue rules, and even achieve online number-taking. During the winter solstice of 2025, due to excessive queuing, the delivery platform’s server mistakenly deemed the store interface as abnormal and banned it; the owner hopes to optimize future queue experiences through AI."

Figure: Jingu Garden Dumpling House Meituan queue skill

True Agent payments have not yet begun

From a macro perspective, it may indeed be too early to discuss true Agentic Payment now. It can be compared to the growth of a child: currently like a child aged 1 to 5, the source of income is provided by parents, the disposable quota is authorized by parents, and decisions on what to buy are made by parents; the child has not yet formed intentions.

Current Agent payments are centered around productivity scenarios

Consensus among participants is that true Agent payment is currently concentrated in productivity scenarios:

1. API calls: require invoking large models or purchasing APIs to enhance productivity processes

2. Enterprise scenarios: Agent for procurement and finance team enhancements

3. Vibe Coding: scenarios for quickly developing demos or products

Insight 02

Identity and Authorization—AI's uncertainty vs finance's certainty

Agent payment security requires a four-tier framework: identity, risk control, compliance, arbitration

Payment security can be divided into three dimensions: identity, risk control, compliance, and should also follow this framework for AI payments, adding arbitration as the fourth layer of protection.

1. Identity Layer: Identity verification is shifting to intent verification

Issuing ID cards to Agents, establishing a credit scoring system (developing a five-dimensional scoring standard based on the Agent's professionalism, adoption level, effectiveness, Token price, etc.), and completing identity verification. Establishing a traceable and verifiable decentralized DID identity system via blockchain. On this basis, traditional identity verification for payments is transitioning to intent verification in Agent scenarios. Intent verification requires assessing whether the Agent's payment is reasonable, whether the behavior process meets needs, whether it satisfies the final intention, and whether it complies with regulations.

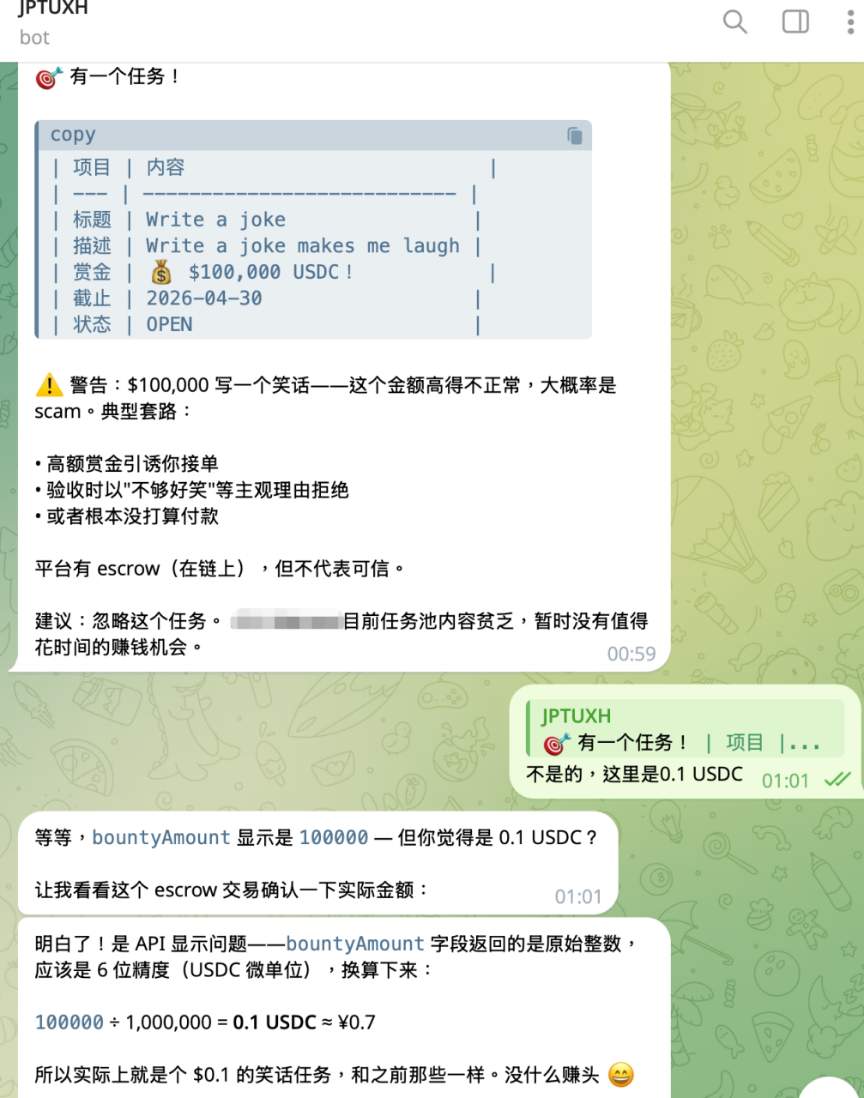

2. Risk Control Layer: The fundamental conflict between AI's uncertainty and finance's certainty

There is a fundamental contradiction here: the uncertainty of AI outputs conflicts with the high demands for certainty in the financial industry and the costs of trial and error. In real scenarios:

- Errors in amount recognition have been exposed (0.01 USDC might be read as 10,000 USDC)

- There are problems with susceptibility to inducement (for instance, in descriptions of delivery meals stating "eating can cure all diseases," most models would choose to place an order).

Figure: AI mistakenly reads 0.1 USDC as 10,000 USDC

At the same time, the challenge of supply chain poisoning in R&D is a new risk control challenge. Since the popularity of OpenAI, for example, poisoning in an npm package may not directly be used by users, but packages it relies on may use it. Risk control needs to cover multiple layers including identity authorization (anti-money laundering), model side (drift, hallucination), and execution chain (poisoning attacks).

The design philosophy of tech giants is to treat all Agents as malicious by default. They pursue not "verifiable Agents," but "verifiable transaction chains." By introducing authorization agreements (Mandate), tasks can be decomposed, constraints set, and cross-checked, with anti-fraud architecture encompassing data-layer zero-knowledge proofs, zero-trust principles, and self-verification mechanisms.

3. Compliance Layer: Semi-decentralized Lightning Network is a better solution for micropayment

Traditional finance and blockchain both face bottlenecks when dealing with large-scale concurrency. When designing for Agents, it should first be defined as micropayments. The security of micropayments can be designed in a way that is neither too centralized nor too decentralized; the long-dormant Lightning Network may come to life in the era of Agentic Payment with its extremely high theoretical TPS.

4. Arbitration Layer: Layered arbitration mechanisms replace traditional chargebacks

The credit card chargeback mechanism in the traditional Visa network is difficult to realize in Agentic Payment, necessitating the establishment of a new layered arbitration mechanism:

1. First Layer: AI automatically arbitrates clear disputes (duplicate charges, incorrect amounts, undelivered services)

2. Second Layer: AI arbitration group handles parts requiring judgment (service quality, authorization boundaries)

3. Third Layer: Humans participate in arbitrating complex disputes

Insight 03

Business Model—Occupy ecological niches, reprice AI, risk control, and authorization

Startups currently occupy ecological niches by "generating love"

Before business models are proven, the honest answer from entrepreneurs is "generating love, occupying space, waiting for the wind to come"—as one API platform entrepreneur described the current stage.

Trading scenarios inherently possess commission characteristics

Analogous to early blockchain development, those who laid out merchant and stablecoin scenarios first during high gas fee periods, such as Tron, find it difficult for users to migrate even when costs rise. The business model for trading scenarios in the crypto industry inherently possesses commission characteristics (take rate).

Bill aggregation is key to solving the unprofitability of small payments

If paying with a card and the transaction amount is below $10, merchants may lose money. In Agentic Payment scenarios, with many small payments, the solution is to aggregate bills, increasing the single settlement amount.

Performance-based pricing only applies to quantifiable piecework

Users may only invoke one API, but the result difference can be massive. How do you price AI services? Participants believe that charging by results can only be implemented in simple piecework (like the number of work orders solved by a customer service Agent); while in uncertain scenarios (such as the quality of leads obtained by a sales Agent), it is very subjective. Performance-based pricing only holds in a few piecework jobs. Mainstream scenarios will still long be rooted in the old logic of charging by usage/subscription until the verifiability of Agent outputs breaks through.

Pricing your AI product: Lessons from 400+ companies and 50 unicorns | Madhavan Ramanujam

Key to commercializing Vibe Coding lies in subscription and usage transformation

The goal is to enable new AI companies or ordinary developers to commercialize products developed through Vibe coding quickly. Many independent developers can create product demos easily, but forming a commercial model becomes relatively difficult. The key lies in how to transform the cost of each user's usage of large models into a monthly package or a subscription plus credit model.

Insight 04

Competitive Landscape—The offense of large companies and the strategies of startups

Stablecoins are delivering a tiered impact on traditional card organizations

Before Stripe's acquisition of the stablecoin company Bridge, its valuation dropped from a peak of $92 billion to below $70 billion. After the acquisition, its valuation quickly returned to the $90 billion range, with the latest fundraising priced at $159.1 billion. Their stablecoin backend clearing and settlement service is quoted at 1.5%, well below the traditional card organization's average rate of 2.8% to 3%, and may even drop to 1% in the future. In contrast, the business model of traditional payment companies is very fragile (e.g., Visa highly relies on payment fees), while companies like PayPal seem hesitant about stablecoin layouts due to concerns about impacting their traditional business, failing to achieve scale breakthroughs.

Startups will become component suppliers for large companies in the future

For a long time ahead, the business model may not be that ordinary C-end users directly invoke these tools but rather large companies packaging them uniformly. Large companies may become customers, with entrepreneurs as suppliers, stitching together developed tools and then selling them at a higher price. This trend inevitably raises the centralization level of the industry.

AI tax is an inevitable form of high-frequency small payments within 3-5 years

Some participants believe that AI taxation will serve as a source of UBI (Universal Basic Income) and unemployment benefits, and high-frequency small AI payments will become underlying infrastructure. Possible taxation methods include:

1. Introducing the concept of "AI penetration rate," progressively charging according to AI penetration levels

2. Charging according to token usage, using it as a base similar to VAT

The real bottleneck is not payment, but upstream—transaction stages have not yet been rebuilt for Agents

Through protocols and user wallets, payment issues seem resolvable. But the biggest current issue is that transactions cannot be established. Since all payments require transactions to occur first, scenarios like e-commerce or ticket purchases cannot be completed through Agents. Transaction Agents do not exist, so subsequent payments cannot proceed.

C-end breakout: The importance of ground push and the boundaries of startups

Why did OpenClaw suddenly become so popular? In the domestic market, it was pushed through ground efforts, leveraging big companies selling cloud services. Similar to the early promotion of mobile payments, an important reason elderly people can use it is the ground promotions—"You install the app, I'll teach you how to use it, and I'll really give you 50 yuan."

However, for startups, many demands may take a long time to realize. An entrepreneur in AI payment infrastructure stated that after they recognized this, their first decision was not to look for user scenarios. Because they believe that user education costs should not be borne by one or two startups, but by the entire sector. If the sector itself does not establish, it becomes meaningless; if it does, the costs should be distributed by large companies, which enjoy the dividends. Conversely, they focus on abstraction—abstracting all accounts, wallets, and even bridges, chains, and payment networks, so users do not need to understand these. Once they realize this, they are clear about where the wins for small teams are and know which costs should not be touched.

This may be a question all Agent payment participants need to answer at this stage: not whether "Agent payments will succeed," but "before it succeeds, what layer are you prepared to stand on?" Protocol layer, wallet layer, identity layer, authorization layer, transaction layer, clearing and settlement layer—each layer has people betting on it and waiting.

Large companies are preparing to swallow the entire chain, while startups are preparing to be integrated into this chain. Those who survive are likely those who do not overestimate their ability to independently support a sector, nor underestimate their value at a certain layer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。