Original Author: Joey Shin

Original Source: IOSG Ventures

The crypto industry claims it lacks users every day, but the data does not support this. The number of active users in consumer-level crypto has already reached tens of millions, just not in the view of Silicon Valley and New York. These users are in Manila, Lagos, Buenos Aires, and Hanoi, using Coins.ph (18 million users), MiniPay (4.2 million weekly active), Lemon Cash (the top finance app in Argentina) every day, yet the English media has hardly reported on them. In contrast, the protocols discussed daily by Western VCs have daily activity that doesn't even reach the volume of Tron’s shadow settlement network in one hour.

Seven core conclusions: The user problem in crypto is fundamentally a geographic problem; Tron is the most important consumer-grade public chain, but no one in NYC or SF talks about it; on-chain e-commerce hardly exists; the largest prediction market is centralized; revenue and user numbers often move in opposite directions; the perpetual DEX battle has already ended; there are indeed profitable consumer-grade crypto companies—just not those resembling DeFi.

Payments and New Banking: Users Have Long Existed, Just Not in VCs' Sight

Common understanding: Crypto needs to enter the mainstream and bring the next billion users, and wallet UX is the bottleneck.

Data shows: The next billion users are already present, and the largest bottleneck is not customer acquisition but monetization.

First, let's look at the existing scale. Telegram Wallet claims to have 150 million registered users (unverified—low confidence), but let's set that aside. Just looking at verified data, the user base is already astonishing: Coins.ph has 18 million confirmed users in the Philippines, mainly operating on Tron’s USDT track; MiniPay, as Opera's mobile stablecoin wallet on Celo, had 14 million registered users by March 2026, with 4.23 million weekly active USDT users and a monthly transaction volume of $153 million, with on-chain activity up 506% year-on-year (high confidence—from Tether/Opera/Celo joint disclosure). Chipper Cash covers 7 million users across nine African countries and recently achieved positive cash flow. Lemon Cash has 5.4 million downloads, ranking first in financial apps in both Argentina and Peru, and its MAU has quadrupled since 2021. Paga processes an annual transaction volume of 17 trillion Naira in Nigeria, but the crypto-related percentage is unclear (medium confidence).

The only payment company that has simultaneously achieved scale and revenue is RedotPay: 6 million users, annualized revenue of $158 million, annualized transaction volume of $10 billion, and its valuation has increased 16 times since seed round (high confidence—The Block, CoinDesk, company disclosure). RedotPay's model is that of a crypto-to-fiat card processor targeting the Asia-Pacific region, taking a commission per transaction with zero chargeback risk—essentially a crypto-native Visa issuing and acquiring entity. It is currently the clearest case proving that consumer-grade crypto can generate real, recurring, non-incentivized revenue at scale.

Another highlight on the revenue front is Exodus, which disclosed in its SEC 8-K filings an income of $121.6 million in 2025 (high confidence), being one of the few publicly listed and audited consumer-grade crypto companies in the US. Its revenue comes from transaction and staking fees on 1.5 million MAUs, with shares listed on the New York Stock Exchange under the EXOD ticker.

Ether.fi's Cash product is the most noteworthy DeFi-native entrant: it became profitable in its first year, with over 70,000 cards issued, and Cash currently contributes about 50% of total revenue, with monthly revenue of $2.8 million (high confidence—TokenTerminal verified daily). It proves that a DeFi protocol can create a real consumer-grade product—though 200,000 total users remains niche.

The user acquisition problem in emerging markets has been resolved; the monetization problem remains. The gap between MiniPay's 4.2 million weekly active users and its undisclosed (presumably very low) revenue may well be the biggest unsolved problem in the crypto industry—and also the biggest opportunity.

Marginal Improvement vs. Non-Incremental Value: Refining the Selection Criteria

A common rebuttal to investing in consumer-grade crypto is that crypto must offer non-incremental value compared to fiat solutions to offset integration costs. Data indicates that this premise itself is flawed. Comparing two of the clearest data points in the payments category. MiniPay's advantage over traditional mobile money products like M-Pesa is, at most, marginal for users—slightly cheaper transfers, slightly broader US dollar exposure, slightly wider cross-border coverage. It has 4.2 million weekly active users, and its revenue is essentially zero. RedotPay's advantage over traditional Visa issuing-acquiring mechanisms is also marginal in terms of consumer experience—swiping a card, buying a hot dog—but the underlying mechanisms are structurally different: zero chargeback risk, instant cross-border settlement, no reliance on intermediary banks. RedotPay has generated an annualized revenue of $158 million from 6 million users.

Both products are working, both have PMF. The difference is that RedotPay's "marginal yet structural" advantage can compound into pricing power, while MiniPay's "marginal yet superficial" advantage cannot. Zero chargeback risk is not a feature users will notice, but it translates to about a 1.5% gross margin captured on every transaction for the issuer. Slightly cheaper transfers are something users only pay attention to once and stop valuing once they form a habit.

From this, we deduce that the correct selection question is not "Is this non-incremental?" but "Does this marginal improvement reflect structural characteristics of unit economics?" If the answer is yes—chargeback risk, settlement timeliness, intermediaries, capital efficiency, custody costs—then a product that feels virtually unchanged to users can still compound into a large business. If the answer is no, then this product, even with tens of millions of users, lacks investment value. Consumer-grade crypto has both types, and conflating them has already cost this category an entire generation of capital.

E-commerce

Common understanding: Crypto payments are gradually being adopted by e-commerce; it's just a matter of time.

Data shows: No on-chain e-commerce protocol on DeFiLlama reported income exceeding $10,000. Not "very little;" it is literally zero.

This chapter discusses not the competition among initial players but the absence of competitors. After auditing all protocols tracked by DeFiLlama and TokenTerminal and all companies publicly disclosed, we found only one noteworthy player: Travala, a centralized travel booking platform, reported income of $7.17 million in February 2026 (medium confidence—self-reported, not independently verified). Travala is not a protocol; it is a travel agency that accepts cryptocurrency.

UQUID claims 220 million users and 50 million monthly visits (the 220 million figure actually represents users of partner platforms—such as Binance—not UQUID’s own users). The headline figures are misleading, but its product catalog is indeed quite large—175 million physical goods and 546,000 digital products—the share of Tron in its transaction volume doubled to 39% in the first half of 2025, with 54% of transactions priced in USDT-TRC20. However, there is no publicly available income data, and the user counts are questionable.

Gift card and coupon service provider Bitrefill has a monthly income of about $1 million (low confidence—Growjo estimates, traditionally inaccurate). Other than this, there are no other notable on-chain e-commerce protocols.

What truly exists is a shadow e-commerce economy operating on the Tron USDT track—but it is P2P and entirely informal. Coins.ph handles remittances from overseas Filipino workers, with funds flowing into retail consumption. Nigeria's P2P ecosystem guides $59 billion in crypto transaction volume annually through OTC platforms and dollar savings accounts (from Chainalysis), serving as a substitute for a fractured banking system. In Argentina, SUBE bus recharges are completed via Tron USDT and cash OTC channels. Vietnamese freelancers receive payments in USDT-TRC20 and then exchange them through local P2P networks.

This is real economic activity—but it is not e-commerce infrastructure. No protocol has genuinely captured any part of it. The entire crypto-native e-commerce stack—product selection, checkout, custody, fulfillment tracking, dispute resolution, rewards—remains almost entirely vacant.

How Much Demand Will Remain After Compliance?

Before declaring this as the largest product gap in crypto, a more difficult question must first be answered: how much of the existing demand is structural, and how much is regulatory arbitrage? The honest judgment is that the vast majority is regulatory arbitrage. Today, the mainstream use cases on the Tron-USDT e-commerce track can be categorized into three: demand for US dollar exposure from users in capital-controlled regions (Argentina, Venezuela, Nigeria)—who are unable to legally hold US dollars through traditional channels; the avoidance of VAT, sales tax, and import duties, especially on digital goods and gift cards—tax authorities find it challenging to verify buyer identities; and freelance and gig payments circumventing bank controls across borders—mainly occurring in Vietnam, Iran, and parts of Africa. UQUID's product catalog is heavily skewed toward gift cards, mobile top-ups, and digital goods—these categories exist precisely because they can convert opaque crypto balances into spendable fiat equivalents with little identity friction.

This is crucial for the investment argument because the survival rate of regulatory arbitrage demand under compliance varies greatly. Domestic VAT and tax avoidance demand drops to zero the moment KYC is enforced at the merchant level—these users are not paying for a better checkout experience but actually for “no tax ID field;” and as soon as tax IDs are required, value disappears instantly. Demand for circumvention of currency controls is somewhat more persistent because its underlying issues (capital controls in Argentina, Naira controls in Nigeria, Bolívar in Venezuela) are structural and long-standing. However, platforms servicing these needs cannot operate legally within the required corridors. They can grow, but cannot register, cannot raise financing, nor can they engage in partnerships with local fintechs—such partnerships are key to establishing their moats.

Opportunities that can survive compliance are narrow but real. Cross-border merchant settlement where traditional channels are slow or expensive—Latin America ↔ Asia, Africa ↔ anywhere, freelancer receipts—can work under any regulatory framework because the underlying value proposition is that “stablecoins are structurally cheaper than SWIFT” rather than “stablecoins help you bypass the rules.” B2B settlements between SMEs in different jurisdictions also fall into this category. Merchant settlements for cross-border digital services are similarly situated.

Thus, framing the discussion of the “$5 trillion global e-commerce” opportunity is incorrect for this context. The truly investable area is closer to the $200 billion to $400 billion cross-border B2B and freelancer payment market—an area where value propositions can transition from gray zones to legitimate markets. Domestic crypto checkout targeting Western consumers—the thing most “crypto payment” narratives envision—is not this opportunity and never was. The protocols winning in this category will look more like “stablecoin versions of Wise” than “crypto versions of Shopify.” For investors, the critical question is whether a team is building for a market that can survive or one that is about to disappear.

Speculation: The Perpetual War Has Long Ended

Common understanding: Decentralized perpetuals are a competitive market, with dYdX, GMX, and others vying for market share against Hyperliquid.

Data shows: Hyperliquid has already won. GMX and dYdX are not competitors, but protocols in terminal decline.

Hyperliquid currently controls over 70% of all on-chain perpetuals' open contracts, with a nominal monthly trading volume of $105 billion and has generated $58.8 million in fees just in March—annualizing to over $640 million (high confidence—TokenTerminal, DeFiLlama, Dune). In the most recent reporting period, fees grew by 56% month-on-month. It has executed over $800 million in HYPE buybacks and is one of the few protocols where token value capture is not just talk.

Comparing with older players. GMX has daily revenue of $5,000 and daily active users of around 500. dYdX has daily revenue between $10,000 and $13,000, with around 1,300 daily active users, and its fees have dropped 84% year-on-year. These are not struggling competitors—these are protocols whose runway has ended mathematically rather than strategically.

edgeX's data is notable: it had $14.7 million in verified 30-day fees, with a 73% fee retention rate, running on StarkEx ZK-rollup. There was an aggregation error in our previous dataset, initially showing $2.5 million—corrected, edgeX firmly holds second place in on-chain perpetuals by revenue (high confidence—TokenTerminal verified daily). Whether edgeX can maintain growth or will follow the path of GMX/dYdX is the only unanswered question in this category.

Hyperliquid is worth analyzing because its success is not driven by better trading UX—it has real, though marginal, differences in order execution levels compared to GMX or dYdX. It wins on liquidity depth, speed of listings, and branding. Once perpetual liquidity concentrates in one venue, the network effect is nearly unshakeable: traders move to the venues with the narrowest spreads, the narrowest spreads attract the highest volume, and volume returns to where the traders are. The perpetual DEX category has completed its winner-takes-all phase, and deploying capital to counter Hyperliquid in this category is akin to throwing money away.

Prediction Markets: A Story of Category Choice, Not Decentralization

Another speculative category worth examining is prediction markets, with the mainstream narrative being that Polymarket validated the path of on-chain prediction markets. Data tells a different story—and the lessons of this story are not fundamentally related to decentralization.

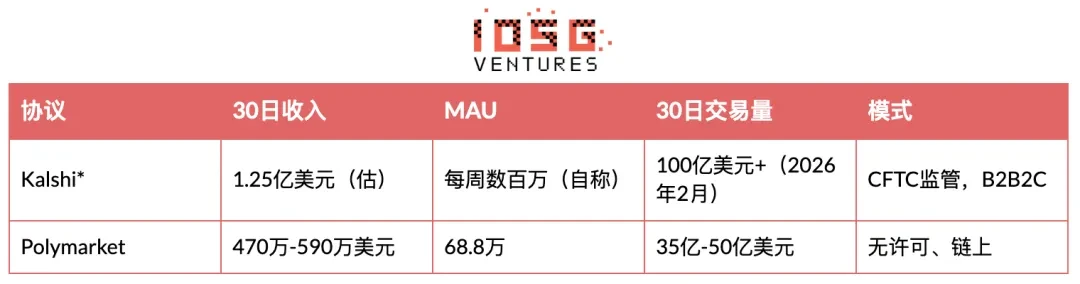

Kalshi operates off-chain / like a CEX. The comparison itself reveals insights.

According to Bloomberg (high confidence), as of March 2026, Kalshi has annualized revenue of $1.5 billion and a valuation of $22 billion. Just in February 2026, it processed over $10 billion in trading volume, with 12-fold growth in volume within six months. Sports betting contributes 89% of its revenue. The on-chain alternative Polymarket generates monthly revenue of $4.7 million to $5.9 million, with 688,000 MAUs. Kalshi's monthly revenue is approximately 25 times that of Polymarket.

The lazy explanation is that Polymarket has a UX problem. From most product dimensions, Polymarket is the better-built platform—cleaner order books, faster settlements, and an even more mature trading experience than Kalshi. The UX rationale fails to account for a 25-fold revenue difference. The so-called defense that Polymarket "hasn't started charging yet" actually worsens the comparison, not improves it: if Polymarket is losing 25 to 1 without any rates, then the underlying potential revenue gap is likely even greater than the surface numbers suggest.

The real explanation lies in category choice, distribution channels, and jurisdictional positioning—none of which have anything to do with decentralization.

Kalshi chose sports. Sports is a high-frequency, mainstream, structurally recurring category: there are betting opportunities every week, every day, every year; rules are widely understood, and audiences self-update with new seasons. Users who come to Polymarket for the 2024 election have no reason to return in March 2026. Users who come to Kalshi for the NFL have reasons to return every Sunday. Frequent participation compounds into liquidity, liquidity compounds into spreads, and spreads compound into more users. Polymarket has positioned itself on the wrong side of the flywheel.

The second factor is distribution. Kalshi has built a B2B2C model, integrating its order book into broker platforms, fintech applications, and partners, rather than relying on direct-to-consumer acquisition. Polymarket only does DTC, with every active trader bearing the full cost of marketing. Crucially, Kalshi operates legally under CFTC regulation in the U.S., while Polymarket—following its 2022 settlement with the same agency—has completely geo-blocked U.S. users. The largest audience for English-language prediction markets is structurally unreachable by on-chain products. Kalshi does not merely win in execution; it possesses a market that Polymarket is legally barred from entering.

The implications for evaluating prediction market projects are quite specific. The correct due diligence questions are: (1) How frequent is participation in the chosen category; (2) Does the project have a B2B2C distribution path, or does it rely on direct acquisition; (3) What is the regulatory stance in the target market? The level of decentralization is fundamentally irrelevant to the outcome. Polymarket's loss of 25 to 1 stems from wrong category choice, wrong distribution mode, and wrong jurisdiction—generally in that order of importance.

Inferences from This Chapter

The speculation segment has two key points: (1) Categories that have already produced winners have indeed produced winners; capital should no longer flow there; (2) The mechanisms behind winner outcomes are not decentralization, UX, or token economic models—perpetuals depend on liquidity concentration, while prediction markets depend on category choice and distribution. Both conclusions point to the DeFi mullet thesis: the most defensible consumer end positioning is to wrap a compliant front end around a crypto-native back end. Ether.fi Cash is currently the cleanest case. CrediFi and next-generation payment adjacent products belong to the same model.

Stablecoin Infrastructure: Tron is the Most Important Consumer-Grade Public Chain, Yet No One Talks About It

Common understanding: Ethereum L2 and Solana are the main consumer-grade public chains; Tron is an old network mainly used for cheap transfers.

Data shows: Tron has monthly stablecoin transaction volumes exceeding $600 billion—comparable to Visa—with 14.3 million MAUs, 72.8 million USDT holders, and a stablecoin velocity ratio of 0.2–0.3. This proves its activity is for payments rather than speculation. It has an entire suite of unmarked protocol shadow economies, of which Western media has zero coverage.

The numbers are staggering. The USDT-TRC20 supply on Tron stands at $86.4 billion. Monthly transfer amounts range between $600 billion and $1.35 trillion (the lower limit is high confidence—TronScan, TokenTerminal; the upper limit includes cyclical trading volume). On March 29, 2026, the daily transfer volume reached $44.9 billion. The network processes over 2 million transactions daily, covering 13.8 million MAUs, with an estimated 80% of the transaction volume below $1,000 and 60%–70% below $100. This is a retail payment network, not a settlement layer dominated by whales.

Speed metrics are key analytical signals. The USDT velocity in Tron is 0.2–0.3, meaning that, on average, one dollar of USDT on Tron circulates approximately every 3 to 5 months. In contrast, speculative public chains can have speeds exceeding 10 times this—rapidly cycling through DeFi protocols, leverage positions, and launchpads. Tron’s stable, slow speeds reflect payment track characteristics: money comes in for a real-world transaction and then stays in wallets awaiting the next bill or remittance. The top ten USDT holders on Tron control only 8.7% of the supply—indicating broad and decentralized retail distribution.

Next is the shadow economy. We audited TronScan and identified several unmarked, revenue-generating protocols with no English documentation whatsoever:

CatFee has a daily fee of $82,000. No one in Western crypto media knows what it is. TRONSAVE has monthly revenue of $863,000, with all parties' identities unknown. These protocols operate within Vietnam’s P2P networks, Nigeria's OTC platforms, Philippine remittance corridors, and shadow economies in Latin America. We estimate that tens of billions of dollars flow through these unmarked clearinghouses daily—dynamic addresses, collected settlements, and freelance payment infrastructures, effectively serving as a banking system for people shut out by traditional finance.

Celo is the fastest-growing public chain in this category, driven entirely by integration with MiniPay and Tether. Independent user numbers have grown 506% year-on-year, with a total of 12.6 million wallets and a transaction volume of $153 million in December 2025 (high confidence). However, its scale still represents only a small fraction of Tron.

Ethereum remains the settlement track for institutions—its high fees limit retail use. Solana’s stablecoin activity is dominated by trading and launchpad traffic (pump.fun, Jupiter, Meteora), rather than payments. BNB Chain carries a monthly stablecoin trading volume of $60 billion, mainly for CEX settlements. TON is a variable—Telegram’s wallet integration has brought large registration numbers, but the participation depth remains unclear.

Summary: The Lifecycle of Regulatory Arbitrage and the DeFi Mullet

Every successful consumer-level crypto category identified in this census has gone through the same arc. It starts with regulatory arbitrage; accumulates capital and users in gray areas; undergoes—or fails to withstand—an enforcement pushing event; and the portion that makes it through becomes legal financial infrastructure. Today, protocols and companies generating real revenue are at different stages of this lifecycle, and their positioning determines the risk-return curve of investment.

Stage 1—Gray Area Launch. A protocol or service emerges to solve problems that traditional finance refuses or is unable to service, almost always due to some regulatory constraint. The user base is small, technologically sophisticated, and tolerant of legal ambiguity. Profit margins are extremely high, as regulatory risks are priced into the cut. Tail risk is unlimited. Today's examples: unmarked shadow clearinghouses on Tron (CatFee, TRONSAVE), Nigeria's P2P USDT platforms, and early pump.fun, NFT, and even early Hyperliquid.

Stage 2—User and Capital Accumulation. PMF becomes indisputable. Transaction volumes grow, with users starting to come from outside the core tech circles. Western media starts to pay attention, but regulators have not yet acted. Tron’s USDT economy is currently in this stage—14.3 million MAUs and monthly transaction volume over $600 billion. The pump.fun of 2024, Polymarket during the 2024 election cycle, and current Hyperliquid are also in this stage.

Stage 3—Compliance Transition. A forcing event—a lawsuit, enforcement action, settlement, or proactive regulatory communication—drives projects to choose legality, fragmentation, or death. This stage has the highest variance and is also the most analytically valuable from an investment perspective. Polymarket's 2022 settlement with the CFTC, the $500 million lawsuit against pump.fun, and any potential future enforcement actions targeting offshore perpetual venues are at this stage. Most projects cannot fully traverse this stage.

Stage 4—Legal Economy. The portion that has made it through becomes substantial, auditable, and fundable. Returns compress because businesses are now priced based on fintech valuations rather than moonshot valuations. Kalshi (CFTC-regulated, valuation of $22 billion), Exodus (NYSE-listed in the US, SEC-registered), Circle (S-1 disclosed), and RedotPay (financing at fintech comparable multiples) are all located here.

When we lay out the arc this way, the timing of investment issues becomes specific. Stage 1 has the greatest upside potential, but is virtually uninvestable for institutional capital—the underlying business can be zeroed out overnight with an enforcement order, and underwriting can't realistically happen. Stage 4 is already fully priced; the multiples are fintech multiples, and asymmetry has disappeared. Stage 2 has historically been the best for VC returns in this sector, but only if there is a credible path to traverse Stage 3. The due diligence question for Stage 2 is no longer "Has the product worked?"—Stage 2 has evidently worked. The question is whether the business model can survive under compliance.

Tron’s shadow protocols cannot pass this test because their very reason for existence is circumvention. Once Vietnam implements KYC for Tron USDT liquidity, CatFee’s daily fees of $82,000 would vanish immediately—users are paying not for utility but for "having no identity." There is not a compliant business model underneath. This is the fundamental difference between a “protocol with PMF” and a “protocol that fits only within regulatory arbitrage.” Both can generate income, but only one is investable.

The DeFi mullet thesis is directly derived from this framework. Products like Ether.fi Cash and next-generation Latin American fintech can succeed because they wrap a layer of compliance around a crypto-native back end. Users do not see or care what the chain is. Regulators see an ordinary fintech. Protocols capture the economics of “the cheapest track.” These projects currently do not issue tokens—this in itself is a signal: value capture occurs at the equity level rather than the token level, and the institutional investors who will win in this cycle will be those holding equity positions rather than token shares.

The three structural opportunities repeatedly emerging in this report also derive from this synthesis: monetization infrastructure in emerging markets (users are already present, revenue has not yet arrived); cross-border B2B and freelance payment e-commerce tracks (the parts that can survive the e-commerce gap); and the still-undiscovered ecosystem of adjacent protocols to Tron in Stage 2 of their lifecycle. All three are best suited for entry in a DeFi mullet model; all three reward category choice rather than decentralization purity; all three are currently undervalued because Western capital is still looking at the wrong dashboards.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。