This text is from:Arrakis Finance

Compiled by|Odaily Planet Daily(@OdailyChina);Translator|Azuma(@azuma_eth)

Earlier this month, we wrote an article titled “Who is Trading on HIP-3,” which used a statistical inference attribution method to classify each address based on trading behavior over the past three months: addresses primarily placing orders (makers) were classified as Market Makers, addresses with high-frequency taking behavior were categorized as Arbitrageurs, and addresses with lower transaction rates marked as builders were considered Retail.

Although this method revealed some interesting patterns in market structure, the classification was still essentially probabilistic, and about 70% of addresses could not be effectively categorized.

In today's article, we will adopt a mechanical attribution method instead of statistical inference. On HyperliquidX, each order includes a set of deterministic labels, which are signed and released by the exchange (such as time-in-force, builder code, fill flag, hold time). Based on this order metadata, we classified all addresses into four main categories —Retail, Market Maker, Arbitrage Bot, or Airdrop Farmer.

The second step is to identify the specific identities behind these classifications. We extracted identity and trading behavior data from the APIs of Arkham and HyperTracker. The top 450 addresses contributed 78% of the total trading volume. In this set, we identified several related entities, including addresses associated with Polymarket, Jump, Selini Capital, Wintermute, Abraxas Capital, and others.

Through these two classification methods, we observed some critical conclusions, which will be analyzed in detail below.

Address Distribution

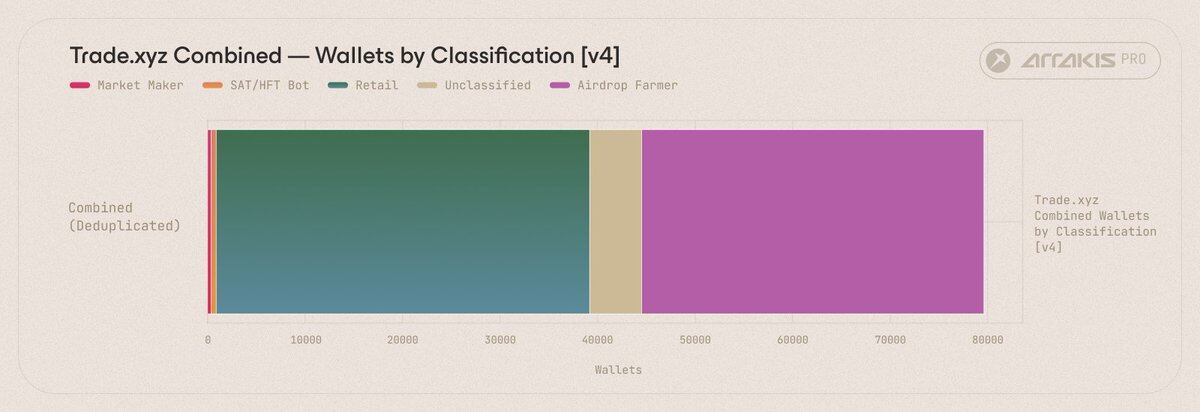

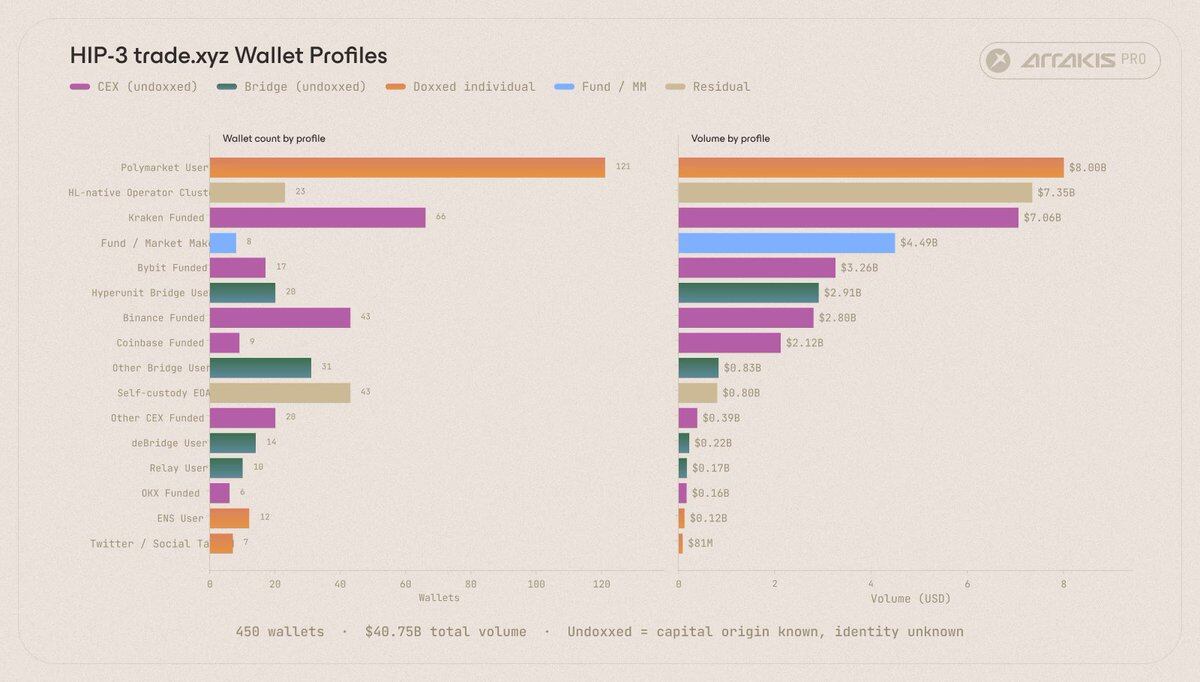

Our observation period was from March 10, 2026, to March 31, 2026, totaling 21 days. During this time, we observed four Trade.xyz markets, including CL (crude oil), SILVER (silver), TSLA (Tesla), and XYZ100 (index), recording a total of 79,622 independent participating wallets and a total trading volume of 5.195 billion dollars.

Among the 79,622 addresses that participated in trading within 21 days, although Market Makers account for less than 0.5% of the total addresses, they contributed 63% of the trading volume.

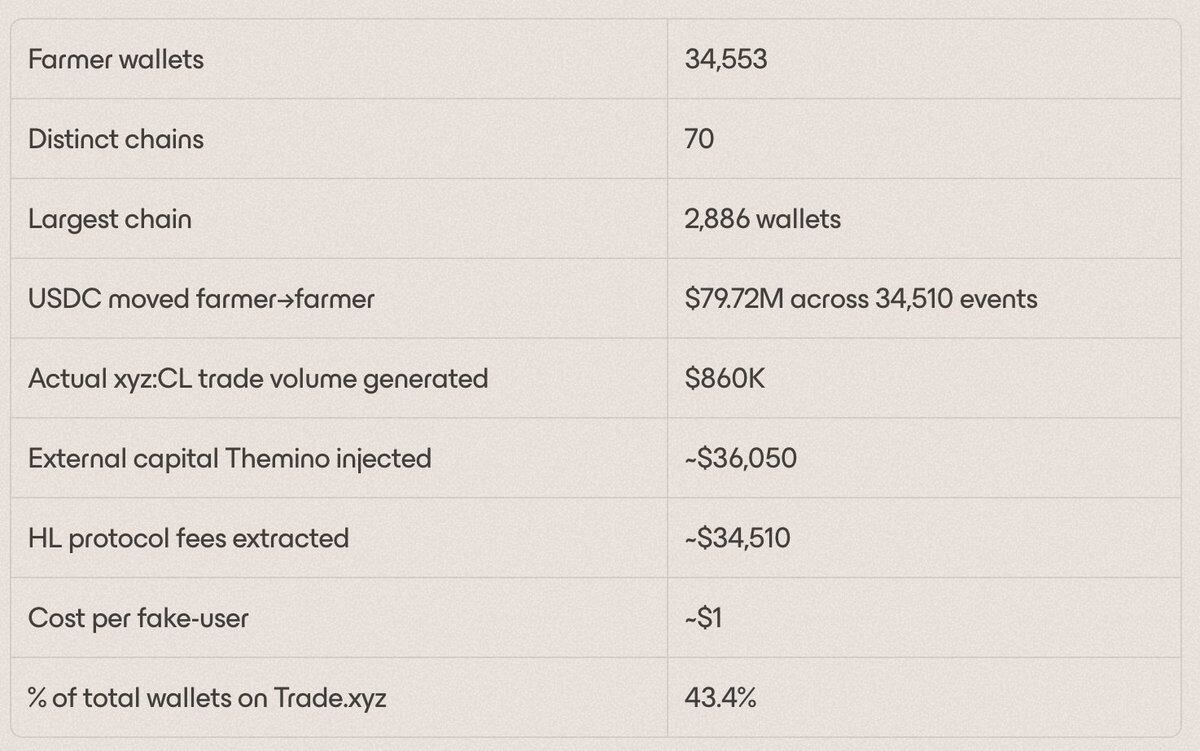

If classified by wallet number instead of trading volume, the Airdrop Farmer category alone includes 35,091 addresses, nearly half of the total recognized addresses.

Airdrop Farmers are one of the largest categories by address count, but they account for the smallest proportion of trading volume. 35,091 addresses only account for 44.07% of the total, but generated only 400 million dollars in trading volume during the observation period, accounting for 0.77% of the platform’s total trading volume of 5.195 billion dollars. In other words, nearly half of the active addresses on Trade.xyz contributed less than 1% of the total market trading volume.

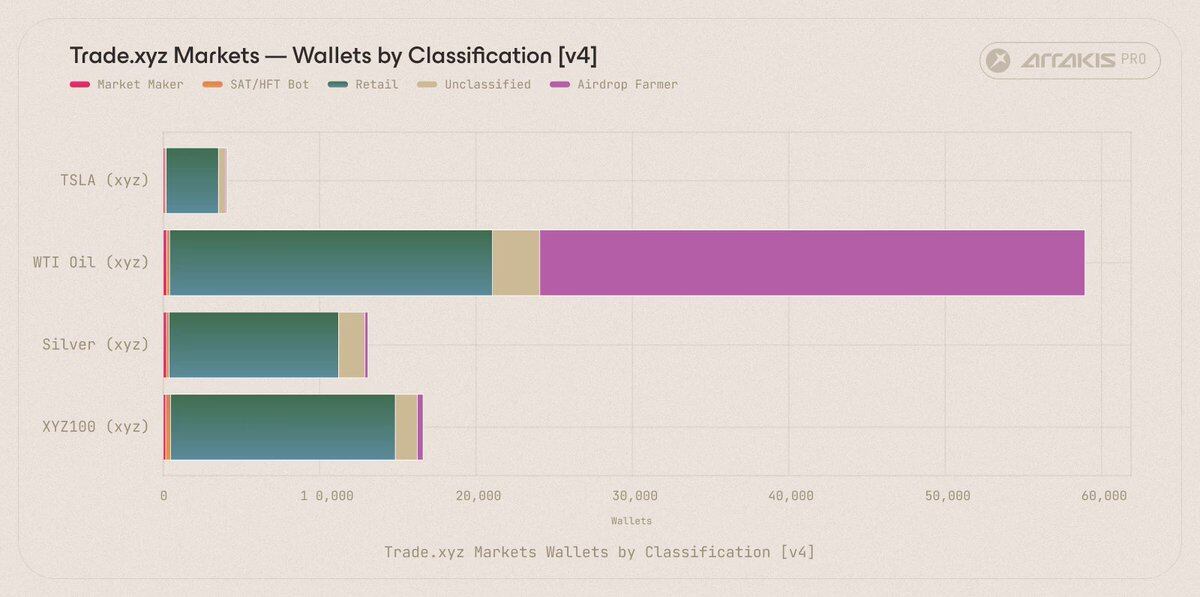

When broken down by specific markets participated in, another significant pattern is observed.

The address distribution by market shows that the CL (crude oil) market, due to its best execution efficiency, absorbed 99.3% of the Airdrop Farmers.

Among the 35,091 Airdrop Farmer addresses, 34,859 (99.3%) traded CL during the observation period, while the remaining 232 wallets were distributed across SILVER, TSLA, and XYZ100. This pattern aligns with Airdrop farming behavior characteristics — each wallet accumulates trading volume through bidirectional continuous small transactions, without bearing price risk. This strategy relies on very low execution costs and benefits from minimal slippage. CL is the deepest of these four markets on Trade.xyz, making it a natural venue for such behavior.

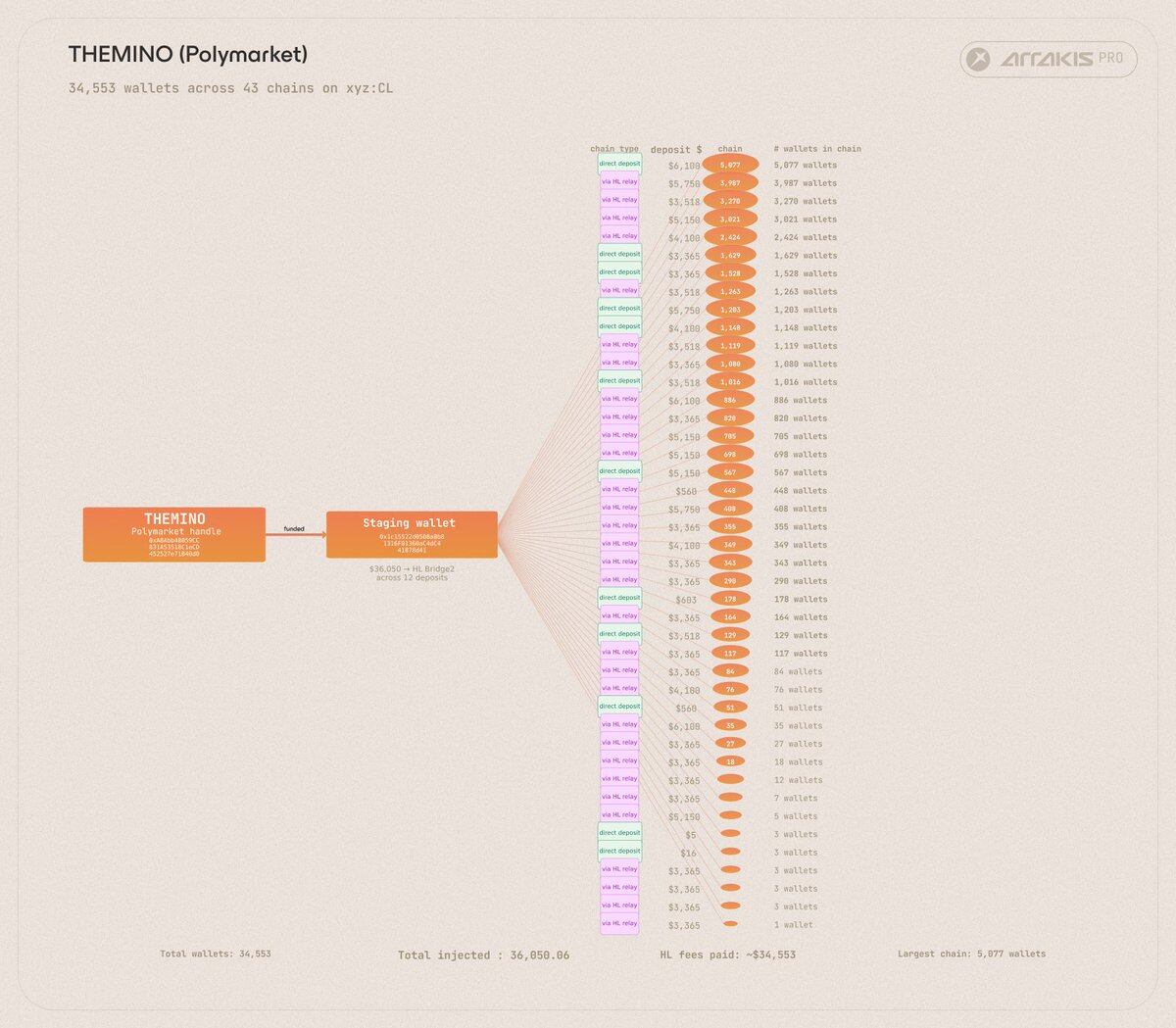

Another interesting observation is the entities behind these addresses. The on-chain tracing shown later in the article links 34,553 of the farmer addresses to a single Polymarket operator, which alone accounted for 43.4% of all participating addresses on Trade.xyz during the observation period.

The other extreme in this classification is Market Makers. 363 wallets (accounting for 0.46% of active addresses) completed 32.75 billion dollars in trading volume during the observation period, accounting for 63% of Trade.xyz's total trading volume. The remaining three categories are distributed between these two (Market Makers and Airdrop Farmers) — 522 SAT/HFT bots contributed 3.5 billion dollars (6.7%), 38,307 addresses categorized as retail contributed 8.7 billion dollars (16.7%), and another 5,339 unclassified addresses contributed 6.61 billion dollars in trading volume (12.7%).

This 12.7% of unclassified trading volume cannot be attributed to a clear strategy based solely on metadata. It is reasonable to speculate that a considerable portion of this comes from retail users placing limit orders through Hyperliquid’s frontend, or users submitting market and limit orders via Trade.xyz’s frontend. Since the orders from these two channels do not include a clear builder code or a dedicated TIF label, these transactions are invisible in the metadata-based classification.

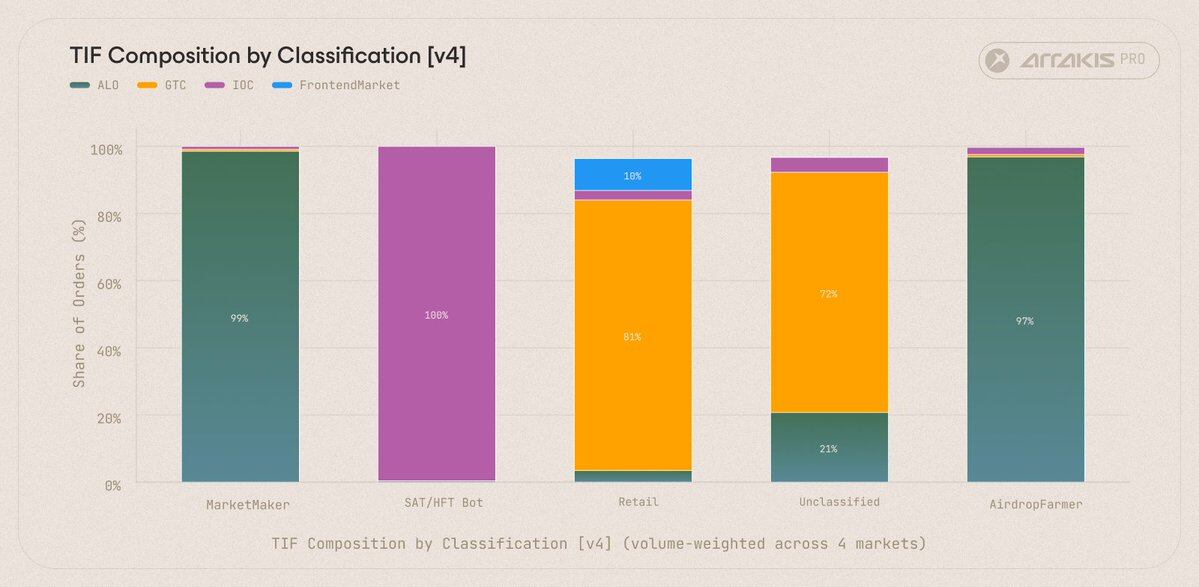

The time-in-force (TIF) distribution weighted by order quantity shows that 98.5% of Market Makers are ALO orders, whereas 100% of Arbitrage Bots use IOC orders; 71.5% of the unclassified category are GTC, which is typical for limit orders manually placed by frontend users.

The TIF structure further supports this speculation. Among the aggregated orders in the unclassified category, 71.5% are labeled with GTC (Good Till Cancel) time validity, which is typically used for limit orders with continuous effectiveness placed by frontend users.

Introducing the Real High-Level Player, Themino

In the past few weeks, a controversy around Trade.xyz has been heating up — does its apparent user count reflect genuine human participation, or is it artificially inflated by airdrop-interactive behavior in anticipation of the platform's upcoming TGE? Although we cannot comprehensively comment on the interactions across the entire trading platform, we found a noteworthy clue while analyzing the detailed transaction data of the four Trade.xyz markets in March.

Among the 34,602 addresses classified as Airdrop Farmers, 34,553 (99.9%) can be traced back to a Polymarket user named Themino.

Themino Cluster: A user identity on Polymarket that derived 70 independent linear links covering 34,553 Airdrop Farmer addresses.

The operation of Themino is as follows. Hyperliquid's Layer1 provides an internalTransfer primitive that allows USDC to be transferred between addresses, with a fixed fee of 1 dollar regardless of the amount. The operator of Themino leverages this mechanism to “pass” an initial amount of funds among tens of thousands of new addresses one by one. Each address executes the same five-step operation flow in about 26 seconds:

- Receiving funds from the previous address via internalTransfer (paying a 1 dollar transfer fee during the transfer process);

- Transferring 14 dollars into an xyz sub-account;

- Executing two IOC orders on the CL market (one buy, one sell), generating two trades, thus recording a certain trading volume;

- Transferring about 13.99 dollars back to the main account (this penny difference comes from executed slippage and transaction fees);

- Again transferring funds to the next address via internalTransfer (paying another 1 dollar fee);

- Repeating this process…

Throughout Themino's entire operation, there were a total of 34,510 internal-transfer events, resulting in Themino accumulating 34,510 dollars in protocol fees, which aligns with their trading history on Polymarket.

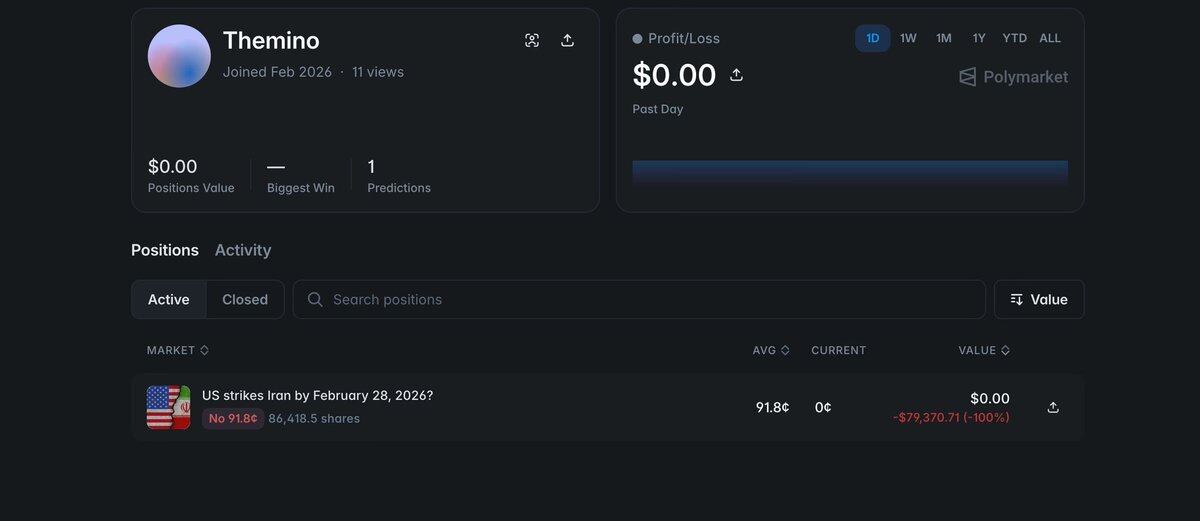

Additionally, Themino placed a bet on Polymarket regarding the event “Will the U.S. strike Iran before February 28, 2026?” betting “no,” ultimately losing around 80,000 dollars — the airstrike indeed happened on February 28.

The Different Groups Behind the Builders Tag

Hyperliquid adds an identifier to orders routed through third-party frontends to facilitate charging custom frontend fees. This identifier is the Builder Code, which is also the most direct basis for determining which interface an address trades through (if any). Among the addresses participating in trading in these four markets, the Builders tags can be summarized into three groups.

Algorithmic Builders (Algorithm Builders). This type of product is mainly used by retail traders to maximize trading volume on DEX to earn potential airdrop points. Before the end of 2025, interacting on Perp DEX usually meant executing wash trading or non-directional taker-taker orders through algorithms, which is costly for participants and a net loss for exchanges. Retail market-making bots like tread.fi, Planemo Trading, and Origami Tech have replaced wash trading with “valuable market-making behavior.” The orders submitted through these products are all post-only, providing liquidity to the order book rather than consuming liquidity.

As David Jeong (CEO of tread.fi) stated: “Before retail market-making solutions emerged, farming on Perp DEX meant wash trading, artificially inflating trading volumes through execution fees, slippage costs, and even the risk of bans. We solved this problem by constructing a new interaction scheme where the bots only place maker orders on both sides. Users interact at lower costs and typically profit from capturing price spreads, while the byproduct is providing genuine optimal price liquidity for the market—this is exactly what is needed during nighttime and weekends when traditional market makers do not quote HIP-3 stock perpetual contracts. It’s a better way to interact, and it’s why HIP-3 markets now have good execution quality.”

The contributions of these market-making bots to the market are especially evident during times when traditional market makers do not provide quotes. CME WTI crude oil futures close on Friday afternoon and reopen on Sunday evening, while stock perpetual contracts face similar overnight and weekend gaps. During these time windows, retail market-making bots filled the top liquidity for markets such as CL and TSLA.

It is important to note that although in this analysis we classify the addresses routed through these algorithm products as airdrops, their trading behavior and impact on the market are structurally different from witching behavior.

Wallet-integrated Builders are perpetual contract trading interfaces embedded in user wallets. Since early 2026, this type of integration has become one of the largest sources of retail order flow on HIP-3. This category includes Phantom, MetaMask, Rabby, Rainbow, and OneKey. The median trading volume per wallet ranges from 1,000 to 3,000 dollars, aligning with retail user characteristics that emphasize convenience over subtle differences in builder fees.

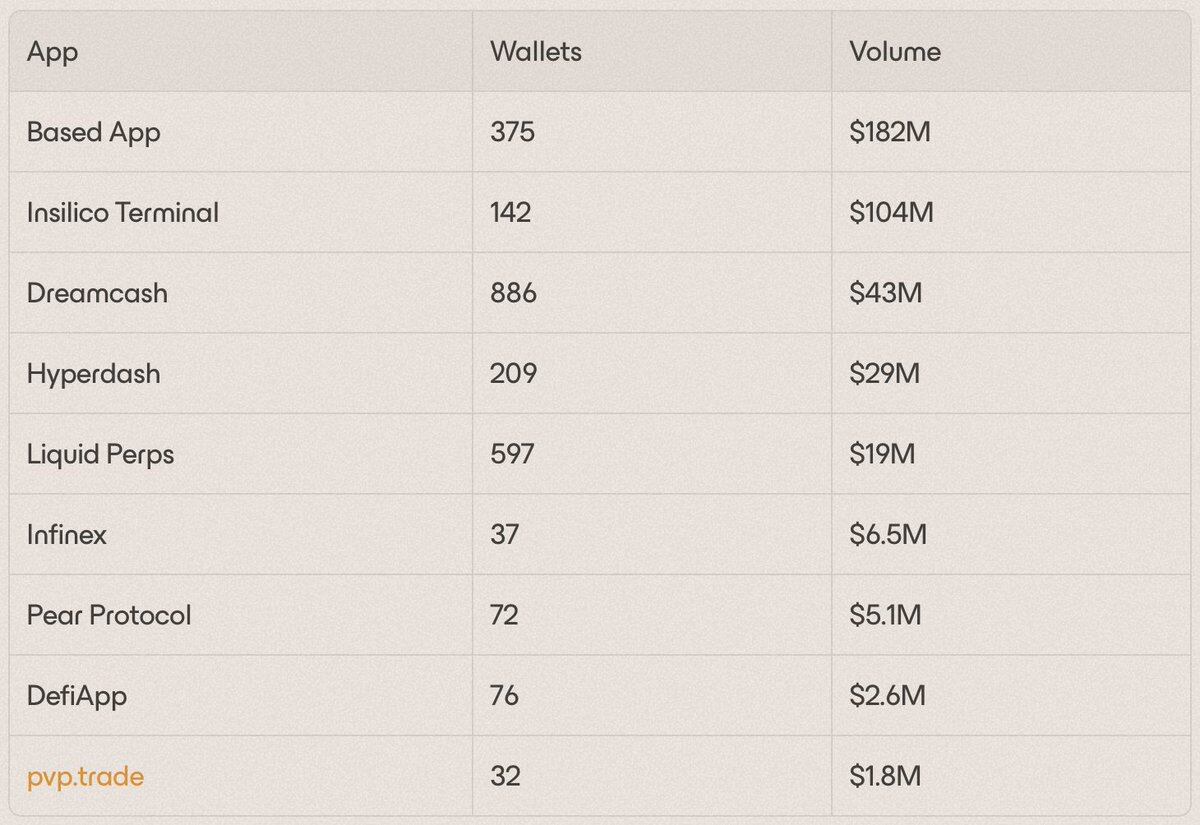

Apps Builders are independent perpetual contract trading frontends and integrated products — tools for traders, providing more complete workflows for users who need to go beyond wallet plugin experiences, including better ordering experiences, charting features, position management, and execution tools. This category has fewer addresses than wallet-integrated channels but higher trading volume per address, characteristic of heavy user groups — they prioritize functional depth over out-of-the-box convenience. Related products include Insilico Terminal, Liquid, Hyperdash, Based, Dreamcash, Infinex, Pear Protocol, Defi App, and pvp.trade.

VKTR (Growth Lead at Insilico) summarized this: “At Insilico, we see the HIP-3 market as the next step towards letting real-world asset exposure natively operate on cryptographic rails. Traders do not just want another frontend; they need fast execution, clear market access, and the ability to switch freely between crypto assets and macro assets without leaving their existing workflow. Trade.xyz is one of the clearest manifestations of this demand. The order flow routed through Insilico indicates that when a trading venue has enough depth, products are sufficiently practical, and the trading experience is designed for professional participants, there indeed exists a genuine high-level user group in the on-chain perpetual contract market.”

Market Maker Address Analysis

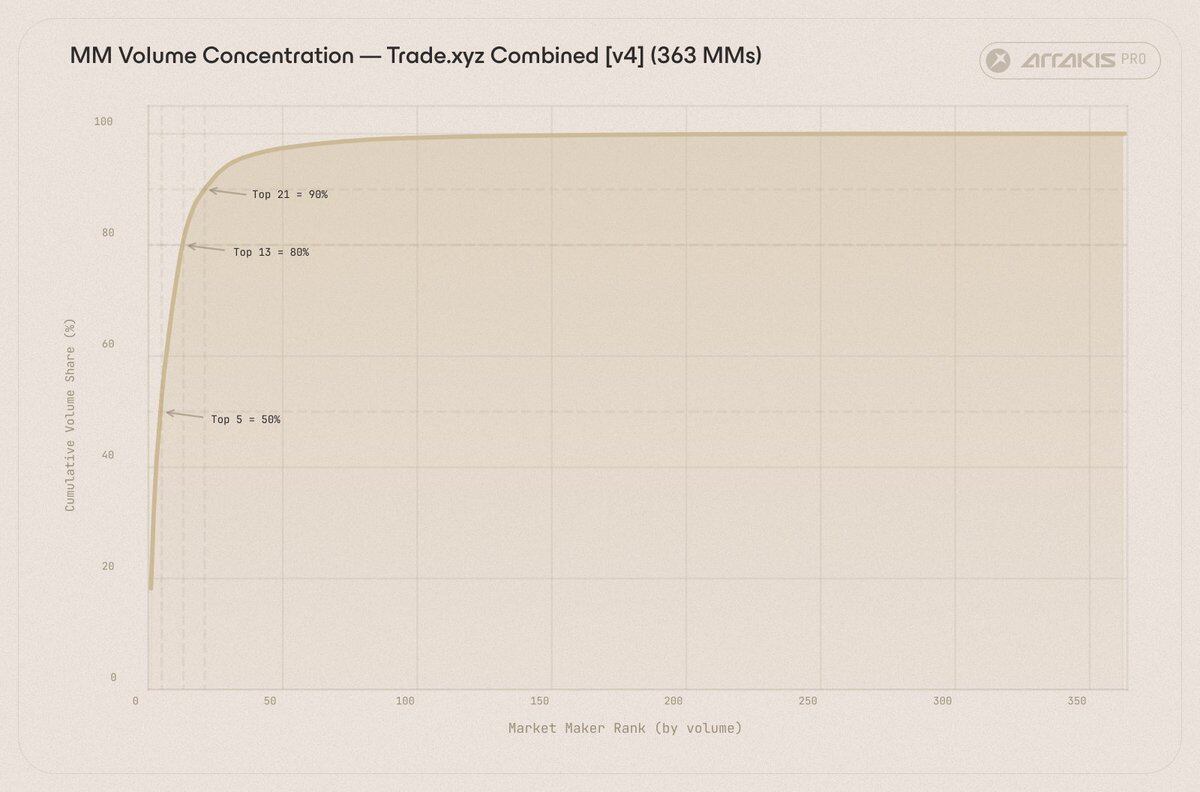

The market-making pattern across the Trade.xyz markets is highly concentrated. The top 5 market makers contribute 50% of the market-making trading volume, the top 13 account for 80%, and the top 21 make up 90%. In other words, the vast majority of market-making orders are dominated by a few trading desks.

The cumulative proportion of market-making trading volume ranked by address shows that the top 5 trading desks contribute 50% of all market-making flow, the top 13 reach 80%, and the top 21 reach 90%.

The second-largest market-making address is one of the most interesting addresses in the entire sample. 0xc926ddba…98d3 achieved a trading volume of 4.39 billion dollars with a 0.52% fill rate, a typical characteristic of market-making behavior. Arkham has tagged this address as Powell on Polymarket. This means that one of the largest market makers on Trade.xyz is, in fact, a Polymarket user making bilateral quotes across multiple markets on HIP-3.

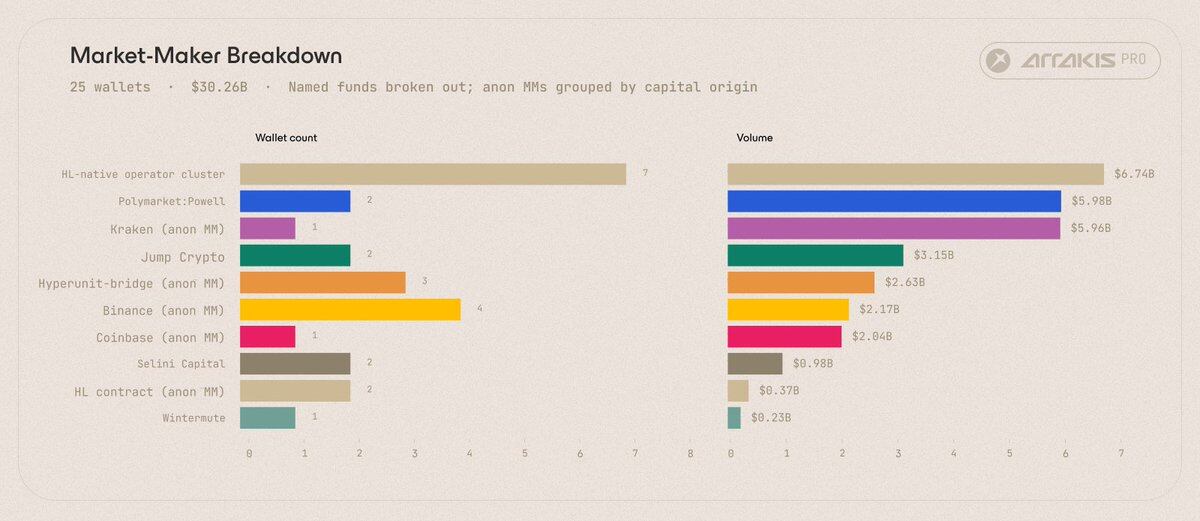

Other notable market trading entities include:

- Jump Crypto operates two addresses, with a total trading volume of 3.15 billion dollars, with funds originating from 0xf584…d621 (recognized by Arkham as Jump’s liquidity pool address), which holds over 160 million dollars in a diversified asset portfolio, including LINK, LIT, EIGEN, BNB, ETH, USDC, and USDT.

- Selini Capital operates three addresses, two for pure market-making quotes (0x44a3e1…35dd, 0x76987c…4480) and one for purely taking orders (0x427be6…d1d9), all operating via API, with a total trading scale of 1.03 billion dollars. Hyperliquid’s order flow labeling mechanism allows Selini’s market-making wallets to be distinguished from their high-frequency trading wallets, as the same trading desk operates both sides of the order book simultaneously.

- Wintermute operates one market-making address, with a trading volume of 229.6 million dollars (0xecb63caa…2b00), smaller than Jump and Selini, with funding sourced from OKX.

Among the top market makers ranked by trading volume on Trade.xyz, Powell, Jump Crypto, Selini Capital, and Wintermute form a part of the order book that can be clearly attributed.

Aside from these known institutions, most of the market-making trading volume comes from addresses of unrecognized entities, but their funding sources are clear, such as from Kraken, Binance, Coinbase, Unit cross-chain bridges, or Hyperliquid native funds. The behavioral characteristics of these addresses align with market makers, but their operators have never used tagging services that could be associated with Arkham identities.

The median order fill ratio for market makers is 19.4, meaning that for every completed transaction, about 18 orders are placed and then canceled to maintain bilateral quotes. The same group of top 5 market makers is active across the four markets mentioned above, indicating that these are unified trading desks for cross-market quoting, not four separate businesses.

During the observation period, the clearing rate for market makers was 19.2%, almost identical to the 20.4% of retail. On Trade.xyz, market makers assume directional risks when orders are filled: a large sell order hitting the buy side will convert the market maker into a long position; a buy order taking out a sell side will convert them into a short position. During the volatility of the crude oil market in March, these accumulated position changes outpaced the trading desk’s ability to hedge, ultimately resulting in about one-fifth of market makers experiencing at least one liquidation.

Arbitrage Bot Address Analysis

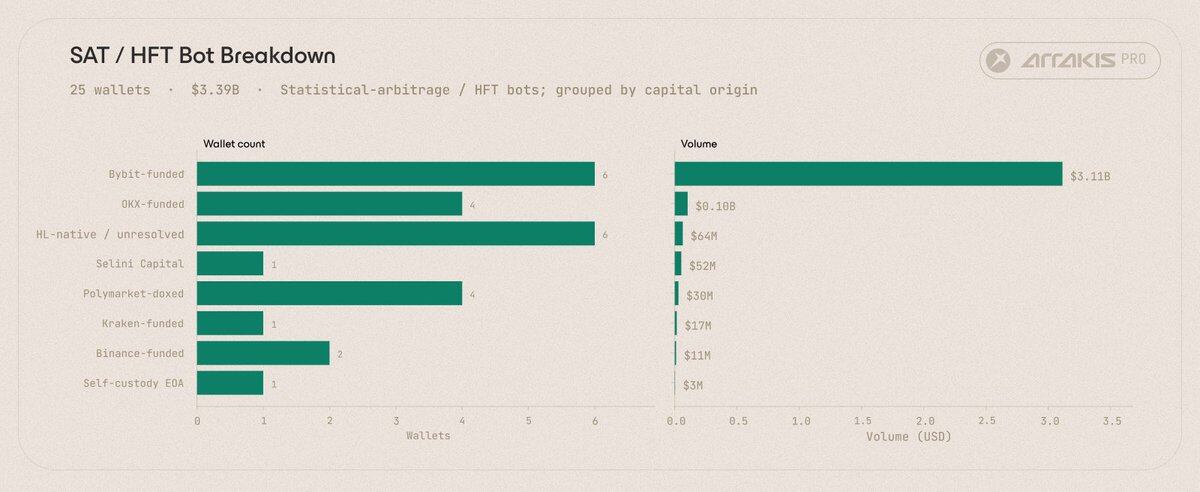

Arbitrage takers (SAT) and medium-frequency trading bots are generally counterparties to the market-making order book. Over 90% of these addresses use IOC (Immediate or Cancel) order types, being pure active takers that directly sweep market makers’ quotes.

Among the top ranked SAT/HFT bots by trading volume, the top 4 addresses account for 89% of the entire SAT order book, and their funding sources are highly concentrated in Bybit.

The top 4 SATs contributed 3.1 billion dollars out of 3.5 billion dollars in total SAT trading volume, accounting for 89%. Two of these addresses' orders are 100% IOC, meaning all their orders are immediate execution or cancellation, with no market-making intentions.

Clustering analysis of funding sources shows that the dominant SAT behavior pattern points to Bybit. Most top SAT trading volumes can be traced to addresses funded by Bybit, consistent with the characteristics of single bot operators or small groups of bot operators.

There are three SATs marked with Polymarket identities: loracles (15.5 million dollars in trading volume, Hyperliquid historical PnL of +25.7 million dollars), Conduit (5.3 million dollars), and ChadwickLongman (3.7 million dollars). The reason Polymarket appears here is consistent with its dominant position in the upcoming retail section — the user group from prediction markets is the most common cross-platform identity source on Trade.xyz.

During the observation period, the clearing rate for SATs was 8.1%, about half that of market makers and retail clearing rates, making them the best risk-controlled group in the order book. They usually hedge externally and seldom trigger margin liquidations.

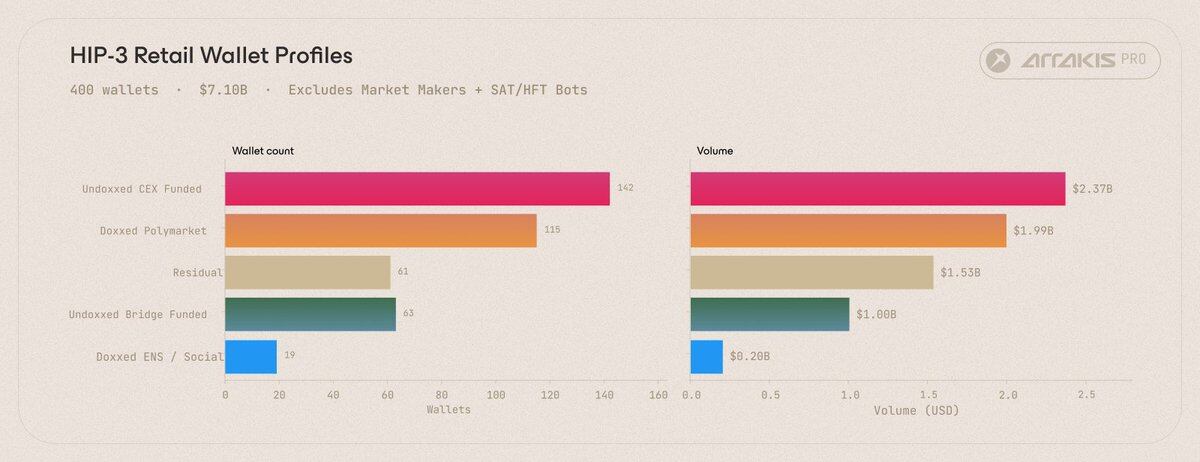

Retail Group Analysis

We further analyzed a subset of 400 high-transaction-volume addresses that traded through Hyperliquid UI or builder-integrated frontends, excluding the algorithm products (Tread.fi, Planemo Trading, and the broader algorithm builders group) mentioned earlier.

Among the top 400 high-transaction-volume retail addresses divided by attribution category, Polymarket users dominate, contributing 1.63 billion dollars in trading volume.

The most prominent retail group in the figure above is Polymarket users. Among the 400 top retail addresses, 94 (22%, corresponding to 1.63 billion dollars in trading volume) can be verified as Polymarket users, representing the largest identifiable group within the retail layer. Combining Polymarket market makers (Powell, 4.39 billion dollars) and the 3 Polymarket SATs (approximately 24 million dollars), Polymarket’s total footprint on Trade.xyz is about 6 billion dollars.

The top 15 Polymarket retail addresses by trading volume are as follows.

This overlap is reasonable. Polymarket and Trade.xyz each provide users with cryptographic native exposure to real-world outcomes through different market structures, prediction markets and perpetual contracts, respectively, and address data indicates the same batch of users trade simultaneously across both platforms using the same EVM address.

ENS users further contributed 26 retail addresses, with a total trading volume of about 400 million dollars. Representative addresses include caydenb.eth (33 million dollars), eggnoodle.eth (33 million dollars), ethmerg.eth (19 million dollars), baitf1sh.eth (16 million dollars), and wanyekest69.eth (6.8 million dollars, historical PnL of +17.6 million dollars).

The unrecognized wallets are split by funding sources as follows.

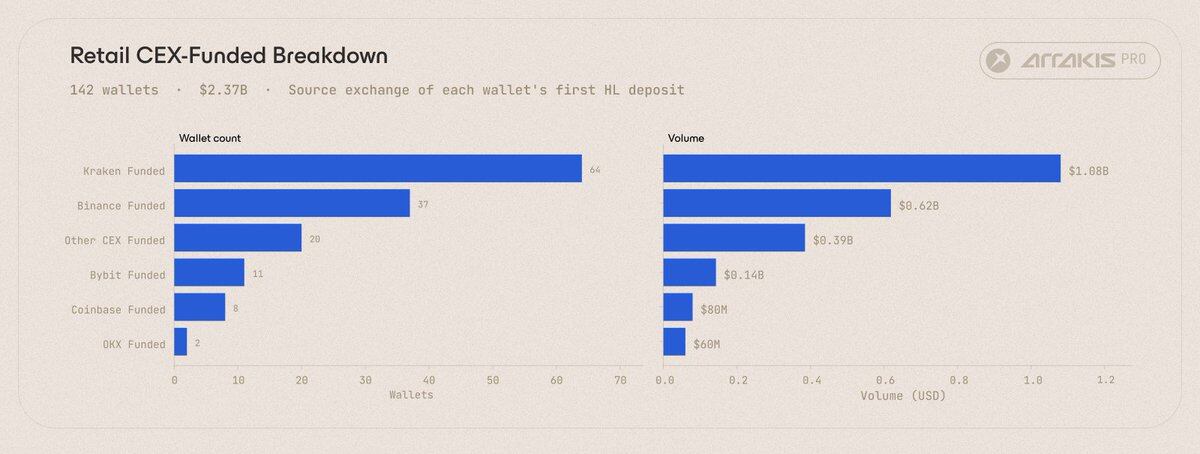

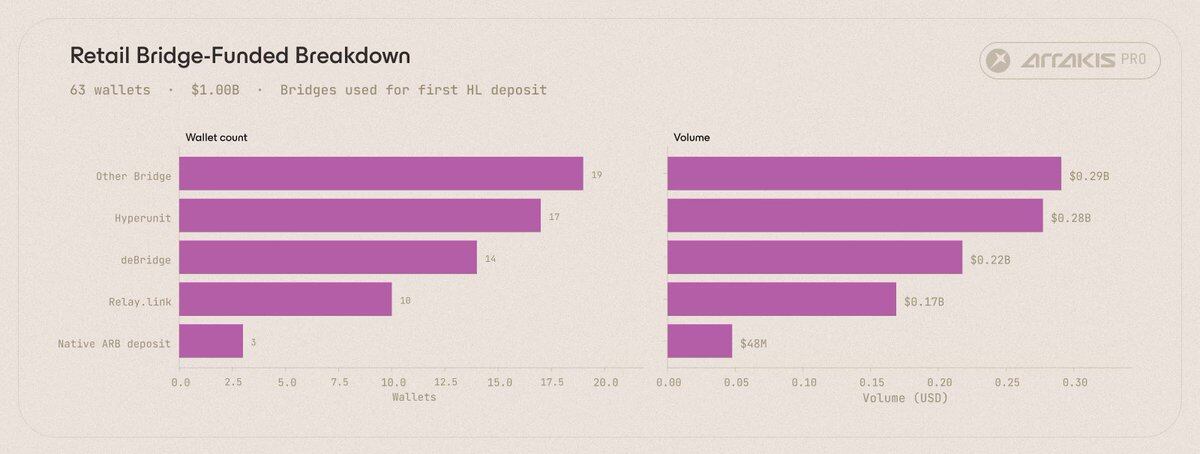

In the retail wallets with CEX sources ranked by exchange, Kraken occupies an absolute dominant position; among cross-chain wallets ranked by bridge sources, Hyperunit and deBridge dominate, with the rest consisting of Stargate Finance and long-tail bridges.

Therefore, retail traders who genuinely trade on Trade.xyz can be categorized into three groups: Polymarket cross-platform traders, independent traders from Kraken, and DeFi native users entering through Hyperunit or deBridge.

Reintegrating the Market Makers, SATs, and retail groups gives a simplified structure of Trade.xyz participants after excluding Airdrop Farmers.

After excluding Airdrop Farmers, the participant structure consists of a few professional market makers facing a few robot teams, and a long-tail group composed of old Polymarket users and independent traders from CEX, these users engage in directional trading through Hyperliquid UI.

A few professional market makers facing a few robot teams, along with a long-tail group made up of old Polymarket users and independent traders from CEX, engage in directional betting through Hyperliquid UI — this constitutes the overall structure of the Trade.xyz order book.

Final Conclusion

Recent discussions around Trade.xyz have primarily centered on one question — is its level of participation genuine, or is the platform dominated by numerous airdrop farmer accounts artificially inflating behavior in anticipation of a TGE? This analysis gives an answer closer to a “layered structure.”

Like any DeFi market prior to a TGE, there indeed exists a group of Airdrop Farmers on Trade.xyz. For instance, a single operator controlled tens of thousands of wallets through “relay-style interaction.” However, it is important to note that this witching layer primarily amplifies the number of addresses, not dollar trading volume.

We did not find evidence of an independent large-scale wash trading system artificially creating dollar transaction amounts. The behavior in the data that appears to be “wash trading” mostly comes from retail-level market-making bots — these addresses place both buy and sell orders simultaneously to provide depth to the order book, rather than actively taking orders to generate transactions.

The real trading volume comes from identifiable order books. A considerable portion of top retail addresses carries Polymarket account identifiers, ENS domain names, or social graph labels; meanwhile, large crypto liquidity firms such as Jump Crypto, Selini Capital, Wintermute, and directional funds like Abraxas Capital also leave clear activity footprints. It is worth noting that these retail groups significantly overlap with Polymarket — both essentially serve the same type of “speculative preference” users.

The growth in address numbers is a typical behavior before a TGE, which is not surprising. However, this growth did not translate to dollar trading volume levels and did not change the core participant group structure that dominates trading.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。