Original|Odaily Planet Daily(@OdailyChina)

Author|Wenser(@wenser 2010 )

In the early hours of today, the Strategy Q1 2026 earnings conference call officially concluded, and Q1 earnings report was officially released. As a result, the true operational status of this "industry heart" holding 818,300 BTC is once again exposed to the market, with a net loss of 12.54 billion dollars driven by a BTC price that once fell to around 62,000 dollars, a continuous increase of 63,400 BTC, and an increase in STRC's scale to 8.5 billion dollars.

Of course, the most evocative part of the earnings report and Michael Saylor's statements is the indication that "Strategy may sell some BTC to pay dividends." Perhaps influenced by this news, despite Q1's performance falling short of market expectations, the capital market has shown optimism, with Strategy's stock price rising slightly by 3%.

Odaily Planet Daily specially summarizes the key points and potential prospects from the Q1 earnings report as follows.

Strategy's Q1 Digital Ledger: A net loss of 12.5 billion dollars on the books, the possibility of selling BTC to pay dividends cannot be ruled out

Key Point 1: Selling BTC is no longer impossible; it is an option

A closer look at the Q1 earnings report and conference call reveals that Strategy repeatedly mentions in its forward-looking statements and KPI descriptions—“If the convertible bonds mature or are redeemed without being converted into common stock, the company may need to sell common stock or Bitcoin to generate sufficient cash to meet these obligations.”

As of the end of Q1, Strategy's net long-term debt stood at 8.17 billion dollars, with a preferred stock redemption value of 10 billion dollars and cash of only 2.21 billion dollars. At the same time, the company must continue to pay preferred stock dividends (current STRC annual interest rate 11.5%) and has already begun issuing common stock to finance dividends. If BTC prices continue to be under pressure, leading to limited financing windows, the sale of coins to repay debts will shift from a theoretical assumption to a real possibility, which will inevitably have a ripple effect on the market.

Strategy's founder Michael Saylor stated, “This move is simply to convey a message to the market, indicating that this model (referring to the validation that Bitcoin assets can support shareholder returns within the corporate financial system) has been realized.”

It is worth mentioning that, unlike traditional companies' KPI metrics, Strategy has created its own KPI system, which includes: BPS (Bitcoin per share), BTC Yield (9.4%), BTC Gain (63,410), BTC$ Gain (BTC dollar earnings of 4.97 billion dollars) (Note by Odaily Planet Daily: The above data is as of May 3). However, in the disclaimer, it also points out that these metrics do not consider debts, do not account for the priority repayment rights of preferred stock, do not represent investment returns, do not represent fair value gains, and that “BTC dollar earnings may be positive while the company is recording huge fair value losses.” In fact, Strategy's Q1 business performance corroborated this mechanism: the KPI shows 4.97 billion dollars in BTC dollar earnings, but a GAAP basis recorded an unrealized loss of 14.46 billion dollars. This KPI system's core function is to maintain the narrative in the capital markets, rather than reflect the true financial situation. To put it directly, “celebrating at a funeral” or “framing the narrative positively while concealing the negatives” has become Strategy's common practice in the capital markets.

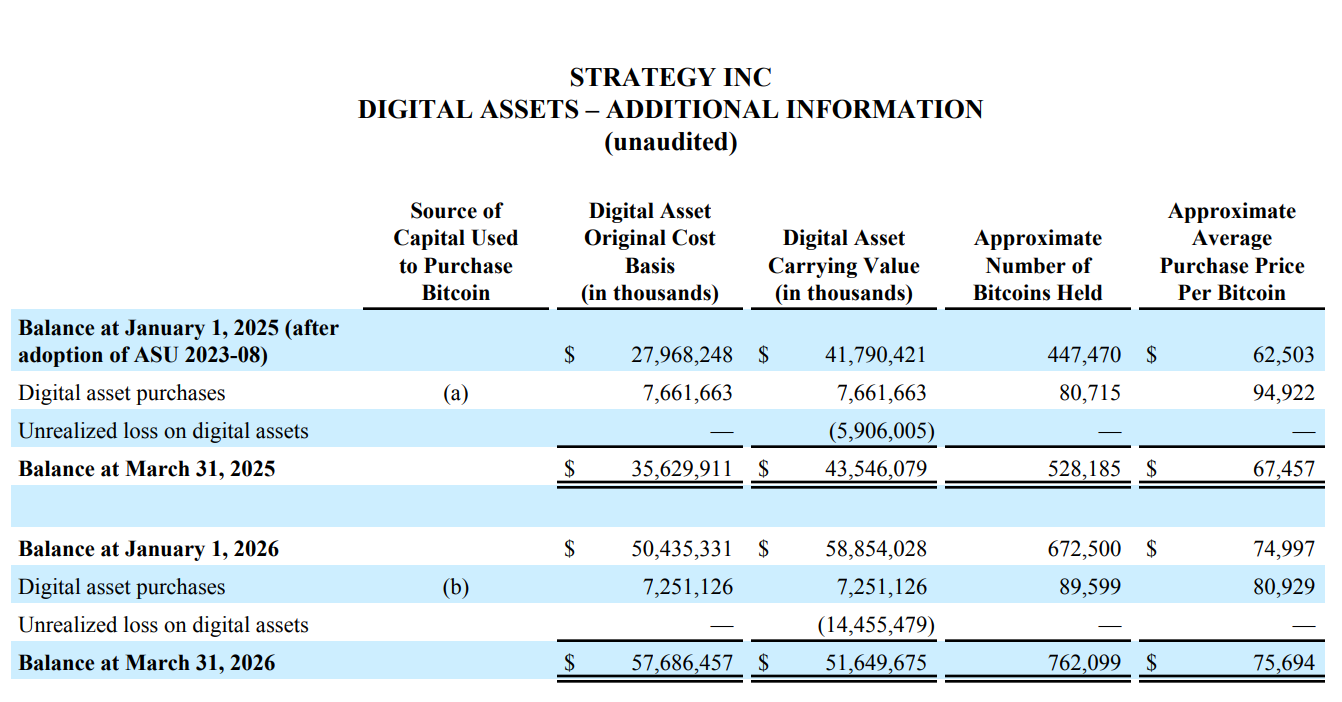

As of May 3, 2026, Strategy holds 818,334 Bitcoins, a 22% increase since the beginning of the year. However, the Q1 earnings report recorded a net loss of 12.54 billion dollars, almost entirely from unrealized losses on digital assets (14.46 billion dollars); the total cost basis for 818,334 BTC is 61.81 billion dollars, corresponding to an average purchase price of approximately 75,537 dollars per coin. It is worth mentioning that, thanks to a recent market rebound, the floating profit for Q2 amounts to 8.3 billion dollars.

Key Point 2: Spent 7.25 billion dollars to buy BTC in Q1, but BTC's quarter-end book value shrunk by 7.2 billion

Simply in terms of buying and selling figures, Strategy’s Q1 bill can roughly be summed up as “break-even.”

The earnings report shows that in Q1, Strategy purchased 89,599 BTC, costing 7.25 billion dollars, with an average price of about 80,929 dollars. However, due to the drop in BTC prices, the book value of digital assets decreased from 58.85 billion dollars at the beginning of the year to 51.65 billion dollars, netting a decrease of about 7.2 billion dollars.

One must say, in a bear market, continuously leveraging (financing + dividends) to bottom fish BTC, this result is already quite good.

Key Point 3: AI's impact on Strategy is objectively present, and software business income is completely marginalized

Nominally, Strategy still publicly claims to be an "AI-driven enterprise analysis software company," which is evident from its revenue structure, which includes software subscription service income, licensing income, product support income, etc.

However, in a structural comparison, Strategy's total software revenue in Q1 was only 124.3 million dollars, with a gross profit of only 83.35 million dollars; compared to the staggering 64.1 billion dollars in BTC holdings market value, the more than 500-fold quarterly revenue gap clearly tells the market: in the era of rapid AI development, software business even slightly related to AI has been completely marginalized.

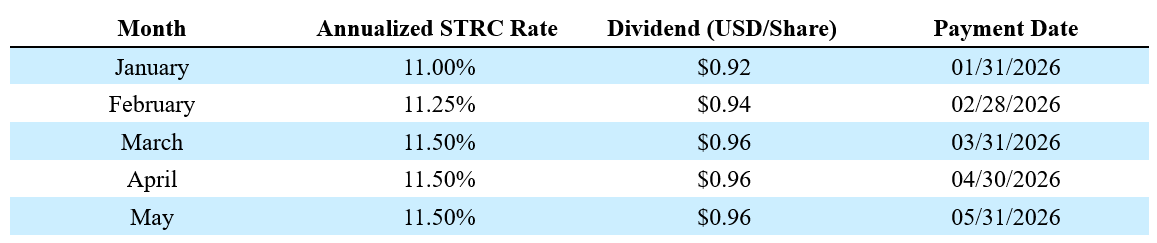

Key Point 4: STRC became the brightest business, with a market value of 8.5 billion dollars in 9 months

As Strategy's “financing tool,” STRC’s market performance in the ongoing bear market can be described as a “lifeline.”

Currently, STRC (Variable Rate Series A Perpetual Preferred Stock) has quickly grown to a scale of 8.5 billion dollars in just 9 months, becoming the largest preferred stock by market value in the world. Since the beginning of the year, Strategy has raised 5.58 billion dollars through STRC, a growth rate of 189%.

Additionally, Strategy stated that STRC's Sharpe ratio is 2.53, volatility is only 3%, and the average daily trading volume reaches 375 million dollars. This means that leveraging STRC, a low-volatility, high-yield, and high-liquidity fixed-income product, has created a new BTC reserve-backed asset in the traditional financial market.

Key Point 5: Major transformation in financing structure for Q1 and Q2, with STRC as the main financing force

In the earnings report, Strategy's Q1 financing completed at 7.37 billion dollars, with MSTR common stock ATM contributing 5.3 billion dollars and STRC contributing 2.07 billion, accounting for about 72% versus 28%; however, upon entering Q2 (from April 1 to May 3), this structure encountered a reversal—STRC contributed 3.51 billion dollars in financing, while MSTR contributed only 810 million dollars.

This means that the financing gap for common stock is getting smaller and smaller, and Strategy is increasingly relying on preferred stock to maintain its capital base to continue driving BTC accumulation.

Furthermore, perhaps considering STRC's impressive performance and strong capital attraction, Strategy is also promoting this “wealth management-type fixed-income product” in the traditional financial market; currently, the company has initiated a STRC semi-monthly dividend payment voting proposal, aiming to shorten the dividend payment cycle to attract more capital to participate in purchases.

Key Point 6: Strategy has first-time historical cumulative deficits in earnings

In the traditional financial market, retained earnings are an important indicator of a company's financial health, representing the cumulative net profit since the company's establishment minus all dividends. In other words, it is a company's “money bag.”

From its founding in 1989 until the end of 2025, after more than thirty years of operations, Strategy had a cumulative profit of 6.32 billion dollars; however, by the end of Q1 this year, this figure had turned from positive to negative, resulting in a cumulative deficit of 6.47 billion dollars.

This is a direct result of the ASU 2023-08 standard (Note by Odaily Planet Daily: This standard requires that starting in 2025, listed companies must measure BTC at fair value, with changes directly reflected in the profit and loss statement), but from the perspective of the commonly used GAAP in the traditional financial market, Strategy's historical cumulative profits accumulated over more than thirty years have been completely wiped out by one quarter's BTC decline.

Of course, with losses come gains; if BTC prices rise again in the future, this figure can still turn positive. This indicator also highlights the high risk and volatility of crypto assets compared to traditional financial assets.

Key Point 7: The STRC-centered DeFi ecosystem is under construction

Strategy's Q1 earnings report mentioned that DeFi protocols such as Apyx and Saturn absorbed over 270 million dollars of STRC assets; 150 million dollars of STRC assets were incorporated into corporate asset reserves by listed companies such as Prevalon, Strive, and Anchorage.

In other words, STRC is evolving from a single preferred stock financing tool into a foundational collateral asset for on-chain ecosystems in the cryptocurrency market. Should STRC's appeal to capital markets and crypto ecosystems continue to grow (Note by Odaily Planet Daily: Fixed income is quite attractive in both traditional financial and crypto markets), STRC will gradually surpass MSTR (traditional preferred stock).

Of course, with gains, there are also losses; the increased proportion of STRC raises the requirements for Strategy's dividend payment capabilities and broadens the impact range of market risk transmission.

Key Point 8: Tax deduction credits exist, but will not be utilized in the next 10 years

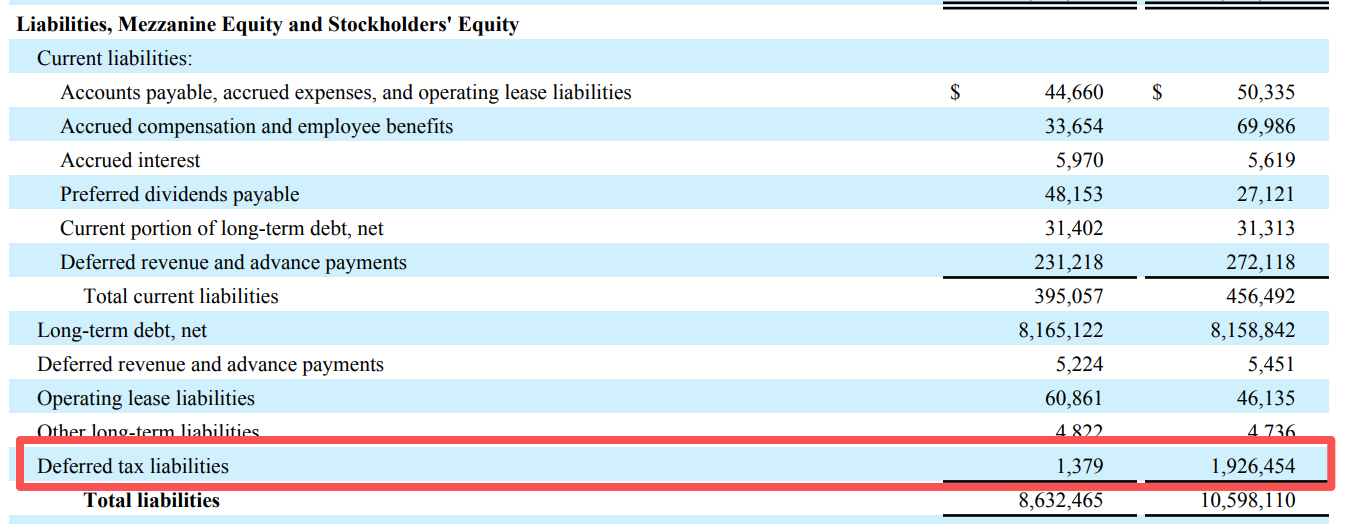

Aside from the business data information, Strategy's Q1 earnings report also mentioned drastic changes in deferred tax liabilities.

According to table data, Strategy's deferred tax liabilities plummeted from nearly 1.93 billion dollars at the beginning of the year to only 1.38 million dollars at the end of Q1, nearly zeroing out.

In other words, previously, Strategy had an “accrued tax” of nearly 1.93 billion dollars due to business profit floating gains, but due to business losses triggered by the drop in BTC, the company's asset profit and loss statement recorded this unpaid tax as “income tax benefit.” Additionally, Strategy's Q1 unrealized loss of 14.46 billion dollars theoretically will also offset some taxes, meaning that the company's tax obligations are reduced due to business losses, resulting in a “tax shield.”

However, the issue is that this tax shield, which can offset tax payments, is only valid when Strategy truly has taxable profits in the future; however, it has indicated that it does not expect to have taxable profits for over a decade. In other words, Strategy gained a “tax deduction benefit” of 1.9 billion dollars due to BTC's decline, but due to the absence of future taxable profits, it is highly probable that this benefit will not be enjoyed.

Finally, aside from purchasing stocks related to Strategy, betting events on whether “Strategy will sell Bitcoin before the end of the year” have gone live, and currently the probability of “yes” is reported at 44%.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。