Original author: Jared Mitovich, the Wall Street Journal

Translated by: Peggy, BlockBeats

Editor's note: AI trading is shifting from "model narratives" to "hardware bottlenecks".

In the past year, market discussions about AI have increasingly focused on large model companies, cloud vendor capital expenditures, and whether AI applications can truly generate revenue. However, the recent rise in U.S. stocks indicates that investors are re-evaluating the more fundamental and scarcer links in the AI infrastructure chain: storage, semiconductor manufacturing, and high-performance chip supply.

The surge in the storage chip sector essentially reflects that the AI industry has entered a more realistic stage of expansion. Training data, model parameters, inference loads, and data center expansions all require higher performance and greater capacity storage and computing hardware. For terminal technology giants like Apple, rising storage prices mean cost pressure; but for chip manufacturers like Micron, SanDisk, Intel, and Samsung, this marks the beginning of a new profit cycle.

It is noteworthy that the market is not solely optimistic. The Wells Fargo sentiment indicator triggered a "sell" signal for the first time since 2021, suggesting that the current market has shown certain signs of overheating. AI remains a main focus, but the issues investors are paying attention to are changing: it is no longer about who tells a grander AI story, but who truly grasps the supply bottlenecks and who can convert capital expenditures into revenue and profit.

Meanwhile, the situation in the Middle East, fluctuations in oil prices, and U.S. Federal Reserve interest rate expectations continue to disrupt the market. In other words, the new highs in U.S. stocks are not solely driven by AI enthusiasm, but rather a result of the buoyancy of AI infrastructure, a easing of geopolitical risks, and liquidity expectations working together.

The AI bull market is becoming more "physical." As computing power, storage, energy, and supply chains become the real constraints, the market now rewards not just those companies telling stories, but those manufacturers able to provide critical infrastructure.

The following is the original text:

John G Mabanglo / EPA / Shutterstock

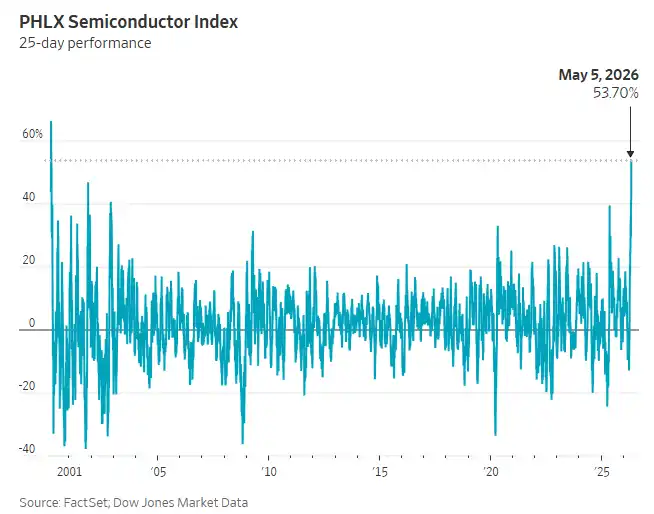

On Tuesday, investors flocked to the storage chip sector, driving the Nasdaq Composite Index and S&P 500 Index to new highs, further solidifying the best performance of the PHLX Semiconductor Index since the internet bubble.

Since the end of March, the semiconductor index has risen by 54%, marking the best performance in a 25 trading day span since March 2000. With the surge in demand for critical specialized chips for artificial intelligence, chip manufacturers are ramping up production to meet market demand.

Rising storage prices are increasing costs for tech giants like Apple, but on the whole, this poses a significant benefit for the entire chip manufacturing industry. Tuesday's gains pushed Intel's stock price up by 13%, increasing its market value to about $544 billion, surpassing Oracle and Johnson & Johnson. Stocks of SanDisk, Micron, and Qualcomm all rose by more than 10%, propelling the Nasdaq Composite Index, which has a higher weight in tech stocks, up by 1%.

Ohsung Kwon, Chief Equity Strategist at Wells Fargo Securities, stated that companies that design, produce, or sell computing chips needed for high-intensity AI tasks are the biggest beneficiaries of the current massive AI infrastructure build-out. "This is where the real bottleneck lies," he said.

Kwon indicated that AI trading has entered a healthier cycle: the emphasis for investors is shifting from capital expenditures to whether this technology can achieve commercial monetization. This shift in focus is also reflected in the financial reports of tech giants like Amazon and Google last week—traders were more concerned about whether these companies' massive investments in AI have truly translated into revenue.

Although the AI craze continues, Wells Fargo's sentiment indicator triggered a "sell" signal for the first time since November 2021. Kwon described the recent rise in financial markets as a "sugar rush" type of euphoria, a signal that investors should start to add protective measures to their portfolios.

Reports have indicated that Apple is considering having Intel and Samsung produce its main chips in the U.S., leading to optimistic sentiment among investors, thus pushing Intel's stock price higher. Samsung's stock also rose by about 5% in the South Korean market.

Among major U.S. stock indices, the Nasdaq led the gains, with the S&P 500 Index rising by 0.8% and the Dow Jones Industrial Average up by 0.7%, or 356 points. All 11 sectors of the S&P 500 rose on that day, with the materials and technology sectors leading; the small-cap Russell 2000 Index rose by 1.8%, reaching a historic high. The financial services sector opened lower, following job cuts announced by Coinbase and PayPal, but later recovered and ended essentially flat.

On Tuesday, hopes among investors increased that the U.S. and Iran could avoid the resumption of full-scale hostilities after Monday's Gulf of Persia conflict.

Recently, Brent crude oil futures fell by 4% to $109.87 per barrel. On Monday, after Iran attacked a key oil terminal in the UAE and vessels in the Strait of Hormuz, the most actively traded crude oil contract closed at its highest level in nearly four years. However, U.S. Defense Secretary Pete Hegseth downplayed the impacts of these attacks on Tuesday, stating that the ceasefire agreement reached with Tehran and in place for four weeks is still effective.

Bill Northey, Senior Investment Director at U.S. Bank Asset Management Group, stated: "At present, it seems that the situation has not materially escalated, and the market has thus breathed a sigh of relief."

He added that although hostilities in the Middle East appeared to have eased on Tuesday, this conflict continues to influence future U.S. economic data and the Fed's interest rate decisions. For instance, if the Strait of Hormuz can safely and fully reopen, it will weaken market expectations for higher inflation and push the yield on the 10-year U.S. Treasury bond lower.

Northey stated: "Our baseline judgment is that this volatility is likely to continue."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。