Written by: Long Yue

The burn rate of the AI arms race is outpacing the speed at which these tech giants earn money.

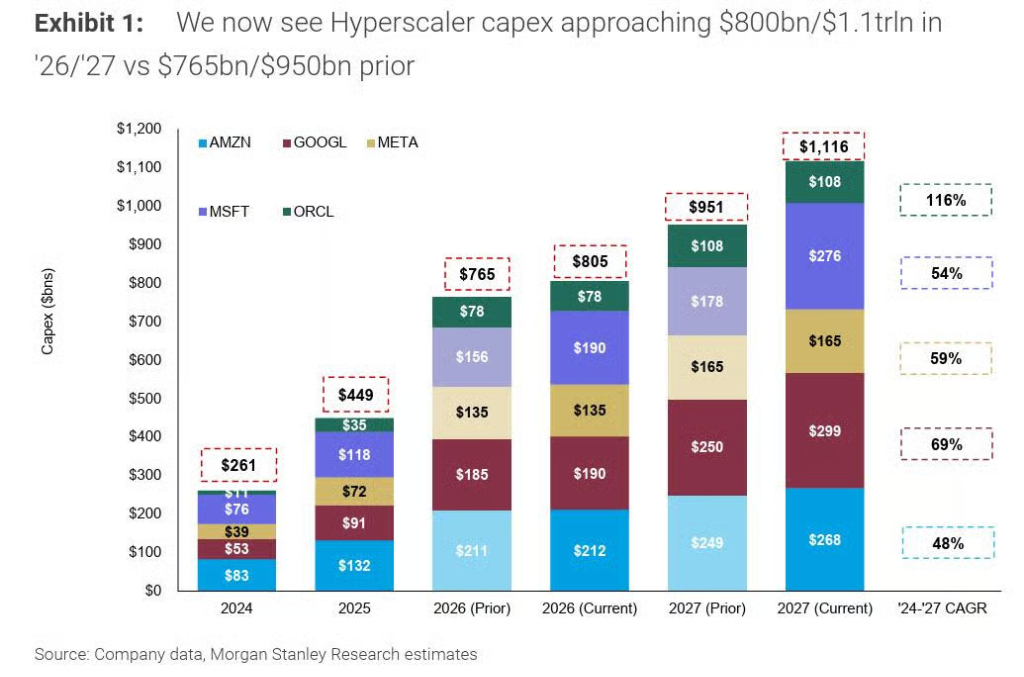

In the past week, five super-large tech companies—Amazon, Google, Meta, Microsoft, and Oracle (with a combined market value exceeding $12 trillion)—have successively released their first-quarter financial reports, all without exception raising their capital expenditure plans.

Andrew Sheets, Chief Cross-Asset Strategist at Morgan Stanley, promptly updated his forecasts, raising the combined capital expenditure forecast for the five tech giants to $800 billion for 2026, and further increasing it to over $1.1 trillion for 2027.

Sheets wrote:

We predict that capital expenditure for super-large tech companies will be about $800 billion in 2026, which is almost double the expenditure of 2025 and three times that of 2024. Next year, my colleagues estimate that capital expenditure for super-large tech companies in the U.S. could reach $1.1 trillion.

The numbers are astonishing, but questions arise as well.

Where is the money coming from? The answer is borrowing.

For many years, these tech giants accumulated a substantial amount of free cash flow through a "light asset" business model. However, the situation has quietly reversed.

Free cash flow data shows that both Amazon and Meta are close to or have fallen into negative territory.

What does this mean? Simply put: there is not enough money, and they can only borrow.

Especially since these companies need to maintain stock buybacks and dividends, the new capital expenditure can almost only be supported by issuing bonds.

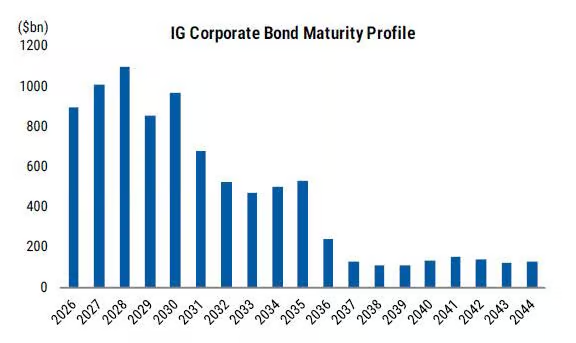

Morgan Stanley forecasts that 2026 will be the busiest year in history for the U.S. investment-grade (IG) bond market:

Total issuance is expected to be about $2.25 trillion, a year-on-year increase of 25%.

Net supply is about $1 trillion, a year-on-year increase of 57%.

Among them, the tech industry has contributed 18% to the U.S. investment-grade bond supply this year—this is the highest share ever for the industry and double that of the same period in 2025.

The core logic driving all of this is summarized by Morgan Stanley in four words: "AI capital expenditure driving supply."

The bond market is showing signs of fatigue.

The market is not oblivious.

After experiencing a $300 billion AI debt frenzy, investors are starting to show signs of fatigue.

The most straightforward example: Meta issued up to $25 billion in investment-grade bonds last week, with peak orders reaching about $96 billion. This number looks substantial, but compared to the $30 billion bond that the same issuer attracted $125 billion in demand for last October, it is clearly diminished.

More noteworthy details:

An issuer associated with SoftBank Group was forced to raise the issuance yield due to insufficient demand before completing financing.

Investors are beginning to demand stronger protective clauses—including backing from Google's parent company, Alphabet, which guarantees rent payments for data centers in case of tenant defaults.

Some investors have directly rejected certain transactions. One investor told Bloomberg that they walked away from an Oracle Michigan data center $14 billion bond due to, among other reasons, unfavorable redemption clauses for creditors.

Robert Tipp, Head of Global Bonds at PGIM Fixed Income, stated:

Ultimately, these companies are selling substantial amounts of debt, and they'll have to pay a higher price to borrow money. The market is facing a wall of concern after corporate spreads have narrowed significantly to historical lows.

John Servidea, Co-Head of the Global Investment-Grade Debt Capital Markets at JPMorgan, said:

We are seeing varying priorities among different investors regarding these financings, and how they assess risk and return. We see fairly strong demand for these transactions, but as supply increases, we expect transaction terms and structures to continue to evolve.

Banks "can barely hold on."

The fatigue in the bond market is just the tip of the iceberg. Deeper pressures are building within the banking system.

According to a report from the Financial Times on May 3, major lenders like JPMorgan, Morgan Stanley, and Sumitomo Mitsui Trust Bank (SMBC) are actively seeking ways to spread the risks of debt related to data centers to a broader range of investors, in order to free up balance sheet space.

Matthew Moniot, Co-Head of Credit Risk Sharing at Man Group, bluntly stated:

The scale we are talking about... far exceeds anything we've ever imagined. Banks are about to become overwhelmed.

A specific case illustrates the severity of the issue: Banks like JPMorgan and MUFG spent over six months trying to distribute a $38 billion construction debt associated with Oracle's Texas and Wisconsin data center projects. The result was—insufficient demand, forcing some banks to sell at a discount, offloading these loans to non-bank lenders.

$38 billion, a single project, unable to sell in six months.

This is driven by hard constraints on banks' internal risk limits—once the exposure to a single borrower or industry reaches its cap, banks cannot finance new projects.

Moniot said:

If I were the Chief Risk Officer of a bank, facing credit requests worth billions for a single project from bankers, I would question how they plan to distribute those risks.

To address this issue, banks are starting to explore "Significant Risk Transfer" (SRT) tools—slicing concentrated loans for data centers and transferring the riskiest parts off the balance sheet, selling them to private credit funds, insurance companies, and other investors.

David Lucking, a lawyer at Linklaters, stated:

Banks typically still retain a certain percentage of exposure. SRT investors want to confirm that the banks still have some interest aligned.

Frank Benhamou, Portfolio Manager at Cheyne Capital, pointed out that SRTs related to data centers are fundamentally different from traditional products:

The number of operators is limited, extremely concentrated, and there are significant construction risks. Naturally, you would demand a higher return for this.

Goldman Sachs warns: the investment-grade bond market is becoming "equity-like."

This AI debt wave is also changing the structure of the entire investment-grade bond market.

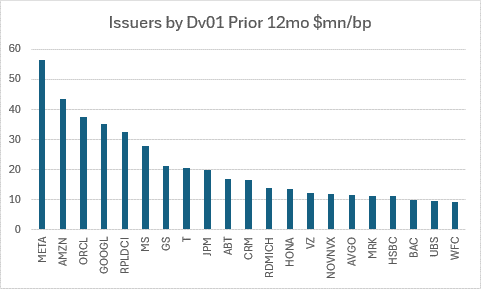

Goldman Sachs investment-grade bond strategist Amanda Lynam pointed out that since 2026, the issuance volume of U.S. investment-grade bonds has reached the strongest start in historical same-period comparison—with issuance amounting to $794 billion as of April 20, annualized to align closely with Morgan Stanley's forecast of $2.25 trillion for the year.

However, what is more noteworthy is the structural change.

Jeffrey Papai, a Goldman Sachs investment-grade bond trader, wrote in a recent report that among the 660 issuers that issued investment-grade bonds in the past year, only 11 accounted for around 25% of the duration-adjusted issuance. Among them, four super-large tech companies (Meta, Amazon, Oracle, Google) and four large data center financings accounted for nearly 20% of the total duration-weighted issuance.

A comparison highlights how extreme this is: Oracle (ORCL) is now the largest single issuer in the investment-grade index in terms of risk-adjusted size; Meta has jumped from the 51st largest issuer in the investment-grade index to the 8th largest in under a year.

Last week, Meta's single $25 billion bond, or the largest single data center financing transaction (RPLDCI), had a duration-weighted size close to the total amount of Boeing's (BA) outstanding bonds, even exceeding the total of Ford's (F) or General Motors' (GM) outstanding bonds combined.

Goldman Sachs therefore issued a warning:

"What we are facing now is an increasingly concentrated market heavily tilted towards AI construction, resembling the stock market but presented in a way that is more negatively convex—because fixed income has no inherent upside."

In other words: betting on AI stocks can result in profits when they rise; betting on AI bonds can provide interest, but if issues arise, the losses are tangible.

When money is tight, borrow globally.

Faced with the capacity limits of the U.S. investment-grade bond market (where a single issuer usually does not exceed 2-3% of the market), tech giants have begun to seek financing from global markets.

Goldman Sachs data shows that since 2024, the issuance of Euro, Pound, and Swiss Franc-denominated bonds by super-large tech companies has significantly increased.

At the time of this article's deadline, Alphabet, Google's parent company, had just launched an issuance of at least €9 billion in Euro-denominated bonds, while also starting a Canadian dollar bond sale—both setting new records in their respective markets.

Meta has taken a different path: by establishing off-balance-sheet special purpose vehicles (SPVs) to distribute debt pressure. After completing the $27 billion "Beignet project" to finance a Louisiana data center last year in collaboration with Blue Owl, Meta is working with Morgan Stanley and JPMorgan to advance the $13 billion "Sopaipilla project" to finance its data center in El Paso, Texas.

The essence of this structure is to spread the debt as widely as possible among more parties.

Morgan Stanley: When will the AI bubble burst? Watch for these four signals.

As the entire AI super cycle increasingly depends on the smooth operation of the debt market, Morgan Stanley has listed four potential warning signals that could trigger a surge in credit spreads, leading to the collapse of the AI "house of cards":

Debt growth exceeding profit growth

Leverage in the financing market growing faster than high-quality credit

Merger and acquisition activity exceeding long-term trend levels

Acceleration of private equity-supported transactions and a decline in equity contribution ratios

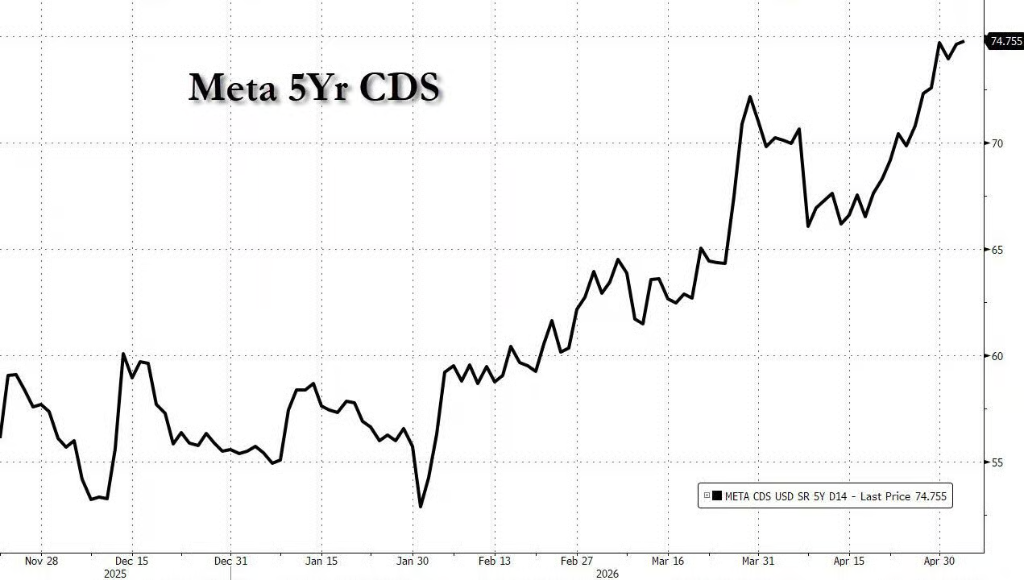

Another more intuitive market signal worth noting: On the same day that U.S. stocks closed at historic highs with many of the "Tech Seven" stocks surging, the credit default swap (CDS) spread for Meta hit a historical high and has been widening daily.

Record high stock prices and record high CDS spreads occurring simultaneously is itself a signal that warrants deep reflection.

Morgan Stanley concluded with a concise but weighty statement:

The credit market is providing financing for AI construction.

The implication is: once the credit market shuts down, the AI super cycle comes to an end.

This article does not constitute personal investment advice, does not represent the opinions of the platform, and the market carries risks. Investment should be approached with caution; please make independent judgments and decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。