Written by: Glendon, Techub News

In the early hours of today, Coinbase released its financial report for the first quarter of 2026. The figures are not impressive: the net loss reached $394 million, significantly reversing the profit of $66 million from the same period last year; total revenue was $1.41 billion, down 31% year on year; trading revenue was $756 million, plummeting 40% year on year. It is worth emphasizing that this marks the second consecutive quarter of net losses for Coinbase, as the previous quarter saw a net loss of as much as $667 million.

Ironically, just three days before this report was released, Coinbase CEO Brian Armstrong announced a 14% layoff, affecting around 700 positions on Twitter, claiming it was due to "AI changing the way businesses operate." This news had briefly propelled Coinbase's stock price up about 4% to $207—Wall Street liked the "AI narrative." However, once the financial report was released, the stock fell 4.38% to $184.5 in after-hours trading, down nearly 18% year to date. The turbulence reflected in just a few days of trading perhaps already illustrated the market's complex attitude toward this financial report.

Where Do Coinbase's Losses Come From?

Looking at the revenue structure, the answer to the question is clear. In the first quarter of 2026, the cryptocurrency market was dominated by risk-averse sentiments. The main reason is that the prices of mainstream assets like Bitcoin and Ethereum were under pressure, and the trading enthusiasm for long-tail tokens declined, leading to a more than 20% quarter-on-quarter drop in total spot trading volume across the industry. Consequently, trading fees, the core source of revenue for exchanges, naturally took the hardest hit.

According to the financial report, Coinbase recorded trading revenue of $756 million for the quarter, a 40% year-on-year decline. Of this, consumer trading revenue was $567 million, down 23% quarter-on-quarter, directly dragging down the overall revenue performance. Institutional trading revenue was $136 million, also under pressure, but a highlight was hidden in the corner: the derivatives business. Coinbase acquired Deribit last August for about $2.9 billion; this quarter, Deribit contributed about $68.5 million in incremental revenue, making this business's revenue grow 37% year on year.

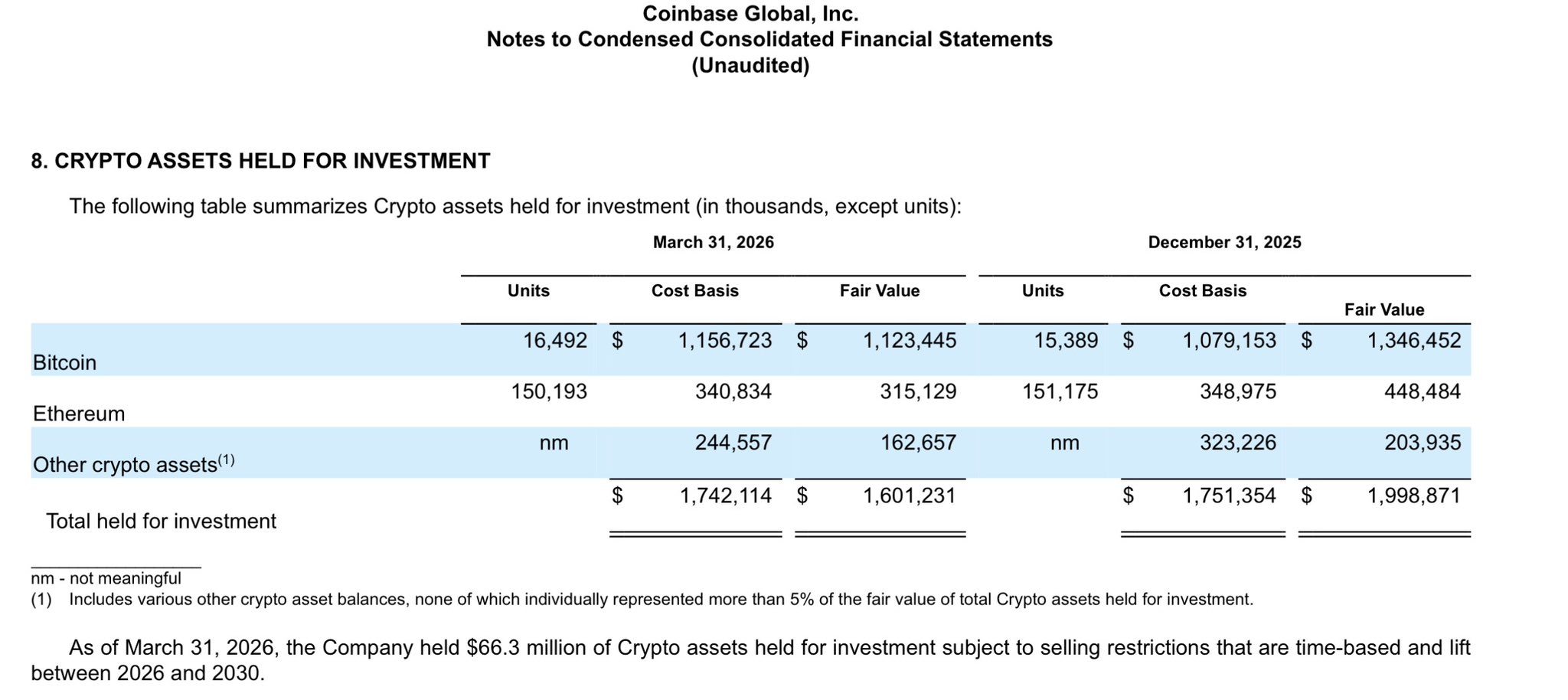

Another factor not to be overlooked comes from the asset and liability side. Looking at the balance sheet, Coinbase held 16,492 Bitcoins, an increase of 1,103 coins from the previous quarter; Ethereum was reduced by 982 coins, leaving about 150,000. Against the backdrop of an overall decline in cryptocurrency prices, these holdings' fair value changes are directly accounted for in the profit and loss, resulting in a massive book loss of approximately $482 million.

It is important to emphasize that this is a non-cash accounting loss. In other words, as long as Coinbase does not actually sell at a low point, the losses will not translate into real cash flow losses. This "paper loss" can turn into "paper profits" during a bull market; for instance, in Q4 2025, investment gains from digital assets reached as high as $718 million. However, when cycles turn, it becomes the most eye-catching item on the profit and loss statement.

This inevitably brings to mind an old question: when an exchange deeply binds its fate to asset prices, is it a platform or a "gambler"? The choices made by Coinbase and most companies in the cryptocurrency industry are to be both, using profits from the platform to buy assets, then letting asset volatility bite back into platform profits. However, this cycle works as an amplifier in a bull market but becomes a meat grinder in a bear market.

In summary, the significant decline in trading income is the primary reason for the overall revenue contraction of the company. However, Coinbase stated that this structural change is not entirely attributed to short-term fluctuations; it is also the result of its proactive strategy to "reduce reliance on trading."

Armstrong has continuously emphasized the "everything exchange" strategy: expanding from spot trading to derivatives, commodities, futures, and prediction markets. Today, Armstrong also stated on X that the company is moving away from dependence on spot trading towards a broader multi-asset platform. He noted that Coinbase is transforming from a "crypto platform focused on spot trading" to a platform where users can trade a wider range of asset classes, including derivatives, commodities, futures, and prediction market event contracts.

However, this raises an unavoidable question: when the core spot trading income is halved, can an emerging derivatives business support half the burden?

The answer is clearly no. The proportion of trading income to total revenue has decreased from over 60% in the bull market to 53% this quarter, but this is more a passive decline rather than a victory of active transformation. Armstrong stated in a tweet: "Despite the decline in the cryptocurrency market, the fundamentals of the on-chain economy continue to grow strongly." While this statement sounds good in a tweet, it appears somewhat pale in front of the profit and loss statement.

Stablecoin Business and the Impending "Reef"

It is noteworthy that on the other side of weak trading income, the subscription and services revenue segment shows remarkable resilience. This quarter, this segment generated revenue of $584 million, although it still fell 14% year on year, this decline is much smaller than that of trading income, and its share of net income peaked at 44%, a historical high. This seems to indicate that even when market trading is at a standstill, Coinbase can still secure stable recurring revenue through its existing users and infrastructure services.

Within this segment, revenue related to stablecoins (mainly from interest income distribution on USDC) reached $305 million, an 11% year-on-year increase, making it the only core revenue item that achieved positive year-on-year growth. This success is attributed to several key factors, including USDC's market cap reaching a historical high of around $80 billion in this quarter, Coinbase's platform hosting about 25% of the circulating USDC, and over 90% of on-chain proxy stablecoin trading volume concentrated on Coinbase.

Additionally, blockchain rewards revenue (mainly from staking services) was $101 million, basically stable; benefiting from historically high average loan balances, interest and financing expenses revenue reached $68 million, up 13% quarter-on-quarter. Meanwhile, the user count and penetration rate of the subscription product Coinbase One are also steadily increasing. The common characteristic of these non-trading revenues is their insensitivity to short-term market fluctuations, depending more on the existing asset stocks and user retention on the platform.

However, a "reef" impacting Coinbase's core business in this segment is emerging.

Currently, the latest progress of the CLARITY Act prohibits users from passively earning interest on stablecoins but retains space for active rewards, allowing issuers or platforms to design reward mechanisms based on users' real activities (like trading, payments, transfers, staking, etc.).

While Coinbase has reached an agreement on crucial stablecoin revenue clauses, once the compromise becomes law, users will no longer be able to earn returns similar to deposit interest simply by holding stablecoins. This means that the logic for growth of its stablecoin business revenue must shift from "generating interest from existing holdings" to "earning incentives through frequent use of the currency," and it also indicates that Coinbase must accelerate the transformation of its current profit model, focusing on providing more value-added services linked to actual usage.

For Coinbase, this represents the most direct income pain. We cannot help but wonder, when the act is implemented, can its stablecoin business revenue maintain positive year-on-year growth? The answer to this question will depend on whether Coinbase can design a system of incentives within a compliance framework that gets users to "move."

Interestingly, the above information is just one side of the coin. In the financial report, after excluding non-operational items including losses from cryptocurrency holdings, equity incentive expenses, depreciation, and amortization, its adjusted EBITDA was $303 million, showing a positive value for the 13th consecutive quarter. This data indicates that, notwithstanding the severe volatility of cryptocurrency prices, Coinbase's core business profitability remains intact.

This is clearly a love-hate indicator. Those who love it say: Coinbase's core business is still making money, cash flow is not a problem. Those who hate it, however, argue: a book loss of $482 million is simply "adjusted" away, so what significance does the net profit have?

In fact, the "scissors gap" between income and losses is the tension that cannot be avoided when interpreting this financial report. On one hand, trading income has dramatically declined, leading to a net loss of $394 million; on the other hand, adjusted profits are positive, cash flow is robust, and cash and cash equivalents exceed $10 billion. Both narratives simultaneously exist and pull against each other, making it difficult for investors to simply label it as "good" or "bad."

As for how investors should approach this contradiction, which narrative should they trust?

Perhaps this is not an either-or choice, but rather a matter of perspective. The GAAP net profit loss is an "fact" that cannot be avoided under accounting rules, while the positive adjusted EBITDA is not entirely a "cover-up," but rather the "core" that Coinbase's management wants you to see: after excluding what they consider to be "noise," the company's core business remains viable.

Coinbase takes confidence in its cash reserves exceeding $10 billion; even if trading income remains sluggish, it can endure a long bear market and wait for the next cycle.

Conclusion

Looking back, Coinbase's first-quarter financial report is merely a snapshot of the cyclical cleanup within the crypto industry.

Beneath the surface of the net loss of $394 million is a structural story of trading income naturally receding with the market, passive impairment of digital asset holdings, and the maturation of non-trading revenues. The crypto industry cannot escape the fate of cyclical volatility; however, from a positive perspective, Coinbase is attempting to evolve from a "bull market amplifier" into a more resilient financial infrastructure platform.

According to Coinbase's disclosures, its market share of cryptocurrency trading volume has reached a historical high, with total assets on the platform amounting to $294 billion, achieving a net native unit net inflow for the 12th consecutive quarter. In new areas such as derivatives, prediction markets, and DEX, Coinbase is showing particularly strong growth: prediction market products surpassed $100 million in annualized revenue in March, and DEX trading volume doubled quarter-on-quarter. Currently, 12 products have achieved annualized revenues exceeding $100 million, and business diversification is starting to show results.

It is evident that over $10 billion in cash reserves, 13 consecutive quarters of positive adjusted EBITDA, and the counter-cyclical growth of stablecoin revenue indeed paint the picture of a company that remains steady during the crypto winter. However, financial reports and various metrics do not fully represent the company's true health status and inherent risks.

When the narrative of becoming an "everything exchange" is still underway, and the passive income model is also hindered by regulations, whether Coinbase's resilience is genuine skill or merely the result of a solid foundation is unclear. The difference between those projects that failed due to funding break and user exits and Coinbase may not be strategic vision but rather a balance sheet that reads $10 billion. This is very realistic and harsh, but at least it allows Coinbase to survive until the next spring. As for whether Coinbase can outpace its competitors when spring arrives, that is the story of another financial report.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。