Author: Yuan Chuan Investment Review

When the number of people chatting in an investment group decreases, just throw out a value curve chart of Wu Yuefeng, and the atmosphere can instantly become lively.

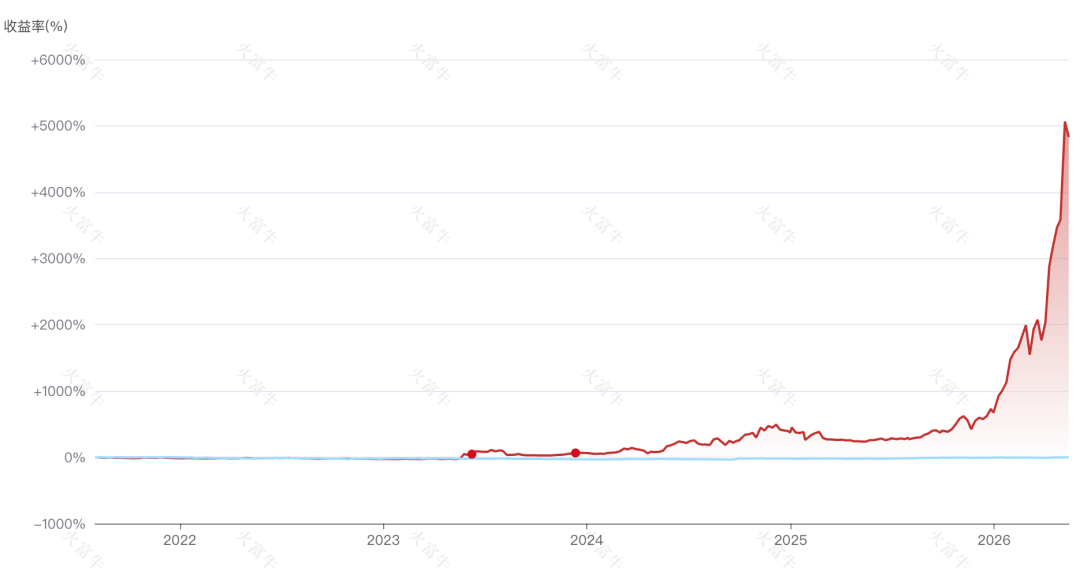

This time, the net value of Jiayue Yuefeng Investment Genesis has not only returned to the surface but has also set a historical high. Last year, Wu Yuefeng managed to bring the net value back to over 30 cents, thinking that he had climbed out of the abyss, but soon it fell back to over 50 cents. Until May 8 of this year, the net value has risen 167.54% in nearly a month, and Wu Yuefeng is back.

From the product report position, the total equity position has reached 100%, with 35% in AI computing power infrastructure + 20% in storage chips, which constitutes the main driving force behind the surge in net value. AH stock optical modules and PCBs account for 5%, and Wu Yuefeng has almost all bets on the AI computing power industry chain [1].

In the past year, as long as one slightly changes their thinking to chase light communication and storage, rather than defending in liquor stocks, it doesn't matter how poorly one has performed before or how big the pit they dug, it can all be filled in one go. Standing in the light and close to the core is the biggest wealth code of this year.

Yuan Lesheng, Hiva, and Quishi, these subjective funds that were at their peak between 2020-2021, have seen their product net values explode in the past year, breaking historical highs. Teacher Fu from Ruiyuan has quietly doubled in the past year, setting a new historical high for net value. A private placement product named Zhun Jin Zhi Zhan No. 1 is even more exaggerated, multiplying by 5 times this year, and has increased by 50 times in less than 5 years since its establishment.

What is Thunder Value

There is also the rumor that the Yao Jinghe private equity fund has made astronomical numbers relying on storage and CPO, increasing its hedge fund scale from $225 million to $5.5 billion by the former OpenAI employee Leopold, and Hefei State-owned Assets is poised to regain the title of "Best Venture Capital" as Changxin goes public. It seems that everywhere are people in the "Chip Light Lithium" making money, while those who aren’t can only watch as the value continuously rises, anxiously observing the various Thunder Values to the point of frontal lobe damage.

At this time, the people standing in Hengkai and value stocks can’t help but have a question in mind: How can the KTV girls in Shanghai make 18 million, and the market hasn't cut high or low yet?

Silicon Bull, Carbon Bear

One bizarre aspect of this round of market is that the AI industry chain, no matter how crowded it becomes, cannot drop.

In the first quarter of this year, the allocation ratio of active equity funds to AI hardware was 31.5%, with an overweight ratio of 17.7%. Compared to the historical core tracks, while not exceeding the year of the Mao index, it has surpassed the peak of the Ning combination [2].

Liu Chenming from GF also pointed out that last year the TMT holdings of funds exceeded 40%, and electronic holdings have been over 20% for more than a year, with A-share TMT trading volume exceeding the 40% threshold of the previous industrial cycle.

Despite this crowding, since April, the Philadelphia Semiconductor Index has risen 54%, and the Science and Technology Chip Index has risen 60%. Not to mention Teacher Fu, who heavily invested in Zhongji Xuchuang in the first quarter, even 18 firms that bought semiconductor positions exceeding 10% of fixed income+ have also pulled off a wave of Thunder Values.

Another bizarre aspect of this round of market is that no matter how much Hengkai falls, it still cannot be revived.

It has been two months since Xia Junjie said "Hengkai may have fallen too far," and Hengkai still shows no signs of improvement, like a dead fish lying flat on the ice in a seafood stall.

The weakness of Hengkai has its inevitable reasons, just as Liu Xiaolong from Juming responded to why he cleared out Hong Kong tech stocks: 1) The potential impact of AI on internet business models; 2) The Hong Kong market is more affected by overseas liquidity tightening; 3) A large amount of capital raised in IPOs is being consumed over 25 years.

In the end, the current large models still reflect a winner-takes-all scenario and long-tail homogeneous competition. Hongshang Asset believes that in the C-end “free” and “low price” internal competition has led to the valuation dilemma of Chinese AI companies:

When the monetization ability is highly doubted, even Tencent and Alibaba’s AI businesses find it hard to gain recognition from the capital market. Although Alibaba's Qianwen and others started trying a closed-source paid model, the results have not been good. This is also why the market has gradually lost patience with Tencent and Alibaba’s AI stories recently, which is the core reason for their lack of valuation expansion momentum.

The most bizarre part of this round of market is that consumer fund managers have begun to transform to chase the light.

Not long ago, I wanted to bottom fish in consumer funds, feeling that the "Bosera Female Consumption Theme" name was very appetizing, only to find upon opening the top ten holdings that it was flooded with Crystal Optoelectronics and Zhongji Xuchuang.

Well-known consumer master's Tong Xun and Xiao Nan are also gradually synchronizing with light. After changing their thinking, Teacher Tong has seen a V-shaped reversal in net value since April; after the third quarter of last year, Xiao Nan's management of E-fund Ruiheng’s light holding has gradually increased, leading to an ever-growing performance gap with Zhang Kun, who is deep in the liquor quagmire along with peers.

These bizarre phenomena remind people of the peak of the last round of subjective bullishness from 2020 to 2021.

Only back then, the protagonists had muscle memory of "monopoly barrier + perpetual operation," relatively over focused on Kweichow Moutai and Alibaba, the fund managers of the 60s; while this round's protagonists have become those born after the 85s, who have an extreme faith in hard technology, relatively over focused on Zhongji Xuchuang and Cambrian, most of whom faced the market for the first time at 4200 points.

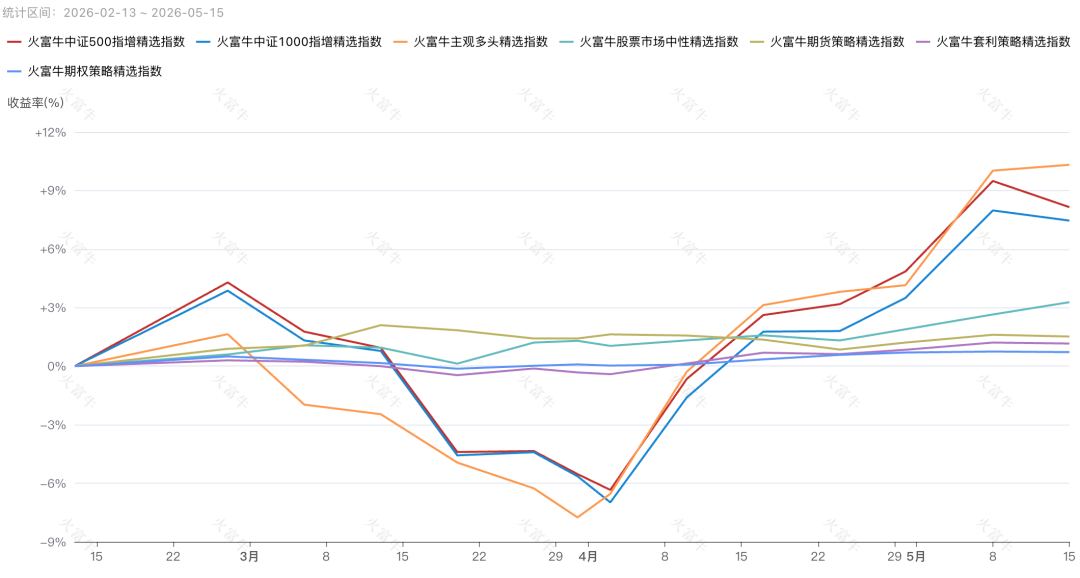

If it weren't for AI, the long-suffering subjective bulls suppressed for years wouldn't have been able to stand tall. In the past year, 12 subjective long-biased products of public funds have seen yields exceeding 300%; and in the past three months, Huo Fu Niu’s private subjective long-biased selected index has surpassed the CSI 500 Index, becoming the strongest strategy index.

Ren Zeping said this is a once-in-a-decade bull market, attributed to a combination of policy bull + tech bull + liquidity bull. I think a more accurate expression is that those who have confidence in silicon are in a bull market, and those who are attempting to bottom feed carbon are in a bear market.

Attack or Defense

For many fund managers, the current situation is like Flick leading this poor Barcelona team, seemingly without any other choice.

Flick's tactic is to replace defense with offense, maintaining ball control in the opponent's half to lower the chances of the opponent facing his own goal. Once he withdraws and sits in defense, relying on Barcelona's weak defense will only lead to worse losses. The same logic applies; even sitting defensively in Hengkai and consumption, if the bull market ends, they will still drop, but at least attacking by buying AI can accumulate profit cushions.

Moreover, under the extremely FOMO emotion, managing the emotions on the liability side is increasingly difficult. After all, customers can easily make money trading stocks themselves chasing the light; looking at friends buying subjective stocks that are all Thunder Values, why should they spend time and management fees listening to you speak about value investing, and then miss out on the few epoch-making trains of their lives?

Since it's a fast-moving train of the era, should those who are not on board chase after it? And should those onboard get off? These are the questions every manager must face. Just like the five giants of American technology have adjusted their capital expenditures to $720 billion, no one wants to be left behind by the times.

Wang Zhongyuan, the founder of Zhi Rui Xing Investment, who entered the industry in 1993, personally experienced the "327" national debt incident in 1995 and witnessed the internet bubble in 1999. He shared a real story with Yuan Chuan:

Stanley Druckenmiller shorted tech stocks in the first half of 1999, heavily returned to long positions at the end of the year, and liquidated to escape the peak in January 2000. But by March 2000, as technology soared again, he couldn't resist and went all in, resulting in an 18% loss in a month and a half.

"What does this story illustrate? Even the world’s most recognized top trader can make irrational decisions when facing FOMO emotions. So, how many of today’s fund managers chasing light are better than Druckenmiller?"

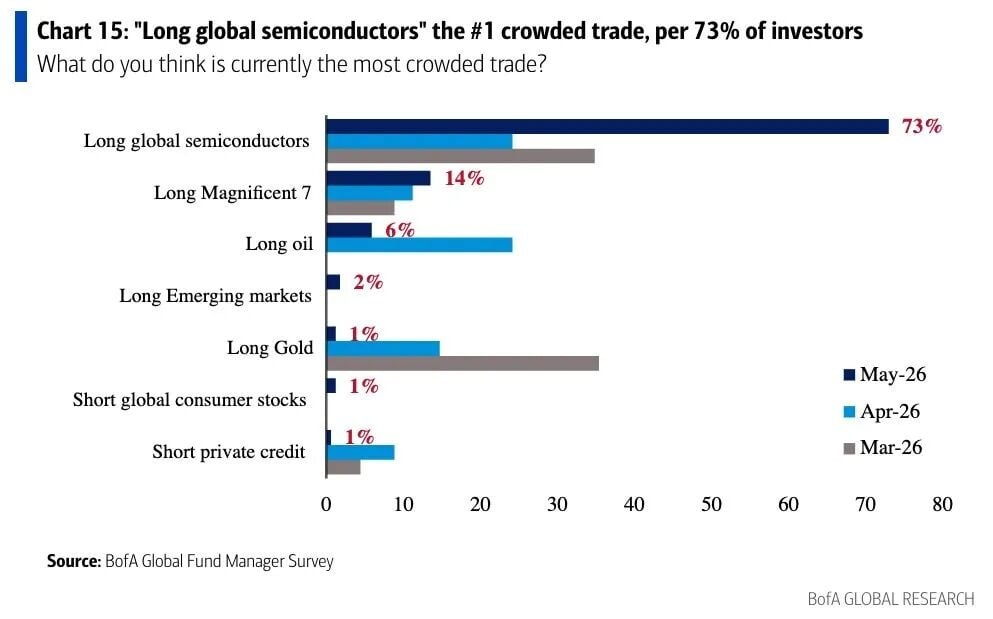

Interestingly, Zeyuan Investment recently posted a picture on their public account—“Semiconductors topped the global trading leaderboard in May.”

They suggest that investors lower their expectations of Zeyuan, which is currently similar to the peak of tech stock bubbles, and absolutely will not change their traditional value investment strategies to chase the tech stock bubble, no matter how fervently the bubble becomes, they will “never surrender.” They quoted a saying, “The stock market is a place where dreams and money exchange, those who sell dreams extract money, while those who spend money are often stuck hoping to regain their dreams in the stock market.”

Compared to Zhi Rui Xing and Zeyuan, Jing Yi Investment expressed it more straightforwardly—this AI revolution's underlying large models and the most critical infrastructure and hardware are mostly in the hands of those leading American tech giants across the ocean. The fundamental support for the current A-share AI speculation is far less than that of the past new energy.

“In 2021, the photovoltaic and lithium battery sectors saw most companies exploding with real performance and rapid penetration, while today, many so-called 'AI companies' in A-shares that are being hyped to a market value of several hundred billion haven’t even achieved the profit explosion moment that new energy experienced back then.”

Undeniably, some subjective private placements are not gambling; they withstood last year's short attacks from Michael Burry's $379 subscription articles and captured that the core storyline of AI investment is AI hardware. However, as the speculation has spread from optical modules to storage, CPUs, electronic fabrics, fibers, and other segments, the room for high-low cuts within the sector is constantly narrowing, and the potential costs of making mistakes are rising.

Moreover, with 30-year U.S. Treasury yields breaking 5%, chasing AI now is under a different macro scene compared to when Michael Burry shouted bubble last year.

It’s like Flick's Barcelona—having a smooth sailing season, occasionally racking up thunderous scores. Until meeting Atletico Madrid, who excel in counterattacks during the Champions League quarterfinals, stubbornly insisting on high-level attacks led to defenders frequently chasing back and getting two red cards, completely ruining the game.

Epilogue

When people still believe in carbon, Thunder Values haven't been absent.

In the last round of the liquor bull market, from 2020 to June 2021, Lin Yuan's performance increased by 150%, then oscillated downwards for five years, leaving only over 20% gains now. Back then, the concentration on photovoltaic new energy of Zhengyuan and Chongji is now a memory that financial planners are reluctant to revisit.

Moreover, like pulling off Thunder Values before, the peak scale of 30 billion Shifeng assets attempts to transform quant but couldn't reverse the decline, now shrinking to 2-5 billion, and has recently learned that it has moved from Lujiazui Century Financial Plaza to a more affordable rental in Yuanshen Financial Building.

These may seem somewhat distant, but when gold prices peaked at the beginning of the year, that private equity fund that shouted “hold on tight” three times is probably not easily forgotten.

I sometimes ask people in the industry why they are optimistic about a certain private equity fund, and the answers usually consist of three points: Big tech employees starting their own businesses, the strategy still being effective despite the small scale, and the most crucial factor—good-looking net value curve.

Behind Thunder Values often lies the amplified gains brought by concentrated positions and even leverage. Simply using performance sharpness as a buying criterion, you are likely to buy an ordinary product that represents merely past strong market styles. The lesson of buying on the line to drop has repeated itself over and over.

Qin Yuan’s Wu Dingwen once shared: “Allocation requires recognition of the underlying logic, that is, recognizing the trade, recognizing value, recognizing the team, rather than just recognizing making money.” Simply recognizing making money will likely fall into the cycle of buying whatever is hot, where whatever is bought drops, and where losses occur repeatedly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。