Let's talk about the pits buried last time and discuss the AI liquid cooling sector! 🧐

In the liquid cooling sector, I personally hold #VRT, which should be the undisputed leader. Recently, I have also been looking for some smaller market cap companies that belong to the core supply chain. I am currently zeroing in on one, and everyone can discuss in the comments section.

The logic behind liquid cooling is very simple, as described in the video. The power density of data centers is already at its peak, with the upcoming Nvidia Vera Rubin Ultra VR200 directly hitting 600 kilowatts per cabinet, and only liquid cooling can handle that. One cabinet can cost as much as 7.8 million US dollars, so liquid cooling must work with reliable big names, not just any player.

🎯 Explosive market growth

Although liquid cooling may not be as glamorous as memory chips and optical modules, the overall growth momentum cannot be ignored, and due to the high concentration of enterprises, there is a certain monopolistic pricing advantage!

According to the latest data from the authoritative industry agency Dell'Oro Group, the global liquid cooling market size for data centers is expected to soar from approximately 3 billion dollars in 2025 to 27.65 billion dollars by 2033, with a compound annual growth rate as high as 31.5%.

The core driver of this growth is the explosive capital expenditure of hyperscale cloud service providers on AI infrastructure. Goldman Sachs predicts that from 2025 to 2027, the total CapEx of the four major hyperscale firms worldwide will reach 1.15 trillion US dollars, with about 75% directly allocated to AI-related physical infrastructure construction.

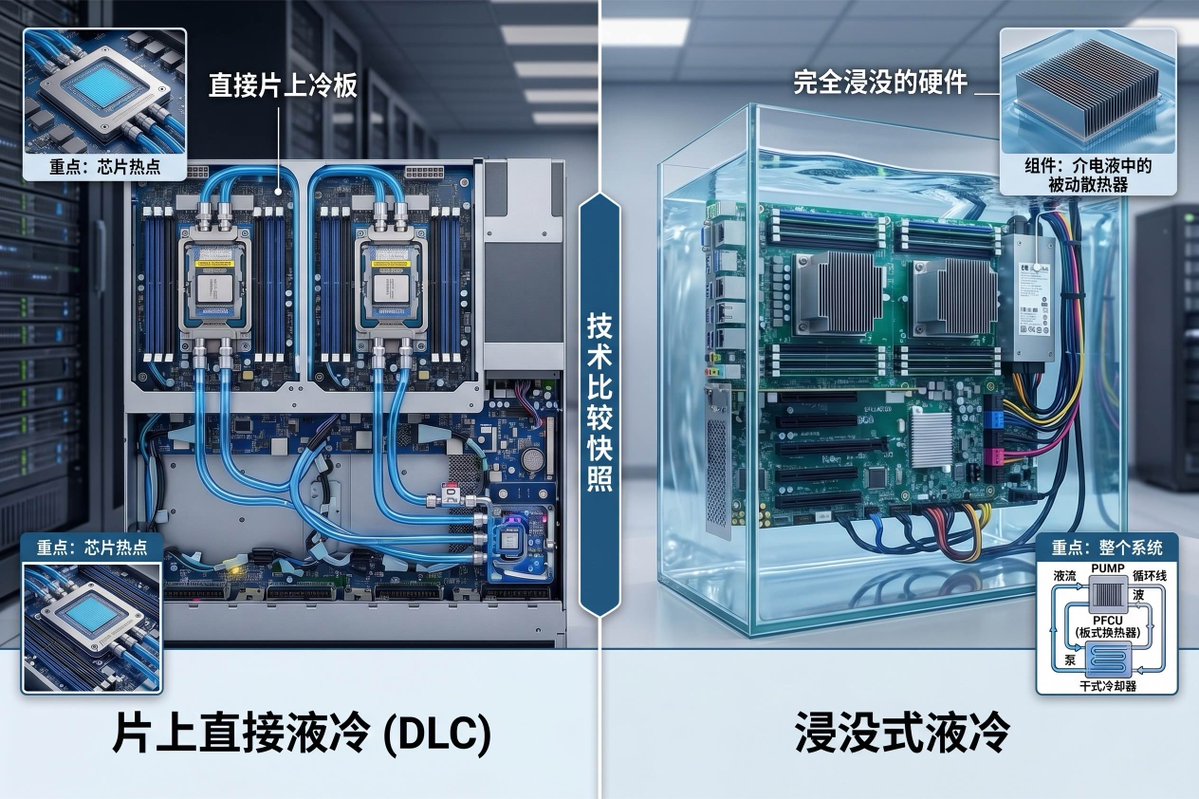

📊 Currently, the liquid cooling technology on the market is mainly divided into two camps: direct liquid cooling and immersion liquid cooling.

In direct liquid cooling technology, the cooling liquid flows through closed pipes attached to the copper cold plates on the surface of chips, without directly contacting electronic components. The dispersion efficiency is relatively high, easily handling single cabinet densities of 100KW+. Furthermore, it is compatible with existing air-cooled data centers and standard server racks. It is the mainstream solution in the market today, including Nvidia's Blackwell, which adopts this solution.

In immersion liquid cooling technology, servers are completely immersed in a non-conductive dielectric fluid, with the liquid dissipating heat through natural convection or pump circulation (this scheme, we tried back in the ETH mining days by immersing GPUs in silicone oil, and the cooling effect was great, but it occupies a lot of space). Theoretically, this is the best cooling solution, especially when immersed in fluorinated fluids, which can easily handle 200KW of single cabinet density. However, it has poor compatibility, requiring major renovations to data centers, and unique bespoke tanks and pipeline designs must be completely rebuilt. Moreover, maintenance costs are relatively high, making it a niche non-mainstream solution.

From the supply chain logic perspective, the AI data center liquid cooling supply chain is relatively simple compared to optical modules, mainly covering from the most basic chemical liquids, precision pumps and valves, cold plates, to system-level cooling distribution units (CDU) and outer water treatment infrastructure.

Next, let's discuss the core companies and investment logic in detail:

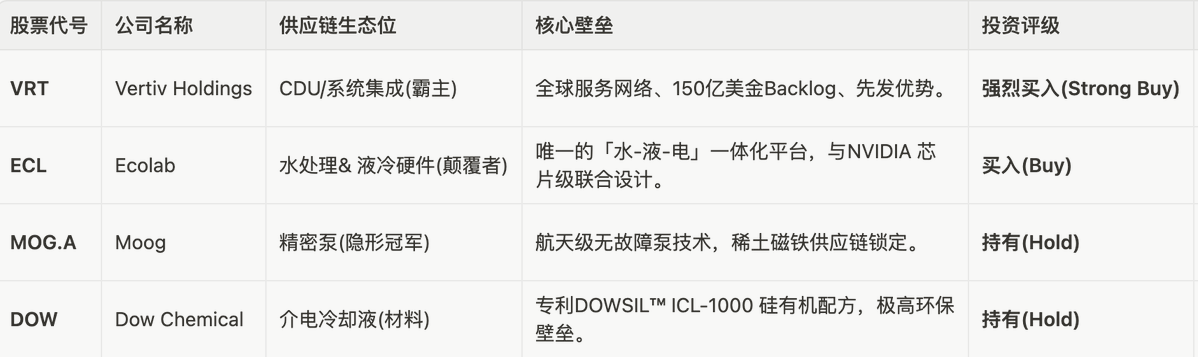

1️⃣ Vertiv Holdings (Stock code #VRT): The absolute leader in the liquid cooling field

Vertiv is the purest and largest provider of data center physical infrastructure in the US stock market, primarily engaged in power and thermal management. In the era of liquid cooling, Vertiv has built an almost unbreakable moat.

• Unreplaceable global service network: The biggest difference between liquid cooling and air cooling is that liquid leakage is catastrophic. For hyperscale customers like Meta and Microsoft, when choosing a liquid cooling supplier, the primary consideration is not hardware price, but "who can send an engineer to the site within 15 minutes when the system experiences minor leakage." Vertiv has over 3,000 technical service engineers stationed in data centers around the world, and this scale of service network is something any new entrant or server OEM could not replicate in the next 5-10 years.

• Amazing order backlog and visibility: As of Q1 2026, Vertiv's order backlog reached a record 15 billion dollars, a year-on-year increase of 109%. Its order-to-shipment ratio is as high as 2.9, which means Vertiv has locked down revenue for the next several years, and the backlog is expanding as the next-generation Nvidia Rubin enters production.

• Financials and valuation: Revenue reached 2.65 billion dollars in Q1 2026, and adjusted diluted EPS surged 83% year-on-year. Management raised the 2026 full-year EPS guidance to $5.97-6.07, implying a 51% growth. Although the forward P/E is currently at 46 times, relative to its 43% EPS compound growth rate, its PEG is only 1.07, making it even more attractive on a growth-adjusted basis compared to the S&P 500 index.

2️⃣ Ecolab (Stock code #ECL): The ultimate integrator of "water-liquid-electric" through the acquisition of CoolIT

Ecolab is originally a global giant in water treatment and industrial hygiene with a market cap of 77 billion dollars. However, in March 2026, it made a shocking decision that stunned Wall Street: it acquired the global leader in liquid cooling hardware, CoolIT Systems, for 4.75 billion dollars in all cash.

• A staggering premium of 29 times EBITDA: Ecolab paid as much as 29 times forward EBITDA as consideration. At the time, the entire Wall Street analyst community was shocked; many could not understand how a utility company could venture into AI liquid cooling. However, the market later understood that this integration had a terrifying aspect: liquid cooling had essentially transitioned from a hardware business to a business focused on chemical and fluid lifecycle management.

• The only exclusive platform for "cooling as a service": Ecolab deeply integrated CoolIT's chip-level hardware (CDU, cold plates, manifolds) with its own 3D TRASAR™ water quality digital monitoring, chemical corrosion prevention and scale control technologies, as well as its global industrial water treatment network.

• Personal understanding: In the past, hyperscale customers needed to procure cold plates from CoolIT, CDUs from Vertiv, and once-through water treatment services from Ecolab. If pipeline corrosion, scaling or coolant degradation occurred, suppliers easily shifted responsibility. After Ecolab acquired CoolIT, it became the only global supplier capable of providing end-to-end fluid lifecycle management from "chip-level microchannels" to "cooling towers outside the plant." This one-stop solution capability has a strong customer lock-in effect, and once cooperation occurs, the replacement costs are significant.

• Exclusive partnership with NVIDIA: CoolIT is a core member of the NVIDIA Partner Network, and its OMNI cold plate is a result of co-engineering for the NVIDIA GB200/GB300 chips. After Ecolab acquired CoolIT, it directly inherited this highly scarce chip-level design entry, doubling its addressable market from 5 billion dollars to 10 billion dollars, while the company's water treatment business itself provides a steady cash flow.

🧐 Next, let's discuss the "invisible champions" and scarce component suppliers in the liquid cooling supply chain. They hold the core supply chain of liquid cooling and are indispensable!

3️⃣ Precision power source: Moog (Stock code #MOG.A), market cap 10 billion

The CDU and pump in the liquid cooling system must ensure 100,000 hours of failure-free operation; even the slightest vibration or electromagnetic interference could damage the server.

• Uniqueness: Moog, with its precision servo control technology in the aerospace sector, is the almost exclusive designated choice for high-performance CDUs with its CoreMotion™ liquid cooling distribution pump.

• Supply chain lock-in: Moog signed an exclusive memorandum with USA Rare Earth, ensuring stable supply of high-performance neodymium-iron-boron rare earth permanent magnets for pumps, creating a high raw material barrier in a politically volatile environment in 2026, but rare earth materials ultimately still depend on China's policies.

4️⃣ Core heat exchange medium: Dow Chemical (Stock code #DOW), market cap 25 billion

The chemical formulation of the coolant is the core of immersion liquid cooling.

• Dow's exclusive weapon: Dow Chemical launched the patented DOWSIL™ ICL-1000 silicone organic coolant, which has won the R&D 100 award. Its heat transfer efficiency is 1,000 times that of air, can reduce server cooling energy consumption by 95%, and possesses an extremely low global warming potential value, complying with the EU and US's stringent environmental standards. The core issue is that Dow Chemical's scale in this area is not large and is not its main business line.

Stay tuned for the next issue discussing the power sector! 🧐

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。