Author: Ben Lakoff

Translation: Deep Tide TechFlow

Deep Tide Intro: As the founder of Bankless liquidates his ETH and 19-year-old developers flock to Solana, the bearish narrative around Ethereum has become a consensus. But BanklessVC partner Ben Lakoff believes this mirrors the “Ballmer era” of Microsoft — where the surface narrative is bearish, but the underlying fundamentals are growing steadily. A 30% staking rate, ETF accumulation, and clearer regulations are compressing the circulating supply, while crypto regulations transitioning from a survival threat to a legal framework is precisely when one should enter the market.

Welcome to the May trading flow summary.

This month's argumentative section is a bit longer, so I put it at the front, with all financing rounds, fund raisings, and hackathon results at the back.

Ethereum's Ballmer Era

Last month, David Hoffman liquidated all his ETH at $2070 and wrote a thoughtful article explaining why. This went viral on X (Twitter).

David then participated in the Chopping Block podcast, and I really enjoyed that conversation. Tarun said Ethereum is “stagnating” because no 19-year-olds want to build there. Max Resnick described the Ethereum Foundation as “risk-averse.” The bullish Haseeb coined a name for the entire bearish narrative: it’s Ethereum's Ballmer era. This phrase resonated with me.

This framework is too good to let slip away.

Yes, I am bullish on “crypto”, I am bullish on BTC, I am bullish on ETH… I am bullish on this trend. But pretending the bearish narrative is weak is just self-deception, so I want to elaborate further on my stance. These are my opinions and do not necessarily represent the views of BanklessVC and are certainly not investment advice.

The Bearish Narrative Has a Name, and It’s Correct

The substantive content is real. In fact, we have fallen another 10% since that article was published.

David’s argument: ETH as a currency is a long-term bet, and the rollup-centric roadmap makes it even longer. Ethereum is a “giver, not a taker” … it’s designed to distribute block space at cost. L2 profit margins are hitting 98% of blob revenue. Gas limits are gradually increasing to over 100 million. BPO forks are aggressively expanding blob supply. $3 billion to $163 billion in stablecoins has created value for Circle and Tether, not ETH. Meanwhile, SOL, NEAR, BNB, and TRX have already reset their valuations to fee-driven benchmarks. He is mechanically correct. The protocol is designed to have abundant block space, which is entirely at odds with the fee-driven value capture you want.

Tarun’s “stagnation” viewpoint is a cultural version of the same thing. Talent follows the founder’s energy, and right now that energy is on Solana, Monad, Hyperliquid, and whatever comes next (perhaps not on Ethereum, not on cryptocurrency). Resnick’s “risk-averse EF” is the institutional version. The foundation is focused on maintaining network integrity at a time when it needs to be competitive.

Haseeb is right. A “Ballmer era.” Slow product cadence. Botched transitions. Sharply competitive rivals with killer instincts. Loud critics who are right in their viewpoints.

What Microsoft Actually Paid During the Ballmer Era

Ballmer ran Microsoft from 2000 to 2014. The joke is: wasted 14 years. Missed mobile, missed search, missed social, released Vista, threw some chairs.

This is the joke I recall, but it misses something. Microsoft stock was flat for over a decade, while enterprise franchises were compounding ruthlessly in the background. Dividends did most of the heavy lifting. Office and Windows licensing printed money throughout the "Microsoft is dead" narrative. Then Satya took over, and MSFT shot up 10 times.

The lesson (at least in the Microsoft version) is that deeply integrated, enterprise-loved, time-tested infrastructure often continues to compound growth even within its own bearish narrative. The bearish narrative is often right on the surface. Just not enough to short.

Ethereum remains the largest trusted neutral public chain for tokenized assets. BUIDL is there. About 66% of USDC’s supply is there. The deepest DeFi liquidity is there.

But the lead is rapidly narrowing. BUIDL is not just on Ethereum (40%), down from about 85% a year ago. USDC exists across 34 chains. Western Union chose Solana over Ethereum for USDPT. Institutional default choice is shifting from the singular “Ethereum” to the plural “public chains.”

The incumbents are still bullish. Just not monopolized anymore. Whether 19-year-olds want to build there is a real long-term concern. But that's not what will decide the next two years.

Under the Noise: Circulating Supply is Collapsing

This is the part of the bearish narrative that mostly gets overlooked.

About 30% of ETH is staked. The treasury companies hold another 6% and are still growing. BitMine alone holds 4.47% of the supply and publicly aims for 5%. Spot ETFs continue to accumulate more. The SEC/CFTC ruling on March 17 classified staking rewards as non-securities, clearing the way for the entire staking ETF pipeline. Five more issuers (Fidelity, Franklin, Invesco, 21Shares, VanEck) have staking amendment decisions pending for Q2.

Every ETH staked through an ETF is ETH that cannot be sold off in a price surge. Net issuance is about 0.23% annualized. The rate of circulation contraction is faster than this, with these receiving entities competing on most days. Math does not care if ETH is boring.

So David is right, ETH will not be repriced because of fee destruction. The roadmap chose to be rich. But ETH can be repriced due to circulating supply compression, staking yield demand, and institutional Shearing Point premiums without needing to win the fee battle. At least in the short term.

The TAM for Cryptocurrency is Continuing to Rise

Zooming out from ETH. The real story over the past 12 months is that crypto regulation has transitioned from a survival threat to a legal framework.

The GENIUS Act has become law. Payment stablecoins now have a federal framework. The CLARITY Act passed the House last July and is structurally likely to pass the Senate Banking Committee on May 14, potentially ahead of midterm elections. Stablecoin circulation exceeds $280 billion and is compounding. Tokenized Treasuries are scaling. Spot ETFs exist across an increasing number of assets.

This is not a phase of cryptocurrency’s demise. It’s a phase of cryptocurrency becoming a regulated, trillion-dollar slice of the financial system, with boring institutions mandated to connect.

In previous bear markets, we genuinely worried whether this ecosystem would exist in the future. However, there are some warnings, and they are significant.

First: Winning in cryptocurrency and winning in decentralized cryptocurrency are not the same thing. The truly scary bearish scenario is not David’s fee math. It’s that “blockchain wins” ultimately looks like licensed ledgers from Canton, JPM Onyx, DTCC, and a few Avalanche subnets, with the public crypto asset complex basically not capturing real value.

That world exists (and is concerning), but I would bet on the public chain side for several reasons. Purely permissioned chains as institutional answers have been pitched for a decade, yet continue to lose adoption (maybe this time is different?). The truly winning architecture is permissioned assets on public chain tracks: BUIDL, BENJI, Ondo's USDY. Tokens execute KYC and transfer restrictions; settlements run on Ethereum, Solana, and other public infrastructure. The empirical record of KYC pools existing alongside open public pools (Aave Arc, Compound Treasury) shows that they fail.

This remains bullish for public chains as settlement layers, including ETH. But it's weaker than full DeFi composability. Permissioned assets cannot freely combine with open pools, but gated access versions are the winning model.

Second: The question is no longer whether cryptocurrency adoption will occur. It's which cryptocurrency will capture it. The honest answer is, not all will flow to ETH, but a massive, regulated, “needs trustworthy neutrality” segment will almost certainly do so. Because the alternative is requiring tier one banks to operate on-chain for tokenized asset settlement like startups… unlikely.

This is where the Ballmer framework underestimates the bull market. It only works when the underlying market continues to grow. The underlying market for cryptocurrency is rapidly growing in the most regulatorily blessed, institutionalized way.

Barbell Strategy: Bullish on Trends, Not Extremism

The bearish narrative I take seriously is not the fee analysis. It’s leadership and competition. The EF may indeed need its Satya moment. The killer instinct vacuum is real. Solana, Monad, and Hyperliquid are not slowing down. ETH/BTC and ETH/SOL could trade sideways or dip for some time before turning.

The positioning around this is simple: stop being extremists.

Hold ETH as a time-tested/institutional/circulating supply compression trade. Hold SOL as a consumer/throughput/distribution trade. Hold BTC as a macro hedge. Hold a small basket of next-gen L1 and application layer winners, where the cultural energy is really flowing.

I know. ETH is a $250 billion asset, influenced by macro trends, and there’s always a trade-off on where you put your funds. I’m not an extremist, but I’m still bullish on ETH. To summarize the reasons:

The rate of circulating supply contraction is faster than issuance.

Q2 staking ETF approval is a real-time, dated catalyst.

The CLARITY Act passing releases institutional cryptocurrency widely. Clearer rules allow regulated capital to deploy across the asset class at scale. ETH's moat is its incumbency network effects plus trustworthy neutrality, making it the default public chain settlement layer for tokenized assets, even as the lead narrows.

The bearish narrative is so loud that it has now become consensus. The historical hit rate of consensus bearish narratives after a 60% drawdown from $2000 is quite low.

The option value of a “Satya moment” is not priced in. If the EF gets reorganized or a more aggressive entity emerges to lead protocol development, that’s pure upside space not included in any bearish model.

I think of this trade as “David is partially right and ETH still matters.” Microsoft operated effectively under Ballmer. Cryptocurrency adoption is winning. The asset you most want to own is the one most deeply embedded in the part of cryptocurrency where the US government just spent two years writing the rules.

Step back and look at what regulators are actually saying. The SEC and CFTC are telling you they want to rebuild finance on-chain. Moving dollars on-chain. In that world, how could it not be massively bullish? Maybe if you are a crypto punk, this isn’t the world you envision… gated assets, KYC tracks, everything needing permission. But for public chains as settlement infrastructure? Undoubtedly bullish.

This is the key to where we are in the cycle. AI is the center of attention, period. It’s hot, parabolic, and as an early investor, that’s precisely the issue. You want to deploy capital where it’s not hot. When a sector is so overheated, it’s hard to put capital in without overpaying, except for the very earliest seed pre-stage.

Cryptocurrency, right now, is not hot. The bearish narrative is consensus. Energy is elsewhere. That’s the setup you want, not the one you want to flee from.

On a long enough time horizon, everything turns into AI, everything turns into blockchain. Pricing one of these as if it has already happened. The other just gained a two-year lead with written law while everyone is looking elsewhere.

Buckle up. Now turning to the rest of the cryptocurrency/web3 financing:)

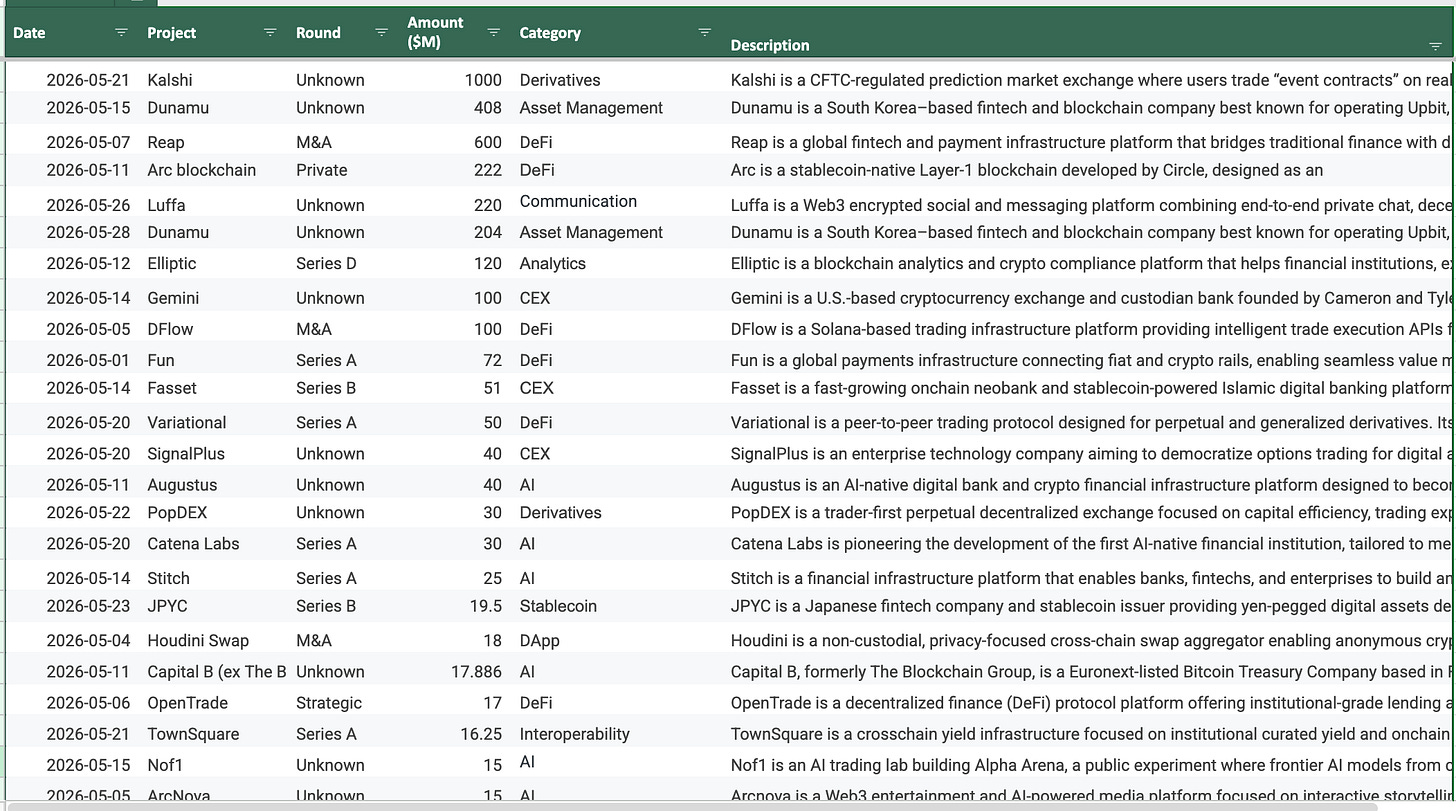

Top Ten Cryptocurrency Financing Rounds

Kalshi | Series F | Prediction Market | $1 billion | 2026-05-07

Coatue led, with participation from Sequoia, a16z, IVP, Paradigm, Morgan Stanley, and ARK Invest. This $1 billion financing round values Kalshi at $22 billion, double the $11 billion valuation just five months ago. Annualized trading volume tripled to $178 billion in six months, with institutional trading volume up 800%. Kalshi is regulated by the CFTC rather than being crypto-native, so consider this an asterisk on this list, but it now commands over 90% of US prediction market activity, which is one of the cleanest entry stories currently held by cryptocurrency.

Dunamu (Upbit) | Strategic Investment | Centralized Exchange | $408 million | 2026-05-28

Three Samsung-affiliated companies (Samsung Securities, Samsung SDS, Samsung Card) agreed to purchase a 4% stake in Dunamu, the operator of Korea's largest cryptocurrency exchange, Upbit, from Kakao for approximately $408 million (612.8 billion Korean won). Each buyer mentioned positioning for a won-pegged stablecoin, tokenized securities, and on-chain settlement ahead of Korea’s Digital Assets Basic Act. This is part of a May sprint, transferring about 14% of Dunamu’s shares to Korean giants like Hana and Hanwha. Completion by June 19.

Circle (Arc) | Token Pre-sale | Infrastructure/Stability | $222 million | 2026-05-11

Circle raised $222 million for Arc (FDV at $3 billion), which is its L1 for stablecoin settlement and tokenized assets. a16z crypto invested $75 million, with participation from BlackRock, Apollo, ICE, Standard Chartered Ventures, SBI, Janus Henderson, General Catalyst, Marshall Wace, ARK, Haun, and Bullish. This is the clearest signal of 2026 that “traditional finance is choosing a track.” A regulated stablecoin issuer is building its own chain, with the biggest asset management firms on the shareholder list.

Ripple (Ripple Prime) | Debt Financing | Infrastructure/Prime Brokerage | $200 million | 2026-05-11

Ripple secured $200 million in debt financing from funds managed by Neuberger Specialty Finance to expand its lending capacity for its multi-asset prime brokerage, Ripple Prime. Existing institutional loans serve as collateral. Since Ripple acquired the platform in 2025, Ripple Prime’s revenue has tripled year-on-year. Traditional financial credit backs the loan book of cryptocurrency prime brokers.

Elliptic | Series D | Compliance/AI x Crypto | $120 million | 2026-05-12

One Peak led this $120 million round of financing (valuation at $670 million), with Nasdaq Ventures, Deutsche Bank, and British Business Bank participating. This is the largest pure equity venture capital round of the month. Elliptic is building agency-style AML/compliance tools. From the perspective following April: this is the operational and compliance layer that DeFi has been constantly reminded it needs, now backed by traditional financial capital.

Fun | Series A | Payment/Consumer | $72 million | 2026-05-01

Multicoin Capital and SignalFire jointly led, with participation from Infinity Ventures, Pharsalus Capital, and Justin Mateen. Fun is a crypto/fiat on-ramp providing support for financial platforms like Polymarket. This is the largest consumer/payment venture capital round of the month, representing a clean bet on the predictive markets and consumer crypto hype tracks.

Fasset | Series B | Stablecoin/Payments | $51 million | May 14, 2026

SBI Group led this $51 million financing round, with participation from Investcorp and Arz Portföy. Fasset is a stablecoin-driven neobank targeting emerging markets, with an annualized trading volume of about $32 billion. This is real proof of the assertion that stablecoins are a means of payment, and it’s happening in the most vital places: corners of the world where dollar tracks truly change lives.

Variational | Series A | DeFi/Derivatives/RWA | $50 million | 2026-05-20

Dragonfly led, with participation from Bain Capital Crypto and Coinbase Ventures. Variational operates a platform based on the RFQ model, providing on-chain perpetual contracts for real-world assets: oil, gold, silver, copper. The team’s judgment is that RWA perpetual contracts may surpass BTC and ETH perpetual contracts within a year. This is the deepest argument of the month for small trades.

OpenTrade | Strategic/Growth Round | Stablecoin/RWA | $17 million | 2026-05-06

Mercury Fund and Notion Capital support OpenTrade’s $17 million financing, aiming to expand its yield infrastructure supported by real-world assets-backed stablecoins. This is another data point reflecting the dominant theme of the month: yield-bearing stablecoin tracks backed by RWA collateral.

Cycles | Seed Round | Infrastructure/Clearing | $6.4 million | 2026-05-21

Blockchange Ventures led, with participation from Coinbase Ventures, Compound VC, and Primitive Ventures. Cycles is building a privacy-protecting multilateral clearing network for on-chain finance and stablecoins. While small, this is the type of institutional-grade pipeline that must exist before the “next $10 trillion influx” story comes true.

Click here to see all financing rounds from May

May Cryptocurrency VC Fundraising Announcements

After a busy April, this month’s new fund announcements have been relatively quiet, but there are two major moves...

Haun Ventures | Phase II Fund $1 billion | May 2026

Katie Haun’s firm raised $1 billion through early-stage funds and later companion funds, bringing the total assets under management to over $2 billion. Three central priority themes: next-gen financial infrastructure, asset tokenization, and new markets, as well as the “agent economy” where AI systems represent humans in trading. Funds will be deployed over the next 2-3 years.

a16z crypto | Crypto Fund Phase 5 $2.2 billion | May 2026

Our fund, marked in March at about a $2 billion target, formally closed at $2.2 billion. Full phase, 10-year investment horizon, focusing on practical applications: stablecoins, payments, financial services, perpetual contracts, lending, prediction markets, asset tokenization. a16z states that the fundamentals of cryptocurrency are “at an all-time historical high.”

Reminder, if you are interested in learning more about Bankless Ventures Phase II Fund, please fill out this form, and we will get in touch with you!

ETHGlobal New York 2026 | June 12-14, 2026

New York City, offline event. Previously there was ETHConf NYC (June 8-10) and Pragma NYC.

Base Onchain Summer Hackathon | Around June 2026 (date TBD)

Online event. Base’s flagship on-chain hackathon; the last round attracted over 7,500 developers, with sponsors including Stripe, Shopify, Farcaster, and Zora. (2026 date has yet to be confirmed, please verify on Devfolio.)

ETHGlobal Lisbon 2026 | July 24-26, 2026

Lisbon, Portugal, offline event. Pragma Lisbon on July 25.

Solana Frontier Hackathon | April 6 to May 11, 2026

Online event. The largest entrepreneurial competition in cryptocurrency, with around 2,857 submissions over five weeks. Awards: $30,000 total champion, 20 outstanding teams of $10,000 each, plus $2.5 million in venture capital and accelerator admission eligibility provided by Colosseum. Winners have yet to be announced by the end of the month; judging is in process, so please check back in early to mid-June at blog.colosseum.com.

ETHPrague 2026 | May 8-10, 2026

Prague, Czech Republic (City Hall). The fifth edition; conference plus hackathon, focusing on Ethereum's "solar punk" future.

Solana Mobile Hackathon | April 2026

Online event. Completed, with developers from 66 countries submitting over 400 applications.

Solana Frontier Demo Day | June 2026 (date TBD)

Online event. The final presentations from Frontier hackathon teams, expected to be held after the announcement of the winners.

ETHGlobal New York Demo Day | June 14, 2026

New York City. Project reviews and presentations on the last day of hackathon.

ETHPrague 2026 Closing Demo | May 10, 2026

Prague. Presentations and reviews on the last day of ETHPrague hackathon.

Open Accelerator Applications

Solana Incubator (Phase 5) | Open Applications/Early Deadline around June 5

New York City. A 3-month program starting in September 2026; rolling reviews, early applicants prioritized. Looking for 4-6 teams (existing Solana teams, web3 teams considering Solana, or web2 teams adding web3).

Alliance DAO (ALL18) | Open Applications/Rolling Reviews

Virtual plus offline retreat. ALL18 phase starts September 7, 2026; interview decisions will be made within about 2 weeks after application. About 5% acceptance rate; median funding for graduates is $3.5 million, valuation $25 million.

a16z Crypto Startup Accelerator (CSX) | Open Applications (verify next phase)

Offline, 9-week program, held twice a year in different cities. $500,000 for 7% equity; about 3% acceptance rate.

Outlier Ventures Base Camp | Rolling Applications

Virtual plus offline. A 12-week accelerator, accepting early applications in 2026 DeAI, DeFi, RWA, and DePIN directions.

Techstars Web3 | Open Applications

Virtual plus offline. Applications are reportedly open for 2026.

That concludes the May summary!

Thank you all, good luck!

Ben Lakoff, CFA

https://twitter.com/benlakoff

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。