Author: Rhythm

On June 3, the USD/JPY touched 160.44 during intraday trading, marking a new high since July 2024. On the same day, the Nikkei 225 index broke through 68,000 for the first time, reaching a peak of 68,634.74. With these two numbers combined, a familiar narrative appeared in the market: "the carry trade is about to collapse, repeating what happened in August 2024."

This narrative is half correct. The other half tells a completely different story.

Bears are not retreating, but rather increasing their positions

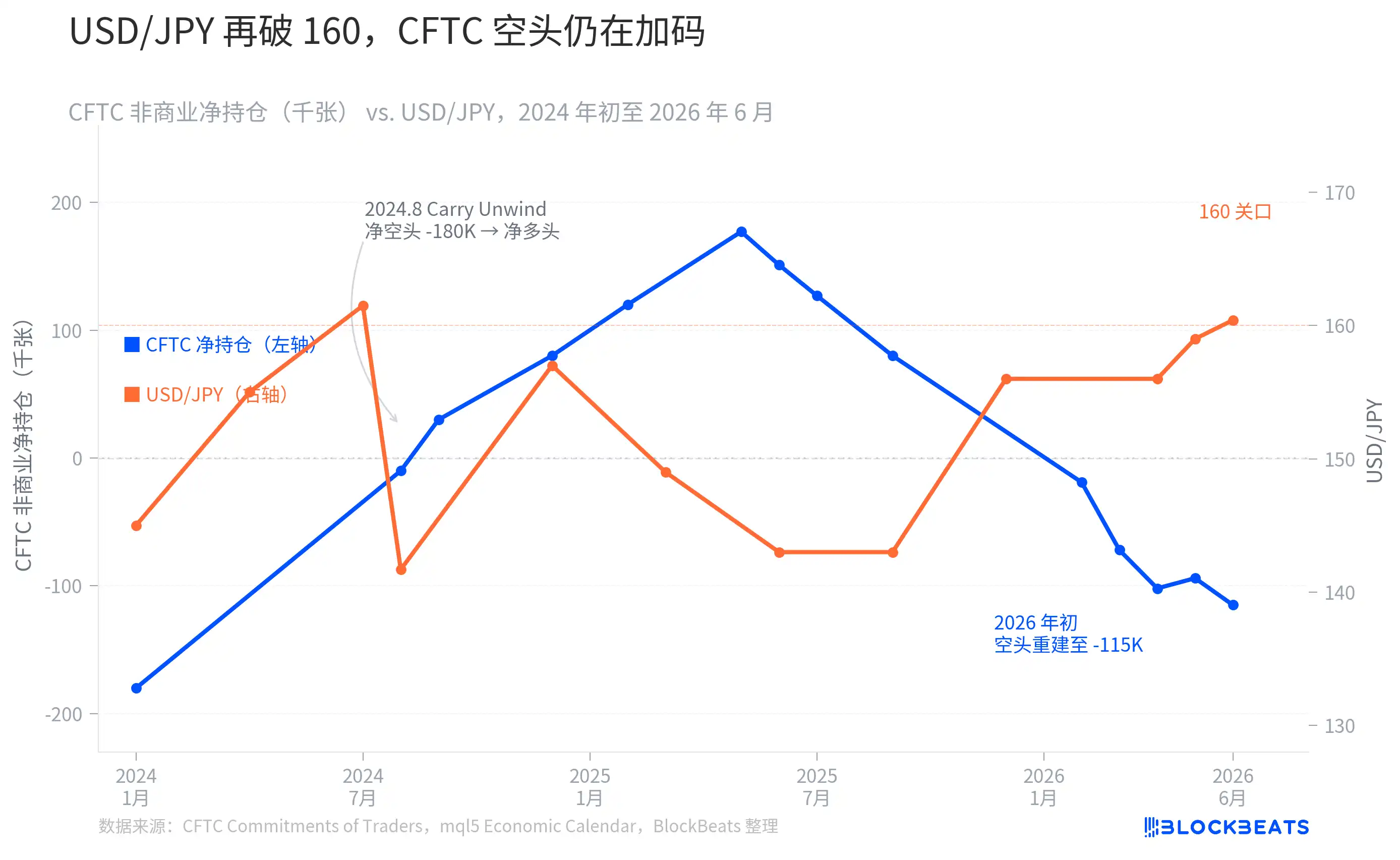

The most direct indicator of the crowding in yen carry trades is the weekly CFTC (Commodity Futures Trading Commission) non-commercial positioning report. It records the net long or net short positions of speculative traders in the yen futures market.

According to the CFTC positioning report, for the week ending May 26, non-commercial accounts had a net short position in yen futures of 114,667 contracts——long positions at 112,993 and short positions at 227,660. Compared to the previous week, the net short position increased by 27,152 contracts.

From the chart, one can see a somewhat counterintuitive trend. In July 2024, when USD/JPY reached its peak near 161, the CFTC net short positions were at the historical extreme range of about -180,000 contracts. Shortly after, at the beginning of August, the Bank of Japan (BOJ) unexpectedly raised interest rates, combined with the US non-farm data coming in significantly below expectations, causing yen bears to be forced to cover their positions within just a few weeks; the net short position contracted sharply from about -180,000 contracts to more than +177,000 contracts by the second quarter of 2025——the carry trade indeed experienced systemic short squeezes during that period.

However, the subsequent trend was completely opposite to the "squeeze narrative." Starting from the end of 2025, net short positions in yen accumulated again, turning negative in February 2026 and rapidly expanding to -102,000 contracts in April. By May 26, net shorts had reached -114,667 contracts. When USD/JPY returned to around 160, global speculative funds were not fleeing but rather continuing to increase their positions.

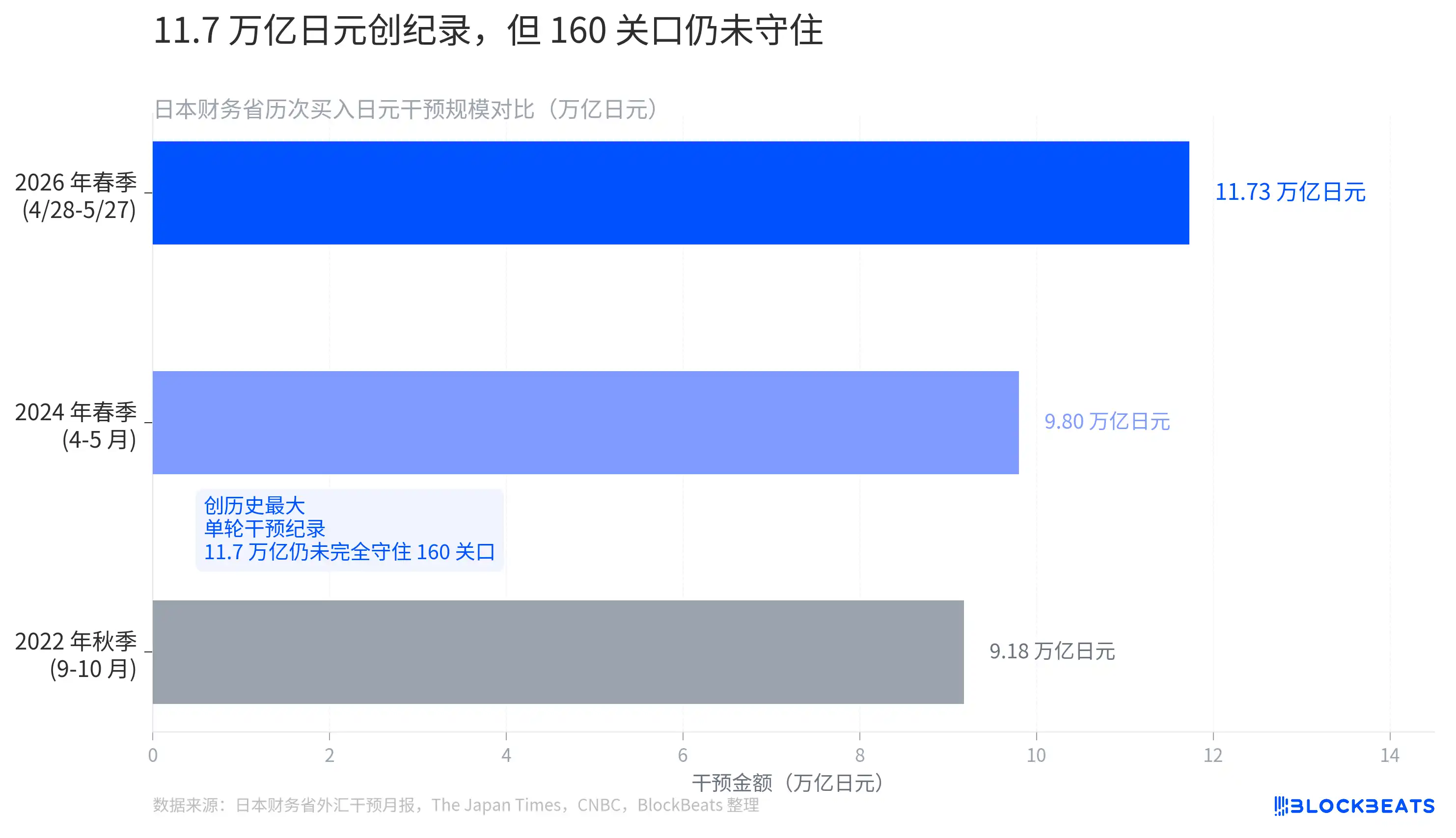

This means that if the BOJ sends out a more hawkish signal in its July meeting, or if US economic data weakens again unexpectedly, these -114,667 contracts of net shorts will face passive liquidation pressures reminiscent of August 2024. The Japanese Ministry of Finance is also aware of this——from April 28 to May 27, the ministry used a record 11.7349 trillion yen to buy yen and sell foreign exchange in an attempt to suppress the shorts.

The largest single-round intervention failed to maintain 160

The Japanese Ministry of Finance's history of foreign exchange intervention dates back to 1998. In the fall of 2022, when the yen fell to around 152, the ministry conducted its first "buy yen" operation since 1998: in September, it spent 2.84 trillion yen, followed by an additional 6.34 trillion yen in October, totaling approximately 9.18 trillion yen. That round of intervention briefly pushed USD/JPY back from 152 to around 127, but the effect lasted only a few months.

In the spring of 2024, when USD/JPY again approached 160 and briefly surpassed it, the ministry intervened with about 9.80 trillion yen, marking the largest single-round operation since 2022 and the "first confirmed buying intervention since 2022."

According to the monthly intervention data released by the Japanese Ministry of Finance on May 29, 2026, the scale of the operation from April 28 to May 27 was 11.7349 trillion yen (approximately 73.6 billion USD), making it the largest single-round intervention on record, exceeding the total amount of interventions in 2022 and nearly 2 trillion yen more than the spring of 2024.

However, less than a week after the ministry disclosed the figures, USD/JPY still broke back above the 160 mark. The largest scale of intervention failed to fully maintain this psychological threshold.

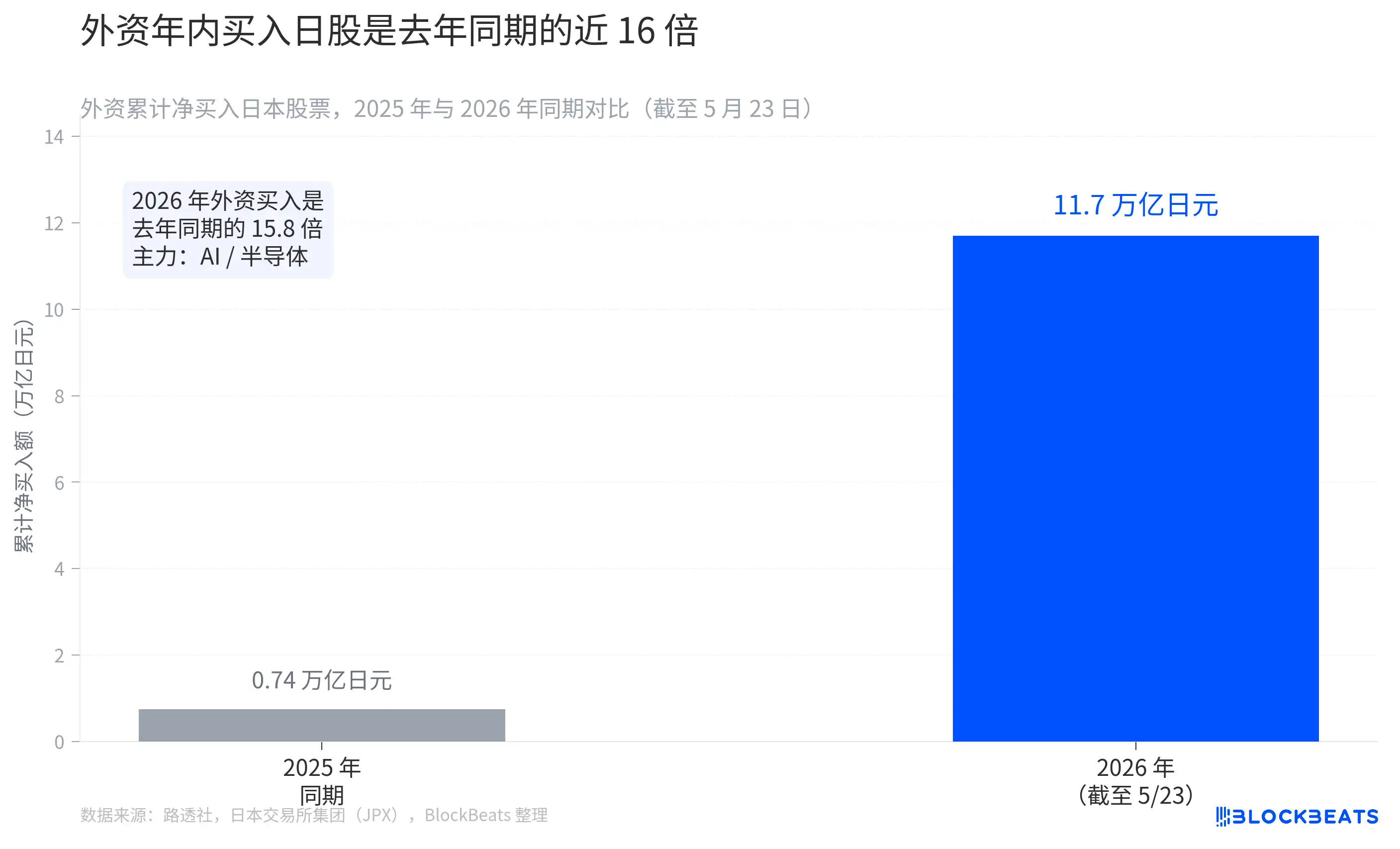

Foreign capital is buying Japanese stocks, chasing AI, not safe-haven funds from carry liquidations

If the carry trade is still crowded, why is the Nikkei 225 still reaching new highs?

According to Reuters citing data from the Japan Exchange Group (JPX), for the week ending May 23, overseas investors have net bought Japanese stocks for eight consecutive weeks, with a weekly net purchase reaching 1.08 trillion yen. The cumulative net purchase for the year is approaching 11.7 trillion yen.

During the same period in 2025, foreign capital's cumulative net purchases were only 742.1 billion yen. In 2026, this figure is 15.8 times that.

The direction of this funding is very concentrated. Among the individual stocks that saw significant price increases during the same period, AI investment platform SoftBank Group rose by 17.62% in a week, while chip designer Socionext increased by 12.26%. Reuters’ report directly explains the purchase motivation: Nvidia's (Nvidia) performance outlook has boosted expectations for AI and semiconductor demand, with foreign capital leveraging the Japanese market to chase this main line.

This is in stark contrast to the logic of "carry unwind triggering sell-offs" in August 2024. That instance involved forced position reductions and indiscriminate selling, with funds fleeing the Japanese market. In contrast, the net purchases by foreign capital in 2026 indicate an active choice to enter the Japanese market to chase AI-induced reflation. The driving mechanisms behind these two scenarios are different, leading to different implications for the Nikkei index.

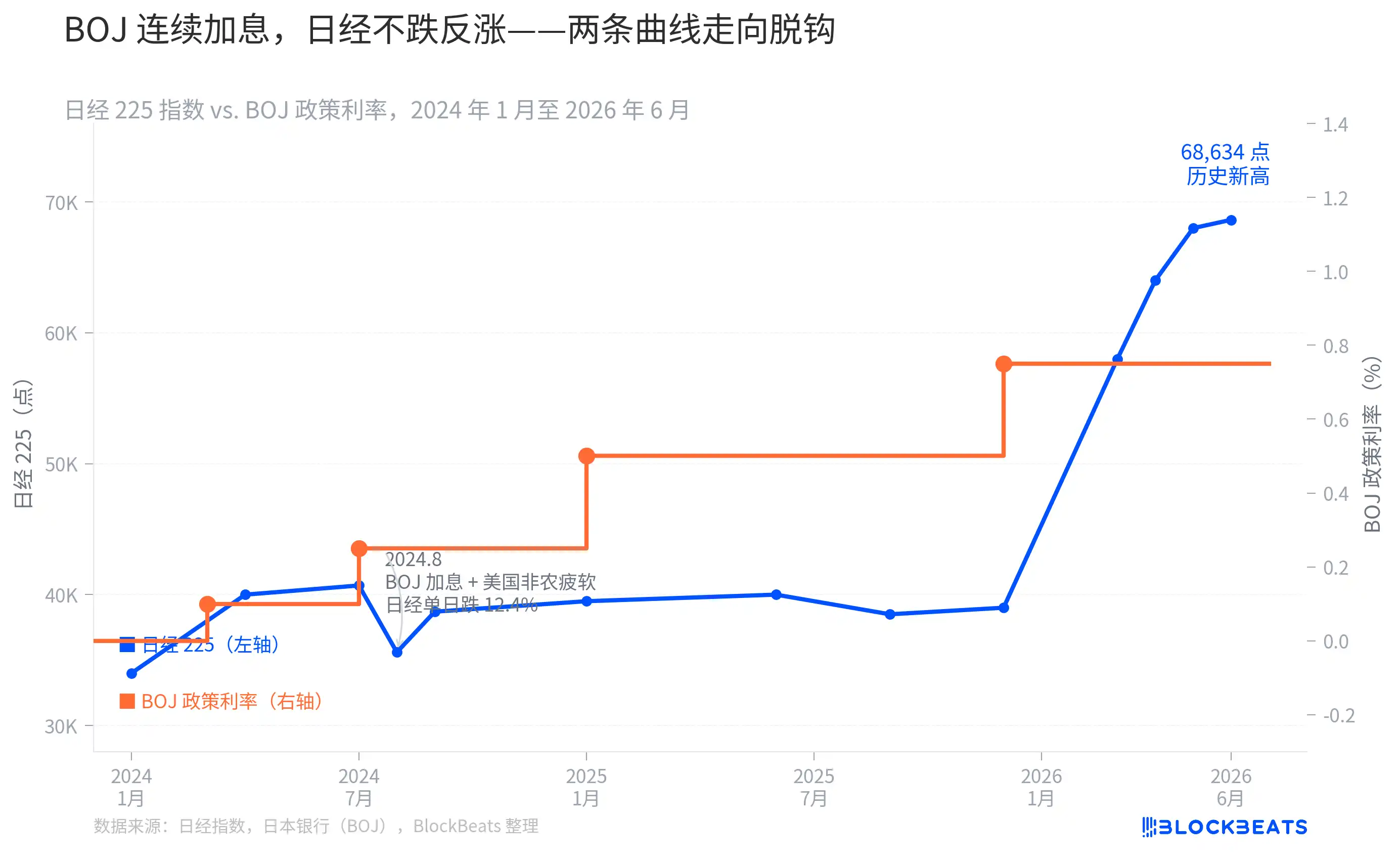

Rate hikes do not press down the stock market, but this relationship is becoming more fragile

Another counterintuitive aspect of the Nikkei 225 is its continued rise in the context of the BOJ's consecutive rate hikes.

According to the BOJ's announcements of its policy decisions over the past two years, the rate hike path is as follows: In March 2024, it ended the negative interest rate policy, raising the policy rate from -0.1% to 0.1%; in July 2024, it raised rates again to 0.25%; in January 2025, it increased to 0.5%; and in December 2025, it rose to 0.75%, the highest level since 1995. In April 2026, the meeting maintained the rate at 0.75%, with a 6 to 3 vote——three members (Hajime Takata, Naoki Tamura, and Junko Nakagawa) explicitly advocated raising rates to 1.0%.

From the chart, it is clear that the correlation between rate hike points and Japanese stock trends varies significantly at different stages. The rate hike in July 2024 triggered a historic drop of 12.4% in the Nikkei 225——this was due to the simultaneous impact of the BOJ's rate hike and US non-farm data, which directly ignited a carry unwind. However, the two rate hikes in January and December 2025 were accompanied by the Nikkei 225 climbing from around 40,000 points to the current new high of 68,634 points.

The reasons behind this are not complicated: when the logic for foreign capital to buy is chasing AI-induced reflation, rather than relying on low financing costs from yen, small rate hikes by the BOJ have a limited impact on this part of the capital. Of course, this relationship is not immutable——if the BOJ actually pushes rates to 1.0% in the July meeting, while the dollar weakens due to other factors, the funding costs of carry trades could rise sharply, and at that point, the direction of the two curves might couple again.

When putting these three charts together, one can derive a relatively complete cognitive framework: yen shorts remain crowded, the Ministry of Finance's historically largest intervention failed to maintain 160, but the driving force behind the new highs in Japanese stocks is AI-related foreign capital——all three things can be true simultaneously, are not contradictory, and none can individually predict what will happen next.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。