What is the core issue now? Is the truce of the Iran war merely providing absolute benefits to the technology sector, especially in the semiconductor field (SMH)?

Written by: Damir Tokic, Professor of Finance, Seeking Alpha Analyst

Led by technology stocks, the S&P 500 index is approaching historically high valuations, indicating that a massive bubble has formed. At the same time, the Iran war is likely to trigger inflation shocks, leading to skyrocketing oil prices and rising US Treasury yields, and the current situation seems to be escalating, significantly increasing the probability of this pessimistic forecast becoming a reality. Although the Federal Reserve currently maintains a dovish stance, the market has begun to price in interest rate hikes, so the Fed's hawkish shift in June is highly likely to become the catalyst for bursting this bubble.

President Trump attending the swearing-in ceremony of the new Federal Reserve Chairman

Is the truce agreement only favorable for tech stocks?

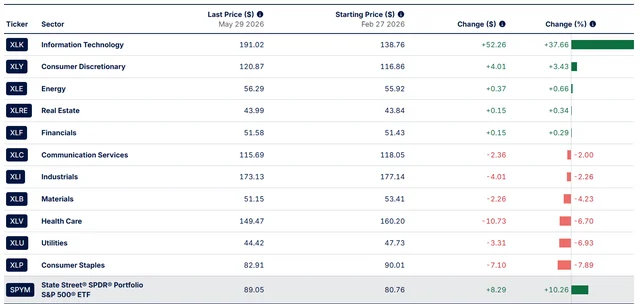

Here is the performance of the S&P 500 index (SPY) over the past three months since the outbreak of the Iran war:

- Since February 27, the S&P 500 index has risen by 10%.

- The technology sector (XLK) has increased by over 37%.

- Ranking second is the consumer discretionary sector (XLY), which has only risen by 3%. It is noteworthy that Amazon (AMZN) accounts for 27% of XLY's weight and its stock price has risen by 28%; Tesla (TSLA) accounts for 20% of XLY's weight and its stock price has risen by 8%. Both of these companies are essentially tech companies and are members of the "Tech Giants" (Mag 7).

So, what is the core issue now? Is the truce of the Iran war merely giving absolute benefits to the technology sector, especially to the semiconductor field (SMH)?

From my perspective, the answer is no. The market has previously blindly assumed that the war was over, and more importantly, believed that we could miraculously avoid the inflation shock and the subsequent economic recession that would damage demand. Therefore, this has become a green light for speculators to frantically hype and inflate the bubble again.

However, it must be pointed out that the current bubble is not the same as the internet bubble of 2000. The bubble of 2000 was entirely driven by expectations and the disorderly expansion of price-to-earnings (PE) multiples. The bubble of 2026 is much worse! It is built on "backward-looking" realized profits and naively expects these profits to continue indefinitely. Specifically, major mega-cap companies have splurged $770 billion on AI capital expenditures, and it is evident that these profits are concentrated among the core beneficiaries of this capital expenditure, primarily semiconductor companies like Micron Technology (MU).

However, the cyclically adjusted price-to-earnings ratio (Shiller P/E) of 2000 and 2026 is almost comparable, both staying above 40 times. This means that the severity of the 2026 bubble is already on par with that of 2000.

But, the profits of tech giants are not sustainable for cashing out. The growth of AI capital expenditures is likely to slow down and eventually decline. When will this inflection point occur?

In my view, this $770 billion AI capital expenditure can be traced back to the early days of Trump's second term when he met with tech executives. At that time, President Trump sat next to Zuckerberg and asked him how much Meta planned to spend on AI capital expenditures, to which Zuckerberg replied, "Sorry, I'm not ready yet... I'm not sure what number you're looking for."

Therefore, I believe this $770 billion AI capital expenditure is actually a "Trump stimulus plan" imposed on private enterprises, and it is unsustainable. If the Democrats win the upcoming midterm elections, this trend is likely to reverse.

Thus, the market's frenzied reaction after the Iran war truce is merely part of the "Trump stimulus plan," and it could very well be a final mad surge. The question now is, where is the peak of this surge? And what will trigger this crash?

SPY Performance by Sector (Data Source: SSGA.COM)

Escalation of Iran war and inflation shock

Now, let's turn our attention back to the Iran war. This is a crucial variable as it is very likely to trigger a classic systemic shock that would completely burst the bubble.

A classic bubble burst typically follows the following trajectory: 1) Intensified inflation, 2) Federal Reserve interest rate hikes, 3) Economic recession leading to a bear market.

Let’s first examine inflation. Inflation can be demand-driven or supply-driven.

Demand-driven inflation is initially favorable for the market because companies have pricing power, which usually accompanies an "overheated" economy, allowing companies to achieve revenue and profit growth in the initial phase. The Federal Reserve would then raise interest rates to suppress demand, but this ultimately leads to higher unemployment and results in an economic recession.

In contrast, supply-driven inflation is greatly detrimental to the market in the initial phase because companies lose pricing power—this usually occurs in environments of economic weakness or stagflation. The Federal Reserve is forced to raise interest rates in a situation where the economy is already weak, which will inevitably lead to a deeper recession.

The Iran war is triggering a destructive supply-driven inflation, as it causes a global energy shortage, and additionally, food shortages due to fertilizer shortages and many other derived products and chemicals.

Fundamentally, Iran has closed the Strait of Hormuz, and this closure has lasted for three months. During these three months, the global economy has been drawing from strategic oil reserves to fill the lost oil gap, and these reserves are expected to reach critical operational levels in June.

If Iran does not immediately reopen the Strait of Hormuz, the global economy will face the most severe energy shock in history. Due to the real and tangible physical shortage, crude oil prices could soar to over $200 a barrel until demand is completely destroyed, leading to a price drop. The destruction of demand directly corresponds to an economic recession.

For this reason, Trump is acutely aware of the severity of the situation. Over the past two months, he has been trying to negotiate with Iran to reopen the Strait of Hormuz, but to no avail.

Currently, reaching an agreement with Iran seems almost impossible for three reasons:

- First, Iran wants to maintain control over the Strait of Hormuz even after it is reopened, which crosses a red line for the United States;

- Second, Iran refuses to negotiate on nuclear issues and is highly unlikely to want to reach any nuclear agreement, which is another red line for the United States;

- Third, even if Trump compromises on Iran's conditions in order to reopen the strait and reaches some sort of agreement, Israel will intervene to prevent it because Israel views a nuclear-armed Iran as a matter of life and death.

So, what is the real situation now?

In my view, the possibility of Trump reaching an agreement with Iran at the last moment to prevent an inflation shock is becoming increasingly likely.

However, Israel absolutely does not agree with this agreement. Because part of the content of the Iran agreement is that all fronts must cease fire, including Lebanon. Israel could completely veto this agreement by directly attacking Lebanon. This is a matter of life and death for Israel, given that Hezbollah is a real threat.

Currently, we are facing a potential significant escalation.

Reports indicate that Iran has canceled all contact with the United States, meaning that all negotiations have come to a standstill. Moreover, Iran has completely sealed off the Strait of Hormuz and threatens to further close the Mandeb Strait. Should this happen, over 30% of the global energy supply will evaporate directly—this would be like a real disaster.

Although Trump claims he has been in dialogue with Israel and Hezbollah, and even states that negotiations with Iran are ongoing, these assertions alone are enough to push the tech sector to historical highs. However, to date, these claims have not received any official confirmation.

June Crash

Therefore, the likelihood of a crash occurring in June is becoming increasingly high. Global oil inventories will reach critical levels in June, and once they fall below that level, crude oil (CL1:COM) prices will skyrocket due to real supply shortages, at which point it will be very difficult to "talk down" oil prices just based on statements.

The result is that with rising inflation expectations and actual interest rates driven up by fiscal concerns, bond yields will soar. Additionally, when inflation surges, attempts to verbally intervene to "dissuade" the bond market from selling will also become futile.

Most importantly, the Federal Reserve must respond at the FOMC meeting in June. This is likely to become the final trigger to burst the bubble. Specifically, the Federal Reserve's officials still signal in the quarterly economic projections (SEP) that their next move will be a rate cut, maintaining a dovish policy stance.

However, the federal funds futures market has effectively priced in a tightening bias, with the market currently predicting a probability of over 50% for an interest rate hike once before December 2026, and possibly even two hikes.

At that time, the Federal Reserve will have to conform to market expectations and officially change its stance to hawkish in June's meeting. This alone could cause the bubble to burst instantly. Furthermore, even if the Federal Reserve insists on maintaining a dovish bias, the loss of market credibility could lead to a surge in ten-year Treasury yields, sparking a much larger systemic shock.

Investment Implications

The cyclically adjusted price-to-earnings ratio of the S&P 500 index is currently approaching a new historical high, far exceeding 40 times, thus forming a super bubble. The inflation shock triggered by the Iran war could burst it at any time, and the Federal Reserve's official tilt toward hawkishness in June might just be that fatal bullet. Investors should be prepared for a major pullback, the severity of which could rival that of the bear markets of 2000 and 2008. Remember, it is a bubble, and it will eventually burst.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。